Insomnia Drugs Market Size, Share & Industry Analysis, By Drug Class (Dual Orexin Receptor Antagonists (DORAs), Z-drugs/Non-Benzodiazepine Hypnotics, Benzodiazepine Hypnotics, Melatonin Pathway Agents, and Others), By Disease Indication (Primary Chronic Insomnia Disorder, Comorbid Psychiatric Insomnia, Comorbid Neurologic/Pain-Related Insomnia, & Others), By Age Group (Adults and Pediatric), By Type (Branded and Generic), By Route of Administration (Oral and Others), By Distribution Channel (Hospital pharmacies, Drug Stores & Retail Pharmacies, & Others), and Regional Forecast, 2026-2034

Insomnia Drugs Market Size and Future Outlook

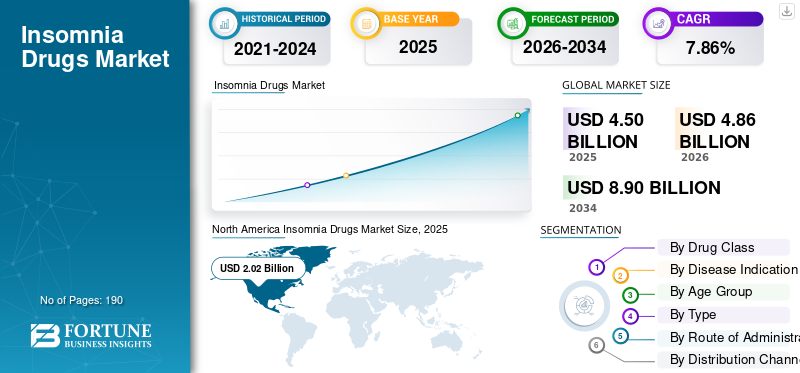

The global insomnia drugs market size was valued at USD 4.50 billion in 2025. The market is projected to grow from USD 4.86 billion in 2026 to USD 8.90 billion by 2034, exhibiting a CAGR of 7.86% during the forecast period. North America dominated the insomnia drugs market with a market share of 44.88% in 2025.

The global market is growing steadily as sleep disorders are becoming more prominent across aging populations. Rising stress levels, anxiety, depression, irregular work schedules, and lifestyle-related sleep disturbances are increasing the number of patients seeking medical treatment for insomnia. These factors have led to increased global market demand that improves both sleep onset and sleep maintenance, with better safety, tolerability, and next-day functioning. The market is also benefiting from continued innovation and expanding pipelines of candidates from key companies and emerging markets.

- For instance, in March 2026, Idorsia reported positive top-line results from its Phase 2 trial of daridorexant in children with insomnia disorder. The study reported clinically meaningful and statistically significant improvements across multiple sleep measures, showing that newer insomnia therapies are continuing to expand into additional patient groups beyond the traditional adult population. Such pipeline progress is expected to support product innovation and strengthen long-term growth opportunities in the overall market.

Furthermore, leading players in the industry, such as Eisai Co., Ltd., Idorsia Ltd, Merck & Co., Inc., and Takeda Pharmaceutical Company Limited, are focusing on research and development to strengthen their market positions.

Download Free sample to learn more about this report.

INSOMNIA DRUGS MARKET TRENDS

Growing Demand for Safer, Better-Tolerated Insomnia Therapies is an Emerging Market Trend

A key global market trend observed is the growing demand for safer and better-tolerated insomnia therapies. The rising demand is due to patients and healthcare providers becoming more cautious about traditional sleep medicines that may pose risks of residual sedation, impaired alertness, or long-term tolerability issues. As this concern increases, demand is shifting toward newer therapies designed to deliver sleep benefits with lower next-morning burden and a better overall treatment experience. This is pushing innovation toward mechanism-based drugs, especially orexin receptor antagonists, and is helping reshape prescription sleep patterns in the market.

