Intravenous Equipment Market Size, Share & Industry Analysis, By Product Type (IV Catheters, Infusion Pumps, IV Administration & Fluid Delivery Sets, IV Accessories & Components, Securement & Stabilization Devices, and Others), By End-user (Hospitals & ASCs, Specialty clinics, Home Healthcare Settings, and Others), and Regional Forecast, 2026-2034

Intravenous Equipment Market Size and Future Outlook

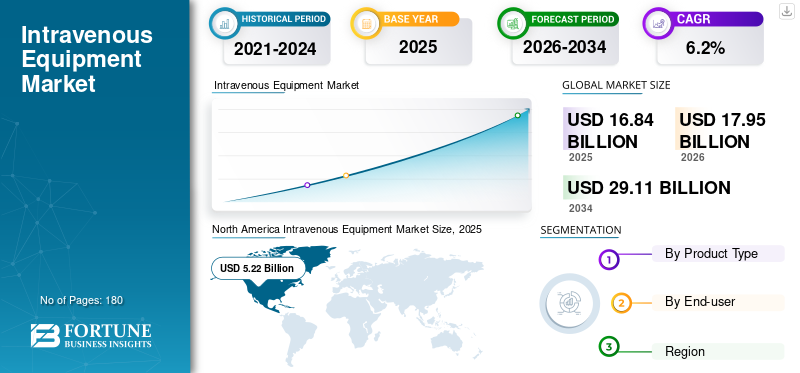

The global intravenous (IV) equipment market size was valued at USD 16.84 billion in 2025. The market is projected to grow from USD 17.95 billion in 2026 to USD 29.11 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. North America dominated the intravenous equipment market with a market share of 31% in 2025.

Intravenous equipment refers to medical devices used to deliver fluids, medications, blood products, and nutrients directly into a patient’s bloodstream. These devices include IV catheters, IV administration sets, infusion pumps, connectors, and securement devices. The market growth is attributed to an increasing number of hospital admissions, rising surgical procedures, and growing prevalence of chronic diseases.

BD, Baxter, B. Braun SE, and ICU Medical, Inc. held the majority of the market share due to broad portfolios and established geographic footprints.

Download Free sample to learn more about this report.

IV EQUIPMENT MARKET TRENDS

Adoption of Smart Infusion Pumps and Safety IV Devices to Emerge as a Key Trend

Hospitals are increasingly adopting smart infusion pumps to reduce medication errors. These devices improve treatment accuracy and enhance patient safety. At the same time, safety IV catheters and needleless connectors are gaining traction in many healthcare facilities to prevent needlestick injuries. As a result, key players are introducing new products, shaping the IV treatment.

- For instance, in April 2024, Baxter announced U.S. FDA 510(k) clearance for its Novum IQ large volume infusion pump (LVP) with Dose IQ Safety Software.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Number of Hospitalizations and Surgical Procedures to Fuel Market Growth

In recent years, the increasing number of hospital admissions and surgical procedures worldwide has heightened the need for IV therapy to administer medications, fluids, or anesthesia during treatment. Additionally, the increased rate of chronic diseases such as cancer, cardiovascular disorders, and infections is driving the demand for infusion therapy, which is influencing companies to launch products such as infusion pumps, driving growth in the global intravenous equipment market.

- For instance, according to the data from the American Hospital Association (AHA) Statistics 2026, there were 35,658,583 hospital admissions in the U.S. in 2025.

MARKET RESTRAINTS

Risk of Catheter-Related Infections and Complications to Restrict Market Growth

Despite widespread use, IV therapy carries risks such as catheter-related bloodstream infections and complications caused by improper catheter placement or prolonged use, which can lead to increased hospital stays and healthcare costs. Moreover, hospitals are required to follow strict infection control guidelines that limit the use of certain devices, leading to recalls, thereby hindering the intravenous equipment market growth.

- For instance, in March 2026, the FDA issued Class I recalls, the most serious type, for two Smiths Medical infusion pumps, such as the CADD-Solis Ambulatory Infusion Pump and CADD-Solis VIP Ambulatory Infusion Pump.

MARKET OPPORTUNITIES

Growing Demand for Home Infusion Therapy to Offer Lucrative Growth Opportunities

Recently, there has been an increased demand for home-based healthcare, such as home infusion therapy, which allows patients to receive treatments such as chemotherapy, antibiotics, and parenteral nutrition. Home-based care reduces hospital costs and improves patient convenience, which is a main factor in increasing the adoption of home-based IV equipment, offering lucrative opportunities for key players to introduce relevant products.

MARKET CHALLENGES

Strong Pricing Pressure on Manufacturers to Challenge Market Expansion

Tertiary hospitals often purchase IV equipment through large procurement contracts or group purchasing organizations, creating strong pricing pressure on manufacturers. In several countries, it poses a major challenge for key players to maintain business profits for high-volume consumables such as administration sets and IV catheters.

Segmentation Analysis

By Product Type

Widespread Usage and Improved Designs Boosted the IV Catheters Segment’s Growth

Based on product type, the market is segmented into IV catheters, infusion pumps, IV administration & fluid delivery sets, IV accessories & components, securement & stabilization devices, and others.

The IV catheters segment accounted for the largest global intravenous equipment market share in 2025. The growth is attributed to widespread adoption in almost every IV therapy procedure. In addition, safety-engineered catheters designed to prevent needlestick injuries are becoming widely popular in hospitals, further driving the segment’s growth.

To know how our report can help streamline your business, Speak to Analyst

The infusion pumps segment is projected to grow at a CAGR of 6.7% during the forecast period.

By End-user

Large Volume of Inpatient Admissions Propelled the Hospitals & ASCs Segment’s Growth

On the basis of end-user, the market is segmented into hospitals & ASCs, specialty clinics, home healthcare settings, and others.

