Iron Oxide Market Size, Share & Industry Analysis, By Type (Red Iron Oxide, Yellow Iron Oxide, Black Iron Oxide, and Others), By Application (Building & Construction, Industrial Manufacturing, Consumer Goods, Healthcare, and Others), and Regional Forecast, 2026-2034

IRON OXIDE MARKET SIZE AND FUTURE OUTLOOK

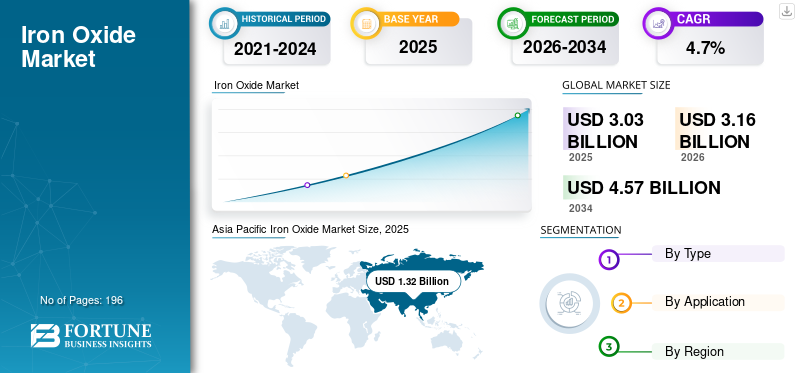

The global iron oxide market size was valued at USD 3.03 billion in 2025. The market is projected to grow from USD 3.16 billion in 2026 to USD 4.57 billion by 2034 at a CAGR of 4.7% during the forecast period. Asia Pacific dominated the iron oxide market with a market share of 43.56% in 2025.

The iron oxide market refers to the global industry involved in the production, distribution, and consumption of iron oxide across different commercial grades and applications. In the broader market context, iron oxide includes not only coloration products but also technical and functional iron oxide materials used where properties such as purity, hardness, reactivity, or magnetism are important. LANXESS explicitly distinguishes its Bayoxide technical iron oxides from pigment-focused products, while JFE Chemical states that it produces iron oxide powders, including nanoscale iron oxide, for magnetic and electronic-material applications.

Key players operating in the market include LANXESS AG, TODA KOGYO CORP., JFE Chemical Corporation, SLB, and OXERRA.

Download Free sample to learn more about this report.

IRON OXIDE MARKET TRENDS

Shift Toward Application-Specific Grades and Higher-Purity Specialty Uses Lead to Market Trend

The trend in the global market is the move away from treating iron oxide only as a low-cost coloring material and toward application-specific grades designed around color consistency, heat stability, purity, weather resistance, and functional performance. LANXESS states that its Bayferrox and Colortherm iron oxide pigments are used across construction, paints and coatings, and plastics, while its Bayoxide line is positioned for technical applications where chemical properties matter more than color. This shows that the market is no longer driven only by bulk coloration demand, but also by more specialized requirements in industrial and technical end uses.

A second trend is the rising importance of cleaner, higher-purity, and compliance-linked iron oxide grades in consumer-facing and regulated applications. The U.S. FDA’s cosmetics regulation states that iron oxides are safe for use in coloring cosmetics generally, including products applied to the eye area, subject to good manufacturing practice. This supports the market’s expansion beyond construction and coatings into cosmetics and other higher-value segments where consistency, impurity control, and regulatory acceptance are important.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Growth in Paints & Coatings Industry Continues to Drives Iron Oxide Demand

The growth of the paints and coatings industry is a major demand driver for iron oxide pigments, primarily due to their functional and aesthetic advantages. Iron oxides are extensively used in architectural coatings for residential and commercial buildings, where they provide durable coloration along with excellent resistance to UV radiation, weathering, and chemical exposure. As construction activity accelerates across emerging economies such as India and Southeast Asia, the demand for decorative paints—both interior and exterior—continues to rise. Additionally, increasing consumer preference for long-lasting, low-maintenance coatings has reinforced the adoption of iron oxide pigments, particularly in exterior applications where color stability and fade resistance are critical.

