Locomotive Market Size, Share & Industry Analysis, By Propulsion Type (Combustion (Diesel and Hydrogen) and Electric), By End User (Passenger and Freight), By Technology (IGBT Module, GTO Module, and SiC Module), By Component (Rectifier, Alternator, Motor, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

KEY MARKET INSIGHTS

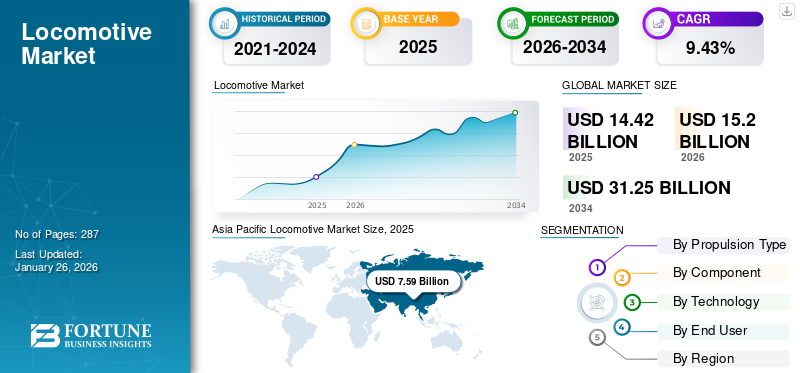

- The locomotive market is expected to grow from $15.20 billion in 2026 to about $31.25 billion by 2034, reflecting a compound annual growth rate (CAGR) of 9.43% during the forecast period.

- Adoption of locomotives is likely to accelerate with increasing investments in railway infrastructure and modernization projects, as governments and rail operators expand transportation capacity and efficiency.

- Although the market continues to evolve, demand for locomotives is being supported by growing freight transportation requirements and increasing deployment of electric locomotives across rail networks.

- Asia Pacific currently leads the locomotive market, accounting for 52.63% of market share in 2025, supported by expanding railway networks and significant rail infrastructure investments across major economies such as China and India.

The global locomotive market size was valued at USD 14.42 billion in 2025 and is projected to grow from USD 15.2 billion in 2026 to USD 31.25 billion by 2034, exhibiting a CAGR of 9.43% during the forecast period. Asia Pacific dominated the global locomotive market with a market share of 52.63% in 2025.

The locomotive is a type of train car that powers the entire train set. A locomotive is self-propelled and generates energy either by burning fuel or using electricity. Its primary function is to push or pull the other train cars, enabling the transport of goods and passengers globally from one point to another.

The global locomotive market occupies a strategic position within the broader transportation and infrastructure ecosystem, supported by growing freight volumes, railway modernization programs, and increasing emphasis on low-emission mobility solutions. Demand patterns are being influenced by fleet replacement cycles, urbanization, industrial development, and national investments aimed at improving rail efficiency and connectivity. These factors collectively underpin long-term locomotive market growth across both developed and emerging economies.

Market dynamics are increasingly shaped by propulsion technologies and energy transition priorities. Electric locomotives are attracting substantial investment because railway operators seek lower operating costs and reduced carbon emissions. At the same time, diesel-powered systems retain relevance in regions characterized by limited electrification infrastructure, while hydrogen technologies are emerging as an alternative for decarbonization strategies and non-electrified routes. Consequently, technological diversity remains a defining feature of the locomotive industry.

Freight transportation continues to account for a significant share of the locomotive market size, reflecting rising cross-border trade, e-commerce activity, and the need for efficient bulk cargo movement. Passenger applications are also benefiting from urban transit expansion and high-speed rail development. Governments increasingly recognize rail transport as a critical component of sustainable mobility frameworks, creating favorable conditions for long-term capital investment.

Power electronics and digital technologies are becoming increasingly important sources of differentiation. Silicon carbide modules, advanced traction motors, predictive maintenance systems, and intelligent fleet management platforms are improving operational efficiency and asset utilization. These developments are influencing locomotive market trends and encouraging manufacturers to expand innovation capabilities.

Despite capital-intensive procurement cycles and infrastructure constraints, the global locomotive market remains supported by electrification initiatives, technological advancement, and the growing importance of rail transport within decarbonization and logistics strategies. Such structural factors are expected to sustain long-term locomotive market growth and reinforce industry resilience.

Increasing levels of carbon emissions and the resulting degradation in air quality globally have raised significant environmental concerns. In response, governments globally are focused on reducing their carbon footprint and aiming toward sustainable mobility to reduce fossil fuel dependency and promote green energy transportation. As a result, electrification technologies are being adopted across multiple modes of road transport, including road and rail vehicles.

Major railway ministries globally are actively expanding their rail network with electric lines to integrate electric engines to haul passengers and cargo shipments globally. Thus, the market is expected to witness a drastic change in operations, with more nations integrating electric units into their operation fleets.

Leading players such as Siemens AG, Hitachi Rail, Wabtec Corporation, Stadler Rail, and Alstom dominate the marketplace, leveraging extensive R&D, global manufacturing capabilities, and long-term government contracts to maintain their market positions.

Download Free sample to learn more about this report.

