LNG Storage Tank Market Size, Share & Industry Analysis, By Material (9% Nickel Steel, Prestressed Concrete, Steel + Concrete Hybrid, and Others), By Capacity (Up to 50,000 m³, 50,000 – 150,000 m³, 150,000 – 200,000 m³, and Above 200,000 m³), By End User (LNG Export Terminals, Peak Shaving Facilities, Regasification Terminals, and Others), and Regional Forecast, 2026-2034

LNG Storage Tank Market Size and Future Outlook

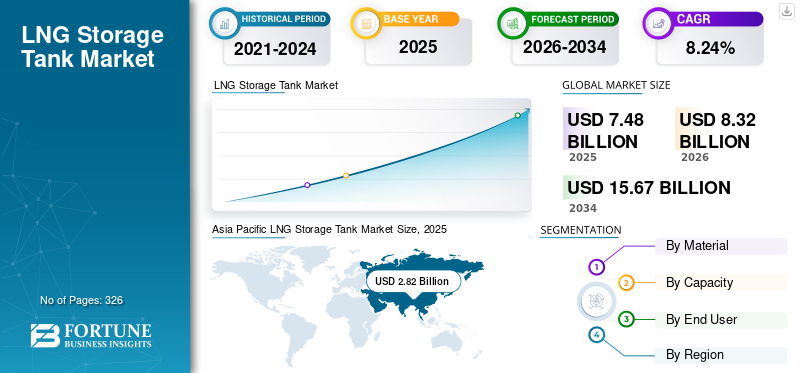

The global LNG Storage tank market size was valued at USD 7.48 billion in 2025. The market is projected to grow from USD 8.32 billion in 2026 to USD 15.67 billion by 2034, exhibiting a CAGR of 8.24% over the forecast period. Asia Pacific dominated the LNG storage tank market with a market share of 37.7% in 2025.

An LNG Storage Tank is a specialized cryogenic storage vessel designed to store Liquefied Natural Gas (LNG) at extremely low temperatures of around −162 °C, keeping it in liquid form for efficient storage and transportation. These tanks are typically constructed using materials such as 9% nickel steel and prestressed concrete to withstand cryogenic conditions and maintain structural integrity. LNG storage tanks are widely used in liquefaction plants, regasification terminals, export facilities, and peak-shaving plants to store LNG before it is transported or converted back into gaseous form. They are engineered with advanced insulation and containment systems to minimize heat transfer and ensure safe long-term storage.

The growth of the market is primarily driven by the rising global demand for Liquefied Natural Gas as a cleaner alternative to coal and oil. Increasing investments in LNG exports and regasification terminals are creating strong demand for large-capacity storage tanks. Additionally, many countries are expanding LNG infrastructure to improve energy security and diversify gas supply sources. The growth of LNG trade, along with the development of small scale LNG and bunkering facilities for maritime transport, is further supporting the installation of advanced cryogenic storage tanks worldwide.

Leading companies in the market such as Linde plc, McDermott International, Wärtsilä, IHI Corporation, and CIMC Enric Holdings Limited are actively contributing to the expansion of LNG infrastructure worldwide. These companies focus on developing advanced cryogenic storage technologies, constructing large-capacity storage tanks, and providing engineering, procurement, and construction (EPC) services for LNG export, import, and regasification terminals. Their efforts commonly include investments in research and development to enhance tank safety, improve insulation efficiency, and optimize materials such as nickel steel for cryogenic conditions. Additionally, they engage in strategic partnerships and large-scale LNG projects to support the growing demand for Liquefied Natural Gas as a cleaner energy source.

Download Free sample to learn more about this report.

LNG Storage Tank Market Key Takeaways

- 2025 Market Size: USD 7.48 billion

- 2026 Market Size: USD 8.32 billion

- 2034 Forecast Market Size: USD 15.67 billion

- CAGR: 8.24% from 2026–2034

- Asia Pacific dominated the LNG storage tank market with a 37.7% share in 2025.

- Nickel steel segment accounted for approximately 61.71% of the LNG storage tank market in 2025.

- LNG export terminals segment is the fastest growing segment with a 8.84% CAGR during the forecast period.

Asia Pacific

Asia Pacific generated USD 2.82 billion in 2025, accounting for 37.72% of global revenues with strong LNG infrastructure expansion.

Europe

Europe accounted for USD 1.89 billion in 2025, representing 25.28% of global revenues supported by stable energy import demand.

North America

North America was valued at USD 1.61 billion in 2025, driven by expanding LNG production and export capacity.