In the industrial coatings segment, iron oxide pigments play a crucial role in corrosion protection and surface durability, especially in primers such as red oxide coatings used for steel structures, machinery, and infrastructure assets. Sectors including automotive, marine, oil & gas, and heavy equipment are witnessing steady growth, driving the need for high-performance coatings that can withstand harsh operating conditions. Moreover, tightening environmental regulations are encouraging the shift toward eco-friendly and non-toxic pigment alternatives, further strengthening the position of iron oxides over heavy-metal-based pigments. Combined with ongoing maintenance and repainting cycles in developed markets, these factors ensure sustained and stable demand for iron oxide pigments in the global paints and coatings industry.

MARKET RESTRAINTS

Environmental Controls, Workplace Exposure Rules, and Process Costs Can Limit Market Expansion

A major restraint for the iron oxide market is the operational and regulatory burden associated with mining, processing, dust handling, and environmental compliance. USGS notes that the iron oxide pigments industry faces continued cost exposure from environmental compliance, domestic competition, and higher energy costs. Even though iron oxide pigments are valued for stability and nonbleeding performance, manufacturing economics remain exposed to raw material, utility, and compliance pressures, especially in large-scale pigment operations.

This restraint is also relevant because iron oxide production and handling can involve particulate-control requirements, particularly where powder materials are processed at scale. The need for tighter operating discipline, waste handling, and compliance spending can reduce margin flexibility and make expansion more difficult for smaller producers. As a result, the market remains attractive in demand terms, but not all suppliers are equally positioned to scale under stricter cost and environmental conditions.

MARKET OPPORTUNITIES

Specialty Technical Oxides, Cosmetic Grades, and Higher-Performance Industrial Uses Create Premium Growth Space

One of the clearest opportunities in the market is the continued expansion of technical iron oxide uses beyond traditional pigment demand. LANXESS states that Bayoxide is used as a technical iron oxide adsorber for removing arsenic and phosphate from drinking water and wastewater, showing that iron oxide can create value in functional applications where adsorption and chemical behavior matter more than color. This widens the addressable market beyond construction and coatings and creates room for higher-value technical positioning.

Another opportunity lies in high-purity consumer and specialty industrial applications. FDA-permitted use in cosmetics supports demand for iron oxide in beauty and personal-care formulations, while OXERRA emphasizes high-purity grades for coatings, plastics, and specialty applications. This means producers that can supply tighter purity, better dispersibility, and more application-specific grades should be able to defend stronger value realization than suppliers focused only on bulk construction pigmentation.

MARKET CHALLENGES

Demand Diversity Helps, but the Market Remains Highly Competitive and End-Use Specific

A major challenge for the iron oxide market growth is that although it serves many industries, competition is intense because many applications still view iron oxide as a performance-and-cost tradeoff rather than a proprietary material. Construction materials, coatings, plastics, and consumer products all require durable color, but they often also demand price discipline, shade consistency, process compatibility, and long-term supply reliability. This means producers must compete simultaneously on quality, cost, technical support, and regional availability.

The market also faces fragmentation by grade and application. Red, yellow, black, and other iron oxide types are not fully interchangeable across all end uses, and technical oxides used in water treatment or specialty processing have very different requirements from pigment products used in concrete or paints. That makes the market broader than a simple pigment commodity category, but it also raises the complexity of portfolio management, customer qualification, and technical service.

TRADE PROTECTIONISM AND GEOPOLITICAL IMPACT

Trade protectionism and geopolitical tensions can affect the market by increasing uncertainty around raw material costs, energy pricing, cross-border pigment flows, and industrial competitiveness in construction, coatings, and plastics. OECD’s 2024 inventory says export restrictions on industrial raw materials are becoming more common and more prohibitive, with spillovers across downstream supply chains. Iron oxide is not usually treated as a headline critical mineral, but it is part of industrial pigment and specialty-material supply systems that remain exposed to logistics disruptions, trade friction, and shifting cost structures.