LOCOMOTIVE MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 14.42 billion

- 2026 Market Size: USD 15.2 billion

- 2034 Forecast Market Size: USD 31.25 billion

- CAGR: 9.43% from 2026–2034

- Asia Pacific dominated the global locomotive market with a market share of 52.63% in 2025.

- The electric segment will account for the largest locomotive market share of 54.94% in 2026.

- The other segment dominated the global market share of 76.06% in 2026.

North America

The market in North America reached USD 1.93 billion in 2025, representing 13.36% of total market revenue, and is projected to reach USD 2 billion in 2026.

Europe

Europe contributed approximately USD 4.32 billion to the global market in 2025, accounting for 29.98% share, and is expected to reach USD 4.53 billion in 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 7.59 billion, representing 52.63% of global demand, and is projected to grow to USD 8.04 billion in 2026.

U.S.

The U.S. market is projected to reach USD 1.21 billion by 2026.

Japan

The Japanese market is projected to reach USD 0.27 billion by 2026.

Read More

Market Dynamics

Locomotive Market Trends:

Technological Advancements to Emerge as a Key Trend in the Market

Autonomous trains are emerging as an innovative solution to enhance the efficiency and reliability of trains in cities and urban areas. Technological advancements, such as real-time data transmission systems and advanced sensor technology, fuel the development of autonomous trains in the locomotive industry. For instance, in November 2022, Alstom successfully demonstrated its autonomous shunter in Breda, the Netherlands. The vehicle is equipped with advanced obstacle-detection capabilities and provides positive results during testing.

Moreover, significant players and railway corporations have begun adopting automatic train control systems to enhance the exchange of data, minimize technical errors, and build passengers’ confidence in autonomous operations. Governments across various countries have started the pilot testing and adoption of autonomous trains on their tracks. For instance, in March 2023, the Indian Ministry of Railway announced plans to integrate IoT devices into over 8,700 locomotives as part of its Real-Time Train Information System project, enabling accurate live tracking. Thus, growing implementation of autonomous technology and sensor-based technologies in the rail industry is likely to shape locomotive market growth during the forecast period.

Decarbonization priorities are reshaping locomotive market trends across major railway economies. Governments and operators are allocating greater resources toward electric traction systems and alternative propulsion technologies to reduce dependence on conventional diesel fleets. Hydrogen-powered locomotives and battery-assisted systems are gaining attention, particularly on routes where full electrification remains economically challenging. These developments are encouraging manufacturers to diversify product portfolios and accelerate research activities.

Digital transformation represents another defining trend. Railway operators increasingly rely on predictive maintenance platforms, remote diagnostics, and condition-monitoring technologies to improve asset utilization and minimize downtime. Artificial intelligence and data analytics are becoming integral components of fleet management strategies, allowing operators to optimize maintenance schedules and improve operational efficiency.

Power electronics are undergoing rapid evolution. Silicon carbide modules are attracting growing interest because they offer superior efficiency, lower heat generation, and improved performance compared with conventional technologies. These advancements support lower lifecycle costs and contribute to energy efficiency objectives.

Download Free sample to learn more about this report.

Market Growth Drivers:

Increasing Freight Transportation to Drive Market Growth

As the population is increasing, the difficulty in transportation is increasing, resulting in traffic congestion and higher levels of pollution emitted from road vehicles. In response, railway transit has emerged as a prime mode of transportation for daily commuting both within and between cities. Moreover, mass transit of the people by rail offers people cost-efficient and time-efficient traveling. Rail freight transportation provides a cost-effective cargo transportation solution and helps lower carbon emissions. Furthermore, the increasing focus of governments globally on reducing the carbon footprint is expected to cause a shift from road to rail transportation for the supply of heavy bulk materials such as cargo goods.

Major countries, such as India, the U.S., and China, are aiming toward transporting cargo through rails instead of on roads to curb carbon footprints and support sustainable mobility. Additionally, railway networks across the globe are actively phasing out diesel-powered models in favor of green energy sources to enhance environmental sustainability in freight transportation. For instance, according to the Federal Railroad Administration, the U.S. freight rail network is one of the largest, safest, and cost-efficient freight systems in the world. The industry, valued at nearly USD 80 billion, is widely operated by 7 Class I railroads, each generating an average annual revenue of USD 490 million.

Rising Focus of Expanding Rail Networks in Developed and Developing Nations to Drive Market Growth

During the COVID-19 pandemic, the e-commerce segment witnessed a significant surge in demand, as it enabled end users to receive goods without visiting physical stores. This decreasing contactless delivery helped minimize the risk of virus transmission and has continued to grow steadily in the post-pandemic period due to its convenience.

Many developed and developing nations are increasingly focused on expanding their rail network to enhance the efficiency of passenger transport and cargo shipments. This shift is also expected to drive further investment in rolling stock across the rail industry. For instance, in September 2023, during the group summit of the top 20 economies, the U.S. and India revealed a rail and shipping corridor linking India to Europe and the Middle East. Similarly, in December 2022, the U.S. unveiled a USD 2.3 billion investment initiative to expand passenger rail services in the country. The program focuses on developing intercity passenger lines and high-speed railway services and improving the safety and performance of the national rail networks.

