Automotive V2X Market Size, Share & Industry Analysis, By Connectivity Type (DSRC, Cellular), By Communication Type (Vehicle-to-Vehicle (V2V), Vehicle-to-Infrastructure (V2I), Vehicle-to-Pedestrian (V2P), Others), By Vehicle Type (Passenger Cars, Commercial Vehicles), By Unit Type (Onboard Unit, Roadside Unit), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

Automotive V2X Market Outlook & Analysis 2026-2034

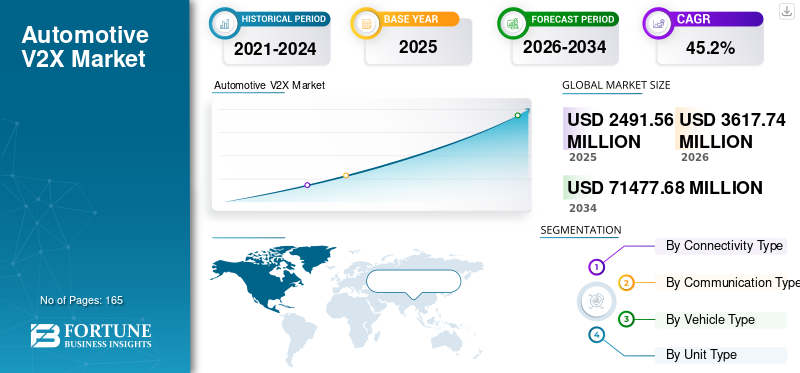

The global automotive V2X market size was estimated at USD 2491.56 million in 2025 and is projected to grow from USD 3617.74 million in 2026 to USD 71477.68 million by 2034, growing at a CAGR of 45.20% from 2026 to 2034. Asia Pacific dominated the automotive V2X market with a market share of 46.21% in 2025. The U.S. market is projected to grow significantly, reaching an estimated value of USD 2847.7 million by 2029.

The automotive V2X market is entering a pivotal stage as connected mobility shifts from pilot deployments toward broader commercial implementation. Rather than serving as a standalone communication technology, Vehicle-to-Everything (V2X) is increasingly positioned as foundational infrastructure supporting cooperative intelligent transportation systems (C-ITS), advanced driver assistance systems (ADAS), and the future evolution of automated driving. According to the European Telecommunications Standards Institute (ETSI) and the 5G Automotive Association (5GAA), standardized V2X communications are expected to strengthen road safety, improve traffic efficiency, and enable interoperability between vehicles, roadside infrastructure, and vulnerable road users.

Market momentum is driven by government-backed intelligent transportation initiatives, expanding deployment of connected road infrastructure, and growing integration of V2X capabilities into next-generation vehicle platforms. Regulatory agencies, including the U.S. Department of Transportation (USDOT), the European Commission, and China's Ministry of Industry and Information Technology (MIIT), continue supporting connected mobility through standards development, pilot corridors, and cooperative transportation programs. These initiatives create value through improved situational awareness, collision avoidance, emergency response coordination, and traffic optimization.

Download Free sample to learn more about this report.

Automotive V2X Market KEY TAKEAWAYS

- 2025 Market Size: USD 2,491.56 million

- 2026 Market Size: USD 3,617.74 million

- 2034 Forecast Market Size: USD 71,477.68 million

- CAGR: 45.20% from 2026–2034

- Asia Pacific dominated the automotive V2X market with a 46.21% share in 2025.

- The DSRC segment accounted for the largest market share.

- The V2V segment accounted for the largest market share.

Asia Pacific

Valued at USD 1,151.24 million in 2025, driven by strong V2X development and autonomous vehicle initiatives in China and Japan.

Europe

Expected to witness steady growth, driven by collaborative V2X research and intelligent transport system initiatives.

North America

Expected to witness significant growth, supported by increasing V2X deployments and smart mobility projects.

U.S.

Expected to witness steady growth, supported by expanding V2X deployment and smart transportation projects.