This is especially relevant because commercial iron oxide production is globally distributed, while end-use demand is tied to construction, coatings, consumer goods, and industrial manufacturing cycles in many different regions. Changes in freight costs, regional industrial policy, or trade rules can therefore influence delivered pricing and competitive positioning even when underlying end-market demand remains stable.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the market is increasingly centered on shade consistency, purity control, dispersion behavior, weather durability, and application-specific functionality rather than on radical chemistry changes. LANXESS differentiates between pigment families for coloration and technical oxide systems for functional applications, while OXERRA emphasizes high-purity and highly technological grades for coatings, plastics, construction, and specialty uses. This indicates that product development is increasingly focused on performance within the final application system rather than simply producing more colorant volume.

That makes iron oxide R&D strongly application-led. In construction, the focus is on weather resistance, UV stability, and color consistency. In coatings and plastics, the focus is on dispersion, temperature stability, and processing performance. In technical iron oxide applications such as water treatment, the focus is on adsorption efficiency and material behavior in operating conditions. Across the market, development priorities are likely to remain centered on durability, compliance, and better end-use functionality.

SEGMENTATION ANALYSIS

By Type

Red Iron Oxide Dominates Due to Its Broad Suitability and Usage Across Construction Materials

Based on type, the market is segmented into red iron oxide, yellow iron oxide, black iron oxide, and others.

Among these, red iron oxide is expected to hold the dominant share because it is one of the most widely used and commercially established grades in construction materials, coatings, and general industrial coloration. LANXESS specifically highlights iron oxide pigments for concrete components, roof tiles, pavers, and asphalt, while product pages such as Bayferrox 4130 show red iron oxide being used across construction materials, paints and coatings, plastics, and paper.

The yellow iron oxide segment also holds a significant position because yellow and brown shades are widely used in construction and decorative applications. The segment is projected to grow at a positive pace with CAGR of 4.7% during the forecast period.

The black iron oxide remains commercially important in coatings, flooring, industrial materials, and consumer formulations.

The others segment includes brown, orange, blended, and technical iron oxide grades used in niche industrial or specialty applications. Virginia Energy’s iron oxide pigment overview also links red, yellow, brown, and black shades to different iron-bearing mineral forms, reinforcing the practical color-based structure of the market.

By Application

To know how our report can help streamline your business, Speak to Analyst

Building & Construction Leads Due to Iron Oxide’s Long-Established Role in Mineral-Based Materials

Based on application, the market is segmented into building & construction, industrial manufacturing, consumer goods, healthcare, and others.

Among these, building & construction is expected to hold the leading iron oxide market share. This dominance is supported by the long-established use of iron oxide pigments in concrete, precast materials, roof tiles, pavers, and bituminous construction systems. LANXESS explicitly positions Bayferrox pigments for these uses, and OXERRA also highlights strong relevance in the construction industry.

The industrial manufacturing segment is also expected to account for a notable share of the market because iron oxide is used in coatings, plastics, paper, flooring, and technical oxide applications.

Healthcare remains smaller in tonnage but commercially relevant because regulated iron oxide grades are used in cosmetics and related quality-sensitive applications. The segment expected to grow at a CSGR of 3.7% during forecast period.

The others segment includes technical uses such as water treatment adsorbers and additional specialty industrial applications.

IRON OXIDE MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Iron Oxide Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the dominant share of the global market. The region benefits from large construction demand, broad manufacturing depth, strong coatings and plastics consumption, and significant iron oxide production presence.

China Iron Oxide Market

China’s market is one of the largest globally, with 2025 revenue at USD 0.49 billion, representing roughly 16.1% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America is expected to register steady growth during the forecast period. The region benefits from established use of iron oxide in construction products, coatings, industrial materials, and consumer-facing formulations. Demand is supported by infrastructure-related building materials as well as regulated and specialty applications that favor consistent, high-quality iron oxide grades.