In June 2025, Turkey unveiled its strategic plan to expand the railways in the country. The country’s ultimate objective is to develop 28,500 kilometers of railways, which include traditional rail lines and high-speed and specialized freight corridors. As part of its efforts to reduce dependence on imports and bolster domestic production, Turkey successfully developed the E5000 electric train engine, entirely in Turkey, manufactured entirely within the country by TÜRASAŞ (Turkey Rail System Vehicles Industry Inc.). 5 Units were delivered, and an additional 15 were aimed to be delivered in 2025.

Infrastructure modernization programs represent a major catalyst for locomotive market growth. Governments across developed and emerging economies are investing in rail networks to enhance logistics efficiency, reduce congestion, and strengthen economic connectivity. Fleet renewal initiatives are creating sustained demand for technologically advanced locomotives capable of delivering improved reliability and operational performance.

Freight transportation requirements provide another important growth driver. Industrialization, rising international trade, and expanding e-commerce activities are increasing the need for efficient cargo movement. Rail systems offer cost advantages for bulk commodities and long-distance transportation, supporting demand for high-performance freight locomotives. These dynamics contribute significantly to locomotive market size expansion.

Market Restraints:

High Cost Associated with Rail Systems to Hinder the Growth of the Market

Besides being a substantial mode of transportation, the railway network requires significant capital investment and ongoing maintenance costs for its establishment and operation. An entire rail system comprises numerous components and complex electrical systems and diesel systems, especially in diesel-electric models, which contribute significantly to the overall manufacturing and component cost. The high cost of individual components further adds to the total cost of a rail vehicle.

The costs of electric trains tend to be more expensive compared to diesel-electric due to the integration of advanced electrification systems within the engine. Additionally, the supporting rail infrastructure also needs to be electrified for the smooth functioning of electric propulsion on rail tracks. These infrastructure updates require high capital costs. Despite this, diesel models typically offer lower fuel efficiency, leading to higher long-term operational costs.

Out of all the components, the locomotive represents the highest cost. Poor technical performance often results in higher fuel consumption, further increasing the operational cost. However, as more countries upgrade their railway infrastructure to support electric trains and gradually phase out diesel-powered units, a large-scale shift toward railway electrification is anticipated in the upcoming years.

Capital intensity remains one of the principal constraints affecting the locomotive market. Procurement of modern locomotives requires substantial upfront investment, often involving long financing cycles and extensive infrastructure commitments. Budget limitations and economic uncertainty can delay fleet modernization programs, particularly in developing regions with competing public spending priorities.

Infrastructure disparities create additional challenges. Electrification levels vary considerably across countries, limiting the adoption of advanced propulsion technologies in certain markets. Operators serving remote or underdeveloped routes may continue relying on legacy systems because infrastructure upgrades require significant resources and long implementation periods.

Regulatory complexity influences project execution and market entry. Safety standards, environmental requirements, and certification procedures differ across jurisdictions, increasing development costs and extending commercialization timelines. Compliance obligations may affect product customization requirements and complicate cross-border expansion strategies for manufacturers.

Market Opportunities:

Growing Rail Expansion and Infrastructure Projects Across Various Regions

Governments in major regions are motivated to expand their rail networks across national and international borders to reduce dependency on road transportation and promote more sustainable means of transportation for passengers and freight services. In line with environmental priorities, many governments are imposing strict regulations and increasing infrastructure budgets to accelerate the development of rail systems. These initiatives are contributing to the high demand for locomotives globally.

Countries in North America have well-established freight rail networks, which are responsible for a substantial amount of freight transport each year on the rail network. However, the passenger rail network is not well established, and the governments are increasing spending on developing passenger rail networks. For instance, in January 2022, Argentina and China signed three rail project contracts, which will include the electrification of the Belgrano Norte line and several sections on the Sarmiento line, part of the Buenos Aires rail network, and the renewal of the Urquiza line.

In February 2025, Northrail signed a contract with Siemens Mobility for the procurement of 50 new Vectron models. Deliveries are expected to begin in 2025. This fleet expansion is intended to enhance NoNorthrail's rthrails’s leasing offerings for sustainable rail transport and reflects the increasing demand for freight rail operations.

Electrification initiatives represent one of the most attractive opportunities within the locomotive market. Governments pursuing decarbonization targets are allocating substantial resources toward railway modernization and expanding electrified corridors. Such investments create favorable conditions for manufacturers specializing in energy-efficient locomotives and advanced traction technologies.

Hydrogen propulsion offers another promising avenue for growth. Regions lacking extensive electrification infrastructure are exploring hydrogen-powered solutions as an alternative to conventional diesel fleets. Pilot projects and technological advancements are gradually improving commercial viability, creating opportunities for early adopters and technology providers. This emerging segment may reshape competitive dynamics over the long term.

