Marine Telematics Market Size, Share & Industry Analysis, By Offering (Hardware, Connectivity, and Others), By Application (Fleet Tracking & Visibility, Vessel Performance, and Others), By Vessel Type (Commercial Cargo Vessels, Passenger Vessels, Offshore & Energy Vessels, and Others), By End User (Shipowners, Ship Operators, Charterers & Cargo Owners, and Others), By Technology (Sensor & Data Capture, Edge Processing, and Others), By Deployment Model (Vessel Deployment, Architecture, and Others), By Data Source (Navigation / Bridge, Machinery, and Others), and Regional Forecast 2026-2034

Marine Telematics Market Size and Future Outlook

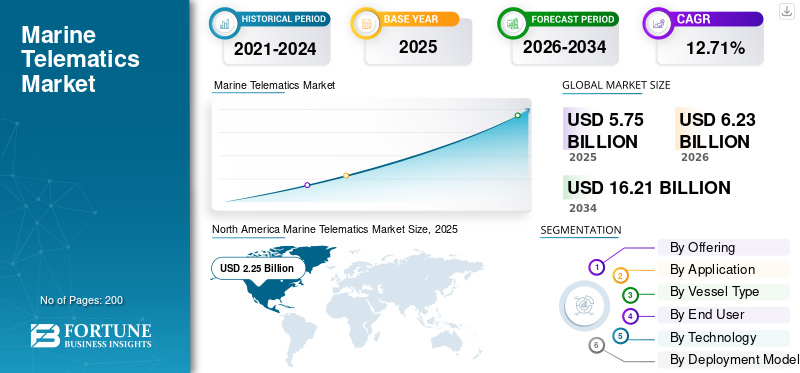

The global marine telematics market size was valued at USD 5.75 billion in 2025. The market is projected to grow from USD 6.23 billion in 2026 to USD 16.21 billion by 2034, exhibiting a CAGR of 12.71% during the forecast period. North America dominated the marine telematics market with a market share of 39.13% in 2025.

The marine telematics market covers digital systems that collect, transmit, and analyze vessel data such as location, fuel use, engine health, real time data transmission, voyage performance, cargo status, safety alerts, real time vessel tracking, and emissions. In practical terms, it sits at the intersection of satellite connectivity, AIS/GPS tracking, IoT sensors, vessel-performance software, and cloud analytics, helping shipowners run fleets with better visibility and lower operating risk.

The market growth is being driven by rising pressure to improve fuel efficiency, voyage optimization, fleet uptime, safety, compliance, and emissions reporting. The regulatory push is especially strong as IMO’s 2023 GHG strategy targets net-zero emissions from international shipping by or around 2050, with interim reduction checkpoints for 2030 and 2040, making data-led vessel monitoring more valuable for operators.

Major key players include Kongsberg Maritime, Wärtsilä, Inmarsat Maritime/Viasat, Marlink, and Danelec.

Download Free sample to learn more about this report.

Marine Telematics Market Key Takeaways

- 2025 Market Size: USD 5.75 billion

- 2026 Market Size: USD 6.23 billion

- 2034 Forecast Market Size: USD 16.21 billion

- CAGR: 12.71% from 2026–2034

- North America dominated the marine telematics market with a 39.13% share in 2025.

- The government & defense sub-segment accounted for the largest market share of 52.95% in 2025.

- The fleet tracking & visibility sub-segment is expected to witness the fastest growth during the forecast period.

North America

North America led the global marine telematics market with a value of USD 2.25 billion in 2025 and maintained its leadership at USD 2.42 billion in 2026.

Europe

Europe was valued at USD 1.38 billion in 2025 and is projected to register the highest CAGR of 14.46% during the forecast period.

Asia Pacific

Asia Pacific accounted for USD 1.59 billion in 2025, making it the second-largest regional market.

U.S.

U.S. The marine telematics market reached USD 2.06 billion in 2025.

Japan

Japan The marine telematics market was valued at USD 0.24 billion in 2025.

