Lightweight Packaging Market Size, Share & Industry Analysis, By Material (Plastic, Paper & Paperboard, Metal, Glass, Others), By Packaging Type (Films & Wraps, Bags & Pouches, Boxes & Cartons, Cans, Trays & Clamshells, Others), By End-use Industry (Food & Beverages, Healthcare, Personal Care & Cosmetics, Consumer Goods, Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

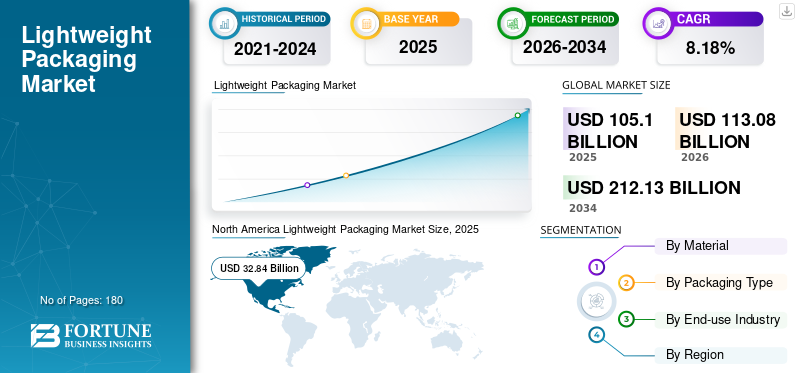

The global lightweight packaging market size was valued at USD 105.10 billion in 2025. The market is projected to grow from USD 113.08 billion in 2026 to USD 212.13 billion by 2034, exhibiting a CAGR of 8.18% during the forecast period. North America dominated the global lightweight packaging market with a market share of 31.25% in 2025.

Lightweight packaging refers to the design and implementation of packaging solutions that minimize material consumption and total package weight, while maintaining necessary performance, product protection, safety, and functionality standards. The swift growth of e-commerce has heightened the need for packaging that provides both safety and lower shipping expenses, thus driving the global market growth.

Furthermore, many key industry players, such as Amcor Plc, Sealed Air, and Mondi, operating in the market, are focusing on developing various innovative products and conducting R&D activities.

Download Free sample to learn more about this report.

LIGHTWEIGHT PACKAGING MARKET TRENDS

Integration of Sustainability and Cost Efficiency is a Prominent Trend Observed in Market

The combination of sustainability and cost efficiency has emerged as a pivotal trend in the sector, significantly altering the approach to packaging decision-making. Instead of viewing sustainability merely as a compliance-related or image-enhancing effort, businesses are progressively incorporating it into their fundamental cost-optimization strategies. Moreover, the fusion of sustainability and cost efficiency is impacting procurement and supplier strategies. Brands and converters are increasingly favoring suppliers who can demonstrate material efficiency, reduced carbon intensity, and competitive pricing simultaneously.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Sustainability-Led Material Reduction is Hastening Market Growth

The primary motivator for lightweight packaging market growth is the global initiative to reduce material intensity per unit of packaging. Governments, brands, and retailers are emphasizing packaging designs that utilize fewer raw recycled materials while still ensuring performance. Lightweighting effectively reduces carbon emissions throughout manufacturing and transportation, aligning with corporate net-zero objectives and circular economy requirements. This motivator is both structural and long-term, as reducing materials is frequently the initial and most economical sustainability strategy accessible to packaging manufacturers.

MARKET RESTRAINTS

Higher Cost of Advanced Lightweight Materials Hampers Market Growth

Certain applications, such as carbonated drinks, liquid foods, or delicate pharmaceuticals, still require minimum material thresholds to ensure safety and functionality. These technical limitations constrain the extent to which lightweighting can be advanced without the need to redesign materials or formats. Numerous contemporary lightweight solutions depend on sophisticated polymers, specialized paper grades, coatings, or engineered films. These packaging materials frequently have a higher cost per kilogram compared to traditional alternatives and necessitate meticulous processing controls. For markets that are sensitive to costs and for smaller manufacturers, the initial investments in materials and equipment can hinder adoption.

MARKET OPPORTUNITIES

Brand-Led Packaging Redesign Initiatives Provide Market Growth Opportunities

Brand-driven packaging redesign efforts have emerged as a crucial growth factor for the global lightweight package sector, driven by demand for sustainability, cost efficiency objectives, and shifting consumer demands. Major consumer-oriented brands, particularly in the food and beverage, personal care, home care, and pharmaceutical industries, are actively rethinking their packaging strategies rather than waiting for regulatory mandates. Lightweight concept frequently serves as the initial and most scalable approach in these redesign initiatives, as it provides quantifiable environmental and economic advantages without modifying the product itself.

