Insurance Brokerage Market Size, Share & Industry Analysis, By Broker Type (Retail Brokerage, Wholesale Brokerage, and Reinsurance Brokerage), By Insurance Type (Life and Health Insurance, Home Insurance, Auto Insurance, Travel Insurance, Property and Liability Insurance, Cyber Insurance, Commercial Auto Insurance, and Others), By Distribution Channel (Online and Offline), By End User (B2C and B2B), and Regional Forecast, 2026–2034

KEY MARKET INSIGHTS

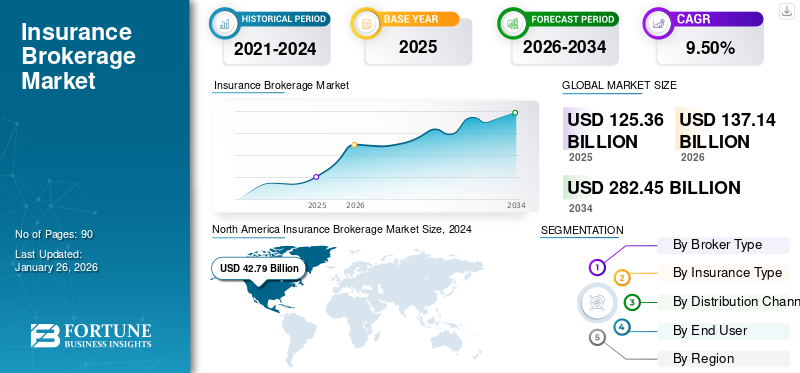

The global insurance brokerage market size was valued at USD 125.36 billion in 2025. The market is projected to grow from USD 137.14 billion in 2026 to USD 282.45 billion by 2034, exhibiting a CAGR of 9.50% during the forecast period. North America dominated the market with a share of 37.50% in 2025.

Insurance brokerage refers to the service that acts as an intermediary between insurance companies and clients (businesses and individuals). The primary part of an insurance broker is to assist clients in searching for the best insurance policies tailored to their specific needs, comparing costs, coverage options, and terms from multiple insurance providers. Unlike insurance agents, who represent particular insurance companies, brokers are independent and work on behalf of the client, aiming to secure the most competitive coverage and rates.

Key companies have adopted multiple strategies to drive business growth, including strengthening client relationships, leveraging digital marketing, and adapting to evolving market trends. These strategies aim to attract new clients, retain existing ones, and increase market share.

Key players in the market include Marsh & McLennan Companies, Aon, and Willis Towers Watson, all of which offer a range of risk management, insurance, and consulting services globally. These firms facilitate the purchase of insurance policies on behalf of clients, helping businesses and individuals find optimal coverage for their needs.

Download Free sample to learn more about this report.

Insurance Brokerage Market Key Takeaways

- 2025 Market Size: USD 125.36 billion

- 2026 Market Size: USD 137.14 billion

- 2034 Forecast Market Size: USD 282.45 billion

- CAGR: 9.50% from 2026–2034

- North America dominated the insurance brokerage market with a 37.50% share in 2025.

- The retail brokerage segment accounted for a 67.60% market share in 2026.

- The life and health insurance segment is projected to hold a 31.64% share in 2026.

North America

North America held a 37.50% share in 2025, valued at USD 46.99 billion.

Europe

Europe accounted for 28.80% share in 2025, valued at USD 36.1 billion.

Asia Pacific

Asia Pacific held a 24.70% share in 2025, valued at USD 31.01 billion.

U.S.

U.S. Market projected to reach USD 38.4 billion by 2026.

Japan

Japan Market projected to reach USD 7.05 billion by 2026.

Read More

IMPACT OF GENERATIVE-AI

Rising Adoption of Gen-AI for Highly Personalized Insurance Products to Aid Market Growth

Gen-AI allows insurance brokers to provide highly personalized insurance products by analyzing a large amount of customer data, including behavioral models, interests, and demographic details. AI-driven processes can tailor insurance policies according to personal needs, improving customer satisfaction and commitment.

- For example, in June 2024, Lemonade, an AI-powered insurance platform, began using Generative AI to personalize policy offerings and deliver instant quotes based on customer choice. By taking advantage of AI, Lemonade can easily adjust its products and pricing, allowing brokers to recommend the best policies for each customer.

As Gen-AI continues to grow, its role in transforming the insurance brokerage will increase. It empowers brokers to answer the requirements of a customer group based on data and information.

MARKET DYNAMICS

Market Drivers

Increased Population in Developed Countries to Drive Market Growth

As the world population is growing, especially in developed countries, the aging demographic is driving an increased need for life insurance and health insurance. Older individuals are more likely to seek health insurance, retirement plans, and life insurance, creating a growing need for brokerage services to help them find the most appropriate coverage. For instance,

- According to the United Nations’ 2024 World Population Prospects report, the global population is projected to reach 8.5 billion people by 2030.

