Liquid Silicone Rubber Market Size, Share & Industry Analysis, By Grade (Industrial Grade, Medical Grade, and Food & Contact Grade), By End Use (Automotive & Transportation, Medical & Healthcare, Electrical & Electronics, Consumer Goods, Industrial Machinery & Components, and Others), and Regional Forecast, 2026-2034

Liquid Silicone Rubber Market Size and Future Outlook

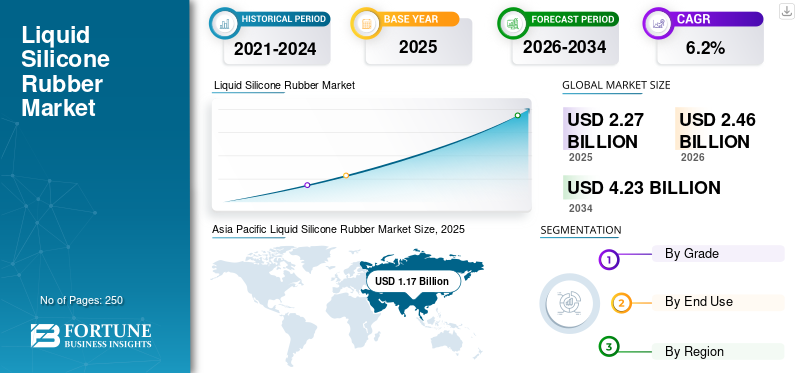

The global liquid silicone rubber market size was valued at USD 2.27 billion in 2025. The market is projected to grow from USD 2.46 billion in 2026 to USD 4.23 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period. Asia Pacific dominated the liquid silicone rubber market with a market share of 51.54% in 2025.

Liquid Silicone Rubber (LSR) is a two-part, platinum-cured silicone elastomer primarily processed by liquid injection molding. It is known for its fast curing, precision molding, exceptional thermal resistance, and suitability for high-volume production. Major producers position LSR for applications across automotive, medical, electronics, food-contact, and industrial components. LSR remains a specialty elastomer segment with healthy medium-term demand, supported by its suitability for miniaturized, high-precision, clean-processing, and compliance-sensitive applications. Market growth is being driven by rising electric vehicle production and steady demand from the medical industry. LSR’s use in seals, gaskets, valves, connectors, cable accessories, wearable parts, and molded healthcare components is driving its demand in both these industries.

Leading companies in the market include Dow, WACKER Chemie AG, Momentive Performance Materials, Elkem ASA, and Shin-Etsu Chemical Co., Ltd. These players strengthen their positions by competing through innovation in medical-grade, automotive, self-adhesive, and high-precision molding solutions and building their global manufacturing presence and customer-specific product portfolio development.

Download Free sample to learn more about this report.

LIQUID SILICONE RUBBER MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 2.27 billion

- 2026 Market Size: USD 2.46 billion

- 2034 Forecast Market Size: USD 4.23 billion

- CAGR: 6.2% from 2026–2034

- Asia Pacific dominated the liquid silicone rubber market with a 51.54% share in 2025.

- The medical and healthcare segment accounted for the largest market share in 2025.

- The industrial grade segment held the largest market share in 2025.

Asia Pacific

Asia Pacific led the global market in 2025, reaching USD 1.17 billion, and is projected to grow to USD 1.24 billion in 2026.

North America

North America was valued at USD 0.51 billion in 2025 and is expected to reach USD 0.54 billion in 2026.

Europe

Europe accounted for USD 0.58 billion in 2025 and is projected to increase to USD 0.61 billion in 2026.

U.S.

U.S. The liquid silicone rubber market is projected to be valued at USD 0.48 billion in 2026, supported by strong demand from healthcare and industrial applications.

Japan

Japan Growing electronics production and increasing demand for high-performance silicone components in industrial and consumer applications are driving market growth.

Read More

LIQUID SILICONE RUBBER MARKET TRENDS

Shift Towards Self-Adhesive and Specialty LSR Grades to Fuel Product Adoption

The shift towards self-adhesive and specialty liquid silicone rubber grades is emerging as a key trend supporting broader product adoption across medical, automotive, and electronics applications. Unlike conventional LSR, self-adhesive grades can bond directly to selected thermoplastics and metals during molding, reducing the need for primers, secondary bonding steps, and additional assembly operations. This improves production efficiency, lowers processing cost, and enables complex multi-material part designs. At the same time, specialty grades such as fluorinated, self-lubricating, and low-temperature-curing LSR are expanding the material’s use in demanding environments.