- For instance, in April 2025, Idorsia reported that positive data with daridorexant in patients with chronic insomnia and nocturia had been published, and also noted new data assessing the transition from night to day in insomnia disorder. This reflects how market demand increasingly favors insomnia therapies positioned on efficacy, along with daytime functioning and tolerability, which supports this market trend.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Prevalence of Insomnia and Sleep Disorders Fueling Market Demand and Driving Growth

A major factor driving the global insomnia drugs market growth is the rising prevalence of insomnia and sleep disorders. A larger diagnosed and treatment-seeking patient base directly increases the need for effective insomnia medicines. As more people experience chronic sleep problems linked to stress, aging, depression, irregular schedules, and other health conditions, physicians are writing more prescriptions, and healthcare systems are paying greater attention to sleep health. This creates robust commercial demand for branded and novel insomnia drugs, which in turn supports product expansion, broader market penetration, and long-term revenue growth for companies operating in this market.

- For instance, a 2025 systematic review-based global analysis estimated that 852.3 million adults worldwide have insomnia, equal to a 16.2% global prevalence, and 415.0 million have severe insomnia (7.9% prevalence). The study also found that insomnia was more prevalent in females than in males across all age groups. That is a strong demand-side statistic for the global market.

MARKET RESTRAINTS

Concerns Regarding Safety and Long-Term Tolerability Continue to Restrain Market Growth

Concerns about the long-term safety of pharmacological treatments are holding back the global market's expansion. Long-term treatment with several insomnia medicines is still associated with concerns such as dependency, falls, residual sedation, and cognitive impairment, particularly in older adults. While insomnia is a common and chronic condition, many patients do not use drug therapy for extended periods as both physicians and patients remain cautious about side effects and long-term treatment burden. This creates a more selective prescribing environment, which slows broader market uptake for several insomnia drug classes. As a result, overall prescription expansion becomes more limited, and the market experiences slower long-term volume growth despite the rising prevalence of insomnia.

- For instance, in April 2026, a published article titled ‘Unmet Needs in the Management of Insomnia in Older Adults and the Role of Lemborexant: A Real-World Perspective’ stated that risks, including dependency constrain available treatments, falls, residual sedation, and cognitive impairment. This directly highlights the clinical caution that can reduce long-term use of insomnia medicines.

MARKET OPPORTUNITIES

Growing Awareness of Sleep Health and Rising Treatment-Seeking Behavior Create New Market Expansion Opportunities

A key market growth opportunity is the growing awareness of sleep health and treatment-seeking behavior. Increased awareness of the awards market growth opportunity, as greater awareness helps move patients from ignoring poor sleep to actively consulting physicians and seeking approved therapies. As insomnia becomes more openly discussed and more clearly linked with daytime performance, emotional well-being, and long-term health, the number of diagnosed and treated patients can rise. These factors collectively increase prescription demand and encourage companies to invest in broader commercialization, physician education, and regional expansion strategies. The growth potential is also encouraging companies to expand geographically and capture new growth opportunities.

- For instance, in March 2026, Idorsia partnered with Pharmalink to distribute and commercialize QUVIVIQ (daridorexant) across the UAE, Kuwait, Qatar, Oman, and Bahrain. The partnership would help ensure that many patients gain access to its insomnia treatment.

MARKET CHALLENGES

Patent Expiry and Generic Competition Are Increasing Pricing Pressure in Market

A key market challenge is patent expiry and generic competition. Once branded insomnia drugs lose exclusivity, lower-cost generic versions can quickly shift prescription demand away from originator products and reduce their pricing power. As more physicians, pharmacies, and payers favor cost-effective alternatives, branded manufacturers may experience faster revenue erosion and weaker market share retention. In addition, strong generic competition can push the market toward price-based competition rather than value-based differentiation, which puts pressure on margins.

- For instance, a February 2025 JAMA study on doxepin for insomnia reported that after generic low-dose doxepin tablets became available in 2020, they replaced the brand-name version, while the article also highlighted distorted utilization and spending patterns in the category. The study found that in 2023, generic low-dose tablets accounted for only 11.2% of presumed insomnia doxepin 30-day supplies but 74.5% of spending, and concluded that this kind of repurposed drug market dynamic can limit access.