Market Challenges:

Slow Return on Investment to Hamper Market Development

Rail projects have long gestation periods, which makes operators and investors hesitant due to long payback timelines, especially in freight corridors, where rail competes directly with road transport. Additionally, uncertainty surrounding future energy and environmental policies complicates long-term planning and ROI assessments. Train engines have an operational lifespan ranging from 25 to 35 years. This delayed ROI poses a challenge for private investors and commercial operators looking for quicker financial returns, making them more cautious about investing in large-scale rail projects.

Impact of COVID-19

The government-enforced lockdowns and economic crisis triggered by the COVID-19 pandemic had widespread effects, including severe restrictions on mobility. The pandemic led to a global economic downturn and temporarily halted manufacturing and testing activities across several sectors. For instance, due to the pandemic, the Integral Coach factory based in India downsized its production target from 4402 to 1954 coaches. The industry witnessed a rapid recovery in 2021 as major players resumed development and manufacturing operations based on their individual capacities.

That year also witnessed an increase in deliveries due to the fulfillment of outstanding package backlogs from existing contracts. During the initial period of 2022, the industry witnessed a surge in long-term and short-term contracts aimed at accelerating rail infrastructure development across various high-demand regions. The post-pandemic period saw increased demand for electric trains, driven by government initiatives focused on lowering carbon emissions and promoting sustainable mobility.

Segmentation Analysis

By Propulsion Type

Based on propulsion type, the market is segmented into combustion and electric. The combustion sub-segment is further divided into diesel and hydrogen.

Electric

Rising Focus on Environmental Sustainability Boosted the Electric Segment Growth

The electric segment will account for the largest locomotive market share of 54.94% in 2026 and is anticipated to maintain its dominance during the forecast period. It is also the fastest-growing segment, registering the highest CAGR. As the leading rail economies of the globe are inclining toward the use of green energy for a better, sustainable future, the electrification of trains plays a significant role in this transformation.

Thus, the increase in interest in environmental safety and green energy will drive market growth over the long term. In March 2024, Turkey launched its first domestically produced electric locomotive, developed by TURASAS; the E5000 model features a 5 MW power rating and is suitable for both passenger and freight transport.

Electrification has become one of the most important structural themes within the locomotive market. Electric locomotives offer lower operating costs, higher efficiency, and reduced emissions compared with conventional alternatives. Consequently, governments and railway operators increasingly prioritize electrified corridors as part of broader climate strategies.

Passenger transportation systems account for a significant portion of electric locomotive demand. High-speed rail networks and metropolitan transit projects require reliable and energy-efficient traction solutions capable of supporting intensive operations. Freight applications are also expanding, particularly across regions with extensive electrified infrastructure.

Technological advancements continue to enhance the attractiveness of electric locomotives. Improvements in traction systems, regenerative braking capabilities, and power electronics contribute to lower lifecycle costs and improved energy utilization. Such developments strengthen the economic case for electrification.

Combustion (Diesel and Hydrogen)

The diesel segment held a decent market share in 2024. The demand for diesel models is attributed to the high need for freight rail transportation and the relatively low infrastructural costs, as diesel engines can operate on existing tracks without the need for electrification or substations. Thus, developing economies and countries with limited rail infrastructure resources continue to prefer diesel units for cargo and freight operations.

Operational flexibility remains the principal advantage supporting combustion-based locomotives. Diesel systems continue to serve routes where electrification infrastructure is economically impractical or geographically challenging. Mining operations, long-distance freight corridors, and remote transportation networks frequently rely on diesel propulsion because of its established ecosystem and refueling convenience.

Hydrogen technologies are introducing a new dimension to the combustion segment. Railway operators are increasingly evaluating hydrogen fuel systems to achieve decarbonization objectives without extensive investments in electrified infrastructure. These solutions are particularly relevant for regional routes characterized by moderate traffic density.

Economic considerations significantly influence adoption patterns. Existing diesel fleets represent substantial capital assets, encouraging operators to extend service life through upgrades and efficiency improvements. Hybrid solutions and lower-emission engines are also attracting attention as transitional technologies.

By Component

Based on components, the market is segmented into rectifier, alternator, motor, and others.

Motor

Motor Segment Displayed the Highest Growth Rate due to Technological Advancements and Retrofitting Initiatives.

The motor segment accounted for the highest growth rate owing to the strong focus of major players on developing and deploying high-efficiency traction motors. These motors help reduce power losses while improving overall power distribution to the wheels. Continuous innovation by manufacturers to provide energy-efficient motors with lower power consumption is expected to further drive the growth of this segment.

For instance, in February 2025, Muller Technologies, a Swiss-based company, retrofitted its 1990s-era diesel engine with ABB’s advanced traction systems to support sustainable hybrid operations. The upgraded Aeam 841 will operate in three modes, including an overhead line, a traction battery, and a 500 KW diesel engine.

Traction motors represent one of the most critical elements influencing locomotive performance. Power output, energy efficiency, and reliability determine overall operational effectiveness and lifecycle economics. Consequently, continuous innovation in motor technologies remains a strategic priority for manufacturers.

Electric locomotives and high-speed rail systems increasingly require sophisticated motor architectures capable of delivering superior acceleration and energy utilization. Advancements in materials and cooling systems are improving performance and reducing maintenance requirements.