Japan

Expected to witness strong growth, driven by advancements in V2X and autonomous vehicle technologies.

Read More

Vehicle-to-everything (V2X) enables real-time communication between the vehicle and its surroundings. It includes vehicle-to-vehicle, vehicle-to-pedestrian, and vehicle-to-infrastructure, among other use cases. This technology facilitates autonomous driving, traffic flow optimization, and road safety by enabling vehicles to communicate with each other and the surrounding infrastructure. This increased situational awareness enables more connected and intelligent solutions.

Key Market Dynamics

Market Trends

Increasing Adoption of C-V2X will Positively Influence Growth

Cellular vehicle-to-everything is supported by leading mobile equipment makers, telecommunications operators, and many automakers, including Daimler, SAIC, Ford, Tesla, Audi, PSA, Nissan, BMW, and Lexus. For instance, beginning in 2022, Ford committed to deploying C-V2X in all new U.S. vehicle models, pending the Federal Communications Commission vote on spectrum allocation. The company also planned to deploy this technology in all Ford vehicles in China in 2021. Thus, the increasing adoption of C-V2X will positively influence the growth rate of this market.

Automotive V2X is evolving from isolated connectivity functions toward cooperative mobility ecosystems in which vehicles, roadside infrastructure, cloud platforms, and traffic management centers exchange real-time information to support safer and more efficient transportation. This shift is supported by ongoing standardization efforts from 3GPP, ETSI, and the 5G Automotive Association (5GAA), illustrating how harmonized communication frameworks enable interoperable V2X services across diverse vehicle platforms and road networks. Technology maturity is therefore becoming increasingly dependent on ecosystem integration rather than individual hardware performance.

A notable trend is the growing preference for Cellular Vehicle-to-Everything (C-V2X) as fifth-generation (5G) networks continue expanding globally. According to 3GPP specifications and 5GAA deployment guidance, advanced cellular connectivity supports lower latency, improved network capacity, and future applications involving cooperative perception, automated driving, and real-time traffic coordination. This signals accelerating industry adoption as automotive manufacturers increasingly align V2X development with software-defined vehicle architectures capable of receiving continuous over-the-air updates.

Another important trend is the integration of V2X with advanced driver assistance systems (ADAS), digital mapping, edge computing, and artificial intelligence-enabled traffic management. Rather than operating independently, these technologies increasingly create value through coordinated decision-making across connected transportation environments. Governments are simultaneously expanding intelligent transportation pilots that demonstrate real-world operational benefits before wider commercialization. Taken together, these developments strengthen commercial readiness, enhance competitive advantage, and position organizations to capture future growth potential as connected mobility becomes an integral component of next-generation transportation infrastructure.

Download Free sample to learn more about this report.

Market Drivers

Traffic Safety Benefits Will Drive Growth of Market

According to a 2018 WHO report on road safety, vehicular traffic-related incidents result in more than 1.3 million fatalities every year. According to research conducted by the U.S. Department of Transportation (DOT), road accidents can be reduced by 80% with the help of vehicle-to-everything. It could help reduce road traffic deaths by detecting and alerting the driver of invisible objects.

For instance, an automotive V2X application such as Emergency Brake Light could alert the driver of the following vehicle in advance if it detects sudden deceleration by the leading car in a blind turn, thus avoiding a crash. According to estimates by the U.S. DOT, vehicle-to-everything would save more than 1,000 lives/year and reduce 2.3 million non-fatal injuries. Therefore, these factors will boost the growth of the market.

Road safety policy has become one of the strongest catalysts for automotive V2X deployment, shifting connected vehicle communications from experimental programs toward mainstream transportation infrastructure. According to the U.S. Department of Transportation (USDOT), connected vehicle technologies can improve situational awareness by enabling vehicles to exchange real-time information with surrounding vehicles, infrastructure, and other road users. That capability supports earlier hazard detection, more informed driving decisions, and coordinated traffic management, creating value through cooperative mobility rather than isolated vehicle intelligence.