Read More

Marine Telematics Market Trends

Shift Toward Multi-Orbit Connectivity, AI, Digital Twins, and Cloud-Ready Vessel Systems to be a Significant Market Trend

The major technology trend is the move from single-channel vessel tracking to always-on, multi-orbit, multi-band, cloud-connected marine telematics. Operators increasingly want shore-like connectivity at sea so they can run cloud applications, cybersecurity monitoring, remote support, video calls, automated reporting, and data exchange between vessel and office without long delays. Inmarsat’s NexusWave is a good example as it bonds GEO Ka-band, LEO, LTE, and L-band networks rather than simply switching between them, supporting real-time data exchange and digital operations.

For instance, in April 2026, Viasat confirmed the scheduled launch of ViaSat-3 F3, designed to expand Asia Pacific capacity and support commercial mobility, fixed services, and defense customers.

Market Dynamics

MARKET DRIVERS

Download Free sample to learn more about this report.

Decarbonization, Compliance Reporting, and Connected-Fleet Efficiency are Making Vessel Data a Business Requirement

Marine telematics is being pushed by one clear business need, shipowners must know, in near-real time, how their vessels are performing, consuming fuel, enabling real time monitoring, emitting carbon, and meeting voyage targets. The regulatory pressure is becoming stronger as IMO approved draft net-zero shipping regulations in April 2025, including a marine fuel standard and GHG pricing mechanism for large ocean-going ships above 5,000 GT, which IMO says account for about 85% of international shipping CO₂ emissions. The European Union’s FuelEU Maritime rules are also forcing operators to monitor onboard energy use from 1 January 2025, with GHG-intensity reduction requirements moving from -2% in 2025 to -80% by 2050.

For instance, in February 2026, Inmarsat Maritime said it would install NexusWave across Auerbach’s newbuild heavy-lift vessels, linking high-speed connectivity with mission-critical ship systems, regulatory compliance, and modern eco-efficient vessels.

MARKET RESTRAINTS

Cybersecurity, Fragmented Systems, and Retrofit Complexity Slow Adoption Despite Clear Operational Benefits

The biggest restraint in global marine telematics market growth is not lack of interest; it is the difficulty of safely integrating telematics into mixed-age fleets with different bridge systems, engines, sensors, satellite terminals, and legacy software. As vessels become more connected, the cyber risk increases as IT and OT systems are no longer isolated, and a weak shore-side network, cloud service, or poorly protected onboard device can affect vessel operations. The U.S. Coast Guard noted in May 2025 that improved satellite connectivity has made vessels more efficient but also more vulnerable to cyberattacks, especially as IT/OT separation becomes blurred.

For instance, in March 2026, Danelec and Thetius highlighted that many shipping companies still struggle with fragmented digital environments, overlapping datasets, and slow decision-making even after investing in digital tools.

MARKET OPPORTUNITIES

Integrated Data Platforms can Turn Telematics from a Cost-Control Tool into a Performance and Service Ecosystem

The strongest opportunity is in integrated platforms that connect vessel performance, compliance, maintenance, hull condition, voyage planning, and procurement decisions in one workflow. This is important as shipowners do not only want more data; they want decision-ready data that reduces fuel cost, avoids off-hire, improves safety, supports emissions reporting, and justifies maintenance spending. GTT’s July 31, 2025 completion of the Danelec acquisition shows this shift clearly, as GTT combined Danelec with Ascenz Marorka and Vessel Performance Solutions to build a broader digital division covering more than 17,000 vessels.

For instance, in April 2026, Danelec and CleanQuote announced a partnership linking vessel-performance insights with underwater inspection and hull-cleaning execution, helping operators move from detecting fouling-related operational efficiency loss to arranging corrective action across more than 1,000 ports.

MARKET CHALLENGES

Market Must Prove ROI While Managing Cybersecurity, Data Quality, and Regulatory Complexity at Same Time

The core challenge is that marine telematics must deliver measurable business value, not just dashboards. Shipowners are dealing with rising fuel consumption and compliance exposure, but they also face capex pressure, crew training needs, cyber audits, software integration work, and the risk of collecting data that is not trusted or not used. Danelec’s March 2026 digitalization analysis captured this problem well: more data has not automatically created better decisions, and in some cases has added noise, slowed processes, and reinforced reliance on experience rather than real-time evidence.

For instance, in November 2025, the U.S. Coast Guard released cybersecurity training and incident-reporting guidance documents tied to IT/OT personnel access and Marine Transportation System cybersecurity requirements.