Digital monitoring and predictive maintenance capabilities further enhance asset management. These developments position traction motors as a central component supporting long-term locomotive market growth.

Rectifier

Power conversion efficiency underpins the strategic importance of rectifiers within locomotive systems. These components regulate electrical flow and ensure stable traction performance across varying operating conditions. Reliability and energy management capabilities strongly influence product selection.

Modern railway networks increasingly require advanced rectification technologies capable of supporting higher efficiency standards. Integration with digital monitoring systems enhances operational visibility and reduces maintenance requirements.

Technological improvements and rising electrification investments continue to support demand. Rectifiers are therefore expected to maintain an essential role within the evolving locomotive ecosystem.

Alternator

Mechanical energy conversion capabilities make alternators indispensable for diesel and hybrid locomotives. These components provide the electrical power required for auxiliary systems and traction operations. Performance characteristics directly influence operational efficiency and reliability.

Fleet modernization initiatives are encouraging the adoption of advanced alternator technologies offering improved durability and energy conversion capabilities. Manufacturers are emphasizing lightweight designs and optimized performance characteristics to address evolving customer expectations.

Although electrification reduces dependence on conventional systems in certain markets, alternators remain important across combustion-based applications. Their continued relevance supports steady demand within the locomotive industry.

The other segment dominated the global market share of 76.06% in 2026, owing to the increasing number of components used in locomotives to improve the efficiency of the machine. Additionally, the segment encompasses a wide range of major and minor components essential for optimum operational efficiency. The broad scope of this category significantly contributes to its greater market share within the component segment.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Based on technology, the market is segmented into IGBT Module, GTO Module, and SiC Module.

IGBT Module

Low Cost of IGBT Modules Contributed to Segment Growth

The IGBT module segment will lead the market with a share of 78.76% in 2026 and is expected to maintain its dominance during the forecast period. The dominance is attributed to several advantages, including lower cost, higher switching frequency, and lower power loss compared to GTO modules, which were commonly used in older models.

For instance, in August 2023, the TRAXX developed by Bombardier (Now Alstom) switched from GTO to IGBT-based traction inverters, starting with second-generation models. These IGBT modules offer improved power efficiency, enhanced cooling, and superior performance, supporting outputs of up to 5,600 kW, especially in mixed traffic and cross-border operations. These performance and efficiency gains are expected to sustain the segment’s leadership during the forecast period.

Insulated Gate Bipolar Transistor (IGBT) modules currently represent the most widely adopted power electronics technology within modern locomotives. Their balance between efficiency, reliability, and cost-effectiveness makes them suitable for diverse operating conditions. Manufacturers increasingly integrate advanced IGBT systems to improve energy management and traction performance.

High-speed rail projects and electrified freight networks contribute substantially to demand. Operators seek technologies capable of supporting efficient power conversion while maintaining operational reliability. These requirements reinforce the strategic importance of IGBT modules.

Continuous innovation is improving thermal management and switching performance. Such advancements enhance energy efficiency and reduce maintenance requirements, strengthening the value proposition of IGBT-based systems.

Established supply chains and broad industry acceptance support the dominant position of this technology within the locomotive market.

SiC Module

SiC Modules are expected to grow at the highest rate owing to the additional benefits they offer compared to GTO modules and IGBT power modules. SiC modules are highly efficient and provide extremely low power loss compared to IGBT power modules and GTO modules. However, the high cost associated with SiC Modules remains a key barrier, potentially limiting their widespread adoption in the near term.

Silicon carbide technology is emerging as a transformative force within locomotive power electronics. Superior switching performance and lower energy losses provide meaningful efficiency advantages compared with conventional technologies. These characteristics support reduced cooling requirements and lower operating expenses.

Railway operators increasingly evaluate silicon carbide modules for high-speed and energy-intensive applications. Performance benefits align closely with sustainability objectives and lifecycle cost reduction strategies. As a result, adoption is expanding across advanced rail systems.

Research activity and manufacturing investments continue to improve commercial viability. Declining costs and technological maturation are strengthening the competitive position of silicon carbide solutions.

GTO Module

Gate Turn-Off Thyristor (GTO) technology retains relevance across legacy locomotive platforms and selected heavy-duty applications. Although newer solutions have gained prominence, numerous railway operators continue utilizing GTO-based systems because of their proven reliability and extensive installed base.

Replacement and modernization programs represent important demand drivers. Existing fleets often undergo upgrades rather than complete replacement, allowing GTO technologies to maintain a presence in the market. Lifecycle economics and compatibility considerations influence these decisions.

Operational durability remains a notable advantage. Heavy freight operations and demanding environments frequently benefit from the robustness associated with GTO systems. However, maintenance requirements and efficiency limitations are encouraging gradual migration toward more advanced alternatives.

By End User

Based on end users, the market is divided into passenger and freight.

