Small Drone Market Size, Share & Industry Analysis, By End Use (Defense, Consumer, Commercial, and Civil), By Type (Fixed Wing, Rotary Wing, and Hybrid Wing), By Maximum Take-off Weight (Less than 5 kg, 5 - 25 kg, and 25 - 150 kg), By Power Source (Fuel Powered, and Battery Powered), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

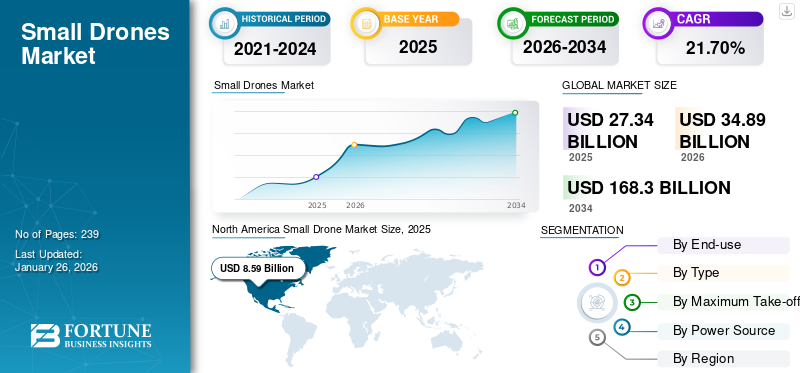

The small drone market size was valued at USD 27.34 billion in 2025 and is projected to grow from USD 34.89 billion in 2026 to USD 168.30 billion by 2034, exhibiting a CAGR of 21.70% during the forecast period. North America dominated the small drone market with a share of 31.44% in 2025.

A small drone is an unmanned aerial vehicle (UAV) designed for relatively short-range flights and small enough to be operated by a single person. These drones are typically lighter and have low maximum weight take-off (MWTO). These drones are commonly referred to as micro-drones, mini-drones, or nano-drones. They are used for various commercial and non-commercial applications, including defense, aerial photography, surveying and mapping, and inspection of infrastructure.

Moreover, small UAVs are powered by either batteries or fuel. They are also equipped with advanced sensors and cameras, including GPS, gyroscopes, accelerometers, and high-resolution cameras to capture detailed images and data about their surroundings. Increased demand for drone-based services from various applications is expected to drive the growth of the global market size from 2025 to 2032. The key players in the market include SZ DJI Technology Co. Ltd., Parrot Drones, AeroVironment Inc., Teledyne Technologies Incorporated, Guangzhou Walkera Technology Co., Ltd., and others. These players are focused on new product development, investments in research and development, along with collaborative activities with government and military agencies to fulfill product demand.

Download Free sample to learn more about this report.

Russia-Ukraine War Impact

The Russia-Ukraine war has significantly influenced the small drone market, which highlights the product application and importance in modern warfare. The countries involved in the warfare have deployed a large number of small drones for surveillance, reconnaissance, and combat operations.

The war has highlighted the increase in demand for small drones, particularly First-Person View (FPV) drones, in targeting enemy assets such as tanks and artillery. For instance, Ukraine announced its plans to triple its FPV drone arsenal in 2025, procuring 4.5 million units for USD 2.6 billion to enhance its defense against Russia. This plan is expected to strengthen the UAV industry and encourage more innovation and production of small drones.

Small drones are used significantly to obtain real-time intelligence and enable precision strikes with minimal risk to personnel. They also provide rapid response times to emergencies and can clear low-priority calls without deploying ground units.

There is an increase in the production capacity of small drones to enhance military capabilities. For instance, in January 2025, the European Union announced that it would provide funding for research into the mass production of kamikaze drones under its 2025 European Defence Fund (EDF) program.

EU to Enhance Small UAV Development for Defense

The European Union is set to increase its focus on the development of small drones for defense purposes. This initiative aims to strengthen the EU's military capabilities in response to evolving security challenges, particularly in light of the ongoing conflict in Ukraine and the need for advanced aerial systems.