U.S.

The U.S. market was valued at USD 1.40 billion in 2025 and is set to reach USD 1.52 billion in 2026, supported by LNG export infrastructure along the Gulf Coast.

Japan

The Japan market was valued at USD 0.59 billion in 2025, supported by consistent LNG import dependency and storage requirements.

Read More

LNG Storage Tank Market Trends

Increasing Adoption of Large-Capacity LNG Storage Tanks Are Amplifying Market Growth

A major market trend is the growing deployment of large-capacity storage tanks above 200,000 m³ to support expanding global trade in Liquefied Natural Gas. LNG export and import terminals are increasing storage capacities to enhance supply reliability and reduce logistics costs. Modern LNG terminals now frequently use tanks with capacities of 200,000 to 270,000 m³, compared to the earlier industry standard of 150,000 to 180,000 m³. This trend is driven by major LNG projects in countries such as Qatar, the U.S., and China, which are expanding export and import infrastructure. Larger tanks enable operators to store greater LNG volumes while minimizing the number of tanks required at terminals. As global LNG trade expands, operators are increasingly investing in advanced full-containment tanks with improved insulation systems and cryogenic materials to enhance operational efficiency and long-term storage performance.

MARKET DYNAMICS

Market Drivers

Download Free sample to learn more about this report.

Rising Global LNG Trade and Infrastructure Investments to Push the Market Growth

One of the key market drivers is the rapid growth of global LNG trade and infrastructure development. Countries are increasingly adopting Liquefied Natural Gas as a transition fuel to reduce reliance on coal and oil. Global LNG trade has already surpassed 400 million tons annually, highlighting the rising demand for natural gas in power generation and industrial applications. To meet this demand, new liquefaction plants and regasification terminals are being constructed worldwide, each requiring multiple cryogenic storage tanks. For example, LNG export expansions in the U.S. and Australia, along with new import terminals in India and China, are creating strong demand for LNG storage infrastructure. These projects require specialized tanks capable of storing LNG at extremely low temperatures of around −162 °C, which is significantly driving LNG storage tank market growth.

Market Restraints

Growing Shift Toward Renewable Energy to Limit the Market Growth

A key market restraint is the growing shift toward renewable energy sources and the adoption of stricter decarbonization policies worldwide. Governments are setting ambitious climate targets to reduce greenhouse gas emissions and accelerate the adoption of renewable energy technologies such as wind and solar. For instance, European countries aim to achieve carbon neutrality by 2050, which encourages investment in renewable energy rather than in fossil fuel infrastructure. As renewable power generation continues to expand, the long-term reliance on Liquefied Natural Gas may gradually decline in certain regions. LNG storage tanks are typically designed to operate for 30–40 years, and uncertainty about future gas demand may slow down new investments. Additionally, environmental regulations and public opposition to fossil fuel projects can delay LNG terminal developments, thereby restraining market growth.

Market Opportunities

Expansion of Small-Scale LNG and LNG Bunkering Infrastructure to Create New Growth Avenues

A major market opportunity lies in expanding small-scale LNG distribution and LNG bunkering infrastructure for the maritime and transportation sectors. With stricter emission regulations in the shipping industry, LNG is increasingly being adopted as a cleaner alternative to conventional marine fuels. Currently, more than 400 LNG-powered vessels are in operation globally, with many more under construction. This growth is driving demand for small and medium LNG storage tanks at ports and bunkering terminals. Countries such as Singapore, South Korea, and the Netherlands are actively investing in LNG bunkering infrastructure. Additionally, small-scale LNG distribution is expanding in remote regions and industrial applications where pipeline gas supply is limited. These developments create new opportunities for modular LNG storage tanks and specialized cryogenic storage solutions.

Market Challenges

High Capital Costs and Long Construction Timelines to Limit Market Growth

A major market challenge is the high capital investment required for LNG storage infrastructure and the lengthy construction timelines associated with such projects. Building a single large LNG storage tank can cost USD 120–250 million, depending on its size, design, and containment structure. In addition to high construction costs, these tanks require specialized cryogenic materials such as nickel steel and advanced insulation systems to maintain LNG at extremely low temperatures. Construction timelines can often exceed 30–36 months, as strict engineering standards, safety regulations, and environmental approvals must be met. These factors increase financial risk for developers and may delay project implementation. Furthermore, fluctuations in LNG prices and uncertainty in global energy markets can impact investment decisions, making it challenging for project developers to plan long-term LNG storage infrastructure.