Economic Savings due to Vehicle-To-Everything to Augment Growth

Congested roads cost around USD 109 billion annually in Europe. The economic savings potential with a safer and more efficient transportation system is enormous. According to the U.S. DOT, annually, around USD 871 billion can be saved in the U.S. with the help of automotive V2X.

Blocked roads cause supply chain delays, increase the complexity and cost of doing business, and lower productivity. With this technology, congestion-causing factors can be detected in advance, and vehicles can react accordingly. By combining simulation models with real-time data, optimized routes can be identified to make rides faster and more efficient. These factors are attributed to the increasing demand for vehicle-to-everything in the automotive industry.

Market Restraints

Challenges Related to Vehicle-To-Everything Testing Will Restrain Growth of the Market

Some of the challenges faced in automotive V2X testing include huge costs in setting up test tracks, actual vehicles, and the infrastructure required for testing. Moreover, setting up high-density traffic with millions of scenarios is practically challenging & cost-intensive. Additionally, certain traffic scenarios are fatal to test with humans. For example, testing of applications such as Abnormal Vehicle Warning (AVW), Control Loss Warning (CLW), and Hazardous Location Warning (HLN). Another challenge with testing is the non-availability of the specific spectrum, a deterrent to testing on real roads, and also replicating test scenarios in the real world is challenging. Hence, these factors will restrain the automotive V2X market growth.

Despite growing policy support, widespread automotive V2X deployment continues to face structural and commercial barriers that influence implementation timelines. One of the most significant challenges is the uneven availability of roadside infrastructure. Vehicle-to-infrastructure communication creates value only when roadside units, traffic signal controllers, and digital traffic management systems are deployed at sufficient scale. According to the U.S. Department of Transportation, connected vehicle benefits increase substantially as both vehicle penetration and infrastructure coverage expand, making coordinated public and private investment essential.

Technology fragmentation remains another restraint. Several regions continue supporting different communication approaches, including Dedicated Short-Range Communications (DSRC) and Cellular Vehicle-to-Everything (C-V2X). Although standards organizations such as ETSI, 3GPP, and the 5G Automotive Association (5GAA) continue advancing interoperability and technology evolution, differing deployment strategies across markets complicate platform standardization for global automotive manufacturers. The result is increased development complexity, longer product qualification cycles, and higher integration costs.

SEGMENTATION

By Connectivity Type Analysis

DSRC Segment Held Largest Market Share Owing to Ease of Implementation

By connectivity type, the market is segmented into DSRC and cellular.

The DSRC segment held the largest market share in 2021 due to ease of implementation, fully designed technology, and verified data security standards. Dedicated Short-Range Communications (DSRC) established the technological foundation for early vehicle-to-everything deployments and continues to maintain relevance in selected intelligent transportation projects where proven low-latency communication and mature standards remain priorities. Based on the IEEE 802.11p standard and supported by deployments initiated by transportation agencies in North America, Europe, and Japan, DSRC demonstrates how direct vehicle communication can enhance collision avoidance, intersection safety, and traffic efficiency without relying on cellular network coverage. While commercial momentum has shifted toward cellular solutions in many regions, DSRC continues to support legacy deployments and infrastructure investments already integrated into connected transportation systems.

The cellular segment is expected to exhibit a higher CAGR in the market during the forecast period. Cellular vehicle-to-everything is a cost-effective and versatile solution that can provide secure short-range and long-range connectivity over a wide area. It offers improved safety features, greater capacity, and lowers the chance of interruptions in service. These factors will fuel the growth of this segment.

Cellular Vehicle-to-Everything (C-V2X) has emerged as the primary growth engine within the automotive V2X market, supported by advances in fourth-generation LTE and fifth-generation (5G) mobile communications defined through 3GPP standards. Unlike earlier communication models, C-V2X enables direct vehicle communication alongside network-assisted services, allowing connected vehicles to exchange information with surrounding traffic, cloud platforms, and intelligent transportation infrastructure through a scalable communications ecosystem. This evolution illustrates how connectivity is expanding beyond safety applications toward comprehensive mobility services.