Ukraine's Drone Manufacturing Surge

Ukraine has significantly ramped up its domestic drone production capacity, aiming to produce 4 million units annually. This increase is part of a broader strategy to enhance its military capabilities amid ongoing conflict with Russia. The Ukrainian government plans to allocate USD 60 million monthly to combat units for new drones, reflecting the critical role of UAVs in modern warfare.

Focus on Inexpensive War Drones

In light of recent conflicts, there is a push within the EU to invest in inexpensive war drones. European leaders are advocating for partnerships with Ukraine and Turkey, which are recognized as leading drone producers. This strategy aims to bolster Europe's defense innovation and reduce reliance on traditional military hardware.

Market Dynamics

Market Drivers

Rise in Adoption of Small Drones Across Diverse Commercial and Recreational Applications to Boost Market Growth

There are various factors associated with the small drone market growth. Small drones are increasingly being used in commercial applications, and their adoption is significantly transforming various industries. Small drones are being used for crop monitoring, irrigation management, and pest infestation identification. Small drones are transforming traditional farming practices through new applications such as spraying, crop scouting, field mapping, and crop monitoring.

Governments and agricultural industries globally are increasingly investing in drone technology to revolutionize farming practices and improve resource efficiency. According to the Agriculture Drone Industry Insight Report (2023/2024) by DJI, by the end of June 2024, agricultural drones will have treated over 500 million hectares of farmland globally.

Moreover, the liberalization of stringent drone regulations is increasing the adoption of drones for precision agriculture activities. For instance, in Brazil, the National Civil Aviation Agency (ANAC) has simplified drone regulations, requiring only registration of the drone and pilot licensing before operations can commence. Therefore, such favorable policies are expected to simplify drone regulations, which is further accelerating the adoption of small drones for conducting safer and more efficient farming operations.

Various industries such as oil & gas, railways, and construction are utilizing small drones for inspection applications. Small drones are used for efficient and time and labor-saving inspection of pipelines, storage tanks, and power lines. For instance, in December 2024, Scout 137 Drone System was used to inspect FPSO cargo tanks in the Gulf of Mexico, achieving 100% BVLOS (Beyond Visual Line of Sight) operations without human entry. This approach drastically reduced inspection time from 5–7 days to 2–3 hours per tank and minimized crew size from 6–8 people to just 2–3. Therefore, the rise in the use of small drones to perform efficient, safe, and cost-effective inspections drives demand for small drones in industrial applications.

Market Restraints

Regulatory Challenges to Hamper the Growth of the Market

One of the primary restraints to the growth of the small drone market is the stringent regulatory framework that governs drone operations across various countries. Many governments impose strict rules that require drone operators to obtain specific certifications and licenses. For instance, in 2024, European drone regulations introduced mandatory C classification markings for all new drones, ensuring compliance with operational and safety standards. Remote identification became compulsory, allowing authorities to track drones and enhance airspace security.

The stringent regulatory framework governing drone operations presents a significant challenge to the growth of the small drone market. Companies must navigate complex compliance requirements to ensure their products meet safety and operational standards. For instance, in December 2024, Autel Robotics achieved C0 certification for its EVO Nano series, demonstrating adherence to the European Drone Regulation (EU) 2019/945. This certification process involved rigorous testing and a firmware update, allowing the drone to operate in the 'Open Category' A1 sub-category.

However, the path to compliance can be time-consuming and resource-intensive. Manufacturers must invest considerable time and effort into meeting these regulatory demands, which can deter smaller companies from entering the market or hinder existing companies from innovating.

Moreover, the inconsistency of drone laws across different regions adds another layer of complexity, making it difficult for companies to scale their operations internationally, which is expected to hamper the growth of the market.