Passenger

Increasing Demand for Public Transportation Encouraged Passenger Segment Growth

Freight

The freight segment is expected to grow at the fastest CAGR, owing to increasing demand for freight operations worldwide as a result of the expansion of e-commerce and logistics activities. Additionally, greater focus from major economies toward freight rail expansion in various regions is further expected to drive the freight segment growth. For instance, in August 2023, the Indian Cabinet approved various rail expansion projects worth USD 3.93 billion to expand the country’s rail infrastructure and strengthen its freight network.

Cargo transportation represents the economic backbone of the locomotive industry. Industrial output, cross-border trade, and growing e-commerce activity continue to increase demand for efficient freight solutions. Rail transport offers substantial advantages in terms of fuel efficiency and bulk cargo handling, supporting long-term investment across freight corridors.

Heavy-haul operations require locomotives capable of delivering high power output and operational reliability. Mining products, agricultural commodities, energy resources, and manufactured goods constitute major cargo categories supporting freight demand.

Cost efficiency remains a primary consideration for freight operators. Fuel consumption, maintenance expenses, and asset utilization strongly influence procurement decisions. Technological advancements aimed at improving traction efficiency and reducing downtime are therefore attracting considerable investment.

Locomotive Market Regional Insights:

Asia-Pacific Locomotive Market Analysis:

Asia Pacific Locomotive Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, the Asia Pacific market stood at USD 7.59 billion, representing 52.63% of global demand, and is projected to grow to USD 8.04 billion in 2026, and held the largest locomotive market share owing to the high frequency and demand for rail operations, coupled with an extensive rolling stock industry.

The rapid expansion of rail infrastructure across economies such as China, India, and Japan, where rail remains a primary means of transport, has significantly fueled the locomotive market growth in the region. Additionally, ongoing contracts for the procurement of orders from past years continue to support product demand.

Rapid urbanization and infrastructure development make the Asia-Pacific the largest growth center within the locomotive market. Expanding freight corridors and high-speed passenger networks create substantial demand for modern rail systems. Government investment programs and manufacturing capabilities support regional competitiveness. Electrification initiatives and increasing industrial activity contribute to sustained locomotive market growth across Asia-Pacific economies.

Additionally, countries in the region are also shifting toward sustainable transportation, adopting electric trains to reduce emissions. For instance, in May 2025, India launched a 9,000 HP electric freight engine, marking a key step in promoting sustainable transportation. The Japanese market is projected to reach USD 0.27 billion by 2026. The Chinese market is expected to reach USD 6.85 billion by 2026. The Indian market is projected to reach USD 0.47 billion by 2026.

Japan Locomotive Market:

Technological sophistication and advanced railway infrastructure define Japan's position within the locomotive market. High-speed transportation systems and strict efficiency standards encourage continuous innovation. Operators emphasize reliability, safety, and digital integration to optimize network performance. Research capabilities and experience in rail engineering strengthen Japan's influence on locomotive market trends and technological advancement globally.

China Locomotive Market:

Large-scale infrastructure investments and manufacturing capabilities make China a dominant force in the locomotive market. Expanding high-speed rail networks and freight transportation corridors support strong demand for advanced systems. Government policies promoting technological self-sufficiency are accelerating innovation. Export activities and continuous capacity expansion contribute significantly to locomotive market growth and international competitiveness.

North America Locomotive Market Analysis:

The market in North America reached USD 1.93 billion in 2025, representing 13.36% of total market revenue, and is projected to reach USD 2 billion in 2026. North America held a sustainable market share in 2025. The U.S. rail system is predominantly freight-centric, in contrast to many regions where passenger rail dominates. Over 80% of locomotives in service in the U.S. are dedicated to freight operations, primarily used by Class I railroads. This strong demand for freight transport ensures a stable market for diesel-electric and continues to drive innovations in the freight segment.

Infrastructure modernization and freight transportation efficiency underpin North America's position within the locomotive market. Fleet replacement programs and decarbonization objectives are encouraging investments in advanced propulsion technologies. Rail operators increasingly emphasize digital asset management and operational optimization. Strong industrial capabilities and growing interest in alternative fuels contribute to sustained locomotive market growth and long-term competitiveness across the region.

United States Locomotive Market:

The U.S. market is projected to reach USD 1.21 billion by 2026. Freight rail dominance and extensive logistics networks make the United States a strategically important locomotive market. Heavy-haul operations and intermodal transportation systems generate consistent demand for fleet modernization. Investments in digital technologies and lower-emission propulsion solutions are influencing procurement strategies. Manufacturing capabilities and supportive infrastructure spending continue to reinforce the country's contribution to locomotive market size expansion.

Europe Locomotive Market Analysis:

Europe contributed approximately USD 4.32 billion to the global market in 2025, accounting for 29.98% share, and is expected to reach USD 4.53 billion in 2026. Europe held the second-largest market share in 2025. Countries such as Germany play a significant role in the production and global supply of rail components.

Government initiatives promoting rail travel to lower carbon emissions are also contributing to market growth. For instance, in July 2022, Germany’s federal and state governments expanded their rail network in central Germany from Frankfurt to Saarland. The UK market is expected to reach USD 0.9 billion by 2026. The German market is projected to reach USD 1.4 billion by 2026.