In 2025, hospitals & ASCs dominated the market. The segment’s growth is driven by the large volumes of inpatient admissions in these settings, where IV fluids, medications, and anesthesia are commonly administered. Moreover, a large number of hospitals and ASCs in developed regions is further supporting the adoption of IV equipment. Furthermore, the segment is set to hold a 62.9% share by 2026.

- For instance, MedPAC data showed that the number of ASCs rose in 2023, with Medicare-certified facilities up 2.5% from 2022 to 6,308.

The specialty clinics segment is projected to grow at an 6.5% CAGR over the forecast period.

Intravenous (IV) Equipment Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Intravenous Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 4.91 billion, and is projected to grow to USD 5.22 billion by 2025. The region’s growth is attributed to high healthcare spending, advanced healthcare infrastructure, and strong adoption of infusion therapy technologies.

U.S. IV Equipment Market

In 2026, the U.S. is projected to reach USD 5.16 billion, accounting for approximately 28.7% of the global market.

Europe

Europe is projected to record a 6.2% growth rate during the projection period, the second-highest globally, reaching USD 4.99 billion by 2026. The growth is attributed to the strong presence of key players, which is contributing to a high penetration rate of IV equipment in the region.

U.K. Intravenous Equipment Market

The U.K. market is expected to reach USD 1.40 billion by 2026, accounting for roughly 7.8% of global revenues.

Germany Intravenous Equipment Market

Germany's market is projected to reach USD 1.43 billion by 2026, accounting for approximately 8.0% of global revenue.

Asia Pacific

By 2026, the market in the Asia Pacific is expected to reach USD 4.79 billion, ranking third globally. The growth is attributed to a large patient pool of cancer, requiring chemotherapy, and a large volume of hospital admissions in China and India, which is expected to favor the adoption of IV equipment in the region.

- For instance, according to the data from the National Institute of Cancer Prevention and Research in March 2026, an estimated 2.5 million people are living with cancer in India.

Japan IV Equipment Market

Japan is projected to generate USD 0.63 billion in revenue by 2026, accounting for approximately 3.5% of the global market.

China IV Equipment Market

China’s market is expected to reach nearly USD 2.36 billion by 2026, accounting for 13.2% of global revenues.

India IV Equipment Market

India’s market is projected to reach USD 0.54 billion by 2026, accounting for around 3.0% of global market revenue.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa are expected to grow moderately, with the Latin America market predicted to reach USD 1.74 billion by 2026. The growth of these regions is expected to be driven by the expansion of hospital networks and rising demand for surgical procedures, encouraging key players to expand their product offerings in these regions.

GCC Intravenous Equipment Market

By 2026, the GCC market is expected to reach USD 0.44 billion, accounting for 2.5% of total market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Extensive Product Portfolios and Focus on Product Innovation to Enhance the Market Share of Key Players

In 2025, BD, Baxter, B Braun SE, and ICU Medical, Inc. held the majority of the global intravenous equipment market share. This share is attributed to their extensive product portfolio, which includes IV catheters, infusion pumps, administration sets, and vascular access devices.

Moreover, other prominent players are increasingly focusing on product innovation, partnerships, and expanding manufacturing capacity to strengthen their market presence in the coming years.

LIST OF KEY Intravenous Equipment MARKET COMPANIES PROFILED

- BD (U.S.)

- Baxter (U.S.)

- Braun SE (Germany)

- ICU Medical, Inc. (U.S.)

- Fresenius Kabi AG (Germany)

- Terumo Corporation (Japan)

- NIPRO (Japan)

- Medtronic (Ireland)

- Medline (U.S.)

- Vygon (France)

KEY INDUSTRY DEVELOPMENTS

- June 2025: Droplet IV, backed by USD 2.0 million in funding, developed an automatic IV line flushing device that ensures full medication delivery by flushing residual drugs trapped in lines when bags empty.

- April 2025: ICU Medical, Inc. introduced a new category of precision IV infusion devices with FDA 510(k) clearances for the single-channel Plum Solo and dual-channel Plum Duo pumps.

- September 2024: Braun SE received FDA 510(k) clearance for the Introcan Safety 2 Deep Access IV Catheter.

- November 2023: BD launched its next-generation PIVO Pro Needle-free Blood Collection Device, now compatible with integrated catheters such as the Nexiva Closed IV Catheter System.

- February 2023: Shenzhen Mindray Bio-Medical Electronics Co., Ltd. launched the BeneFusion i/u Series infusion systems, designed for high precision, adaptive customization, and simplicity to enhance medication safety across clinical settings.

- November 2022: Medtronic launched the world's first and only insulin pump infusion set with up to 7-day wear time in the U.S., doubling the standard 3-day duration.

- July 2022: Braun SE launched the Introcan Safety 2 IV catheter, featuring one-time blood control to automatically reduce blood exposure during insertion and hub access, enhancing clinician safety.

REPORT COVERAGE

The report offers a comprehensive analysis of all market segments, highlighting the key drivers, trends, opportunities, restraints, and challenges influencing industry growth. It also provides insights into technological advancements, the number of healthcare facilities, significant industry developments, market share analysis, and detailed profiles of leading companies.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.2% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, End-user, and Region |

| By Product Type |

|

| By End-user |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global IV Equipment Market value stood at USD 16.84 billion in 2025 and is projected to reach USD 29.11 billion by 2034.

In 2025, the IV Equipment Market value stood at USD 5.22 billion.

The IV Equipment Market is expected to grow at a CAGR of 6.2% over the forecast period (2026-2034).

The IV catheters segment led the market by product type.

The key driver of the market is the rising number of hospitalizations and surgical procedures.

BD, Baxter, B Braun SE, and ICU Medical, Inc. are among the top players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us