Segmentation Analysis

By Drug Class

High Utilization of Z-drugs/Non-Benzodiazepine Hypnotics to Lead Segmental Growth

Based on the drug class, the market is categorized into Dual Orexin Receptor Antagonists (DORAs), z-drugs/non-benzodiazepine hypnotics, benzodiazepine hypnotics, melatonin pathway agents, and others.

Among these, the z-drugs/non-benzodiazepine hypnotics segment accounted for the largest insomnia drugs market share. Z-drugs/non-benzodiazepine hypnotics have been widely used for many years as one of the most established treatment options for insomnia, especially for patients with difficulty falling asleep and, in some cases, staying asleep. Clinical guidance continues to recognize Z-drugs such as zolpidem and zopiclone as licensed short-term insomnia treatments. As these therapies are already familiar to prescribers and are broadly available in oral form, they continue to capture strong prescription volume across cost-sensitive markets. Also, product launches in new geographical regions strengthen the segment's leadership.

- For instance, in June 2023, Idorsia launched QUVIVIQ (daridorexant) in Switzerland – a first-in-class treatment for chronic insomnia disorder to improve both nighttime symptoms and daytime functioning.

The Dual Orexin Receptor Antagonist (DORAs) segment is expected to grow at a CAGR of 18.28% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Disease Indication

Recurring Demand for Therapeutics for Primary Chronic Insomnia Disorder to Boost Segmental Growth

Based on disease indication, the market is segmented into primary chronic insomnia disorder, comorbid psychiatric insomnia, comorbid neurologic/pain-related insomnia, short-term/adjustment insomnia, and others.

In 2025, the primary chronic insomnia disorder accounted for the largest revenue share. The segment dominated the market as it represented the core population for branded insomnia drug development, approval, and long-term treatment use. The segment also tends to generate stronger prescription demand over time owing to patients with chronic symptoms. Due to this recurring pattern, primary chronic insomnia creates a larger and more commercially stable demand base than short-term or narrower comorbid-use clusters.

Key companies are focusing on technologically advanced offerings and geographical expansion to strengthen their market position.

- For instance, in January 2026, Idorsia announced that the global expansion of QUVIVIQ continued through an EMS partnership for Latin America. QUVIVIQ is positioned for adult insomnia characterized by sleep onset and/or sleep maintenance difficulty, which directly supports the strength of the primary chronic insomnia segment.

The others segment is projected to grow at a CAGR of 10.82% over the forecast period.

By Age Group

Increasing Prevalence of Sleep Disorder in Adults to Lead Growth in the Segment

Based on age group, the market is segmented into pediatric and adults.

In 2025, the adults segment dominated the market. The commercial insomnia drug market is largely built around the adult diagnosis, adult prescribing, and adult regulatory approvals. Working-age adults and older adults face high exposure to stress, anxiety, irregular schedules, lifestyle-related sleep disruption, and age-related sleep maintenance issues, which increases treatment demand in this population. Also, most major insomnia product labels, launches, and commercialization efforts are focused on adults, resulting in the segment's dominance.

- For instance, in June 2025, Simcere received approval from China's NMPA for QUVIVIQ® (daridorexant) for the treatment of adult patients with insomnia characterized by difficulty falling asleep and/or maintaining sleep. This supports the dominance of the adult segment as newer insomnia drugs continue to be approved and commercialized first in adult populations.

In addition, the pediatrics segment is projected to grow at a CAGR of 4.31% during the study period.

By Type

Less Cost and Greater Access to Generics Products Fuels the Segment Growth

In terms of type, the market is segmented into branded and generic.

Based on type, the generic drugs dominated the market. The generic segment benefits from the fact that many older insomnia therapies are already deeply established in treatment pathways, while newer branded drugs are still expanding gradually by geography and reimbursement. As generic products are easier to access and usually cost less than novel branded insomnia drugs, they are more likely to be dispensed in everyday retail settings and to be the subject of repeat outpatient prescriptions.

