Intensive Care Unit (ICU) Equipment Market Size, Share & Industry Analysis, By Product (Beds, Ventilators, Pulse Oximeters, Dialysis Equipment, and Others), By Patient (Adult and Pediatric), By Application (Neurology, Cardiology, Respiratory, Oncology, Trauma, and Others), By End User (Hospitals, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

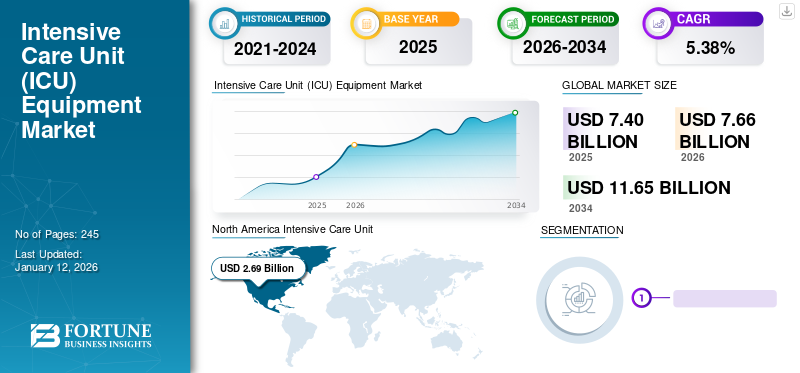

The global intensive care unit (ICU) equipment market size was USD 7.4 billion in 2025 and is projected to grow from USD 7.66 billion in 2026 to USD 11.65 billion by 2034, exhibiting a CAGR of 5.38% during the forecast period. Moreover, the U.S. intensive care unit equipment market size is projected to grow significantly, reaching an estimated value of USD 3.10 billion by 2030, driven by an increase in demand due to the increasing prevalence of chronic diseases. North America dominated the intensive care unit equipment market with a market share of 36.32% in 2025.

Intensive care represents the highest patient care and treatment level designated for critically ill patients with potentially recoverable life-threatening conditions. This intensive care for patients is given in the intensive care unit, a separate self-contained area within a medical facility equipped with high-tech specialized facilities. A patient's medical condition is improved with the help of various medical equipment such as pulse oximeter, dialysis equipment, ventilators, catheters, tubes, pumps, and bedside monitors.

The growing geriatric population, with the rising prevalence of chronic diseases and the increase in the number of fatal accidents and sports injuries, are fueling the global market growth. Moreover, outbreaks of emerging health threats, such as COVID-19, are increasing the ICU admission rate, surging the demand for these types of equipment.

As per a study published in 2023 by the Front Public Health, 176,137 patients were hospitalized with COVID-19 infection in Germany during 2020. Out of these patients, 27,053 were treated in the ICU. To meet this growing demand for ICU care, market players focused on introducing novel products with advanced technologies to improve the treatment outcomes and strengthen their market presence.

Download Free sample to learn more about this report.

Global Intensive Care Unit (ICU) Equipment Market Snapshot & Highlights

Market Size & Forecast:

- 2025 Market Size: USD 7.4 billion

- 2026 Market Size: USD 77.66 billion

- 2034 Forecast Market Size: USD 11.65 billion

- CAGR: 5.38% from 2026–2034

Market Share:

- North America dominated the intensive care unit equipment market with a 36.32% share in 2025, driven by a high prevalence of chronic diseases, well-established healthcare infrastructure, and increased demand for critical care units due to aging population.

- By product, the beds segment is expected to retain its largest market share owing to continuous technological advancements such as wireless integration and nurse-call systems, as well as increased demand during and after the COVID-19 pandemic.

Key Country Highlights:

- United States: Rising geriatric population and increased ICU admissions due to chronic diseases are major factors accelerating the adoption of intensive care unit equipment. Additionally, initiatives by market players to ramp up local production of ventilators and ICU beds post-COVID-19 are supporting market growth.

- Europe: Countries like Germany, the U.K., and France are experiencing growth in the ICU equipment market due to expanding critical care capacities and increasing awareness about advanced treatment technologies among healthcare providers.

- China: Rapid healthcare infrastructure development, coupled with the rising patient pool suffering from chronic respiratory and cardiovascular diseases, is driving the demand for advanced ICU equipment in hospitals and specialty clinics.

- Japan: The country’s aging population and government initiatives to enhance critical care facilities are contributing to the growing demand for technologically advanced ICU equipment across healthcare settings.

COVID-19 IMPACT

Increased ICU Admissions Amid COVID-19 Pandemic Positively Impacted the Market Growth

The COVID-19 pandemic has unprecedentedly impacted the society, economy, and critical care equipment sector. The global market witnessed a positive surge during the COVID-19 pandemic, owing to the growing demand for equipment amidst the pandemic. Due to the rising number of COVID-19 cases, critical care admissions increased during 2020, impacting the market positively.