Segmentation Analysis

By Material

Huge Requirement in Inner Containment Tank to Lead the 9% Nickel Steel Segment Growth

Based on material, the market is segmented into 9% nickel steel, prestressed concrete, steel + concrete hybrid, and others.

9% nickel steel segment accounted for approximately 61.71% of the LNG storage tank market share in 2025. The segmental growth is driven by its widespread use for the inner containment of LNG tanks, due to its excellent fracture toughness and ability to withstand extremely low temperatures around −162°C, which are required to store Liquefied Natural Gas safely. 9% nickel steel has been the industry standard for cryogenic LNG storage for decades due to its high strength, durability, and resistance to brittle fracture in extreme conditions. It is commonly used in full-containment tanks, where the inner tank is constructed of 9% nickel steel, while the outer tank is typically concrete. The material is particularly prevalent in large LNG export terminals and regasification facilities in countries with large-scale LNG infrastructure development.

Steel + concrete hybrid segment is expected to grow at a CAGR of 9.35% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Capacity

Increasing Import and Export Terminal to Lead the 150,000 – 200,000m³ Segment Growth

Based on capacity, the market is segmented into Up to 50,000 m³, 50,000 – 150,000 m³, 150,000 – 200,000 m³, and above 200,000 m³.

150,000 – 200,000 m³ segment accounted for approximately 42.02% of the market share. It remains the dominant share in the market. These tanks are commonly used in large LNG import and export terminals, where significant storage capacity is required to manage high LNG throughput. Full-containment tanks within this capacity range have long been considered the industry standard for large LNG infrastructure, offering strong economies of scale and operational efficiency. Large LNG terminals typically install multiple tanks within this capacity range to ensure adequate storage before regasification or export operations. Tanks ranging from 50,000 to 200,000 m³ are widely used in liquefaction plants and export terminals, underscoring strong demand for large-scale LNG storage infrastructure.

Above 200,000 m³ segment is expected to grow at a CAGR of 8.84% during the forecast period.

By End User

Ensuring Consistent Supply to Downstream Gas Infrastructure to Propel the Regasification Terminals Segment Growth

Based on end user, the market is segmented into LNG export terminals, peak shaving facilities, regasification terminals, and others.

Regasification terminals segment represented the largest market share of around 48.14% in 2025. These terminals receive LNG shipments from exporting countries, store it in cryogenic tanks, and then convert it back to gaseous form for distribution through natural gas pipeline networks. Regasification terminals typically require multiple large storage tanks, often in the 150,000–200,000 m³ capacity range, to ensure a consistent supply to downstream gas infrastructure. Rapid LNG import infrastructure development in countries such as China, India, and several European countries has significantly increased the demand for these tanks. As many nations aim to diversify their energy sources and reduce dependence on pipeline gas imports, regasification terminals continue to drive substantial growth in LNG storage tank installations worldwide.

LNG export terminals is the fastest growing segment with a CAGR of 8.84% over the forecast period.

LNG Storage Tank Market Regional Outlook

By geography, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific LNG Storage Tank Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated the market with a valuation of USD 2.82 billion in 2025, accounting for approximately 37.72% of global revenues. Asia Pacific is the largest and most dynamic region in the market due to its high dependence on imported natural gas and rapidly expanding LNG infrastructure. Countries such as China, Japan, and South Korea operate some of the world’s largest LNG import networks, requiring extensive cryogenic storage facilities at regasification terminals. Japan alone operates more than 30 LNG import terminals, making it one of the largest LNG importers globally. China has also significantly expanded its LNG infrastructure with more than 25 regasification terminals, driven by rising natural gas consumption and efforts to reduce coal usage in power generation. The strong industrial base, increasing energy demand, and growing investments in LNG terminals across countries such as India and Australia continue to support large-scale deployment of LNG storage tanks throughout the region.

China LNG Storage Tank Market

China remains the dominant contributor in the Asia Pacific, valued at USD 0.95 billion in 2025. It is set to reach a valuation of USD 1.08 billion in 2026. China is one of the fastest-growing markets, driven by rising natural gas consumption and strong government support for cleaner energy. The country has developed numerous LNG import terminals along its coastal regions, each requiring large cryogenic storage tanks.

India LNG Storage Tank Market

India was estimated at USD 0.38 billion in 2025 and is likely to reach USD 0.43 billion in 2026. India’s LNG storage tank demand is increasing as the country expands LNG import capacity to meet growing energy demand. New regasification terminals and expansion of existing facilities are driving the installation of additional LNG storage tanks.