With many people looking for life, health, properties, and commercial insurance, brokers play an important role in guiding consumers and businesses to navigate the complexities of insurance policies. Demographic growth, increased awareness, and evolving regulations that support broader insurance brokerage services collectively serve as the main drivers for market expansion.

Market Restraints

Dependence on Traditional Insurance Agents Can Restrict Market Growth

Dependency on traditional insurance agents can restrict market growth by limiting speed, scalability, and customer experience. Despite a rise in digital insurance platforms, multiple brokers still rely on agents to finalize policies, a process that delays coverage execution and reduces operational efficiency.

- For instance, in regions such as parts of Southeast Asia and India, brokers struggled to provide smooth digital experiences owing to procedural bottlenecks caused by agent involvement.

This reliance restricts brokers’ ability to offer instant, customized solutions, putting them at a disadvantage in an increasingly customer-centric and tech-driven landscape. As digital-first models gain momentum, such dependency on traditional agents can hinder market competitiveness and limit long-term growth opportunities for insurance brokers.

Market Opportunities

Rising Insurance Awareness Among Consumers to Expand Market Growth

As consumers become more knowledgeable about the wide range of available insurance products, including life, cyber, health, and property insurance, they are increasingly turning to brokers for tailored solutions. A key example is the rising demand for cyber insurance products as individuals and businesses identify the need for protection against rising cyber threats.

The emergence of digital insurance platforms, such as InsurTech companies such as Lemonade, reflects a shift toward more transparent, accessible, and tech-driven insurance offerings. Regulatory initiatives, such as the Affordable Care Act in the U.S., further fuel demand for brokerage services, as consumers look for guidance on compliance and policy selection. Overall, heightened consumer awareness drives higher adoption of insurance products and deeper engagement with brokers, contributing significantly to insurance brokerage market growth.

Insurance Brokerage Market Trends

Growing Adoption of Automobiles is Considered to be One of Major Market Trends

The rising adoption of automobiles is a major driver of growth in the market. The demand for auto insurance is mandated by law as vehicle ownership increases globally. Insurance brokers benefit from this trend by facilitating claims, offering tailored policies, and leveraging digital tools to reach better and serve customers. Additionally, embedded insurance models, offered through car dealerships and manufacturers, are further accelerating this trend. For instance,

- According to the President of SIAM, the Indian automobile industry recorded a commendable performance, registering a 12.5% growth in the domestic market during the financial year 2023.

- Data from MarkLines Co. Ltd. shows that new vehicle sales in the U.S. reached 1,468,631 units in 2024, marking a 1.4% year-over-year increase.

Segmentation Analysis

By Broker Type

Increased Demand for Health, Life, Motor, and Home Insurance among SMEs Boosted Retail Brokerage Segment Growth

Based on broker type, the market is divided into retail brokerage, wholesale brokerage, and reinsurance brokerage.

The retail brokerage segment led the market accounting for 67.60% market share in 2026, owing to the increasing demand for health, life, motor, and home insurance among SMEs and individuals. Mandatory health and auto insurance policies, rising digital adoption, and upgraded financial literacy are key factors driving the segment’s growth.

- For instance, in 2024, India’s IRDAI reported a significant growth in digital health policy insurance sales through brokers, particularly in Tier 3 cities.

The reinsurance brokerage segment is anticipated to grow at the highest CAGR during the forecast period, owing to increasing cyber threats, climate-related catastrophes, and demand for risk transfer mechanisms. Insurers depend more on brokers to manage capital efficiency and access global reinsurance capacity. Global reinsurers such as Munich Re and Swiss Re expanded partnerships with brokers to address high-risk sectors, especially in the U.S. and Europe.

By Insurance Type

Life and Health Insurance Segment Led Due to Availability of Premium Financing Options

Based on insurance type, the market is fragmented into life and health insurance, home insurance, auto insurance, travel insurance, property and liability insurance, cyber insurance, commercial auto insurance, and others.

The life and health insurance segment will account for 31.64% market share in 2026. Fintech companies introduced premium financing options, enabling individuals and corporations to pay health insurance premiums through manageable EMIs. These solutions enhance affordability and accessibility, encouraging individuals to invest in health insurance.

- For instance, in 2024, SaveIN, an Indian healthcare-focused fintech, raised USD 4.3 million in fresh funding, denoting a major milestone in its efforts to make private healthcare more accessible and affordable across the country. This investment supports the expansion of SaveIN’s innovative no-cost EMI offerings and its rapidly growing network of healthcare partners.

The cyber insurance segment is anticipated to grow at a prominent CAGR during the forecast period. The growing sophistication and frequency of cyberattacks force businesses to invest in cyber insurance to safeguard against operational disruptions and potential financial losses.

