Air Cargo Market Size, Share, Industry & Market Analysis, By Cargo Type (Bulk Cargo, Critical Cargo, General Cargo, and Others), By Carrier (Cargo Airline, Commercial Airline, and E-commerce Airline), By Destination (Domestic and International), and By End-User (Commercial and Civil, Healthcare, E-commerce, and Others), and Regional Forecast, 2025-2032

Air Cargo Market Size and Industry Overview

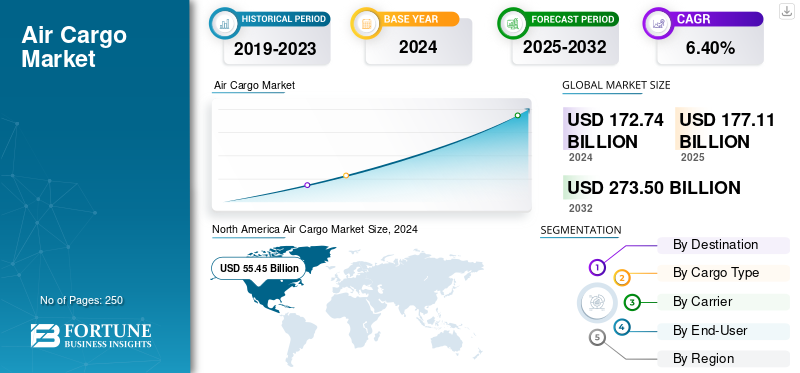

The global air cargo market size was valued at USD 172.74 billion in 2024. The market is projected to grow from USD 177.11 billion in 2025 to USD 273.50 billion by 2032, exhibiting a compound annual growth rate CAGR of 6.40% during the forecast period. North America dominated the air cargo market with a industry share of 32.10% in 2024.

Air cargo, also known as air freight, refers to transporting and moving goods or shipments through charter or commercial airlines over long distances. It involves the carriage of goods by airline. Air freight services are most valuable for shipping courier shipments around the world, including airmail, air freight, and air express.

Global air freight is expected to gain traction in the forecast period owing to the growth in passenger-to-freighter conversions and the growing applications of air cargo services worldwide. The major players FedEx Express, DHL Aviation, UPS Airlines, Emirates SkyCargo, and Lufthansa Cargo dominate the air cargo market due to their extensive global logistics networks, strong fleet capacity, and integrated multimodal operations that ensure reliable, time-critical delivery. Their dominance is reinforced by advanced digital tracking systems, strategic airport hubs, and investments in temperature-controlled supply chains that cater to growing demand from e-commerce and pharma sectors.

Download Free sample to learn more about this report.

Air Cargo Market Key Takeaways

- 2024 Market Size: USD 172.74 billion

- 2025 Market Size: USD 177.11 billion

- 2032 Forecast Market Size: USD 273.50 billion

- CAGR: 6.40% from 2025–2032

- North America dominated the air cargo market with a 32.10% share in 2024.

- The cargo airline segment held over 59% of the market in 2024.

- The commercial and civil segment accounted for more than 45% of the market in 2024.

North America

North America remained the leading regional market, reaching USD 55.45 billion in 2024.

Europe

Europe maintained a strong market position supported by transatlantic trade and pharmaceutical logistics corridors.

Asia Pacific

Asia Pacific recorded robust growth, with carriers achieving around 10% year-over-year demand growth in 2025.

U.S.

Strong demand is supported by major air cargo operators, e-commerce growth, and extensive logistics networks.

Japan

The country remains an important air cargo hub, supported by advanced manufacturing and international trade activities.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Booming E-Commerce Industry to Boost Market Growth

The rapid expansion of e-commerce will promote air cargo growth in the near future. Complex e-commerce logistics heavily depend on local postal systems, express networks, and, in some cases, retailers' widely distributed internal networks. Air freight packages are not specifically identified as e-commerce by shippers and air carriers, as they are usually grouped in pockets with various documents and parcels. However, e-commerce will revolutionize customer expectations and air logistics. In addition, according to the World Cargo Forecast report by The Boeing Company, global e-commerce revenue is expected to more than double pre-pandemic levels by 2026 and reach more than five times the spending of 2015.