- Companies like WACKER offer self-adhesive ELASTOSIL and SILPURAN grades for hard-soft combinations and medical overmolding, while Momentive highlights primeless adhesion and self-lubricating capabilities in its LSR portfolio. Such initiatives will fuel product adoption in high-demand application areas where chemical resistance, smoother surface performance, and compatibility with sensitive substrates are critical.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand from Electric Vehicles to Act as a Major Driver for Market Growth

As EV production expands globally, demand is increasing for high-performance materials used in connectors, seals, gaskets, cable accessories, sensor housings, and battery-related insulation components. LSR is well-suited for these applications because it offers excellent thermal stability, electrical insulation, chemical resistance, and long-term durability under demanding operating conditions. Its compatibility with precision molding also supports the production of compact and complex EV parts. According to the IEA, global electric car sales exceeded 17 million units in 2024 and are projected to surpass 20 million in 2025, reinforcing strong material demand. Companies such as WACKER are also developing silicone solutions specifically for high-voltage battery and e-mobility applications. Therefore, rising demand from electric vehicles is expected to drive the global liquid silicone rubber market growth during the forecast period.

MARKET RESTRAINTS

High Formulation Costs and Competition from Substitutes May Limit Market Expansion

High formulation cost and competition from alternative elastomers remain key restraints for the market. Although LSR offers excellent thermal stability, precision molding, and regulatory compatibility, its use is generally concentrated in applications where such performance justifies a premium. Compared to conventional elastomers, LSR often involves higher raw-material cost, specialized liquid injection molding infrastructure, and qualification requirements for regulated sectors such as medical and food-contact applications. In addition, direct bonding, chemical resistance, or biocompatibility claims still require substrate validation and application-specific testing before commercial scale-up, creating hurdles for market players.

MARKET OPPORTUNITIES

Increasing Healthcare Device Manufacturing to Create Strong Market Growth Opportunities

Increasing healthcare device manufacturing is creating significant growth opportunities for the market. LSR is well-suited for these applications because it offers sterilization resistance, flexibility, durability, and consistency in complex molded designs. As production of medical devices expands globally, demand is rising for high-purity, biocompatible, and precision-moldable materials used in valves, seals, stoppers, respiratory parts, wearable components, tubing accessories, and soft-contact healthcare products. The growing demand for minimally invasive devices, home healthcare equipment, and patient-friendly wearable products is further driving material adoption. In addition, stricter quality and safety requirements are encouraging manufacturers to use specialty medical-grade LSR. Therefore, the continued expansion of healthcare device manufacturing is expected to open attractive long-term opportunities for market participants.

Segmentation Analysis

By Grade

Industrial Grade Dominates Due to Its Broad Usage across Major End Use Industries

Based on the grade, the market is segmented into industrial grade, medical grade, and food & contact grade.

The industrial grade segment holds the largest market share in 2025, driven by its broad use across automotive, electrical, electronics, consumer, and industrial component manufacturing. This grade is widely preferred for seals, gaskets, connectors, keypads, cable accessories, and molded technical parts due to its excellent thermal stability, flexibility, electrical insulation, and suitability for precision injection molding. Its cost-performance balance makes it the most commercially adopted LSR category across large-volume applications. Continued growth in automotive electronics, miniaturized components, and durable industrial products is expected to support steady demand for industrial grade LSR over the forecast period.

The medical grade LSR represents a high-value market and is projected to grow at a 6.5% CAGR during the forecast period. This segment is supported by rising demand from medical devices, wearables, soft-touch healthcare parts, valves, tubing components, respiratory parts, and implantable or skin-contact applications. Medical-grade LSR is preferred for its biocompatibility, resistance to sterilization, softness, purity, and precision-molding capability. Growing healthcare spending, rising production of disposable and reusable medical components, and increasing demand for patient-friendly materials will assist the segment’s expansion.

Food and contact-grade segment holds another important share of the market, supported by growing use in kitchenware, baby care products, food-handling components, beverage-contact parts, and consumer products requiring high purity and safety compliance. This grade is valued for its non-toxicity, flexibility, odor neutrality, heat resistance, and suitability for repeated food-contact applications. The demand is also supported by rising consumer preference for durable, reusable, and safer material alternatives in household and packaged food-related products.

By End Use

To know how our report can help streamline your business, Speak to Analyst

Medical and Healthcare Dominates Due to Increasing Medical Device Manufacturing and Wearable Healthcare Technologies

Based on the end use, the market is segmented into automotive & transportation, medical & healthcare, electrical & electronics, consumer goods, industrial machinery & components, and others.