- For instance, in July 2021, Breckenridge Pharmaceutical launched Zolpidem Tartrate Extended-Release Tablets, USP, described as the generic for Ambien CR.

In addition, the branded segment is projected to grow at a CAGR of 10.05% during the study period.

By Route of Administration

High Adherence and Ease of Administration to Lead Growth in the Oral Segment

Based on the route of administration, the market is segmented into oral and others.

In terms of route of administration, the oral formulations dominated the market as insomnia is usually managed in ambulatory settings where ease of use, convenience, and repeat adherence are critical. Tablets are easier for physicians to prescribe and easier for patients to continue over time, especially in chronic insomnia, where nightly administration and patient comfort influence persistence. As most leading insomnia drugs are developed and commercialized as oral products, the oral segment naturally captures the largest share of treatment use and market revenue.

- For instance, in September 2025, Simcere announced that Chinese Phase III clinical data of QUVIVIQ (Daridorexant Tablets) had been published in SLEEP. This highlights that leading newer insomnia therapies are being advanced and validated in tablet form, which supports the dominance of oral formulations in the market.

The others segment is projected to grow at a CAGR of 13.22% over the study period.

By Distribution Channel

Increasing Demand in Drug Stores & Retail Pharmacies Due to Large Patient Volumes to Lead Segmental Growth

Based on distribution channel, the market is segmented into hospital pharmacies, drug stores & retail pharmacies, and online pharmacies.

In terms of distribution channel, the drug stores & retail pharmacies dominated the market as insomnia treatment is primarily an outpatient therapy area where patients fill prescriptions close to home and return for ongoing refills through community channels. This distribution model becomes even stronger when access expands beyond specialists to general practitioners, as prescriptions can then flow more directly into everyday retail pharmacy networks. As a result, wider prescriber access and routine refill behavior support higher dispensing volume through drug stores and retail pharmacies than through hospital-based channels.

- For instance, in February 2025, Idorsia expanded the commercial reach of QUVIVIQ from specialist prescribers to general practitioners through a partnership with Berlin-Chemie, beginning in early April 2025. The development supports the dominance of retail pharmacy channels as broader GP prescribing typically increases prescription flow into community and retail dispensing settings.

The hospital pharmacies segment is projected to grow at a CAGR of 5.88% over the study period.

Insomnia Drugs Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East and Africa.

North America

North America Insomnia Drugs Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 1.84 billion and maintained its leading position in 2025 at USD 2.02 billion. The market in North America is growing as insomnia remains a large, underserved condition. At the same time, patients and physicians are increasingly interested in newer therapies that improve both sleep and next-day functioning.

U.S. Insomnia Drugs Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 2.01 billion in 2026, accounting for roughly 41.29% of the global market.

Europe

Europe is projected to grow at 7.79% over the coming years, the second-highest among all regions, and reach a valuation of USD 1.31 billion by 2026. The market is growing in Europe due to reimbursement support, wider prescriber access, and growing physician confidence in newer dual orexin receptor antagonists, which are driving uptake.

U.K. Insomnia Drugs Market

The U.K. market is estimated at around USD 0.24 billion in 2026, representing roughly 4.84% of the global market revenues.

Germany Insomnia Drugs Market

Germany's market is projected to reach approximately USD 0.29 billion in 2026, equivalent to around 5.92% of the global market revenues.

Asia Pacific

Asia Pacific is estimated to reach USD 1.01 billion in 2026 and secure the position of the third-largest region in the market. The market is growing in the Asia Pacific due to a large pool of insomnia patients, increased awareness of sleep health, and the rising adoption of newer branded therapies in major countries such as China and Japan.

Japan Insomnia Drugs Market

The Japanese market in 2026 is estimated at around USD 0.19 billion, accounting for approximately 3.84% of the global market.

China Insomnia Drugs Market

China's market is projected to be among the largest worldwide, with 2026 revenues estimated at around USD 0.35 billion, representing approximately 7.21% of global sales.