MARKET CHALLENGES

Balancing Lightweighting with Regulatory Compliance Poses a Critical Challenge to Market Growth

Achieving a balance between lightweighting and adherence to regulatory standards represents one of the most significant and intricate challenges within the global lightweight package sector. Although minimizing material usage provides evident environmental and financial advantages, packaging must still meet rigorous regulations concerning product safety, consumer protection, environmental impacts, and transport integrity. These regulatory stipulations often establish minimum performance criteria that limit the extent to which lightweighting can be implemented without compromising compliance.

Segmentation Analysis

By Material

Versatility, Performance, and Cost Efficiency to Propel Plastic Segmental Growth

Based on the material, the market is divided into plastic, paper & paperboard, metal, glass, and others.

The plastic segment is anticipated to account for the largest share of the market. The segment of plastic materials leads the market due to its unparalleled combination of low weight, high performance, design flexibility, and cost effectiveness across various applications. Plastics facilitate substantial material reduction while maintaining functionality, rendering them the most viable option for extensive lightweighting efforts.

The paper and paperboard segment is expected to grow at a CAGR of 8.26% over the forecast period.

By Packaging Type

Material Efficiency and High-Volume Applicability Boosted Segment Growth

Based on packaging type, the market is segmented into films & wraps, bags & pouches, boxes & cartons, cans, trays & clamshells, and others.

In 2025, the films & wraps segment dominated the global market. The segment of films & wraps in packaging types leads the market, as it embodies the most material-efficient packaging solution available, providing necessary protection with the least amount of material per unit. In contrast to rigid formats, films and wraps fulfill packaging goals such as containment, protection, and extending shelf life while contributing minimal weight, thus inherently supporting lightweighting strategies.

The bags & pouches segment is projected to grow at a CAGR of 8.34% over the forecast period.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Volume, Safety, and Cost Efficiency Drive Segmental Growth

Based on the end-use industry, the market is segmented into food & beverages, healthcare, personal care & cosmetics, consumer goods, and others.

The food & beverages segment is expected to hold a dominant market share over the forecast period. The food & beverages sector leads the market, primarily due to its substantial consumption volume, stringent safety regulations, and ongoing pressure to reduce costs throughout the value chain. No other end-use sector compares to the food and beverages sector regarding packaging intensity, usage frequency, and global scale, which means that even small lightweighting initiatives can have a significant impact. Another key factor driving this trend is the rapid turnover and mass production characteristics of food and beverage items.

The healthcare segment is projected to grow at a CAGR of 8.26% over the forecast period.

Lightweight Packaging Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Lightweight Packaging Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant lightweight packaging market share in 2024, valued at USD 30.35 billion, and maintained its leading position in 2025, with a value of USD 32.84 billion. In North America, the push for lightweight package is primarily driven by cost efficiency, readiness for regulations, and robust sustainability commitments made by brands. Major FMCG and retail companies are actively engaged in lightweighting to lower transportation expenses, enhance supply chain efficiency, and achieve voluntary sustainability goals.

U.S Lightweight Packaging Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 26.38 billion in 2025, accounting for roughly 25.10% of global lightweight package sales.

Asia Pacific

Asia Pacific is estimated to reach USD 27.89 billion in 2025 and secure the position of the second-largest region in the market. In the region, India and China are both estimated to reach USD 7.53 billion and USD 8.98 billion, respectively, in 2025. In the Asia Pacific region, the demand for lightweight package is driven by significant growth in consumption, cost sensitivity, and the ability to scale manufacturing. The swift pace of urbanization, the rise of middle-class populations, and a heightened demand for packaged food, beverages, and personal care items result in substantial volumes of packaging.

Japan Lightweight Packaging Market

The Japanese lightweight packaging market in 2025 is estimated to be around USD 5.30 billion, accounting for roughly 5.05% of global lightweight packaging solutions revenues. The market in Japan is propelled by the principles of resource efficiency, space optimization, and engineering precision.

China Lightweight Packaging Market

China’s lightweight packaging market is projected to be one of the largest worldwide, with 2025 revenues estimated at around USD 8.98 billion, representing roughly 8.54% of global sales.

India Lightweight Packaging Market

The Indian lightweight packaging market in 2025 is estimated to be around USD 7.53 billion, accounting for roughly 7.17% of global revenues.

Europe

Europe is projected to record a growth rate of 7.65% in the coming years, which is the third highest among all regions, and reach a valuation of USD 21.13 billion by 2025. The European lightweight package market is primarily influenced by regulatory pressures and alignment with circular economy principles. Stringent environmental regulations, directives concerning packaging waste, and mandates for recyclability necessitate that manufacturer’s decrease material usage while guaranteeing recyclability.

U.K Lightweight Packaging Market

The U.K. lightweight packaging market in 2025 is estimated to be around USD 3.82 billion, representing approximately 3.63% of global revenues.