- For instance, as per an article published in 2020 by UpToDate, Inc., among those infected with the SARS-CoV-2 virus, up to 20% developed the severe disease, requiring hospitalization. Among those hospitalized, up to one-quarter needed intensive care unit admission, representing approximately 5% to 8% of the infected population. Furthermore, per the same article, the percentage of critical care unit admissions in China due to the COVID-19 pandemic ranged from 7% to 26%.

Moreover, the COVID-19 outbreak resulted in an unprecedented surge in demand for beds, dialysis equipment, and ventilators. According to a study published by the Elsevier, at the beginning of March 2020, Lombardy, the most affected region in Italy, had a total critical care unit capacity of 724 beds. By March 16th, 2020, this number increased to 1100, of which 898 were exclusively for COVID-19 patients.

In 2021, the number of cases was declining, but the outbreak motivated key players and various governmental & non-governmental organizations to strengthen the healthcare infrastructure, especially intensive care units, by increasing investments in R&D to support the rising demand.

- In August 2021, the government of Manitoba, Canada, invested USD 643 million to improve healthcare facilities in the provinces.

The demand for ICU equipment, such as ventilators is moving toward normalization and has been anticipated to steadily return to normal sales from 2022 onwards. However, a surge in the geriatric population that is more prone to diseases and requires critical care and unmet medical demand in developing countries, such as China and India will likely augment the market growth during the forecast period.

LATEST TRENDS

Technological Advancements in the Equipment is a Prominent Trend

In the past few decades, rapid technological advancement has been witnessed in the critical care areas. Incorporating artificial intelligence in the ventilators is one of the most current market trends globally.

- For instance, in August 2020, when ventilators have become critical for treating severe COVID-19 cases, an India-Dutch start-up LEVEN Medical, developed smart ventilators integrated with artificial intelligence (AI) and machine learning (ML).

Moreover, the beds are witnessing innovative developments, such as wireless beds that provide higher service and function levels, such as caregiver and patient assistance, real-time monitoring, automated functions and positions, and data logging.

- For instance, in October 2020, Stryker announced the global launch of the industry's first and only completely wireless hospital bed, ProCuity. This intelligent bed was designed to help reduce in-hospital patient falls at all acuity levels, improve nurse workflow efficiencies and safety, and help lower hospital costs. It is the only bed in the market today that can connect seamlessly to nurse call systems without cables or wires.

Hence, such increasing technological advancements in the intensive care unit equipment are anticipated to spur market growth during the forecast period.

Download Free sample to learn more about this report.

INTENSIVE CARE UNIT (ICU) EQUIPMENT MARKET GROWTH FACTORS

Rising Prevalence of Chronic Diseases and Associated ICU Admissions to Spur Market Growth

Chronic diseases, such as cardiovascular diseases, cancer, neurological diseases, and respiratory diseases, are prevalent globally. For instance, according to an article published by Forbes in 2022, approximately 133 million Americans have at least one chronic disease. They require ongoing monitoring or treatment, leading to long-term hospitalization and intensive care. Hence, the growing prevalence of chronic diseases has simultaneously led to increasing patient admissions in the critical care unit, which is projected to drive market growth.

- For instance, a study published by the Journal of Cardiothoracic and Vascular Anesthesia in 2022, 6% of 2,789 patients with renal failure, COPD, and arrhythmia were readmitted to the ICU.

Additionally, the burden of respiratory diseases is rising globally, owing to various factors, such as obesity, smoking, and lifestyle changes. Acute respiratory failure often requires intensive care unit admission at severe stages of respiratory diseases.

- According to a research article published by the National Center of Biotechnology Information (NCBI), in Germany, around 2.1 million patients are admitted to intensive care units each year, out of which an estimated 42.0% of patients require mechanical ventilation.

Thus, the increasing demand for critical care equipment due to rising critical admissions in developed and developing countries is anticipated to boost the ICU equipment market growth during the forecast period.

RESTRAINING FACTORS

High Cost Associated with the Equipment to Limit Market Growth

Despite the growing population and chronic disease burden, certain factors restrain the market growth. Among them, one of the major restraining factors is the high price tag of critical care equipment. Higher equipment costs result in a higher cost per patient admission in the critical care unit.

- For instance, according to the economic analysis, the cost per patient admission in the ICU ranges from about USD 1,783 to USD 78,435. Hence, the overall treatment cost in the ICU is an out-of-pocket expense in emerging countries, limiting the market growth.

Due to the high cost associated with the equipment, many healthcare providers in emerging countries purchase refurbished equipment for their facilities. This factor significantly hampers market growth. For instance, mid-sized private hospitals that account for over 90% of the healthcare providers in India cannot afford expensive systems, such as patient monitoring equipment and ventilators.

