Investment Banking Market Size, Share & Industry Analysis, By Service Type (Mergers & Acquisition (M&A), Equity Capital Markets, Debt Capital Markets (DCM), Trading & Brokerage Services, and Underwriting), By End User Industry (Financial Services, Healthcare, Energy & Power, Industrials, Real Estate and Construction, and Others), and Regional Forecast, 2026–2034

INVESTMENT BANKING MARKET SIZE AND FUTURE OUTLOOK

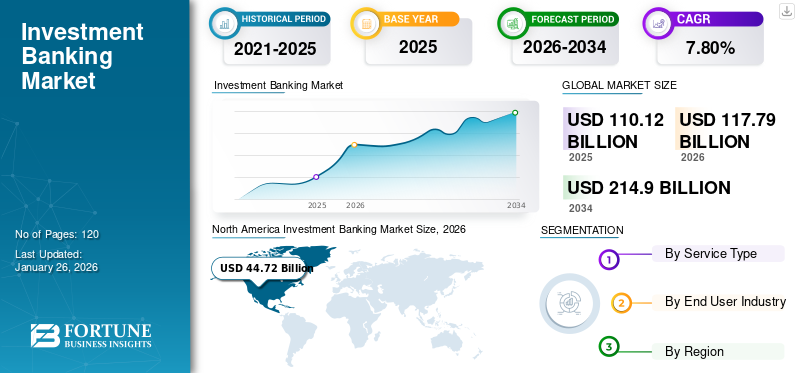

The global investment banking market size was valued at USD 110.12 billion in 2025. The market is projected to grow from USD 117.79 billion in 2026 to USD 214.90 billion by 2034, exhibiting a CAGR of 7.80% during the forecast period.

The global investment bank industry acts as a cornerstone of the financial industry. It facilitates raising capital, mergers and acquisitions, trading, as well as strategic advisory services for corporations, governments, and institutions. The market is cyclical in nature, and is closely related to factors such as macroeconomic trends, interest rate movements, and geopolitical developments. The competitive landscape is majorly dominated by players such as Goldman Sachs, JPMorgan Chase, Morgan Stanley, Barclays, and Bank of America Merrill Lynch, who leverage global reach, advanced data analytics, and diversified portfolios in order to maintain their leadership positions.

Furthermore, the global market is poised for continuous transformation, which is driven by digitalization, increasing demand for ESG advisory, and expanding opportunities in emerging markets such as India. Furthermore, factors including artificial intelligence, automation, and block chain are also completely changing the way trading and compliance functions, while sustainability mandates are further driving banks to provide more innovative financing solutions. In spite of margin compression and increased competition from boutique advisory firms and fintech entrants, global investment banks that are adapting swiftly to rapidly changing client needs and regulatory expectations are likely to retain a competitive edge and capture newer growth avenues.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Generative AI is Reshaping the Investment Bank Landscape

Generative AI is completely altering the global banking market through streamlining operations, improving decision-making abilities, investment, and opening new avenues for client engagement. GenAI is reducing manual workload and boosting efficiency by automating tasks such as financial modeling, pitchbook creation, and market analysis, thus allowing bankers to concentrate more on strategic advisory. It also enables quicker insights from vast datasets, which improve deal sourcing as well as risk assessment. In addition, generative AI improves the overall client experience by personalizing communication and offering dynamic reporting tools. Even though AI presents challenges that are related to data governance and compliance, its integration is quickly becoming a competitive differentiator for the banks that are aiming to innovate and scale.

IMPACT OF TARIFFS

Increase in Volatility in the Market Owing to Recent Reversal of Tariffs

The global investment bank industry has become significantly volatile due to the recent reversal tariffs by the U.S. government. The pause in tariff implementation has momentarily boosted investor confidence. However, it has failed to restore stability in the capital markets completely. Investment activities, especially Mergers & Acquisitions (M&A) as well as equity underwriting, have gone through a sharp decline, with April 2025 recording the lowest M&A activity in over two decades, according to Dealogic. This downturn has further led to estimated bonus reductions of up to 20% for investment bankers. Although trading desks have benefited due to the increased market volatility, the overall uncertainty surrounding trade policies continues to hamper corporate deal-making and investor sentiments, thus creating challenges for the continued growth of the global industry.