Japan LNG Storage Tank Market

Japan was valued at USD 0.59 billion in 2025 and is expected to reach USD 0.66 billion in 2026. It has one of the most extensive LNG import infrastructures globally, with many large regasification terminals requiring significant storage capacity. LNG storage tanks are critical for maintaining a stable gas supply for power generation and industrial use.

North America

North America was valued at USD 1.61 billion in 2025, accounting for approximately 21.53% of the global market. The region plays an important role in the global LNG industry due to its large natural gas reserves and expanding LNG export capacity. The U.S. has become one of the world’s leading LNG exporters, supported by major liquefaction terminals along the Gulf Coast that require large cryogenic storage tanks. Several export facilities in states such as Texas and Louisiana store LNG before loading it onto carriers for international markets. The region also includes LNG import and peak-shaving facilities used to balance seasonal gas demand. Canada is also expanding LNG infrastructure with new export projects under development on its west coast. The presence of extensive natural gas resources and a strong pipeline network supports the development of LNG terminals and related storage infrastructure across North America.

U.S. LNG Storage Tank Market

The U.S. market was estimated at USD 1.40 billion in 2025 and is set to reach USD 1.52 billion in 2026. The U.S. plays a major role in the market due to its strong LNG export infrastructure along the Gulf Coast. Multiple liquefaction terminals require large cryogenic storage tanks to store LNG before shipment to global markets, supporting the country’s position as a leading LNG exporter.

Europe

Europe accounted for USD 1.89 billion in 2025, representing approximately 25.28% of global revenues. The region has developed a strong LNG infrastructure network to enhance energy security and diversify natural gas supply sources. Several countries, including Spain, France, Italy, and the U.K., operate large LNG import terminals equipped with multiple storage tanks. Spain is one of the key LNG entry points in Europe, with eight operational regasification terminals, enabling it to act as a major LNG distribution hub for the region. In recent years, additional LNG infrastructure has been developed in countries such as Germany and Greece, particularly through floating storage and regasification units. The increasing focus on energy supply diversification and gas storage capacity has accelerated investments in LNG terminals and associated storage tanks across Europe.

Germany LNG Storage Tank Market

Germany was estimated at USD 0.18 billion in 2025 and is anticipated to reach USD 0.20 billion in 2026. Germany has rapidly expanded LNG infrastructure in recent years to reduce reliance on pipeline gas imports. New LNG import terminals and floating storage regasification units are increasing the need for LNG storage tanks to support gas supply stability.

U.K. LNG Storage Tank Market

The U.K. market was valued at USD 0.28 billion in 2025 and is likely to reach USD 0.32 billion in 2026. The U.K. has developed LNG storage infrastructure mainly through large import terminals that support gas supply diversification. Facilities such as the Isle of Grain terminal store LNG before regasification and distribution into the national gas grid, helping ensure energy security.

Latin America

Latin America accounted for USD 0.48 billion in 2025, or approximately 6.38% of global revenues. The region has developed LNG infrastructure mainly to support energy security and supplement domestic natural gas production. Countries such as Brazil, Mexico, Chile, and Argentina operate LNG regasification terminals that store LNG and convert it to gaseous form for pipeline distribution. Brazil operates several LNG import terminals that supply natural gas to power plants and industrial users, particularly during periods of high electricity demand. Mexico uses LNG terminals to support gas supply for power generation and industrial activities in regions not fully connected to pipeline networks. Although the LNG infrastructure in Latin America is smaller compared with Asia Pacific and Europe, ongoing investments in gas-fired power generation and energy diversification continue to support the development of LNG storage tanks in the region.

Middle East & Africa

The Middle East & Africa were valued at USD 0.68 billion in 2025. The Middle East & Africa region is an important contributor to global LNG production and trade, particularly through major LNG export projects. Qatar operates some of the world’s largest LNG liquefaction and export facilities, which require extensive LNG storage infrastructure to support large-scale shipments. Several countries in the Middle East, including the UAE, Kuwait, and Jordan, operate LNG import terminals to supplement domestic gas supply. In Africa, LNG infrastructure development is gradually increasing, with projects in Mozambique and South Africa aimed at supporting energy supply and export potential. These developments are contributing to the gradual expansion of LNG storage tank installations in the region.

GCC LNG Storage Tank Market

The GCC market was estimated at USD 0.41 billion in 2025 and is expected to hit USD 0.45 billion in 2026. It is an important hub for LNG production and export, particularly through large liquefaction projects in countries such as Qatar and the UAE. LNG storage tanks support both export operations and domestic gas supply infrastructure across the region.