Automotive manufacturers increasingly prioritize cellular connectivity because it aligns with software-defined vehicle architectures, over-the-air software updates, digital services, and future automated driving capabilities. Telecommunications providers and infrastructure developers are simultaneously expanding 5G coverage, strengthening commercial readiness for advanced V2X applications including cooperative perception, remote driving support, and dynamic traffic management. Customer preferences increasingly favor platforms capable of supporting both immediate safety requirements and future software enhancements throughout the vehicle lifecycle.

By Communication Type Analysis

To know how our report can help streamline your business, Speak to Analyst

V2V Segment Held the Largest Share, Backed by Increasing Demand for Driving Assistance

By communication type, the market is segmented into vehicle-to-vehicle (V2V), vehicle-to-infrastructure (V2I), vehicle-to-pedestrian (V2P), and others.

The V2V segment held the largest share of the market. V2V can provide drivers with other vehicles information, including speed, direction, and location, and alert them to any potential danger in scenarios such as blind spots, heavy traffic, intersections, and terrain issues, among other situations. These factors will drive the growth of this segment.

Vehicle-to-Vehicle (V2V) communication remains the cornerstone of automotive V2X because it enables direct exchange of safety-critical information between nearby vehicles without relying exclusively on centralized traffic management systems. According to the U.S. Department of Transportation (USDOT), V2V applications support collision avoidance by sharing real-time data relating to vehicle speed, position, heading, and braking status. This capability strengthens situational awareness beyond the driver's direct line of sight and creates value through cooperative decision-making that complements onboard sensors such as radar, cameras, and lidar.

The V2I segment is also expected to show considerable growth over the forecast period. V2I can assist the development of driver assistance systems such as autonomous driving and intelligent parking that can enhance future planning of parking lots, traffic lanes, and more to manage optimal traffic flow. This will drive the implementation of V2I technology.

Vehicle-to-Infrastructure (V2I) communication is becoming increasingly important as governments modernize transportation networks with connected traffic signals, roadside sensors, digital signage, and intelligent traffic management systems. Unlike vehicle-centric communication models, V2I creates value through continuous interaction between vehicles and public infrastructure, enabling optimized traffic flow, signal priority management, work-zone warnings, and real-time road condition notifications. According to the European Commission's Cooperative Intelligent Transport Systems (C-ITS) initiative, interoperable infrastructure communication is a key component of future connected mobility.

Vehicle-to-Pedestrian (V2P) communication addresses one of the most critical safety challenges in urban mobility by enabling connected vehicles to detect and communicate with vulnerable road users carrying compatible mobile devices or wearable technologies. This application supports early warning systems for pedestrians, cyclists, and other non-motorized road users, particularly in situations where conventional vehicle sensors may have limited visibility because of buildings, weather conditions, or traffic congestion.

Adoption remains at an earlier stage than V2V or V2I because effective implementation requires broad ecosystem participation involving mobile device manufacturers, application developers, telecommunications providers, municipalities, and transportation agencies. Nevertheless, growing emphasis on road safety initiatives and Vision Zero programs is encouraging governments to evaluate V2P as a complementary safety technology capable of reducing urban traffic incidents.

By Vehicle Type Analysis

Passenger Cars Dominated the Market Owing to Higher Demand Among Private Consumers

Based on vehicle type, the market is segmented into passenger cars and commercial vehicles.

The passenger cars segment held the largest share of the market. Major automakers have already deployed V2X. For instance, Toyota has been instrumental in vehicle-to-everything progress, deploying more than 100,000 Lexus and Toyota vehicles equipped with DSRC technology. Similarly, in Europe, Volkswagen has implemented DSRC-based vehicle-to-everything in its new Golf models. These factors are attributed to the dominance of this segment.