Investment Banking Market Trends

Shift Toward Digitalization to Transform Investment Banking Sector

The global market is rapidly shifting toward digitalization, mainly because of advancements in artificial intelligence, big data, and automation technologies. Digital platforms are enhancing efficiency in trading, risk management, and compliance. Additionally, they also offer personalized client services with the help of AI-driven insights. This ongoing trend of digitalization is reconstructing the traditional business models, since investment banks are now embracing technological tools that not only improve their service offerings but also reduce operational costs. Automation is accelerating and simplifying complex processes, such as financial modeling and transaction execution, which has resulted in quicker decision-making. Due to this ongoing trend, firms that fail to adapt to this ongoing digital transformation fall behind and lose their competitive edge.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Investment Banks Expand ESG Offerings to Meet Market Demand

The increasing emphasis on Environmental, Social, and Governance (ESG) factors is driving the demand for specialized advisory services within the IB market. Since the global investors, institutional clients, and governments are prioritizing sustainability, investment banks are trying to expand their ESG offerings to fulfill this demand. This marker is also directly influencing strategic decision-making, with banks playing a major role in advising on green bonds, sustainable financing, and ESG-compliant investments. As the global market for sustainable assets expands, investment banks are using their expertise to take advantage of this shift, further driving the investment banking market growth.

Market Restraints

Regulatory Pressures Challenge Profit Margins of Investment Bank Market

The global industry continues to struggle with the excess of regulations that have been imposed since the 2008 financial crisis. These regulations, which are designed to mitigate systemic risks as well as ensure market stability, often lead to higher compliance costs and operational limitations for the investment banks. In addition, the increased capital reserve requirements, restrictions on trading activities, along with increased scrutiny on cross-border transactions have further made it even more expensive and complex for firms to conduct business. This restraint has also squeezed the profit margins, especially for smaller banks, which lack the resources required to navigate the continuously evolving regulatory landscape as effectively as larger global players do.

Market Opportunities

Expansion in Emerging Markets Presents Growth Potential

Investment banks are aiming toward emerging markets for growth and opportunities, as these regions experience comparatively rapid economic development and urbanization. As governments in these markets invest in infrastructure projects, privatizations, capital-raising initiatives, and demand for investment banking services will rise alongside. Additionally, the rising number of local and multinational companies that are seeking cross-border expansion creates new opportunities for mergers & acquisitions, IPOs, and financial advisory services. Therefore, investment banks that strategically invest in building their presence in these high-growth emerging markets are more likely to benefit from the burgeoning demand for financial services, especially in regions such as Asia Pacific, Latin America, and parts of the Middle East & Africa.

SEGMENTATION ANALYSIS

By Service Type

Strategic Advisory Fees in Technology and Healthcare Boost Mergers & Acquisitions Segment Growth

Based on service type, the market is segmented into Mergers & Acquisition (M&A), equity capital markets, Debt Capital Markets (DCM), trading & brokerage services, and underwriting.

Mergers & Acquisitions (M&A) had the largest investment banking market share in 2026 by 34.06%, as it continues to meet relentless corporate demand for strategic growth, consolidation, and cross-border deals. Investment banks continue to earn strong advisory fees from large transactions in many critical sectors, such as technology and healthcare.

Equity Capital Markets (ECM) is expected to have the highest Compound Annual Growth Rate (CAGR) over the forecast period, reflecting a resurgence of IPO activity, rising investor interest in equities, and more issuers from emerging markets and technology-based companies.

Debt Capital Markets (DCM) remains a critical avenue for sovereign and corporate funding, particularly during a period of rising interest rates.

Trading and brokerage services, which include all trading on behalf of the bank's counterparty or counterparty clients, are benefiting from ongoing market volatility and increasing retail investor participation.

Underwriting services continue to ensure that debt and equity issuance have a healthy amount of capital access, even under changing market conditions.

To know how our report can help streamline your business, Speak to Analyst

By End User Industry

Financial Services Dominate Due to Risk Management Solutions

Based on industry type, the market is segmented into financial services, healthcare, energy & power, industrials, real estate and construction, and others.

Financial services have a dominant share of the global IB market with consistent demand from banks, insurance companies, as well as asset managers for M&A advisory, capital allocation, and risk management solutions. They also maintain a diverse client base with complex financial instruments, as well as a variety of financial stressors, resulting in higher volumes of both transactions and advisory engagements. The segment is expected to dominate the market share of 37.36% in 2026.

Healthcare is estimated to display the highest CAGR in the upcoming forecast period. There has been a resurgence of M&A, funding biotech, and activity related to IPOs, driven by strong interest from investors after the pandemic. This growth is attributable to innovations and regulatory changes, along with increasing needs for capital in the life sciences industry.

Energy & power relies on IB for project financing, restructuring, and sustainability-linked bonds. This segment is anticipated to exhibit a CAGR of 7.19% during the forecast period.

The industrial sector’s expansion is largely due to consolidation and cross-border transactions, and investment bank services that are required for all kinds of automation, driven by the energy transition.