Competitive Landscape

KEY INDUSTRY PLAYERS

Key Players Focus on Advanced LNG Storage Technologies and Global Project Expansion to Boost Market Share

Leading companies such as Linde plc, McDermott International, Wärtsilä, IHI Corporation, and CIMC Enric Holdings Limited collectively drive the growth of the LNG storage tank market through strong global presence and technological expertise. These players are focused on developing advanced cryogenic storage systems, large-capacity tank designs, and integrated EPC solutions to support expanding LNG infrastructure. Across the market, there is a common emphasis on enhancing safety standards, improving insulation efficiency, and optimizing material performance for long-term storage. Additionally, these companies actively engage in large-scale LNG terminal projects, strategic collaborations, and capacity expansions, ensuring reliable storage solutions to meet the increasing global demand for LNG.

List of Key LNG Storage Tank Companies Profiled

- Linde plc (Ireland)

- McDermott International (U.S.)

- Wärtsilä (Finland)

- IHI Corporation (Japan)

- Chart Industries (U.S.)

- CIMC Enric Holdings Limited (China)

- Air Water Inc. (Japan)

- INOX India Limited (India)

- Cryolor SA (France)

- Isısan A.Ş. (Turkey)

- Mitsubishi Heavy Industries (Japan)

- Samsung Heavy Industries (South Korea)

- Technip Energies (France)

- Saipem (Italy)

- VINCI Construction (France)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Marsa LNG, a joint venture between TotalEnergies and OQ, achieved a key milestone in its USD 1.6 billion LNG bunkering project at Sohar Port, Oman, and Freezone with the successful installation of a critical LNG storage tank roof. The project, set to become the region’s first LNG bunkering hub with a capacity of 1 million tons per year, utilized an advanced “air-raising” technique executed by CB&I, a subsidiary of McDermott International.

- January 2026: L&T Onshore won a major contract from Petronet LNG, a joint venture of Oil and Natural Gas Corporation, Indian Oil Corporation, GAIL (India) Limited, and Bharat Petroleum Corporation Limited. The project, to be executed on a lump-sum turnkey basis at the Dahej Petrochemical Complex India, involves building a 170,000 cubic metre LNG/ethane double-wall storage tank and a 140,000 cubic metre propane double-wall tank. It also includes associated handling and dispatch systems to support downstream PDH and polypropylene production facilities.

- January 2026: CB&I secured a contract from We Energies to design and construct a full-containment LNG storage tank for a peak-shaving facility in Oak Creek, near Milwaukee, U.S. The scope includes Engineering, Procurement, Fabrication, and Construction (EPFC) of a 2 billion cubic feet LNG tank, along with in-tank pumps, topside systems, and associated piping.

- October 2025: The British Columbia Utilities Commission approved FortisBC Energy Inc.’s Tilbury LNG Storage Expansion Project in Delta, Canada. The project involves replacing a 56-year-old LNG storage tank with a larger, modern unit to strengthen storage capacity and improve supply reliability. Following a detailed public review process, the commission determined that the project is in the public interest and essential for ensuring a stable natural gas supply in the region.

- August 2025: Doosan Enerbility secured a USD 420 billion contract from Korea Gas Corporation for the second phase of the Dangjin LNG project in South Chungcheong Province, South Korea. The scope includes building three LNG storage tanks and related auxiliary facilities. Construction is set to begin in September and is expected to be completed by December 2029, following the successful completion of the first phase’s roof installation work.

REPORT COVERAGE

The report provides a comprehensive analysis of the market, focusing on key aspects such as leading companies, product processes, and Porter’s Five Forces. Additionally, the report provides valuable insights into market trends and highlights key industry developments. In addition to the factors mentioned above, the report also encompasses several factors that contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 8.24% from 2026 to 2034 |

| Unit | Value (USD Billion) |

|

Segmentation |

By Material

|

|

By Capacity

|

|

|

By End User

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 7.48 billion in 2025 and is projected to reach USD 15.67 billion by 2034.

In 2025, the Asia Pacifics market value stood at USD 2.82 billion.

The market is expected to exhibit a CAGR of 8.24% during the forecast period.

By material, 9% nickel steel segment led the market in 2025.

Rising global LNG trade and infrastructure investments are the key factors driving the market.

Linde plc, McDermott International, Wärtsilä, IHI Corporation, and CIMC Enric Holdings Limited are the major players in the global market.

Asia Pacific dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 326

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us