Increasing Passenger to Freighter Conversions Boost Market Growth

The passenger-to-cargo transition includes all preparatory work required to access the airframe structure, including dismantling the cabin interior to remove all items, such as seats, kitchen monuments, toilets, luggage bins, and liners. As supply chain logistics diversify and adapt to meet growing customer expectations, the need for new cargo aircraft has increased, with MROs working around the clock to meet customer requirements. However, the need for freight capacity by air is still very high, driven by global e-commerce sales that are expected to grow bi-fold in the forthcoming years and booming demand for international air orders. Therefore, Passenger to Freighter (PTF) conversion is expected to substantially drive the market in the forecast period.

For instance, in June 2023, Avensis Aviation, an innovative provider of passenger-to-cargo solutions, announced that USC GmbH (USC) became the first customer for its main-cabin cargo storage PTF conversion. NAVIS will be installed in USC’s Airbus A340-300 and A340-600 aircraft.

MARKET RESTRAINTS

Growing Preference Among Consumers Toward Naval Cargo to Limit Market Growth

Despite the numerous trends and growing demand for air cargo, a major limitation continues to hinder market growth to a certain extent. Many customers still prefer naval cargo or transport for shipping goods due to underlying reasons. The major reason customers prefer naval transport is cost benefits, since shipment cost by sea is much cheaper than air cargo, and the cargo carrying capacity of a ship is considerably higher. Although shipping goods is a more time-consuming and less reliable compared to air cargo, it remains the preferred option for some consumers, thereby hampering air cargo market growth.

MARKET OPPORTUNITIES

Reopened Belly Capacity and Digitally Bookable Lift Are Expanding High-Value Air Trade

Passenger networks have largely normalized, restoring wide-body belly capacity on trunk routes and unlocking more city-pairs for SMEs to ship time-definite goods (electronics, fashion drops, and perishables). This lowers unit costs compared to pure freighter lift and shortens replenishment cycles, a valuable advantage as retailers push smaller, faster turns and manufacturers protect against ocean freight volatility. Express and heavier B2B flows are also shifting to digital platforms that allow shippers to buy ad-hoc space or charter whole aircraft, improving speed-to-market without fixed contracts. As trade corridors rebalance, operators are adding selective freighter frequencies on Europe, Asia, and Middle East lanes to maintain reliability during seasonal peaks and geopolitical reroutes. Near-term opportunities lie in premium, time-definite products (pharma, semis, aerospace AOG), cross-border e-commerce, and hybrid belly and freighter strategies that monetize seasonality while maintaining service integrity.

- Oct 2025: IATA reported August 2025 air cargo demand up 4.1% YoY—sixth straight monthly gain—while Amazon Air opened excess capacity to third-party shippers, signaling flexible, on-demand access to lift.

Air Cargo MARKET TRENDS

Implementation of Block chain in Air Cargo to Bolster Market Growth

Block chain is a distributed ledger technology that uses ledgers stored on separate networked devices to ensure the accuracy and security of data. This technology can track and record air freight transactions securely and transparently, making it ideal for the air freight industry, where multiple parties are involved in the supply chain and accurate tracking of goods is essential to ensure accuracy. Airlines have now started implementing block chain in their air cargo operations to ensure operational efficiency. For instance,

- July 2025: Airport Authority Hong Kong showcased its block chain-enabled HKIA Cargo Data Platform at HKMA’s Data Summit. The platform integrates airlines, forwarders, and terminals to share trusted shipment data and unlock digital global trade finance.

MARKET CHALLENGES

Geopolitics & Airspace Detours to Challenge Air Cargo Industry Growth

Geopolitics and airspace detours directly hit air cargo costs, capacity, and reliability. When airlines must avoid restricted skies, flight times lengthen, fuel burn rises, and some routes need extra tech stops or reserve crews. These factors push flights beyond duty limits, cut down usable payload, and raise the unit cost per ton-km. Detours also break hub connectivity: missed waves reduce transfer options, making it harder to meet promised cut-offs and next-flight-out commitments. Carriers with access to shorter corridors gain a structural cost edge, fragmenting capacity and destabilizing rate structures. Operational planning becomes harder complex as permits, NOTAMs, and diplomatic waivers change with little notice, forcing last-minute re-routing, holding inventory buffers, and re-adjustments to ground handling.