Germany Lightweight Packaging Market

Germany’s lightweight packaging market is projected to reach approximately USD 4.48 billion by 2025, equivalent to around 4.26% of the global market.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 14.77 billion in 2025. Budget limitations and distribution obstacles influence the demand for lightweight packages in Latin America.

South Africa Lightweight Packaging Market

South Africa is set to reach a value of USD 2.42 billion in 2025.

Saudi Arabia Lightweight Packaging Market

The Saudi Arabian market is projected to reach approximately USD 2.73 billion by 2025, accounting for roughly 2.59% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Focus on Expanding Product Launch and Acquisitions by Key Players to Propel Market Progress

The market holds a semi-consolidated market structure, constituting prominent players such as Amcor Plc., Sealed Air, and Mondi. The significant market share of these companies is due to numerous strategic activities, including collaboration among operating entities to advance research activities.

- For instance, in October 2025, Mondi developed a groundbreaking banana box packaging solution that is lighter yet equally robust and more sustainable. This achievement is the result of close collaboration with partners throughout the value chain. The outcome is a box constructed with approximately 40% recycled fiber and weighing up to 10% less than the prior design, which aids in reducing emissions during transportation while ensuring the protection of the fruit.

Other notable players in the global market include Smurfit Kappa, DS Smith, and Ball Corporation. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY LIGHTWEIGHT PACKAGING COMPANIES PROFILED:

- Amcor Plc (Switzerland)

- Sealed Air (U.S.)

- Mondi (U.K.)

- Smurfit Kappa (Ireland)

- DS Smith (U.K.)

- Ball Corporation (U.S.)

- Crown Holdings, Inc. (U.S.)

- Tetra Pak International S.A. (Switzerland)

- Huhtamaki Oyj (Finland)

- Sonoco Products Company (U.S.)

- UFlex Ltd. (India)

- ALPLA Group (Austria)

- Ardagh Group (Luxembourg)

- Constantia Flexibles (Austria)

- Gerresheimer AG (Germany)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Amcor revealed that the user-friendly, eco friendly, and lightweight design of its Sava Flip Top closure is a primary factor in Kotlin's choice, one of the leading Polish ketchup brands. Kotlin, produced by Maspex, which is among the largest food and drink manufacturers in Central and Eastern Europe, is a contemporary brand with a deep-rooted tradition.

- May 2025: Mondi and ZARELO collaborated to launch a recyclable paper-based packaging solution for fire starters intended for use in fireplaces and barbecues. This smooth shift to lightweight paper-based packaging demonstrates a robust partnership founded on trust and expertise, further emphasizing both companies' commitment to innovative and circular packaging solutions.

- August 2024: Sealed Air launched the BUBBLE WRAP brand Ready-To-Roll Embossed Paper, which merges the established efficiency of BUBBLE WRAP brand cushioning with embossed paper that is recyclable at the curbside. Ideal for packing station settings, this robust and lightweight solution adapts to various shapes while providing wrapping and protection.

- November 2024: Sealed Air Corporation, in collaboration with Bradbury’s Cheese, has unveiled a significant advancement in sustainable packaging through the introduction of the CRYOVAC AutoWrap Lite. This innovative system reduces plastic consumption by up to 65% compared to conventional thermoformed packaging, marking a notable achievement in sustainable packaging solutions.

- June 2022: Ball Corporation introduced a new aluminum aerosol can crafted from its lightweight ReAl alloy, which includes 50% recycled content and aluminum produced using renewable energy sources, aiming to reduce the package's carbon footprints by half.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.18% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Material, Packaging Type, End-use Industry, and Region |

|

By Material |

· Plastic · Paper & Paperboard · Metal · Glass · Others |

|

By Packaging Type |

· Films & Wraps · Bags & Pouches · Boxes & Cartons · Cans · Trays & Clamshells · Others |

|

By End-use Industry |

· Food & Beverages · Healthcare · Personal care & Cosmetics · Consumer Goods · Others |

|

By Region |

· North America (By Material, Packaging Type, End-use Industry, and Country) o U.S. o Canada · Europe (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Germany o U.K. o France o Italy o Spain o Russia o Poland o Romania o Rest of Europe · Asia Pacific (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o China o Japan o India o Australia o Southeast Asia o Rest of Asia Pacific · Latin America (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Brazil o Mexico o Argentina o Rest of Latin America · Middle East & Africa (By Material, Packaging Type, End-use Industry, and Country/Sub-region) o Saudi Arabia o UAE o Oman o South Africa o Rest of Middle East & Africa |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 105.10 billion in 2025 and is projected to reach USD 212.13 billion by 2034.

In 2025, the market value stood at USD 32.84 billion.

The market is expected to exhibit a CAGR of 8.18% during the forecast period of 2026-2034.

By material, the plastic segment is expected to lead the market.

Shifting consumer preferences toward eco-conscious brands are driving the market growth.

Amcor Plc, Sealed Air, and Mondi are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us