Passenger cars represent the leading vehicle segment for automotive V2X deployment because manufacturers increasingly view connected communication as an essential component of next-generation safety, automation, and digital mobility strategies. The transition toward software-defined vehicles, combined with growing adoption of advanced driver assistance systems (ADAS), is driving integration of V2X capabilities into mainstream vehicle platforms rather than limiting deployment to premium models. According to the European Commission's Cooperative Intelligent Transport Systems (C-ITS) program and the 5G Automotive Association (5GAA), cooperative communication strengthens vehicle awareness by enabling the exchange of real-time safety information among surrounding vehicles and roadside infrastructure.

The commercial vehicles segment is also expected to show considerable growth in the market. Factors such as the potential to reduce collisions, decrease emissions, and improve platooning that can make goods transport more efficient will propel the growth of this segment.

Commercial vehicles are emerging as a strategically important segment because fleet operators increasingly evaluate V2X technology through measurable operational benefits rather than solely safety improvements. Logistics companies, public transportation agencies, emergency service operators, and freight carriers prioritize communication systems that enhance route optimization, reduce congestion, improve fleet coordination, and strengthen driver safety. These operational efficiencies illustrate how V2X creates value beyond collision avoidance by supporting more intelligent transportation management across complex commercial networks.

By Unit Type Analysis

OBU Segment Held Largest Market Share in 2021 Owing to its Low Cost

Based on unit type, the market is segmented into the onboard unit (OBU) and roadside unit (RBU).

The OBU segment held the largest share of the market as it is the essential component necessary for sharing data with other vehicles' OBUs and roadside networks in real-time, and can enable adding applications through its established software platform. The RSU segment is also expected to show good growth in the market due to decreasing deployment cost, helping in managing traffic flow, and improving pedestrian and driver safety, among other applications.

Onboard Units (OBUs) constitute the core vehicle-side component of automotive V2X systems, enabling real-time communication between vehicles, roadside infrastructure, pedestrians, and network services. Their strategic importance has increased as automotive manufacturers integrate connected communication into software-defined vehicle architectures rather than treating connectivity as an optional feature. According to the 5G Automotive Association (5GAA) and 3GPP specifications, OBUs support cooperative awareness, hazard notification, traffic signal interaction, and future automated driving applications by processing and transmitting low-latency safety messages.

Current market adoption is led by passenger vehicle manufacturers and commercial fleet operators investing in next-generation connected mobility platforms. Automotive original equipment manufacturers increasingly prioritize factory-installed OBUs that integrate seamlessly with advanced driver assistance systems (ADAS), telematics control units, navigation systems, and cybersecurity frameworks. Customer preferences are shifting toward multifunctional communication modules capable of supporting software updates, evolving communication standards, and future regulatory requirements throughout the vehicle lifecycle.

Roadside Units (RSUs) represent the infrastructure backbone of the automotive V2X ecosystem by enabling continuous communication between connected vehicles and intelligent transportation systems. Unlike vehicle-installed communication devices, RSUs extend digital awareness beyond the vehicle by connecting traffic signals, road sensors, highway management systems, pedestrian crossings, and traffic control centers. According to the U.S. Department of Transportation's Connected Vehicle Program and the European Commission's Cooperative Intelligent Transport Systems (C-ITS) initiative, roadside infrastructure is fundamental to achieving interoperable cooperative mobility at scale.

Adoption remains closely linked to public-sector investment and long-term transportation modernization strategies. National transportation agencies, municipalities, and highway authorities continue deploying RSUs within connected corridors, smart intersections, freight routes, and urban mobility projects to improve traffic efficiency and road safety. Customer demand increasingly emphasizes scalable infrastructure capable of supporting both current connected vehicle applications and future automated mobility services without requiring extensive hardware replacement.