U.S. Iron Oxide Market

In 2025, the U.S. represented a USD 0.38 billion market, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 12.5% of global market sales.

Europe

Europe is expected to maintain a significant position in the market due to its mature construction materials industry, developed coatings and plastics sectors, and presence of major iron oxide producers such as LANXESS. The region is especially relevant in higher-performance and specialty-grade iron oxide applications where consistency, technical service, and compliance matter.

Germany Iron Oxide Market

The Germany market in 2025 was valued at around USD 0.19 billion, representing roughly 6.2% of global market revenues.

U.K. Iron Oxide Market

The U.K. market in 2025 was valued at around USD 0.10 billion, representing roughly 3.4% of global market revenues.

Latin America

Latin America is a smaller but relevant market, supported by construction materials, decorative coatings, and general industrial coloration demand. The region does not stand out as the largest global center for iron oxide, but it remains commercially meaningful due to its link to infrastructure development and broad industrial use of durable inorganic pigments.

Brazil Iron Oxide Market

Brazil market in 2025 was valued at around USD 0.14 billion, representing roughly 4.6% of global market revenues.

Middle East & Africa

The Middle East & Africa market remains comparatively smaller, but opportunities exist in construction materials, coatings, and industrial manufacturing. Growth is likely to depend on building activity, infrastructure development, and access to competitively supplied pigment and specialty grades rather than on a very large domestic specialty market base.

GCC Iron Oxide Market

GCC market in 2025 was valued at around USD 0.08 billion, representing roughly 2.8% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Weather Resistance and Regulatory Compliance Among Key Players Strengthens Market Position

The global iron oxide market is moderately fragmented across multinational inorganic pigment producers, regional synthetic iron oxide manufacturers, and a smaller set of companies active in technical and cosmetic-grade iron oxides. Competition is shaped by shade consistency, weather resistance, dispersion behavior, regulatory compliance for sensitive applications, and the ability to supply red, yellow, black, brown, micronized, transparent, and technical iron oxide grades for building & construction, industrial manufacturing, consumer goods, healthcare, and other specialty uses.

LIST OF KEY IRON OXIDE COMPANIES PROFILED IN REPORT

- LANXESS AG (Germany)

- TODA KOGYO CORP. (Japan)

- JFE Chemical Corporation (Japan)

- SLB (U.S.)

- OXERRA (U.S.)

- Sudarshan Chemical Industries Limited (India)

- Heubach Group (Austria)

- Hunan Three-Ring Pigments Co., Ltd. (China)

- Sun Chemical (U.S.)

KEY INDUSTRY DEVELOPMENTS

- June 2025: OXERRA also broke ground on a 120,000 square-foot warehouse at Augusta, Georgia, a distribution investment intended to improve supply-chain reliability for its growing U.S. iron oxide customer base.

- April 2023: OXERRA completed the acquisition of Venator’s iron oxide pigment business and rebranded from Cathay Industries to OXERRA, creating a larger global manufacturing network across six countries on five continents.

- November 2024: TODA KOGYO exhibited CO2 management technology using iron oxide at the COP29 Japan Pavilion Virtual Showcase, highlighting continued development of iron-oxide-linked functional applications beyond traditional pigments.

REPORT COVERAGE

The iron oxide market report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, and application. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion), Volume (Kiloton) |

| Growth Rate | CAGR of 4.7% from 2026 to 2034 |

| Segmentation | By Type, By Application, By Region |

| By Type |

|

| By Application |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 3.03 billion in 2025 and is projected to reach USD 4.57 billion by 2034.

Recording a CAGR of 4.7%, the market is slated to exhibit steady growth during the forecast period.

The building & construction segment is expected to lead market during the forecast period.

Asia Pacific held the highest market share in 2025.

Broad demand across construction, coatings, plastics, and specialty applications drives market growth

- 2021-2034

- 2025

- 2021-2024

- 196

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us