SEGMENTATION ANALYSIS

By Offering

Software Segment Growth Accelerates as AI and Compliance Tools Scale

By offering, the market is classified into hardware, connectivity, software, data & API products, and services.

The software sub-segment is estimated to grow the fastest with a highest CAGR of 13.96% during the forecast period of 2026-2034. Its growth is being driven by demand for fleet dashboards, AI-based vessel analytics, predictive maintenance, emissions reporting, voyage optimization, and cybersecurity management. Shipowners are no longer buying telematics only as hardware; they are shifting toward software platforms that convert vessel data into fuel savings, operational visibility, and compliance decisions.

The hardware sub-segment accounted for the largest market share valued at 25.62% in the year 2025. In addition, the sub-segment is projected to grow at a CAGR of 11.88% during the forecast period.

By Application

Fleet Tracking & Visibility Segment Leads Growth as Operators Prioritize Real-Time Fleet Control and Safety Visibility

By application, the market is classified into fleet tracking & visibility, vessel performance, voyage optimization, machinery & asset health, compliance & reporting, cargo & container telematics, offshore & energy operations, crew & business connectivity, and others.

The fleet tracking & visibility sub-segment is estimated to grow the fastest with a highest CAGR of 14.85% during the forecast period of 2026-2034. This reflects the core value of marine telematics: knowing where vessels are, how they are moving, whether they are on schedule, and whether any operational risk is emerging. Fleet visibility is becoming a base requirement for shipping companies, offshore operators, port authorities, defense users, and cargo owners.

The crew & business connectivity sub-segment accounted for the largest market share valued at 16.79% in the year 2025. In addition, the sub-segment is projected to grow at a CAGR of 12.05% during the forecast period.

By Vessel Type

Government & Defense Segment Expands Fastest and Dominates Vessel Demand as Maritime Security and Sovereign Fleet Monitoring Become Strategic Priorities

By vessel type, the market is classified into commercial cargo vessels, passenger vessels, offshore & energy vessels, fishing & aquaculture, government & defense, and leisure & high-value marine.

The government & defense sub-segment is estimated to grow the fastest with a highest CAGR of 13.86% during the forecast period of 2026-2034. Also this sub-segment is accounted for the largest market share of 52.95% in year 2025. This growth comes from higher investment in maritime domain awareness, naval fleet tracking, coast guard and maritime operations, border security, search-and-rescue, and surveillance of exclusive economic zones. Government fleets need secure, reliable, and real-time data systems as maritime threats are becoming more complex.

The offshore & energy vessels sub-segment accounted for the second-largest market share valued at 15.34% in the year 2025. In addition, the sub-segment is projected to grow at a CAGR of 12.41% during the forecast period.

By End User

Government & Regulatory Bodies to Lead End-User Demand as Compliance Enforcement and Maritime Monitoring Move Toward Data-Led Operations

By end user, the market is classified into shipowners, ship operators, charterers & cargo owners, government & regulatory bodies, ports & terminals, and OEMS & shipyards.

The government & regulatory bodies sub-segment is estimated to grow the fastest with a highest CAGR of 13.86% during the forecast period of 2026-2034. Also this sub-segment accounted for the largest market share of 46.22% in year 2025. This shows that marine telematics is not only a commercial fleet management tool but also a governance and regulatory technology. Maritime authorities increasingly depend on digital vessel data for safety monitoring, environmental compliance, port control, fishing-zone management, and national maritime security.

The ship operators sub-segment accounted for the second-largest market share of 15.94% in year 2025. In addition, the sub-segment is projected to grow at a CAGR of 12.02% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Technology

Cybersecurity Segment Grows Fastest as Connected Vessels Face Higher Digital Risk

By technology, the market is classified into sensor & data capture, edge processing, communication network, data standards / protocols, cloud / platform, analytics & AI, cybersecurity, and integration.

The cybersecurity sub-segment is estimated to grow at the fastest with a highest CAGR of 14.90% during the forecast period of 2026-2034. The growth is driven by agencies aggressively shifting maritime cybersecurity from voluntary practice to strict compliance. Frameworks including the IMO's Cyber Risk Management Guidelines and the EU’s NIS2 Directive require vessels to prove active risk assessment and continuous security monitoring

The communication network sub-segment accounted for the largest market share valued at 27.19% in the year 2025. In addition, the sub-segment is projected to grow at a CAGR of 12.69% during the forecast period.