Market Opportunities

Integration of Advanced Technologies such as AI and Autonomous Capabilities to Create Market Opportunities for Small Drones

The integration of Artificial Intelligence (AI) and autonomous capabilities into small drones is creating significant opportunities across various industries. AI enhances drone functionality by enabling autonomous navigation, obstacle avoidance, and real-time decision-making without human intervention. This capability is making drones perform complex tasks such as precision mapping, infrastructure inspection, and search-and-rescue operations with high efficiency and accuracy.

There is an increase in demand for AI-powered drones in commercial industries and various critical military operations. For instance, in January 2025, the Indian Army started using AI-powered drones and satellite systems for surveillance, logistics, and real-time intelligence gathering.

To meet this increased demand, small drone manufacturers are integrating artificial intelligence (AI) to transform small drones into intelligent systems capable of performing complex tasks autonomously and efficiently.

For example, ANAFI Ai, a 4G robotic UAV designed by Parrot (France-based drone manufacturer), is equipped with AI technology advantage features such as computer vision for object detection, autonomous navigation using SLAM (Simultaneous Localization and Mapping), and real-time data analysis.

Small Drone Market Trends

Increase in Use of Drones in Drone Responder Programs is the Latest Market Trend

As the capabilities of small drones keep evolving, the significant trend is the use of drones as first responders for maintaining public safety. The Drone as a First Responder (DFR) trend is transforming the emergency response systems with the integration of small drones into traditional public safety frameworks.

This innovative approach allows first responders to use aerial technology, such as small drones, for enhanced situational awareness and quicker response times during emergencies.

DFR programs are using drone technology to provide real-time aerial situational awareness. For instance, Flying Lion (U.S.-based drone service provider) announced that it has completed 55,773 Drone as First Responder (DFR) flights, with over 35,000 of these flights conducted Beyond Visual Line of Sight (BVLOS). Therefore, the increase in the use of small drones in emergency response is expected to drive the demand for small drones in public safety applications.

Drone manufacturers are actively innovating to support the Drone as a First Responder (DFR) trend by integrating advanced technologies and designing drones specifically for emergency response scenarios. For instance, in February 2025, Skydio launched DFR Command, a comprehensive software solution for Drone as First Responder (DFR) programs.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By End Use

Defense Segment Dominated the Market Due to the Increased Demand for Surveillance and Monitoring for Military Applications

By end use, the market is classified into defense, consumer, commercial, and civil.

The defense segment is expected to dominate the market share of 39.77% in 2026 and to be the fastest-growing segment during 2026-2034 due to the increased demand for real-time surveillance and monitoring for military applications globally.

The commercial segment is anticipated to witness second second-highest growth during the forecast period due to the rising demand for aerial photography and videography. Furthermore, increasing demand for drone applications in renewable energy and oil & gas is also expected to foster the growth of the segment over the forecast period.

By Type

To know how our report can help streamline your business, Speak to Analyst

Rotary Wing Segment Commanded the Market Owing to Its Versatility, Lightweight Design, and Accessibility

Based on type, the market is segmented into fixed wing, rotary wing, and hybrid wing.

The rotary wing segment is projected dominated the market share of 73.02% in 2026. Rotary wing drones are also known as quadcopters, are one of the types of unmanned aerial vehicle (UAVs) that utilizes four rotors or propellers to lift and maneuver in the air. This segment is also estimated to be the fastest growing during the forecast period due to their lightweight design and their flight stability, which makes them suitable for various applications.

Fixed wing is another type of UAV that has a rigid structure with wings similar to an airplane. Unlike rotary wing drones, fixed wing drones rely on forward motion to generate lift and stay aloft. Fixed wing segment is expected to register significant growth during the forecast period due to increasing package delivery and transportation use, due to its ability to fly longer distances.

By Maximum Take-off Weight

25-150 Kg Segment Takes the Lead, Owing to the Demand for Search and Rescue and Industrial Inspections

The maximum power take-off segment is categorized into less than 5kg, 5 – 25 kg, and 25 – 150 kg.