REGIONAL INSIGHTS

Asia-Pacific Automotive V2X Market Analysis

Asia Pacific dominated the market with a valuation of USD 1151.24 million in 2025 and USD 1671.6 million in 2026. Telecommunication technology providers and automotive OEMs are the key players working on vehicle-to-everything development in this region. Japan and China are expected to lead the Asia Pacific in terms of technology development. For instance, in Chongqing, a vehicle-to-everything pilot zone within 20 square kilometers of Yongchuan district is testing level 4 autonomous vehicles, which can drive almost all the time without human control.

Asia-Pacific demonstrates the strongest market momentum, supported by large-scale intelligent transportation investment, expanding fifth-generation mobile networks, and government-backed connected mobility initiatives. Automotive manufacturers, telecommunications providers, and infrastructure developers continue accelerating commercial deployment across multiple countries. Rapid urbanization, digital infrastructure expansion, and supportive industrial policies position the region to capture significant future growth potential within automotive V2X technologies.

Japan Automotive V2X Market

Japan continues to strengthen automotive V2X through advanced automotive engineering, connected mobility innovation, and intelligent transportation investments. Collaboration among vehicle manufacturers, telecommunications operators, and government agencies supports the deployment of cooperative driving technologies. Continued emphasis on road safety, automated mobility, and digital transportation infrastructure is expected to accelerate commercial readiness and reinforce Japan's leadership in connected vehicle technologies.

China Automotive V2X Market

China continues accelerating automotive V2X deployment through strong government support, nationwide C-V2X initiatives, and rapid expansion of intelligent transportation infrastructure. Automotive manufacturers and technology companies actively collaborate to commercialize connected mobility solutions across urban transportation networks. Growing investment in smart cities, fifth-generation communications, and autonomous driving technologies positions China to strengthen long-term industry adoption and global competitiveness.

Asia Pacific Automotive V2X Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

Europe Automotive V2X Market Analysis

Europe is expected to show good growth in the market. The region witnessed numerous research initiatives, industrial consortiums, and collaborative testing for vehicle-to-everything communication. For instance, the CAR 2 CAR Communication Consortium, comprising multiple technology developers and automakers, focuses on developing intelligent transport systems and implementing them on European roads.

Europe maintains one of the world's most advanced automotive V2X markets through coordinated regulatory frameworks and the European Commission's Cooperative Intelligent Transport Systems initiative. Strong collaboration among vehicle manufacturers, infrastructure providers, and telecommunications companies supports interoperable deployment. Continued investment in connected corridors, intelligent mobility, and harmonized standards is expected to strengthen commercial readiness and expand future transportation connectivity across Europe.

Germany Automotive V2X Market

Germany remains a leading automotive V2X innovation center because of its globally competitive automotive industry, engineering expertise, and connected mobility research programs. Vehicle manufacturers continue integrating V2X capabilities into next-generation software-defined platforms while supporting intelligent transportation initiatives. Strong industrial collaboration, investment in automated driving technologies, and expanding digital infrastructure are expected to reinforce long-term market growth and technology leadership.

United Kingdom Automotive V2X Market

The United Kingdom continues advancing automotive V2X through connected mobility research, intelligent transport projects, and automated vehicle testing programs. Government-supported innovation initiatives encourage collaboration between automotive manufacturers, technology companies, and academic institutions. Continued investment in digital road infrastructure, cybersecurity, and connected transport ecosystems is expected to strengthen commercial deployment while supporting future autonomous mobility applications.

North America Automotive V2X Market Analysis

North America is expected to have significant growth in the market owing to increasing vehicle-to-everything technology deployment by major automakers in this region. In partnership with the Ohio Department of Transportation, Honda is deploying the highest-density V2X environment of its kind with the U.S. State Route 33 Smart Mobility Corridor. Similarly, in partnership with the Virginia DOT, Audi announced a pilot program for cellular vehicle-to-everything deployments starting in Q3 of 2020.

According to the Alliance for Automotive Innovation (AAI), the companies with deployed or announced deployments account for over 60% of the automotive market share in the U.S. in 2019. Hence, these factors will propel the growth of the market in this region.