Real estate and construction continue to maintain a relationship with investment banks as they manage services related to REITs, non-public sales of assets, and funding of projects related to infrastructure services.

The others segment captures a comprehensive range of sectors such as technology, media, and various other services, where there is a consistently increasing demand for capital market and advisory services.

INVESTMENT BANKING MARKET REGIONAL OUTLOOK

The market has been studied geographically across five main regions: North America, South America, Europe, Asia Pacific, and the Middle East & Africa.

North America

North America Investment Banking Market Size, 2026 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 40.60% to the global market in 2025, with a valuation of USD 44.72 billion, and is projected to reach USD 47.76 billion in 2026. The global market for investment banking based on having a well-established financial infrastructure, a significant amount of corporate activity, and the presence of many large and established global investment banks. North America continues to lead in terms of M&A advisory, trading, and underwriting services, with the U.S. being the world's center for capital markets and deal-making. The high market share of North America is sustained based on the presence of large pools of capital, some of the most advanced regulatory frameworks, strong private equity, and hedge fund ecosystems.

North America Investment Banking Market Size, 2019-2032 (USD Billion)

The United States continues to be the epicenter of the global investment advisory market and is home to major players such as Goldman Sachs, Morgan Stanley, JPMorgan Chase, and Citigroup. The U.S. investment banking landscape is very competitive. It continues to thrive because of the concentration of corporate headquarters, sophisticated capital markets, as well as its leading position in global M&A, IPOs, and financial innovations. Additionally, an enormous population, an open and dynamic regulatory environment, and a rapid adoption of fintech and artificial intelligence tools provide the U.S. with a further strategic advantage. The U.S. market is projected to reach USD 34.86 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

South America

The market in South America is gradually expanding, as debt restructurings, privatizations, and the renewed interest from investors all help drive activities related to mergers & acquisitions. This region is expected to be the fourth-largest region, accounting for USD 4.23 billion in 2025. Challenges such as political turbulence and regulatory uncertainty continue to exist in the region. Moreover, Brazil and Chile have improved macroeconomic stability, providing favorable conditions for modest growth over the forecast period.

Europe

Europe accounted for USD 33.94 billion in 2025, representing 30.80% of the global market share, and is projected to reach USD 36.42 billion in 2026.

Europe constitutes a developed market with restrained growth potential, but is relatively strong in cross-border M&A activity and capital raising in financial centers such as London, Frankfurt, and Paris. The sale and purchase of businesses will always be restricted by regulatory frameworks and geopolitical headwinds. Still, it is expected to register a steady growth in Europe in conjunction with the necessary financial sector reforms and ESG-powered investments. The UK market is projected to reach USD 12.3 billion by 2026, while the Germany market is projected to reach USD 7.69 billion by 2026.

Middle East & Africa

The market in Middle East & Africa reached USD 3.25 billion in 2025, representing 3.00% of total market revenue, and is projected to reach USD 3.42 billion in 2026. The Middle East & Africa is experiencing slow growth on the back of economic diversification strategies, especially in Gulf States, and an increase in sovereign wealth fund activity and infrastructure financing. The region is also piquing the interest of investment banks globally, at the same time as investment in energy transition and real estate is increasing. The GCC market size is expected to stand at USD 1.89 billion in 2025.

Asia Pacific

The Asia Pacific market was valued at USD 23.99 billion in 2025, capturing 21.80% of global revenue, and is estimated to reach USD 25.74 billion in 2026, primarily driven by emerging economies' growing rates of economic development, the expanding capital markets, and rising levels of corporate activity. Asia Pacific region is to be anticipated as the third-largest market with USD 23.99 billion in 2025. Increasing initial public offering volumes, infrastructure investments, and digital financial innovations are causing the region to be very appealing to global investment banks, as well as regional investment banks, with a strong desire to engage in new opportunities to drive earnings growth. The market value in the Japan market is projected to reach USD 5.14 billion by 2026, the China market is projected to reach USD 9.71 billion by 2026, and the India market is projected to reach USD 4.39 billion by 2026.

Competitive Landscape

KEY INDUSTRY PLAYERS

Extensive Capabilities Along With Global Networks Drive Market Leadership among Top Investment Banks

The dominant companies in the global market can be characterized by their broad global reach, universal service capabilities, large capital base, and advanced technical capabilities. These companies, mostly large multinational banks, provide a full range of services (including M&A advisory services, underwriting services, asset management services, and trading) and capitalize on their strong industry experience, strong client relationships, and comprehensive risk management abilities to maintain the lead. Their adaptability to regulatory changes, investments in digital transformation, and their ability to target emerging markets have positioned them to stay in front and capitalize on growth opportunities in different geographical markets.