Insurance and security surcharges creep up on certain corridors, while carbon exposure rises as longer routes burn more fuel and, in regulated markets, attract higher ETS/SAF costs. Downstream, Red Sea or canal disruptions stretch ocean legs, causing air-sea multimodal shipments to miss their handoffs even if flights are on time. The net effect is higher operating costs, tighter effective capacity, more schedule volatility, and greater risk of service credits or penalties. For shippers, that translates to unstable lead times and budgeting challenges; for carriers and forwarders, it results in margin compression unless they proactively reprice services, re-bank schedules, and offer productized guaranteed contingencies solutions.

Download Free sample to learn more about this report.

Air Cargo Market Segmentation Analysis

By Destination

Emergence of Regional Market Players Bolstered Domestic Segment Growth

Based on destination, the market is categorized into domestic and international.

The domestic segment accounted for a larger air cargo market share in 2024 and is expected to grow at a significant CAGR in the forecast period, owing to the availability and emergence of regional cargo services providers. In particular, with rising labor costs in countries such as China and growing freight rates, the economic benefits of outsourcing manufacturing are no longer as strong as they were before the COVID-19 pandemic. This shift, combined with modern consumers' desire for higher-quality products and short delivery times, has driven the growing popularity of on-shoring and nearshoring. As a result, many American companies have moved production from China to countries such as Mexico and Canada.

- August 2025- Guwahati’s LGBI airport set a monthly cargo record of 952 MT, underscoring rising domestic uplift from secondary cities as e-commerce, perishables, and industrial parts densify regional networks. Impact: stronger in-country connectivity and faster replenishment cycles beyond metro hubs.

By Cargo Type

Bulk Cargo Segment Led due to its Ability to Rides Pure Network Frequency

In terms of cargo type, the market is categorized into bulk cargo, critical cargo, general cargo, and others.

The bulk cargo segment dominated the market in 2024. Bulk cargo dominates as its growth scales with flight frequency rather than dependence on specialist infrastructure. Bulk/general cargo leads as it rides pure network frequency without needing cold chain. Freight forwarders can consolidate diverse SKUs and keep cut-offs tight, keeping unit costs predictable and allowing flexible uplift during peaks or route adjustments. As cross-border e-commerce broadens assortments, bulk cargo absorbs demand spikes faster than niche products, reinforcing its throughput advantages at major hubs.

- In July 2024, WorldACD reported general (mainstream) cargo tonnage outpaced special-cargo growth year-to-date, reversing the pattern witnessed in recent years. This evidence that diversified, low-touch shipments reclaimed momentum as networks normalized and shippers began prioritizing speed/price efficiency over specialist handling.

By Carrier

Bulk Cargo Segment Led due to its Ability to offer Night-Wave Connectivity

Based on the carrier, the market is segmented into cargo airlines, commercial airlines, and e-commerce airlines.

The cargo airline segment held a dominant position in 2024. By carrier, the cargo airline segment held over 59% in 2024. Dedicated cargo airlines offer schedule-independent main-deck capacity, night-wave connectivity, and outsized/ULD-flexible payloads, critical for time-critical products and lanes with thin passenger demand. Freighter operators can re-bank rotations around exporter cut-offs, protect peak seasons, and maintain service integrity during detours, keeping SLAs and yields more stable than belly-only supply. Replacement and fleet expansion programs further entrench this leadership, as newer freighters deliver better range, fuel burn, and loading capabilities.

- October 2025: Airbus’s 2025 Cargo GMF projects that the global freighter fleet is expected to rise by ~45%, reaching around ~3,420 aircraft by 2044. The growth will be split between replacements and expansion, with North America and Asia Pacific expected to account for nearly two-thirds of deliveries, signaling durable investment in cargo-airline capacity.

To know how our report can help streamline your business, Speak to Analyst

By End-User

Commercial and Civil Segment Led due to its Ability to Protect Revenue Streams By Avoiding Stock-outs

Based on end-user, the market is segmented into commercial and civil, healthcare, e-commerce, and others.