The 25-150 Kg segment is expected to dominates the market share of 36.49% in 2026 and to be fastest fastest-growing segment during the forecast period. Heavier drones are often employed in military applications requiring substantial operational capabilities, such as reconnaissance missions or equipment transport. In March 2024, Parallel Flight Technologies (PFT), a U.S.-based heavy-lift hybrid drone manufacturer, received an order from Alpha Drones USA, an industrial drone services provider, for five units of its hybrid heavy-lift Firefly UAV, with an option for 20 more in the next year. The Firefly with 122 kg MTOW is capable of carrying a 45 kg payload for up to 1.6 hours.

The 5-25 kg segment has the second-largest share in the maximum power take-off segment. Drones in this weight class are increasingly used for professional photography, surveying, and agricultural monitoring due to their balance of payload capacity and operational flexibility. Many regions have less stringent regulations for this category compared to heavier drones, facilitating easier market entry.

By Power Source

Battery Powered Segment is Anticipated to Command the Market Owing to the Growing Advancements to Improve Battery Life

By power source, the market is categorized into fuel powered and battery powered.

The battery powered segment is expected to dominate the market share of 79.70% in 2026. Advances in battery technology and battery life are increasing flight times and reducing charging times, making battery-powered drones more competitive across various applications. In December 2024, the Defense Innovation Unit (DIU) launched the Family of Advanced Standard Batteries for Unmanned Systems (FASTBAT-U) initiative, which aims to enhance energy storage solutions for small drones.

The fuel powered segment is anticipated to witness significant market share during the study period. Fuel-powered drones typically have longer flight times compared to battery-powered models, making them suitable for extensive missions without frequent recharging. They can often carry heavier payloads due to the energy density of fuel compared to batteries, appealing to commercial logistics sectors.

SMALL DRONE MARKET REGIONAL OUTLOOK

In terms of geography, the market is divided into North America, Europe, Asia Pacific, and the Rest of the World.

North America

North America Small Drone Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America contributed approximately USD 8.59 billion to the global market in 2025, accounting for 31.44% share, and is expected to reach USD 10.8 billion in 2026. This growth is attributed to the presence of Major OEMs in the region and the increasing government contracts to expand its military power. For instance, in December 2024, XTEND (military tactical drone provider) secured a USD 8.8 million contract from the U.S. Department of Defense to supply its Scorpio 500 drones, designed for precision indoor & outdoor strikes. The Scorpio 500 features AI-driven capabilities, a payload capacity of 500 grams, which will be used for precision strike operations. The U.S. market is projected to reach USD 9.41 billion by 2026.

Asia Pacific

The Asia Pacific region captured 31.57% of the global market in 2025, generating USD 8.63 billion in revenue, and is projected to reach USD 11.25 billion in 2026. This regional market growth is due to increasing demand for agriculture crop monitoring and surveying. For instance, in January 2025, DroneShield announced three separate contracts totaling USD 11.8 million for delivery to a military customer in Asia Pacific country. These systems include vehicle-mounted and fixed counter-unmanned systems, indicating a significant increase in demand for drone defense technology. The Japan market is projected to reach USD 1.88 billion by 2026, the China market is projected to reach USD 4.78 billion by 2026, and the India market is projected to reach USD 1.9 billion by 2026.

Europe

In 2025, the Europe market stood at USD 6.71 billion, representing 24.54% of global demand, and is projected to grow to USD 8.65 billion in 2026. This region's high market growth is attributed to the rising demand owing to the Russia-Ukraine war. For instance, in April 2024, the Latvian-U.K. led Drone Coalition raised USD 541.8 million to support Ukraine, aiming to provide 1 million drones for battlefield use. Latvia has already sent the first batch of unmanned aerial vehicles and pledged at least USD 10.8 million annually to the initiative. Therefore, an increase in demand for combat drones to strengthen the defense capabilities of Ukraine is expected to drive market growth. The UK market is projected to reach USD 1.34 billion by 2026, and the Germany market is projected to reach USD 1.49 billion by 2026.