By Deployment Model

Data Ownership Segment Grows Fastest as Operators Demand Control Over Vessel Data

By deployment model, the market is classified into vessel deployment, architecture, commercial model, integration mode, and data ownership.

The data ownership sub-segment is estimated to grow the fastest with a highest CAGR of 13.48% during the forecast period of 2026-2034. This growth reflects a major industry shift as vessel operators want clearer control over who owns, stores, shares, and monetizes operational data. As telematics expands into emissions reporting, predictive maintenance, insurance, charter-party performance, and fleet benchmarking, data ownership becomes a business and compliance issue rather than only a technical matter.

The commercial model sub-segment accounted for the largest market share of 23.82% in the year 2025. In addition, the sub-segment is projected to grow at a CAGR of 12.51% during the forecast period.

By Data Source

External Data Segment Leads Growth as Weather, Port, AIS, Compliance, and Market Data Become Critical to Smarter Vessel Decisions

By data source, the market is classified into navigation / bridge, machinery, energy & fuel, cargo, safety & security, external data, and manual / commercial data.

The external data sub-segment is estimated to grow the fastest with a highest CAGR of 14.36% during the forecast period of 2026-2034. The growth is driven by the shipowners, fleet managers, and port operators increasingly relying on third-party data feeds to improve operational decisions. External data sources such as AIS, weather forecasts, ocean-current data, port congestion data, voyage risk alerts, and emissions-compliance datasets help operators move from simple vessel monitoring toward predictive voyage optimization.

The navigation / bridge sub-segment is accounted for the largest market share of 21.45% in the year 2025. In addition, the sub-segment is projected to grow at a CAGR of 12.10% during the forecast period.

Marine Telematics Market Regional Outlook

By region, the market is categorized into Europe, North America, Asia Pacific, and rest of the world.

North America

North America Marine Telematics Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the global marine telematics market share in 2025, valued at USD 2.25 billion, and also maintained the leading share in 2026, with USD 2.42 billion. The market is experiencing rapid growth, driven by an expanding base of both commercial and recreational vessels. Key factors include rising demands for 24/7 offshore connectivity, strict maritime safety regulations, and the need for advanced vessel tracking.

U.S. Marine Telematics Market

Based on North America's strong contribution and the U.S. dominance within the region, the U.S. market reached USD 2.06 billion in 2025 and is estimated to have a CAGR of 11.84% during the forecast period.

Europe

Europe is projected to grow with a highest CAGR of 14.46% during the forecast period. In 2025, the market value stood at USD 1.38 billion. This growth is driven by stricter environmental regulations, the digital transformation of maritime logistics, and the integration of AI to reduce fuel consumption. The European maritime sector's adoption of telematics is accelerating due to a combination of technological advancements and regional mandates.

U.K. Marine Telematics Market

The U.K. market was valued at USD 0.32 billion in 2025 and is estimated to grow at a rate of 14.26% during the forecast period.

Germany Marine Telematics Market

The German market was valued at USD 0.23 billion in 2025 and is estimated to grow at a rate of 15.14% during the forecast period.

France Marine Telematics Market

The France market was valued at USD 0.24 billion in 2025 and is estimated to grow at a rate of 13.06% during the forecast period.

Asia Pacific

The Asia Pacific market was valued at USD 1.59 billion in 2025 and secures the position of the second-largest region in the market. The Asia Pacific market is experiencing rapid expansion, driven by booming regional sea trade, stringent maritime safety regulations, and increased integration of IoT and AI. With major manufacturing hubs and expanding economies including China and India, the region fosters rapid growth for maritime logistics and smart shipping.

China Marine Telematics Market

The Chinese market was valued at USD 0.63 billion in 2025 and is estimated to grow at a rate of 11.92% during the forecast period.

India Marine Telematics Market

The Indian market was valued at USD 0.27 billion in 2025 and is estimated to grow at a rate of 12.55% during the forecast period.

Japan Marine Telematics Market

The Japanese market was valued at USD 0.24 billion in 2025 and is estimated to grow at a rate of 15.84% during the forecast period.

Rest of World

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market during the forecast period. The Latin America market was valued at USD 0.15 billion in 2025. Growth is driven primarily by offshore oil and gas expansion, port digitalization mandates, and the urgent need to protect valuable commercial fishing and cargo fleets against piracy and cargo theft.