- In March 2020, the Union Ministry of India eased the import policy and commissioned the import of second-hand ventilators until September 2020, as coronavirus infections skyrocketed. In addition, higher import duties on advanced equipment are projected to significantly impact the market growth during the forecast period.

SEGMENTATION

By Product Analysis

Integration of Advanced Technology Led to the Dominance of Bed Segment in the Market

Based on the product, this market is segmented into beds, ventilators, pulse oximeters, dialysis equipment, and others.

The beds segment dominated the market accounting for 30.82% market share in 2026. The growth of this segment is attributed to various technological advancements related to wireless technology and integrated nurse-calling systems. In addition, the outbreak of COVID-19 has also provided significant growth in the segment.

The ventilators segment held the second-largest share in 2024. The increase prevalence of acute respiratory distress syndrome (ARDS) has surged the hospitalization rate and need for critical care. This has increased the demand for life-support equipments such as ventilators.

Dialysis segment generated notable revenue in 2024, owing to the rising number of patients suffering from chronic kidney diseases (CKD) which are at high risk of developing critical illness. This is increasing the ICU addmission rate which is driving the demand of dialysis equipment in ICU.

Pulse oximeters held considerable share of the market in 2024. These equipments are used to monitor vitals of ICU patients and as the number of ICU increase, the demand for these equipments will increase during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Patient Analysis

Adult Segment Held the Dominant Position in 2024 Due to Rising Geriatric Population

Based on the patient, the market is segmented into adult and pediatric.

The adult segment is projected to dominate the market with a share of 60.92% in 2026. The increasing geriatric population, coupled with the rising associated diseases among the adult population, is projected to significantly augment the segment's growth during the forecast period. Moreover, the high smoking rate in the adult population has tremendously influenced the growing prevalence of respiratory diseases in adults, leading to a higher number of critical care unit admissions among this population.

The growing cases of respiratory distress syndrome, bronchopulmonary dysplasia, persistent pulmonary hypertension, pneumonia, and other diseases among neonates is anticipated to surge the demand for this equipment among pediatric patients. For instance, according to the various research studies published in NCBI, in the U.S., around 1% of neonates suffer from respiratory distress syndrome after birth. This is therefore, projected to favor the segment’s growth.

By Application Analysis

Cardiology Segment Accounted for the Highest Share Due to Increasing Adoption of a Sedentary Lifestyle

Based on the application, the global market is segmented into neurology, cardiology, respiratory, oncology, trauma, and others.

The cardiology segment is expected to lead the market, contributing 35.72% globally in 2026. The increasing adoption of a sedentary lifestyle has led to a striking rise in the cases of cardiovascular diseases among the younger population. This has increased critical care unit admissions due to increased heart failure. For instance, according to the CDC, every year, around 800,000 Americans suffer from heart attacks.

The respiratory segment is the second dominating segment in the market. The growing prevalence of respiratory diseases and requiremnet of critical care in hospitals is anticipated to augment the global market growth during the forecast period.

By End User Analysis

Higher Adoption of Equipment in Hospitals Enabled the Dominance of the Segment

By end user, the market includes hospitals, specialty clinics, and others.

The hospitals segment will account for 69.04% market share in 2026. The higher patient admission in hospitals has led to its market dominance in 2024. For instance, according to an article published by the Anaesthesia Critical Care & Pain Medicine in 2023, among 1,594,801 ICU admissions, the yearly ICU admission increased from 3.3 to 3.5 per year per 1000 inhabitants in France between 2013 and 2019.

On the other hand, there is an increase in patient preference toward outpatient centers, such as specialty clinics and ambulatory surgical centers, due to more convenient and cost-effective care. According to a 2019 Health Care Cost Institute study, healthcare services performed in outpatient settings exhibited a growth of 12.9% in 2017 from 2009. This is projected to increase the adoption of intensive care unit equipment in the specialty clinics segment and thus favor segmental growth.

REGIONAL INSIGHTS

In terms of region, the global market is studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Intensive Care Unit (ICU) Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 2.69 billion in 2025, representing 36.32% of the global market share, and is expected to reach USD 2.78 billion in 2026. North America dominated the global intensive care unit equipment market with a share of 36.69% in 2024. The rising geriatric population, higher prevalence of chronic conditions, and well-established healthcare infrastructure in the U.S. are other major factors responsible for the region's dominance in the global market. The market in this region has witnessed remarkable growth owing to the COVID-19 impact. Many machinery & equipment companies have also initiated the production of different intensive care unit equipment, such as ventilators, to meet the surging demand. For instance, according to a U.S. Census Bureau research study, in 2050, the population aged 65 and over in the country is projected to be 83.7 million, double its estimated geriatric population in 2012. The U.S. market is projected to reach USD 2.53 billion by 2026.