Rest of the World

In 2025, Rest of the World represented USD 3.4 billion, accounting for 12.45% of the worldwide market, and is projected to grow to USD 4.19 billion in 2026. The rest of the world is anticipated to witness moderate growth in the market during the forecast period. The growth is owing to the growing mining and exploration industries. Small drones are ideal for exploring and survey mines and other resources, leading to increased efficiency and cost savings.

COMPETITIVE LANDSCAPE

KEY MARKET PLAYERS

Technological Advancements and Product Developments are a Key Focus of Leading Players

The global small drone market is fragmented with key players, such as SZ DJI Technology Co., Ltd., Parrot Drones, AeroVironment Inc., Teledyne Technologies Incorporated, and Guangzhou Walkera Technology Co., Ltd. Key players are focused on technological advancements, product innovations, development of cost-effective drones and expansions into emerging markets to increase their market share and gain competitive edge.

List of Key Small Drone Companies Profiled

- SZ DJI Technology Co., Ltd. (China)

- Parrot Drones SAS (France)

- AeroVironment Inc. (U.S.)

- Teledyne Technologies Incorporated (U.S.)

- Guangzhou Walkera Technology Co., Ltd (China)

- Yuneec (China)

- Northrop Grumman Corporation (U.S.)

- BAE Systems (U.K.)

- Elbit Systems Ltd. (Israel)

- Skydio, Inc. (U.S.)

- Autel Robotics (China)

- Ehang Holdings Limited (China)

KEY INDUSTRY DEVELOPMENTS

- February 2025 – Parrot Drone S.A.S. unveiled a partnership with the Belgian army to provide their ANAFI USA Drone to the army for their reconnaissance missions. The drone is well equipped with 32X zoom and paired with Flir’s Boson thermal camera for operational efficiency.

- January 2025 – SZ DJI Technology Co. Ltd., a pioneer in small drone technology, launched a new compact drone called Flip that has a flying capacity of 30 minutes. It additionally includes a Flip Parallel Charging Hub that allows you to utilize two batteries simultaneously, which means you can swiftly replace the spare battery for longer durations.

- November 2024 – Teledyne Flir was selected as the primary thermal camera provider for Red Cat Holding to provide AI-powered thermal imaging software for Black Widow for the U.S. Army’s SSR awards program.

- October 2024 – AeroVironment Inc. unveiled a new generation e-VTOL drone. The new drone is said to be made to meet the service’s future reconnaissance needs.

- April 2024 – The Ukrainian Ministry of Defense unveiled the purchase of over 4,000 China-origin drones. These drones were purchased from SZ DJI Technology Co., Ltd, in a contract worth USD 14 million.

REPORT COVERAGE

The report outlines competitive dynamics by assessing business segments, product offerings, target market earnings, geographical reach, and significant strategic initiatives by leading manufacturers. The global market analysis provides a detailed insight into the market expansion activities. Besides this, the report offers insights into the global small drone market size, trends. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 21.70% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation

|

By End Use

|

|

By Type

|

|

|

By Maximum Take-off Weight

|

|

|

By Power Source

|

|

|

By Region

|

Frequently Asked Questions

As per the Fortune Business Insights study, the global market size was valued at USD 34.89 billion in 2026 and is anticipated to reach USD 168.30 billion by 2034.

The market is likely to grow at a CAGR of 21.70% during the forecast period (2026-2034).

The top leading players in the industry are SZ DJI Technology Co. Ltd., Parrot Drones, AeroVironment Inc., Teledyne Technologies Incorporated, and Guangzhou Walkera Technology Co., Ltd.

North America dominated in the market in 2025.

The defense segment is expected to be the fastest growing segment during 2026-2034.

The rise in adoption of small drones across diverse commercial and recreational applications to boost market growth.

Regulatory challenges to hamper the growth of the market.

- 2021-2034

- 2025

- 2021-2024

- 239

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us