To know how our report can help streamline your business, Speak to Analyst

By Distribution Channel

Rising Need for Face-to-Face Interactions for Multifaceted Insurance Products Encouraged Offline Segment Growth

Based on the distribution channel, the market is bifurcated into online and offline.

The offline segment led the market accounting for 66.76% market share in 2026. Despite the digital shift, many consumers prefer face-to-face interactions when dealing with multifaceted insurance products. Brokers and agents offer personalized advice and build trust, an approach that remains important in developing countries. In these areas, the existing network of insurance agents and brokers continues to play a crucial role in reaching customers who may have digital access.

The online segment is anticipated to grow at the highest CAGR during the forecast period, owing to the increasing adoption of digital technologies and the convenience of online platforms. Consumers prefer the ease of comparing and purchasing policies online, leading to a surge in digital insurance adoption.

By End User

Growing Adoption of Digital Platforms Boosted B2B Segment Growth

Based on end user, the market is divided into (Business-to-Business) B2B and (Business-to-Consumer) B2C.

The B2C segment will account for 61.96% market share in 2026. The growing adoption of digital platforms has made the procedure easier for consumers to purchase and compare insurance policies online, improving convenience and accessibility. Furthermore, data analytics and AI advancements have enabled brokers to offer tailored insurance products that meet individual consumer needs, thereby boosting customer satisfaction and engagement.

The B2B segment is anticipated to grow at the highest CAGR during the forecast period. As businesses face increasingly complex risks, such as regulatory compliance challenges and rising cyber threats, they are increasingly on specialized risk management services and insurance solutions provided by brokers. Evolving regulatory frameworks require businesses to maintain specific coverages, driving demand for brokerage services that can navigate and manage these requirements effectively.

INSURANCE BROKERAGE MARKET REGIONAL OUTLOOK

By region, the market is divided into North America, Europe, Asia Pacific, the Middle East & Africa, and South America.

North America

North America Insurance Brokerage Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America held 37.50% of the global market share, reaching a valuation of USD 46.99 billion, and is projected to grow to USD 51.7 billion in 2026. owing to increasing demand for digital and personalized insurance solutions across commercial and personal segments. Increasing awareness of cyber threats, risk management, and regulatory compliance has further boosted demand for specialized brokerage services. In 2024, firms such as Aon and Marsh McLennan expanded their advisory and analytics abilities through partnerships and acquisitions that cater to evolving client needs. Additionally, the shift toward online platforms and embedded insurance has accelerated digital transformation within the brokerage landscape. The U.S. market is projected to reach USD 38.4 billion by 2026.

Download Free sample to learn more about this report.

The U.S. accounts for the largest share of the North American market, supported by a highly developed and deeply penetrated financial services sector. The country is home to several leading global players who consistently innovate and adapt their offerings to maintain competitiveness and industry leadership.

Europe

The market in Europe reached USD 36.1 billion in 2025, representing 28.80% of total market revenue, and is projected to reach USD 39 billion in 2026. The European market is growing steadily, owing to rising demand for health, cyber, and ESG-linked insurance, and rising SME insurance penetration. Brokers are transitioning from transactional intermediaries to strategic risk advisors. The UK market is projected to reach USD 11.04 billion by 2026, while the Germany market is projected to reach USD 7.6 billion by 2026. For instance,

- In September 2022, Howden acquired Théorème, a corporate insurance broker headquartered in Paris. This acquisition includes Howden’s recent agreement to acquire C.R.F. Conseils (“CRF”) and underlines Howden’s investment in deepening expertise to serve French clients more effectively.

Asia Pacific

Asia Pacific contributed approximately USD 31.01 billion to the global market in 2025, accounting for 24.70% share, and is expected to reach USD 34.31 billion in 2026. Asia Pacific will grow at the highest CAGR among all regions. The region’s rising populations, particularly in countries such as China, have the largest population of 1.4 billion in the Asia Pacific region, followed by Indonesia, India, and Pakistan. These demographic trends are pushing insurance companies to expand their network and focus on high-growth markets. The lower penetration of Non-Life and Life Insurance in these high-population countries is expected to generate greater demand for the insurance sector. The Japan market is projected to reach USD 7.05 billion by 2026.

Middle East & Africa

The Middle East & Africa region captured 3.40% of the global market in 2025, generating USD 4.27 billion in revenue, and is projected to reach USD 4.55 billion in 2026. The Middle East & Africa region is witnessing considerable growth due to rising insurance awareness and expanding middle-class populations. Government initiatives aimed at boosting insurance penetration, such as Saudi Arabia’s 2030 Vision, are driving the uptake of health and motor insurance across the region.