North America represents a technologically mature automotive V2X market, supported by connected vehicle research, intelligent transportation investments, and regulatory collaboration. The U.S. Department of Transportation continues advancing connected corridor programs and interoperability initiatives that strengthen technology validation. Growing deployment of software-defined vehicles, expanding 5G infrastructure, and increasing public-private partnerships are expected to accelerate commercial readiness and support long-term connected mobility adoption across the region.

United States Automotive V2X Market

The United States leads regional innovation through extensive connected vehicle pilot programs, transportation research, and standards development supported by the U.S. Department of Transportation. Automotive manufacturers, telecommunications providers, and infrastructure developers continue expanding cooperative mobility initiatives. Increasing investment in intelligent transportation systems, cybersecurity, and software-defined vehicles positions the country to strengthen industry adoption and future commercial deployment of V2X technologies.

Latin America Automotive V2X Market Analysis

Latin America remains an emerging automotive V2X market where adoption is supported by transportation modernization, digital infrastructure improvements, and expanding intelligent mobility initiatives. Governments and transportation authorities increasingly evaluate connected vehicle technologies through pilot deployments and smart city programs. Continued investment in communication infrastructure and public-private collaboration is expected to support gradual commercial expansion throughout the region.

Middle East & Africa Automotive V2X Market Analysis

The Middle East and Africa continue developing automotive V2X capabilities through smart city investments, transportation modernization, and digital infrastructure expansion. Governments increasingly support connected mobility initiatives to improve traffic efficiency and road safety. Continued investment in intelligent transportation systems, fifth-generation communications, and public infrastructure is expected to strengthen long-term commercial adoption across the region.

Automotive V2X Industry Competitive Landscape

LG Electronics is a Leading Player in the market due to its Diverse Product and Patent Portfolio.

LG Electronics accounts for the second-largest patent count for this technology behind Qualcomm. It holds the second position regarding C-V2X patents (2,707) and the first position regarding short-range or WLAN-based V2X patents. Hence, a diverse patent portfolio will allow the company to generate significant revenue through its licensing operations.

Competition within the automotive V2X industry is shaped by the convergence of automotive engineering, wireless communications, semiconductor innovation, and intelligent transportation infrastructure. Success increasingly depends on the ability to integrate secure, interoperable, and standards-compliant communication platforms rather than delivering standalone hardware. As commercialization advances, companies are strengthening competitive positioning by aligning product development with 3GPP, ETSI, IEEE, and 5G Automotive Association (5GAA) standards while supporting software-defined vehicle architectures and cooperative intelligent transportation systems.

Global market leaders including Qualcomm Technologies, Continental AG, Bosch, Huawei Technologies, LG Electronics, Harman International, Autotalks, and Keysight Technologies continue advancing end-to-end V2X solutions spanning chipsets, communication modules, onboard units, roadside infrastructure, cybersecurity, and validation platforms. Their strategies illustrate how integrated technology portfolios create competitive advantage by supporting automotive manufacturers, telecommunications operators, and transportation authorities throughout the deployment lifecycle.

Emerging companies increasingly differentiate themselves through specialized semiconductor platforms, edge computing, cybersecurity software, digital traffic management, and infrastructure intelligence. Rather than competing across the entire ecosystem, many focus on high-value applications such as secure communication protocols, cooperative perception, roadside analytics, or software platforms that enhance interoperability between connected vehicles and transportation infrastructure.

Strategic partnerships remain central to industry evolution. Automotive manufacturers continue collaborating with mobile network operators, semiconductor suppliers, mapping providers, and transportation agencies to accelerate technology validation and commercial readiness. Industry organizations such as the 5G Automotive Association (5GAA) further strengthen ecosystem collaboration by promoting interoperable deployment frameworks and cross-industry standardization.