The Middle East & Africa market was valued at USD 0.38 billion in 2025. The growth is driven by booming offshore energy exploration, massive investments in port infrastructure, real time tracking, and strict government maritime surveillance and security mandates.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players to Shift from Hardware Supply to Connected Fleet-Intelligence Platforms to Expand Market Share

The marine telematics industry is becoming more competitive as companies move beyond basic vessel tracking and connectivity toward full digital-fleet ecosystems. The strongest players are investing in bonded satellite connectivity, cloud-based fleet monitoring, AI-supported vessel performance, digital twins, emissions reporting, cybersecurity, and predictive maintenance. Recent developments show this shift clearly. Inmarsat Maritime/Viasat’s NexusWave won a maritime sector innovation award on March 2026 for its bonded, fully managed maritime connectivity service, while Wärtsilä is pushing AI and digital twins for smarter vessel-performance optimization.

Competition is also moving through consolidation and portfolio integration, where large maritime technology groups are buying or absorbing digital specialists to offer more complete solutions. Overall, the market is growing through platform-based services, subscription analytics, OEM partnerships, fleet-wide retrofit programs, and compliance-led digital upgrades rather than one-time equipment sales.

LIST OF KEY MARINE TELEMATICS COMPANIES PROFILED IN REPORT

- Wärtsilä Corporation (Finland)

- Kongsberg Maritime AS (Norway)

- ABB Ltd (Switzerland)

- Danelec Electronics A/S (Denmark)

- Viasat, Inc. (U.S.)

- Iridium Communications Inc. (U.S.)

- Marlink SAS (France)

- Navarino S.A. (Greece)

- GTMaritime Limited (U.K.)

- Dualog AS (Norway)

- Pole Star Global (U.K.)

- NAPA Oy (Finland)

- ZeroNorth A/S (Denmark)

- Space Exploration Technologies Corp (U.S.)

- Intellian Technologies Inc. (South Korea)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Contractor Inmarsat Maritime/Viasat received a contract from EXMAR; the contract covers rollout of NexusWave across EXMAR’s gas carrier fleet, using bonded GX Ka-band, LEO, LTE, and L-band connectivity to improve ship-to-shore operations, crew welfare, cybersecurity, and fleet management operating cost.

- February 2026: Contractors Marlink and Eutelsat received a multi-year agreement from CMA CGM Group; the project will deploy Eutelsat OneWeb LEO connectivity on more than 300 CMA CGM vessels through Marlink’s hybrid network and XChange NextGen edge platform.

- February 2026: Contractor Inmarsat Maritime/Viasat received a deal from Vega Reederei; the contract covers NexusWave connectivity and Fleet Secure cybersecurity tools for 10 new diesel-electric coaster vessels scheduled for delivery in 2026.

- January 2026: Contractor Inmarsat Maritime/Viasat received a fleetwide upgrade commitment from Evergreen Marine; the contract standardizes Evergreen’s fleet on NexusWave bonded connectivity to support digitalization, cybersecurity, predictive analytics, real-time reefer monitoring, and fleet-wide IoT.

- August 2025: Contractor Ascenz Marorka/GTT Group received a contract from Hudong-Zhonghua Shipbuilding; the contract covers installation of the Sloshield real-time monitoring and predictive analysis system on 24 LNG carriers to reduce sloshing risk and improve LNG cargo safety.

REPORT COVERAGE

The global marine telematics market report includes a comprehensive study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and global market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and prevalence by key regions. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2024 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.71% from 2026-2034 |

| Unit | USD Billion |

|

Segmentation |

By Offering

By Application

By Vessel Type

By End User

By Technology

By Deployment Model

By Data Source

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 5.75 billion in 2025 and is projected to reach USD 16.21 billion by 2034.

In 2025, the European market value stood at USD 1.38 billion.

The market is expected to exhibit a CAGR of 12.71% during the forecast period.

The government & defense sub-segment is expected to hold the highest CAGR over the forecast period.

Decarbonization, compliance reporting, and connected-fleet efficiency are making vessel data a business requirement.

Decarbonization, compliance reporting, and connected-fleet efficiency are making vessel data a business requirement.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us