South America

The market in South America is in a growing phase due to increased economic recovery and climate-related risks. Growing digital adoption is enabling brokers to expand outreach, especially in underserved rural areas. In 2024, Grupo Nacional Provincial (GNP) in Brazil partnered with digital platforms to streamline policy distribution and claims management. Countries such as Brazil and Argentina are witnessing a surge in InsurTech collaborations, which are driving innovation and improving customer experience in the brokerage sector.

Competitive Landscape

KEY INDUSTRY PLAYERS

Key Payers Focus on Partnerships to Boost Their Market Share

Key players in the market are focusing on strategic partnerships, acquisitions, and developing comprehensive insurance brokerage services to grow their market share. These strategies aim to enhance regulatory compliance, diversify service offerings, and expand into new geographic markets.

List of Insurance Brokerage Companies Studied (including but not limited to)

- Marsh & McLennan Companies (U.S.)

- Aon plc (U.K.)

- Arthur J. Gallagher & Co. (U.S.)

- Acrisure LLC (U.S.)

- Brown & Brown Inc. (U.S.)

- BMS Group Ltd. (Canada)

- TIH (U.S.)

- Alliant Insurance Services, Inc. (U.S.)

- Lockton Inc. (U.S.)

- Policybazaar Insurance Brokers Pvt. Ltd. (India)

- WNS (Holdings) Ltd (U.S.)

- Brown & Brown, Inc. (U.S.)

- Talanx AG (Germany)

- Hub International (U.S.)

- MST Insurance Service Co. (Japan)

- Cosco Shipping (China)

- Mahindra Insurance Brokers Ltd. (MIBL) (India)

- Ecclesia Holding GmbH (Germany)

- Tri Seguros (Mexico)

- and others

KEY INDUSTRY DEVELOPMENTS

- June 2025- Porch Group, Inc. announced a significant expansion of its insurance agency distribution channel, including new partnerships with Evertree Insurance Services, LLC, MassDrive Insurance Group, LLC, and Roamly Insurance Group. These partnerships support Porch’s vision to build a vertically integrated home services and insurance ecosystem, accelerating revenue growth.

- April 2025- Lockton entered into a strategic partnership with Axio to integrate APIs between Axio’s Axio360 platform and Lockton’s Scout analytics platform. This collaboration enhances Lockton’s cyber brokerage capabilities by providing brokers with real-time, data-driven cyber risk insights through a unified interface.

- March 2025- Gallagher Insurance, a global insurance brokerage and risk management company, and New Zealand Rugby (NZR) partnered at a special launch event in Auckland. This partnership aims to drive local community impact and create significant experiences for Gallagher’s clients in the region.

- February 2025- Newfront, the insurance brokerage firm, and Pave, the complete management platform, announced a partnership to redefine companies’ approach to employee benefits and compensation.

- October 2024- Lockton, an insurance brokerage firm, received regulatory approval from the Insurance Regulatory and Development Authority of India (IRDAI) to acquire Arihant Insurance Broking Services Limited. This significant milestone marks Lockton’s strategic entry into the Indian market, with plans to meet the rising demand for sophisticated risk consulting and management services.

INVESTMENT ANALYSIS AND OPPORTUNITIES

The insurance brokerage market presents strong investment potential, driven by digital transformation, rising demand for specialized insurance solutions (e.g., health, cyber), and regulatory shifts favoring advisory-led models. Players adopting analytics, AI, and embedded insurance platforms are attracting investor interest due to their scalability and operational efficiency. Emerging markets such as India, Brazil, and Southeast Asia present high-growth opportunities due to low insurance penetration and increasing digital adoption. Strategic investments in B2B-focused and tech-driven brokers can potentially deliver significant returns. However, players must manage risks related to compliance, cyber threats, and economic sensitivity.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, broker type, insurance type, distribution channel, and product end users. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.50% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Broker Type

By Insurance Type

By Distribution Channel

By End User

By Region

|

|

Companies Profiled in the Report |

• Marsh & McLennan Companies (U.S.) • Aon plc (U.K.) • Arthur J. Gallagher & Co. (U.S.) • Acrisure LLC (U.S.) • Brown & Brown Inc. (U.S.) • BMS Group Ltd. (Canada) • TIH (U.S.) • Alliant Insurance Services, Inc. (U.S.) • Lockton Inc. (U.S.) • Policybazaar Insurance Brokers Pvt. Ltd. (India) |

Frequently Asked Questions

The market is projected to reach USD 282.45 billion by 2034.

In 2025, the market was valued at USD 125.36 billion.

The market is projected to grow at a CAGR of 9.50% during the forecast period.

By insurance type, the life and health insurance segment led the market.

Increased population in developed countries is a key factor driving the market.

Marsh & McLennan Companies, Aon plc, Arthur J. Gallagher & Co., Acrisure LLC, and Brown & Brown Inc. are the top players in the market.

North America led the market.

- 2021-2034

- 2025

- 2021-2024

- 90

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us