Expansion initiatives increasingly prioritize regional pilot corridors, smart city deployments, and connected freight programs where governments provide long-term infrastructure support. Companies capable of combining advanced communications, functional safety, cybersecurity, cloud connectivity, and scalable software platforms are expected to strengthen market positioning as cooperative mobility matures. This competitive environment continues to reshape industry adoption, encouraging organizations to integrate complementary capabilities while creating long-term value through secure, intelligent, and interoperable connected transportation solutions.

LIST OF KEY COMPANIES PROFILED:

- Denso Corporation (Japan)

- Aptiv (Ireland)

- Infineon Technologies AG (Germany)

- Continental AG (Germany)

- Qualcomm Technologies, Inc. (U.S.)

- Autotalks Ltd. (Israel)

- Cohda Wireless (Australia)

- Kapsch TrafficCom (Austria)

- Savari Inc. (U.S.)

- Lear Corporation (U.S.)

- LG Electronics (South Korea)

- Ford Motor Company (U.S.)

- Robert Bosch GmbH (Germany)

- NXP Semiconductors (Netherlands)

- Harman International (U.S.)

Latest Automotive V2X Industry Developments

- June 2025: Qualcomm Technologies completed its acquisition of Autotalks, adding production-ready, automotive-qualified Vehicle-to-Everything (V2X) communication solutions supporting both DSRC and Cellular V2X (C-V2X) standards. The acquisition strengthens Qualcomm's Snapdragon Digital Chassis portfolio, accelerates global V2X commercialization, and expands safety-focused communication capabilities for connected and automated vehicles.

- July 2025: Continental AG published its "Code Meets the Road" white paper, presenting a framework for software-defined mobility built around verifiable credentials to improve security, privacy, and trust in connected vehicle applications. The initiative supports future V2X-enabled mobility services by strengthening digital identity management and secure communication across connected transportation ecosystems.

- January 2025: Qualcomm Technologies and Hyundai Mobis announced a collaboration to develop next-generation ADAS and digital cockpit platforms by integrating the Snapdragon Ride™ Flex System-on-Chip with Hyundai Mobis' software and sensing technologies. Although broader than V2X alone, the platform enhances connected vehicle capabilities and supports future software-defined vehicle architectures that incorporate cooperative communication technologies.

- January 2025: LG Electronics showcased its latest connected mobility and software-defined vehicle technologies at CES 2025, highlighting advanced telematics, vehicle connectivity platforms, and intelligent mobility solutions designed to support future V2X-enabled transportation services. The developments reinforce LG's strategy of expanding digital vehicle platforms that integrate cloud connectivity, edge computing, and cooperative mobility capabilities.

January 2025: Bosch introduced new software-defined mobility technologies and intelligent transportation solutions at CES 2025, emphasizing integrated vehicle software, advanced connectivity, and digital mobility platforms that support future V2X applications. The initiative strengthens Bosch's long-term strategy to advance connected driving, cooperative traffic management, and automated mobility through scalable software and communication technologies.

REPORT COVERAGE

The global automotive V2X market research report covers a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading product applications. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the factors mentioned above, the report delivers an in-depth market analysis of several factors contributing to its growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Connectivity Type

|

|

By Communication Type

|

|

|

By Vehicle Type

|

|

|

By Unit Type

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 2491.56 million in 2025 and is projected to reach USD 71477.68 million by 2034.

In 2025, the Asia Pacific market value stood at USD 1151.24 million.

The market will exhibit stellar growth with a CAGR of 45.2% during the forecast period (2026-2034).

The DSRC segment held the largest share of the market in 2025.

Rising road traffic safety due to automotive vehicle-to-everything is the key factor driving the growth of the market.

LG Electronics, Qualcomm Technologies, and Ford are the major players in the global market.

Asia Pacific held the largest share in the market in 2025.

Factors such as increasing pedestrian and driving safety, enhanced driving experience, and economic savings due to optimized traffic flow are expected to boost the drive the product adoption during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 165

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us