Medical and healthcare accounted for the largest liquid silicone rubber market share in 2025 and is also expected to remain one of the fastest-growing segments during the forecast period. The segment’s strength is supported by growing use of LSR in medical tubing parts, valves, masks, stoppers, respiratory devices, wearable healthcare products, and soft-contact molded components. The material is preferred because it offers excellent biocompatibility, resistance to sterilization, flexibility, purity, and high-precision molding performance. Increasing medical device manufacturing, rising demand for patient-friendly materials, and expansion of minimally invasive and wearable healthcare technologies are supporting the segment’s growth.

The automotive & transportation segment accounted for another major chunk of the market revenue and is anticipated to grow at a CAGR of 6.2% during the forecast period. Increasing applications include seals, gaskets, cable accessories, connectors, sensor housings, vibration-damping parts, and under-the-hood molded components. LSR is widely used in this segment because of its thermal resistance, flexibility, electrical insulation, and long-term performance in the demanding automotive sector. Rising vehicle electrification is further increasing the need for high-performance silicone materials in battery-related insulation and compact electronic assemblies.

Industrial machinery and components represent a stable end-use segment, supported by its use in seals, diaphragms, gaskets, valves, shock-absorbing elements, and other molded technical parts for industrial systems. LSR is favored for these applications due to its thermal stability, flexibility, durability, and reliability under repeated mechanical and environmental stress. It is also suitable for the automated production of precision industrial parts, thereby enhancing manufacturing efficiency and driving the segment’s growth at 5.7% CAGR during the forecast period.

Liquid Silicone Rubber Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East and Africa.

Asia Pacific

Asia Pacific Liquid Silicone Rubber Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the global liquid silicon rubber market in 2025, reaching USD 1.17 billion, and is projected to reach USD 1.24 billion in 2026. The region’s leadership is driven by large-scale manufacturing in automotive, electronics, medical devices, consumer goods, and industrial components. China remains the largest contributor, while Japan, South Korea, and India also support with strong demand due to expanding electronics production and increasing industrial activity. Asia Pacific benefits from cost-effective manufacturing, rising domestic consumption, and broad adoption of precision-molded silicone parts across high-volume applications.

China Liquid Silicone Rubber Market

China is expected to be valued at USD 0.64 billion in 2026, accounting for nearly 26% of global revenues, driven by its strong position in electronics manufacturing, automotive component production, and large-scale industrial processing. The country’s extensive downstream manufacturing ecosystem supports high consumption in connectors, seals, gaskets, cable accessories, and molded precision parts.

To know how our report can help streamline your business, Speak to Analyst

India Liquid Silicone Rubber Market

The India market is expected to reach USD 0.17 billion in 2026, representing around 7% of global revenues. The demand is supported by expanding automotive production, rising electrical and electronics manufacturing, and increasing use of durable elastomer materials in medical, consumer, and industrial applications.

North America

North America reached USD 0.51 billion in 2025 and is projected to increase to USD 0.54 billion in 2026, supported by demand across medical devices, healthcare components, automotive systems, and advanced electrical applications. The region benefits from a strong base of high-value manufacturing, regulatory-sensitive product demand, and growing adoption of specialty elastomer materials in precision-molded parts.

U.S. Liquid Silicone Rubber Market

The U.S. is expected to be valued at USD 0.48 billion in 2026, accounting for around 20% of global revenues, supported by strong demand from medical devices, healthcare assemblies, automotive components, and electrical applications. In addition, greater adoption of premium-grade silicone materials in regulated and technical applications continues to strengthen the U.S. market outlook.

Europe

Europe was valued at USD 0.58 billion in 2025 and is projected to reach USD 0.61 billion in 2026, growing steadily on the back of its strong automotive engineering base, medical technology sector, and advanced industrial manufacturing capabilities. The region continues to see product demand in automotive seals, technical molded parts, medical-grade components, and food-contact products. Demand is also supported by increasing preference for durable, high-performance elastomer materials in value-added applications.

Germany Liquid Silicone Rubber Market

Germany is expected to reach USD 0.14 billion in 2026, accounting for about 6% of the global market. Demand is supported by the country’s strong base in automotive engineering, industrial machinery, specialty processing, and advanced component manufacturing. Liquid silicone rubber is increasingly used in technical seals, gaskets, connectors, and molded precision parts across automotive and industrial applications.

U.K. Liquid Silicone Rubber Market

The U.K. market is expected to reach USD 0.10 billion in 2026, accounting for approximately 4% of global revenues. Demand is supported by steady consumption across healthcare products, specialty industrial components, electrical applications, and selected consumer goods.