The commercial and civil segment dominated the market in 2024 and held more than 45% of share in the same year. Commercial and civil shippers (electronics, industrial components, fashion, and aerospace spares) use air freight to protect revenue streams by avoiding stock-outs, keeping product launch schedules on track, and shortening cash-to-cash cycles. This segment benefits most from dense belly and freighter networks, late cut-offs, and reliable hub connectivity that support high-frequency consolidations and fast replenishment across multiple markets. As product assortments widen and lifecycles shorten, buyers prioritize time-definite services and predictable handovers over the absolute lowest transport cost. Concurrent infrastructure upgrades at tier-1 gateways, including automation, smarter yard/ULD control, and integrated data flows, further reduce dwell times and variability, reinforcing air freight’s role as the premium mode for mainstream exporters.

- October 2025: Swissport entered China with a next-generation cargo terminal at Shanghai Pudong (PVG), in partnership with Smargo. The facility features automated processing and AI-driven control with around 1.2 million tonnes of design capacity. It is aimed at streamlining throughput for pan-industry exporters and e-commerce flows—directly strengthening service levels for commercial/civil shippers on Asia-Europe lanes.

Air Cargo Market Regional Outlook

The market is categorized by geography into Europe, North America, Asia Pacific, and the Rest of the World.

North America Air Cargo Market Size, 2024 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

North America

North America held the dominant share in 2023, valued at USD 54.12 billion, and retained its leading position in 2024 with USD 55.45 billion. The region continues to lead the industry, underpinned by integrators, strong transatlantic demand, and high-value tech/healthcare exports. The region remains a key region in terms of CTKs, with capacity diversified across belly and freighter fleets. This flexibility allows rapid switches between B2C surges and B2B replenishment. Policy shifts are reshaping e-commerce flows, but the region’s dense network and express infrastructure continue to underpin its scale. one major factor driving the growth of air cargo in the U.S. is due to the presence of major companies. The U.S. is home to large-scale players across the entire air-cargo value chain, where demand and capacity reinforce each other. Integrators such as UPS and FedEx anchor reliable, time-definite networks with dense domestic lift, while Amazon Air adds flex capacity and stimulates e-commerce volumes.

- September 2025: FedEx and UPS adjusted their air networks after U.S. de-minimis changes, rebalancing international and domestic capacity across gateways.

Europe

Strong transatlantic and intra-EU demand, established pharma corridors, and high belly capacity from long-haul passenger services continue to sustain Europe’s market share. However, geopolitical reroutes and Red Sea disruptions have elevated buffer times and operating costs, prompting carriers to blend belly and selective freighter lift to protect reliability. In March 2025, Red Sea disruptions increased sea-air hybrids into Europe, altering trade flows and underscoring the need for resilient air schedules.

Asia Pacific

The Asia Pacific region experiences rapid growth and is expected to grow at the highest CAGR in the air cargo market, driven by export-oriented manufacturing, cross-border e-commerce, and dense long-haul connections compared to North America and Europe. Network restorations and growing intra-Asia trade flows have boosted CTK’s growth above global averages. In May 2025, the IATA highlighted that APAC carriers reached ~10% Y-o-Y demand growth in CTK, which contributed to a global demand rise of 5.8%.

Rest Of The World

The rest of the world region would witness a moderate growth in this market. Growth is concentrated in regions where supportive policies and private capital are transforming gateways into export and logistics hubs. In the Middle East & Africa (MEA), Gulf hubs continue to aggregate Asia-Europe flows, while Africa accelerates perishables, pharma, and e-commerce with new cold chain and integrator capacity. Large-scale, multi-year infrastructure programs are expanding airside handling, warehousing, and cross-border visibility across the region. In Latin America (LATAM), increased freighter additions and widened belly networks are deepening links to Europe and the U.S., supporting electronics, automotive, and retail replenishment as e-commerce volume deepens across the region.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Focus on Product Launches to Reinforce their Market Position

The air cargo market analysis is consolidated, with several global and regional players operating within this industry. Key market players remain competitive while co-existing with emerging and domestic service providers. Major players in the industry include DHL GROUP (Germany), FedEx (U.S.), and other listed companies in the ranking analysis. United Parcel Service, Inc. is expected to lead the market owing to its global presence. Other prominent players involved in the market include All Nippon Airways Co. Ltd (ANA) (Japan), American Airlines (U.S.), Delta Airlines (U.S.), and others that continue to strengthen their market positions through new product launches and strategic partnerships, and acquisitions.