Environmental regulations and widespread rail electrification support Europe's leadership in sustainable railway transportation. High-speed passenger services and cross-border freight corridors drive demand for advanced locomotive technologies. Policy frameworks emphasizing carbon reduction encourage fleet upgrades and electrification programs. Strong engineering expertise and long-established railway ecosystems contribute to steady locomotive market growth throughout the region.

Germany Locomotive Market:

Industrial strength and engineering excellence position Germany among the most influential locomotive markets worldwide. Freight transportation networks and high-speed rail infrastructure support the continuous demand for technologically advanced systems. Digitalization and energy efficiency remain central priorities for operators and manufacturers. Research capabilities and export-oriented production reinforce Germany's significance within global locomotive market share dynamics.

United Kingdom Locomotive Market:

Rail modernization initiatives and sustainability commitments shape the United Kingdom locomotive market. Passenger transportation projects and decarbonization programs are encouraging fleet upgrades and infrastructure improvements. Operators increasingly prioritize energy efficiency and digital monitoring capabilities. Public investment and long-term transport policies support demand for advanced railway technologies and strengthen future locomotive market growth prospects.

Latin America Locomotive Market Analysis:

Commodity transportation and infrastructure investments are supporting locomotive demand across Latin America. Freight rail systems serving mining, agriculture, and industrial sectors remain central to regional development. Fleet modernization initiatives are gradually improving operational efficiency. Economic diversification and increasing logistics requirements create favorable conditions for long-term locomotive market growth throughout major Latin American economies.

Middle East & Africa Locomotive Market Analysis:

Infrastructure expansion and economic diversification are strengthening the Middle East & Africa locomotive market. Freight transportation projects and urban rail developments are increasing the demand for modern systems. Governments are investing in connectivity and logistics efficiency to support economic growth. Emerging railway networks and industrial development provide opportunities for sustained locomotive market growth.

The rest of the World recorded a market size of USD 0.58 billion in 2025, capturing 4.03% of the global market share, and is projected to reach USD 0.62 billion in 2026. In the Rest of the World, regions such as the Middle East, Africa, and Latin America are witnessing growth in the market due to the rising demand for electric propulsion and increasing investments in rail infrastructure. These regions are focusing on revitalizing their rail industries to promote sustainable mobility. For instance, Vale partners with Wabtec Corporation to eliminate its carbon footprint and introduce electric-powered engines for various hauling operations. In March 2025, Vale finalized a substantial diesel-electric models purchase agreement with Wabtec to acquire 50 new Evolution Series for its Vitoria a Minas and Carajas railroads in Brazil.

Competitive Landscape

Key Market Players

Key Players Focus on Innovation to Gain Competitive Edge

The global locomotive market is moderately consolidated yet highly competitive, shaped by rapid technological evolution, sustainability mandates, and strategic geographic expansion. Leading players such as Siemens AG, Hitachi Rail, Wabtec Corporation, Stadler Rail, and Alstom dominate the market by leveraging extensive R&D, global manufacturing capabilities, and long-term government contracts to maintain their market positions. These key players compete across various types, including diesel, electric, hybrid, and emerging hydrogen and battery electric platforms.

Market competitiveness is intensified by the growing demand for eco-friendly train engines that provide energy efficiency, pushing manufacturers to innovate with low-emission technologies, digital systems, and predictive maintenance tools. Stringent emission regulations, especially in Europe and North America, have further accelerated innovation in the industry.

Competitive dynamics within the locomotive market are shaped by engineering capabilities, power electronics expertise, lifecycle service offerings, and long-term customer relationships rather than manufacturing scale alone. Procurement decisions are heavily influenced by reliability, operating efficiency, maintenance economics, and regulatory compliance. Consequently, technological differentiation and after-sales support have become increasingly important determinants of competitive positioning.

Major manufacturers, including CRRC Corporation Limited, Siemens Mobility, Alstom, Wabtec Corporation, Hitachi Rail, Stadler Rail, Hyundai Rotem, CAF, Mitsubishi Heavy Industries, and Kawasaki Rail, maintain substantial locomotive market share through diversified portfolios and global delivery capabilities. Their competitive strength is reinforced by extensive installed bases, engineering expertise, and integrated service networks. Long-term maintenance contracts and digital fleet management solutions are increasingly supporting recurring revenue streams and customer retention.

Energy transition priorities are reshaping competitive strategies. Leading participants are allocating resources toward battery-electric technologies, hydrogen propulsion systems, and high-efficiency traction architectures to address evolving environmental requirements. Digital platforms supporting predictive maintenance and remote diagnostics are also emerging as key differentiators. These capabilities enable operators to improve asset utilization and reduce lifecycle costs.

Strategic partnerships are becoming more common across the locomotive ecosystem. Manufacturers are collaborating with power electronics suppliers, infrastructure developers, software providers, and national railway operators to accelerate innovation and strengthen market access. Localization agreements and technology transfer arrangements are particularly important in emerging economies, where governments increasingly prioritize domestic manufacturing capabilities.