Europe

The Europe market was valued at USD 2.17 billion in 2025, capturing 29.30% of global revenue, and is estimated to reach USD 2.25 billion in 2026. Developed countries in Europe, such as Germany, the U.K., and France, are anticipated to drive the critical care equipment market growth of this region. The growing geriatric population, along with the rising awareness among the patient population, are majorly responsible for the market expansion in the region. The increasing concern about the COVID-19 pandemic and these countries' superfast expansion of the critical care unit capacity have added a stimulus for growth. The UK market is projected to reach USD 0.3 billion by 2026, while the Germany market is projected to reach USD 0.52 billion by 2026.

Asia Pacific

In 2025, Asia Pacific held 18.43% of the global market, reaching a valuation of USD 1.36 billion, and is projected to grow to USD 1.42 billion in 2026. Asia Pacific is projected to witness the highest growth rate in terms of the critical care equipment market revenue. Developing healthcare infrastructure, along with the increasing patient pool of chronic disorders, are likely to augment the market growth in the region. The Japan market is projected to reach USD 0.38 billion by 2026, the China market is projected to reach USD 0.36 billion by 2026, and the India market is projected to reach USD 0.16 billion by 2026.

Latin America and Middle East & Africa

Latin America and the Middle East & Africa are expected to reflect a slower-to-moderate growth in the market owing to the presence of a refurbished market leading to lesser penetration of technologically advanced equipment in these regions. The Latin America region captured 8.53% of the global market in 2025, generating USD 0.63 billion in revenue, and is projected to reach USD 0.65 billion in 2026. Middle East & Africa contributed approximately USD 0.55 billion to the global market in 2025, accounting for 7.41% share, and is expected to reach USD 0.56 billion in 2026.

To know how our report can help streamline your business, Speak to Analyst

KEY INDUSTRY PLAYERS

Leading Players Continue to Maintain Strong Foothold Owing to the Introduction of New Products in Market

Leading players in the competitive landscape of the global market include Koninklijke Philips N.V., GENERAL ELECTRIC COMPANY, B. Braun Melsungen AG, and Medtronic. Numerous product launches, expansion of their product portfolios through organic and inorganic strategies, and increasing research and development in the critical care segment are major imperatives adopted by these players to maintain their strategic position in the market.

Additionally, a strong emphasis on acquisitions & partnerships to expand their critical care segment is likely to help register faster growth in this market. For instance, in March 2020, Ford collaborated with 3M and GE Healthcare, intending to speed up the production of ventilators for people amid the coronavirus pandemic.

LIST OF KEY COMPANIES IN INTENSIVE CARE UNIT (ICU) EQUIPMENT MARKET:

- General Electric Company (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Getinge AB (Sweden)

- Medtronic (Ireland)

- Fresenius SE & Co. KGaA (Germany)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- HILL-ROM HOLDINGS, INC. (U.S.)

- Medline Industries, Inc. (U.S.)

- B. Braun Melsungen AG (Germany)

- Edwards Lifesciences Corporation (U.S.)

- Invacare Corporation (U.S.)

KEY INDUSTRY DEVELOPMENTS:

- March 2023: SAMRIDH Healthcare funded Critical Care Hope to set up tele-ICUs across India to deliver critical care services.

- January 2023: Getinge expanded its ICU offering by launching a Servo-c mechanical ventilator to enable personalized respiratory treatments for adult and pediatric patients.

- August 2022: Fresenius Medical Care launched Speedswap to improve the quality of dialysis treatment in the critical care setting.

- January 2022: OES Medical Ltd. launched an ICU ventilator at Arab Health 2022 to support hospitals in managing oxygen demand.

- February 2021: Hicuity Health partnered with Covenant Health to form a strategic regional critical care telehealth collaboration. This collaboration was carried out to expand intensive care services and launch a tele-ICU initiative across the U.S.

REPORT COVERAGE

This market report provides a detailed analysis of the market. It focuses on key aspects such as leading companies, products, applications, patient type, and end-user. Besides this, it offers insights into the market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Growth Rate |

CAGR of 5.38% from 2026 to 2034 |

|

Historical Period |

2019-2023 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Product

|

|

By Patient

|

|

|

By Application

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market is projected to grow from USD 7.66 billion in 2026 to USD 11.65 billion by 2034.

In 2025, the market size in North America was USD 2.69 billion.

The market will exhibit steady growth at a CAGR of 5.38% during the forecast period (2026-2034).

By product, the beds segment led the market.

The increasing prevalence of chronic diseases and the introduction of technologically advanced products are the key factors driving market growth.

Koninklijke Philips N.V., GENERAL ELECTRIC COMPANY, B. Braun Melsungen AG, and Medtronic are the top players in the market.

- 2021-2034

- 2025

- 2021-2024

- 245

Get 20% Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us