Long List of Companies Studied (including but not limited to):

- Goldman Sachs. (U.S.)

- Morgan Stanley (U.S.)

- Bank of America Corporation (U.S.)

- J.P. Morgan Chase & Co. (U.S.)

- Citigroup Inc. (U.S.)

- Barclays (U.K.)

- UBS Group AG (Switzerland)

- Wells Fargo. (U.S.)

- HSBC Holdings plc (U.K.)

- Deutsche Bank AG (Germany)

- BNP Paribas (France)

- Societe Generale S.A. (France)

- Credit Suisse Group AG (Switzerland)

- RBC Capital Markets (Canada)

- Jefferies Financial Group Inc. (U.S.)

- Nomura Holdings, Inc. (Japan)

- Macquarie Group Limited (Australia)

- Lazard (U.S.)

- Evercore (U.S.)

- Rothschild & Co (France)

KEY INDUSTRY DEVELOPMENTS:

- May 2025: Morgan Stanley achieved the best global IPO bookrunner, leading deals of over USD 7 billion in value across 65 IPO engagements, and conducting some high-profile companies to access the public markets in 2024.

- March 2025: Wells Fargo and Deutsche Bank entered the list of top 10 global investment banks by market capitalization in 2025. This reflects the rapidly changing market dynamics and a shift in the competitive landscape among leading financial institutions.

- January 2025: Stifel Financial Corp. entered into a definitive deal to acquire Bryan Garnier, a premier independent European investment bank that specializes in technology and healthcare. The acquisition will add to Stifel's global advisory business and further access key European markets, while also bolstering its skills in M&A advisory and growth funds.

- November 2023: Janney Montgomery Scott announced the acquisition of TM Capital, a leading middle-market investment bank focused on M&A advisory across the business services, industrials, healthcare, and consumer sectors, expanding Janney's investment banking platform and coverage of notable U.S. markets.

- October 2023: Deutsche Bank concluded its acquisition of Numis Corporation Plc, forming 'Deutsche Numis'-a prominent U.K. investment banking platform focusing on advisory, corporate broking, and ECM services, fostering Deutsche Bank's growth and client connections in the U.K.

INVESTMENT ANALYSIS AND OPPORTUNITIES

The global investment bank market identifies itself as a sturdy and transforming investment environment with increased cross-border merger & acquisition activity, more capital raising in both equity and debt markets, and rapidly changing financial services as consumers continue to embrace digitalization and self-service. The cyclical nature of the market is attractive to investors as they can often take advantage of economic recoveries, while also using the market volatility as a barometer to gauge global capital raising sentiment. Advancements in analytics, generative artificial intelligence, and automation are increasing operational efficiency in assessing risks, client servicing, and generating revenues, which are enhancing the margins of large players in the market. The investment banking market's differentiation across the segments of advisory, underwriting, and trading clients gives those firms revenue, despite changes in market conditions.

Furthermore, international opportunities for global businesses are multiplied by economic recovery in emerging markets, especially throughout Asia Pacific, where continued economic activity, early stage corporate activity, and more robust financial markets are increasing demand for investment bank services. This renewed focus on activity in foreign markets, in conjunction with macro trends such as long-term sustainable finance, increased demand for green bonds, and ESG-linked investments, will create new advisory and underwriting opportunities for investment banks. More traditional sectors such as healthcare, technology, and clean energy will continue to observe increased capital activity and create an active pipeline of future transactions and investor returns. All of these facets put the global investment bank market in a very promising position to access long-term strategic investment opportunities.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, service types, and end user industry of the investment banking sector. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.80% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type

By End User Industry

By Region

|

|

Companies Profiled in the Report |

JPMorgan Chase & Co. (U.S.), Goldman Sachs. (U.S.), Bank of America Corporation (U.S.), Morgan Stanley (U.S.), Citigroup Inc. (U.S.), Barclays (U.K.), Wells Fargo. (U.S.), BNP Paribas (France), Deutsche Bank AG (Germany), Jefferies Financial Group Inc. (U.S.) |

Frequently Asked Questions

The market is projected to reach USD 214.90 billion by 2034.

In 2025, the market was valued at USD 110.12 billion.

The market is projected to grow at a CAGR of 7.80% during the forecast period.

By service type, the Mergers & Acquisition (M&A) segment leads the market.

Growing demand for ESG investments is the key factor driving market growth.

JPMorgan Chase & Co., Goldman Sachs, Bank of America Corporation, Morgan Stanley, and Citigroup Inc. are the top players in the market.

North America holds the highest market share.

By end user industry, the healthcare segment is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us