Smaller and niche participants compete through specialization and regional expertise. Customized locomotives, refurbishment services, and component technologies provide opportunities for differentiated positioning. Suppliers possessing advanced capabilities in silicon carbide power electronics, traction motors, and intelligent control systems are expected to strengthen their competitive standing as locomotive market trends increasingly favor energy efficiency and digitalization.

The competitive environment is also being influenced by sustainability considerations and supply chain resilience. Companies capable of combining technological innovation, manufacturing flexibility, and lifecycle support services are likely to maintain stronger positions and support long-term locomotive market growth.

List of Key Locomotive Companies Profiled

- Progress Rail (U.S.)

- General Electric Company (U.S.)

- Anglo Belgian Corporation NV (Belgium)

- Toshiba Corporation (Japan)

- Cummins Inc. (U.S.)

- CRRC Corporation Limited (CRRC) (China)

- San Engineering (India)

- Alstom SA (France)

- Siemens AG (Germany)

- Kawasaki Heavy Industries, Ltd. (Taiwan)

- Kolomensky Zavod (Russia)

- Bharat Heavy Electricals Limited (BHEL)

- Chittaranjan Locomotive Works (India)

- CAF, Construcciones y Auxiliar de Ferrocarriles, S.A. (Spain)

- Hyundai Rotem Company (South Korea)

- Stadler, Inc. (Switzerland)

- Hitachi Rail Limited (U.K.)

- Republic Locomotive (U.S.)

- Wabtec Corporation (U.S.)

- Medha (India)

Key Industry Developments:

- May 2025- Siemens Mobility introduced the Vectron Dual Mode engine, combining electric and diesel propulsion systems powered by Cummins engines. This hybrid model delivers 2,210 kW in electric mode and 750 kW in diesel mode, achieving a maximum speed of 120 km/h.

- April 2025- TMH (Transmashholding), the parent company of Kolomensky Zavod, launched the Class DP2D diesel-powered push-pull train for Russian Railways (RZD). This train combines a six-axle TEP70BS diesel model, built by Kolomensky Zavod, with modified EP2DM EMU cars from the Demikhovsky Engineering plant. Designed for non-electrified suburban lines, the train can consist of two to six cars, including a driving tráiler, and accommodates up to 636 passengers with provision for wheelchair users.

- March 2025- CLW achieved a historic milestone by producing 700 electric-propelled engines in the fiscal year 2024-2025, marking the highest annual output in its history. This accomplishment underscores CLW’s commitment to enhancing India’s railway infrastructure and reflects its operational excellence in locomotive manufacturing.

- September 2024- SBB Cargo signed a framework agreement with Stadler Rail to procure up to 129 Bo’Bo’ multisystem train engines, beginning with an initial order of 36 units. These advanced electric models are compatible with 25 kV AC, 15 kV AC, and 3 kV DC systems and are designed to replace the aging Re420 fleet.

- August 2024- Medha unveiled the SMH-10 diesel, a 3,00 hp unit designed for freight and mixed-use rail operations. The locomotive features microprocessor-based control, electronically managed fuel systems, and modern diagnostics. Built for speeds up to 120 km/h, it is tailored for both industrial and marine use. With low maintenance needs and high fuel efficiency, the SMH-10 represents Medha’s commitment to enhancing the performance of diesel rail fleets across diverse geographic areas.

Investment Analysis and Opportunities

The global locomotive market presents strong investment opportunities, driven by increasing demand for sustainable transport, urbanization, and the ongoing modernization of rail networks. Key areas attracting investment include electric and hybrid models, hydrogen propulsion, and digitalization of rail operations. Emerging economies are focusing on infrastructure expansion, while developed regions are upgrading and expanding their fleets to comply with stringent emission norms. Investors focusing on innovative technologies and aftermarket services stand to benefit significantly, especially as countries commit to net-zero transportation targets and increasingly shift freight transport from road to rail.

For instance, in May 2025, Siemens Mobility unveiled India’s first 9,000-horsepower electric freight model, the WAG D-9, at the Indian Railway’s Dahod facility. This Co’Co’ configured engine, operating on 25 kV AC, is designed to haul 4,500-ton loads at speeds up to 120 km/h. It is part of a EUR 3 billion (USD 3.3 billion) contract for the supply of 1,200 units and incorporates AI-driven diagnostics and the Kavach safety system. The initiative aims to enhance freight efficiency and support India’s carbon reduction goals.

Report Coverage

The global locomotive market report analyzes the market in-depth. It highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, propulsion type, component, technology, and end-user. Besides this, the report provides insights into the market trends and highlights significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 9.43% from 2026 to 2034 |

|

Unit |

Value (USD billion) & Volume (Units) |

|

Segmentation |

Propulsion Type

By Component

By Technology

By End-user

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market was valued at USD 14.42 billion in 2025 and is projected to reach USD 31.25 billion by 2034.

The market is expected to register a CAGR of 9.43% during the forecast period.

The rising focus on expanding rail networks in developed and developing nations is expected to drive market growth.

Asia Pacific led the global market in 2025.

By end-user, the passenger segment led the market in 2025.

High costs associated with rail systems and slow return on investment hinder the markets growth.

- 2021-2034

- 2025

- 2021-2024

- 287

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us