India Insomnia Drugs Market

The Indian market size in 2026 is estimated at around USD 0.12 billion, accounting for roughly 2.38% of global revenue.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.25 billion in 2026. The market is growing in Latin America as insomnia remains a widely under-treated condition, while demand for safer alternatives to older hypnotics is rising. In the Middle East & Africa, the GCC is set to reach USD 0.06 billion in 2026.

South Africa Insomnia Drugs Market

The South African market is projected to reach approximately USD 0.02 billion by 2026, accounting for roughly 0.45% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Partnerships and New Product Launches by Key Players to Propel Market Progress

The global insomnia drugs market is highly consolidated, with companies such as Eisai Co., Ltd., Idorsia Ltd., Merck & Co., Inc., Takeda Pharmaceutical Company Limited, Sanofi, and Pfizer Inc. holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share gains.

- For instance, in April 2025, Eisai Co., Ltd. announced that its in-house-discovered and developed orexin receptor antagonist DAYVIGO has been launched in China for the treatment of adults with insomnia, characterized by difficulties with sleep onset and/or sleep maintenance. Such innovative product launches aim to drive market growth.

Other notable players in the global market include Currax Pharmaceuticals LLC, Viatris Inc., and Lupin Limited. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period for the global market.

LIST OF KEY INSOMNIA DRUGS COMPANIES PROFILED

- Eisai Co., Ltd. (Japan)

- Idorsia Ltd (Switzerland)

- Merck & Co., Inc. (U.S.)

- Takeda Pharmaceutical Company Limited (Japan)

- Sanofi (France)

- Pfizer Inc. (U.S.)

- Currax Pharmaceuticals LLC (U.S.)

- Viatris Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Lupin Limited (India)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Jiangsu Simcere Pharmaceutical Co., Ltd received the first national prescription at Xuanwu Hospital of Capital Medical University, for Daridorexant, a new-generation global anti-insomnia drug.

- February 2025: Nxera Pharma Co., Ltd. entered a license, supply, and commercialization agreement with Holling Bio-Pharma Corp. for daridorexant in Taiwan.

- July 2024: Cosette Pharmaceuticals Inc has acquired prescription insomnia medication Ambien and Ambien CR in the U.S. from Sanofi US. Ambien is indicated for the short-term treatment of insomnia characterized by difficulties with sleep initiation.

- November 2023: Shionogi & Co., Ltd. and Mochida Pharmaceutical Co., Ltd. entered into a sales partnership agreement for the insomnia treatment drug, daridorexant, in Japan.

- August 2022: ResMed announced the acquisition of Leipzig-based company mementor. With this acquisition, ResMed strengthened its overall sleep portfolio in Germany with a digital solution for insomnia.

REPORT COVERAGE

The report provides a detailed global insomnia drugs market analysis and covers the market across key segments such as product/drug class, disease indication/clinical-use cluster, age group, type, distribution channel, and route of administration/formulation. It evaluates how the growing burden of chronic insomnia, rising treatment-seeking behavior, and the launch of newer mechanism-based therapies are shaping market demand across major countries and regions. The study also examines how branded and generic products are performing in the market, as well as the changing roles of retail pharmacies and outpatient prescription channels in supporting product access.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.86% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Disease Indication, Age Group, Type, Route of Administration, Distribution Channel, and Region |

| By Drug Class |

|

| By Disease Indication |

|

| By Age Group |

|

| By Type |

|

| By Route of Administration |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.50 billion in 2025 and is projected to reach USD 8.90 billion by 2034.

In 2025, the market value stood at USD 2.02 billion.

The market is expected to grow at a CAGR of 7.86% over the forecast period.

The Z-drugs/non-benzodiazepine hypnotics segment is expected to lead the market by drug class.

The increasing prevalence of sleep disorders is fueling global market growth.

Eisai Co., Ltd., Idorsia Ltd, Merck & Co., Inc., Takeda Pharmaceutical Company Limited, and Sanofi are the major market players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us