Latin America

Latin America was valued at USD 0.11 billion in 2025 and is projected to reach USD 0.12 billion in 2026, supported by gradual expansion in automotive production, consumer goods manufacturing, and demand for industrial components. Brazil and Mexico remain the major regional contributors, with demand linked to seals, gaskets, molded consumer parts, and selected medical and electrical applications.

Brazil Liquid Silicone Rubber Market

Brazil is expected to be valued at USD 0.04 billion in 2026, accounting for nearly 2% of global revenues. Automotive components, consumer products, industrial goods, and selected healthcare applications mainly support the demand for the product in the market. The country remains the leading contributor within Latin America due to its relatively stronger manufacturing base and wider downstream use of molded elastomer products.

Middle East & Africa

The Middle East & Africa market stood at USD 0.09 billion in 2025 and is projected to reach USD 0.09 billion in 2026, driven by gradual expansion of healthcare products, electrical systems, industrial components, and selected consumer applications. While the regional manufacturing base remains narrower than other major markets, demand for durable, heat-resistant, and high-performance elastomer materials is steadily improving.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation-Led Competition and Capacity Expansion is Shaping the Market Positioning of the Prominent Players

The market is led by global manufacturers and technology-driven processors such as Dow, WACKER Chemie AG, Momentive Performance Materials, Elkem ASA, and Shin-Etsu Chemical Co., Ltd., supported by broad production footprints and strong downstream relationships. Competition is centered on specialty-grade innovation, application support, regulatory compliance, and global supply reliability rather than pricing alone. Companies are actively strengthening their positions through targeted developments. Dow expanded its automotive-focused portfolio with a selective adhesion LSR series. At the same time, WACKER invested in expanding silicone rubber capacity, and Elkem also launched AMSil™ 20503, an LSR-based elastomer range for additive manufacturing. These moves show that leading players are defending their share through capacity expansion, sustainability, and high-value specialty product development.

LIST OF KEY LIQUID SILICONE RUBBER COMPANIES PROFILED

- ANYSIL (China)

- Dow (U.S.)

- Dynaox (Hong Kong)

- Elkem (Norway)

- WACKER Chemie AG (Germany)

- Momentive Performance Materials (U.S.)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- ELLEGI S.p.A. (Italy)

- Guangzhou Ruihe New Material Technology Co., Ltd (China)

- KCC Silicone Corporation (South Korea)

KEY INDUSTRY DEVELOPMENTS

- September 2025: WACKER introduced ELASTOSIL® eco LR 5003, a non-postcure LSR for food and other sensitive applications, and also presented a new silicone rubber for busbar insulation in high-voltage EV batteries at K 2025. These launches underscore the market’s push toward sustainability and specialty grades focused on e-mobility.

- October 2024: Elkem launched the AMSil™ 20503 series, a new silicone elastomer range for additive manufacturing based on tailored LSR formulations. The launch aimed to improve shelf life, productivity, and part durability for 3D-printed silicone components, including spare parts, anatomical models, and textiles.

- June 2024: WACKER advanced its ELASTOSIL® eco portfolio with new biomethanol-based liquid silicone rubber grades, including ELASTOSIL® eco LR 5040. The development expanded sustainable LSR offerings while maintaining performance standards, especially for non-post-curing and high-tear-resistance applications.

- May 2022: WACKER announced a major global expansion of silicone rubber capacity, earmarking over USD 116 million to increase HCR and LSR output. The capacity expansion is planned to meet the increasing demand from the automotive, electronics, and medical sectors.

- November 2021: Dow launched its SILASTIC™ SA 994X selective adhesion LSR series for the automotive industry. The new series was developed for applications such as connector seals, battery vent gaskets, radiator gasket seals, and LiDAR/radar housing protection in electric, hybrid, and autonomous vehicles.

REPORT COVERAGE

The global liquid silicone rubber market analysis provides an in-depth study of market size & forecast across all market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.2% from 2026-2034 |

| Unit | Value (USD Billion) Volume (Kiloton) |

| Segmentation | By Grade, End Use, and Region |

| By Grade |

|

| By End Use |

|

| By Regiom |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 2.27 billion in 2025 and is projected to reach USD 4.23 billion by 2034.

In 2025, the market value stood at USD 1.17 billion.

Recording a CAGR of 6.2%, the market is slated to exhibit steady growth during the forecast period.

The medical & healthcare segment led in 2025.

Rising demand from electric vehicles is expected to drive market growth.

Dow, WACKER Chemie AG, Momentive Performance Materials, Elkem, and Shin-Etsu Chemical Co., Ltd. are some of the prominent players in the market.

Asia Pacific held the highest market share in 2025.

Shift towards self-adhesive and specialty LSR grades to favor product adoption.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us