LIST OF KEY AIR CARGO COMPANIES PROFILED

- DHL GROUP (Germany)

- FedEx (U.S.)

- The Emirates Group (UAE)

- Cargolux Airlines International SA (Luxembourg)

- China Airlines Ltd (China)

- Turkish Cargo (Turkey)

- Qatar Airways Company QCSC (Qatar)

- Deutsche Lufthansa AG (Germany)

- Cathay Pacific Airways Limited (Hong Kong)

- All Nippon Airways Co. Ltd (ANA) (Japan)

KEY INDUSTRY DEVELOPMENTS

- May 2025 — PPG invested USD 380 million to build a new Shelby for North Carolina facility for aerospace coatings and sealants, expanding U.S. capacity and shortening lead times. The 198,000-sq-ft plant is targeted for completion in the first half of 2027 and will support full aerospace lines, boosting availability for OEM and MRO repaint programs.

- June 2025 — International Aerospace Coatings (IAC) raised over USD 240 Million through its inaugural investment-grade private placement to fund expansion. The financing strengthens paint shop capacity and modernizing efforts globally, improving turnaround times and access for airline livery, OEM ramp-ups, and special-mission work.

- June 2025 — Mankiewicz won two Airbus Supplier Awards (Accredited Supplier + Digitalization), reinforcing its approved-supplier status for cabin/exterior coatings. The recognition supports specification wins on Airbus programs and accelerates digitized adoption of color/paint workflow across OEM and MRO networks.

- July 2025 — Ryanair extended its paint agreement with MAAS Aviation to 2035, covering ~500 repaints in Maastricht and Kaunas. The long-term award secures sustained demand for narrowbody liveries as Ryanair grows toward 800 aircraft, underpinning steady throughput for paint applicators.

- July 2025 — AkzoNobel reported the first-year success of its VR paint training, deploying 26 simulators at OEMs/MROs (including Embraer and IAC). The program reduces rework and material waste while speeding skills transfer and standardizing application quality across global paint lines.

- October 2025 — MAAS Aviation extended its Airbus Mobile (U.S.) contract for five years, supporting the A320/A220 ramp-up with up to ~200 aircraft painted annually across five bays, tightening OEM takt times and U.S. single-aisle delivery cadence.

- October 2025 — AkzoNobel launched an AS7489-certified applicator training program, aligned with SAE’s new global standard. The initiative improves painter qualification, consistency, and compliance for aerospace organics, helping airlines and MROs cut defects and cycle times.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2019-2032 |

|

Base Year |

2024 |

|

Estimated Year |

2025 |

|

Forecast Period |

2025-2032 |

|

Historical Period |

2019-2023 |

|

Growth Rate |

CAGR of 6.40% from 2025-2032 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Destination, Cargo Type, Carrier, End-User, and Region |

|

By Destination |

· Domestic · International |

|

By Cargo Type |

· Bulk Cargo · Critical Cargo · General Cargo · Other |

|

By Carrier |

· Cargo Airline · Commercial Airline · E-Commerce Companies |

|

By End-User |

· Commercial and Civil · Healthcare · E-commerce |

|

By Geography |

By Region

o Middle East & Africa ( By Destination) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 172.74 billion in 2024 and is projected to reach USD 273.50 billion by 2032.

In 2024, the market value stood at USD 55.45 billion.

The market is expected to exhibit a CAGR of 6.40% during the forecast period (2025-2032).

The bulk cargo segment led the market by cargo type.

Increasing passenger to freighter conversions is a key factor driving market growth.

DHL GROUP (Germany), FedEx (U.S.), and The Emirates Group (UAE) are some of the prominent players in the market.

North America dominated the market in 2024.

- 2019-2032

- 2024

- 2019-2023

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us