Maritime Cybersecurity Market Size, Share & Industry Analysis, By Component (Solutions and Services), By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, and Operational Technology (OT) Security), By Deployment (On-premise and Cloud), By Organization Size (Large Enterprises and Small and Medium-sized Enterprises (SMEs)), By End User (Commercial Shipping, Naval and Defense, Port Operators, Offshore Operations, and Others), and Regional Forecast, 2026-2034

Maritime Cybersecurity Market Size and Future Outlook

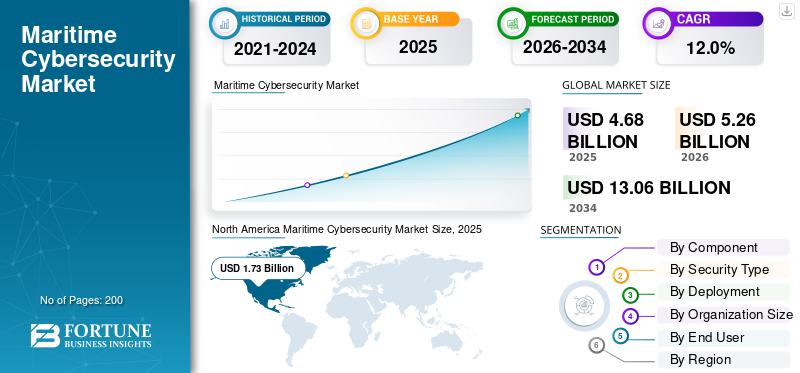

The global maritime cybersecurity market size was valued at USD 4.68 billion in 2025. The market is projected to grow from USD 5.26 billion in 2026 to USD 13.06 billion by 2034, exhibiting a CAGR of 12.0% during the forecast period. North America dominated the maritime cybersecurity market with a market share of 36.96% in 2025.

Maritime cybersecurity involves protecting ships, ports, offshore assets, and maritime communication networks from cyber threats, data breaches, and operational disruption. It includes threat detection, incident response, network monitoring, risk management, and security solutions for commercial shipping, naval operations, and port infrastructure. The market is increasingly centered on securing connected vessels, digitized port systems, and integrated maritime operations without interrupting safety, navigation, or logistics flow. The service adoption is supported by the need for continuous protection across onboard systems, shore-based control centers, and communication networks in an increasingly digital maritime environment.

Key players in the market include Naval Dome Ltd., Cydome Security Ltd., CyberOwl Ltd., ABS Group of Companies, Waterfall Security Solutions Ltd., Kongsberg Gruppen ASA, Northrop Grumman Corporation, Thales Group, BAE Systems plc, and Honeywell International Inc. These companies compete through stronger threat detection, broader cybersecurity portfolios, vessel and port protection capabilities, remote monitoring, compliance-focused services, and integrated security platforms tailored for shipping, naval, and critical maritime infrastructure applications.

Download Free sample to learn more about this report.

Maritime Cybersecurity Market Key Takeaways

- 2025 Market Size: USD 4.68 billion

- 2026 Market Size: USD 5.26 billion

- 2034 Forecast Market Size: USD 13.06 billion

- CAGR: 12.0% from 2026–2034

- North America dominated the maritime cybersecurity market with a 36.96% share in 2025.

- The on-premise segment is anticipated to witness the dominant market share over the forecast period.

- The large enterprises segment dominated the market share in 2025.

North America

North America maintained its leading position, with the market valued at USD 1.73 billion in 2026.

Europe

Europe is projected to become the second-largest regional market, reaching USD 1.49 billion in 2026.

Asia Pacific

Asia Pacific is expected to register the highest CAGR of 12.9% during the forecast period and reach USD 1.36 billion by 2026.

U.S.

U.S. The market is analytically approximated to reach USD 1.61 billion by 2026.

Japan

Japan The market is estimated to reach USD 0.25 billion by 2026.

Read More

MARITIME CYBERSECURITY MARKET TRENDS

Shift toward Integrated, AI-driven Maritime Security Platforms is an Emerging Market Trend

The market is moving toward integrated, AI-enabled security platforms rather than standalone protection tools. Operators are increasingly adopting solutions that combine network monitoring, anomaly detection, behavior analytics, and centralized incident response across vessels, ports, and remote operations. The market is also seeing stronger demand for managed cybersecurity services that support continuous monitoring and faster response. This trend reflects the growing need to secure interconnected maritime systems while maintaining operational continuity and safety across complex marine environments.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Cyber Risk across Maritime Operations Continue to Support Market Expansion

The maritime cybersecurity market growth is driven by the increasing exposure of ships, ports, and logistics networks to cyberattacks. As maritime operations adopt digital navigation, cloud connectivity, remote diagnostics, and automated control systems, the attack surface expands significantly. This raises the need for dedicated cyber protection to prevent disruption, data theft, safety incidents, and operational downtime. The growing awareness among ship operators about the financial and security impact of cyber incidents is also accelerating investment in maritime cybersecurity solutions.

MARKET RESTRAINTS

Legacy Systems and High Implementation Cost May Limit the Pace of Adoption

The market is restrained by the difficulty of securing older vessel and port infrastructure that was not designed for modern cyber protection. Many operators face high costs for upgrading networks, integrating security tools, and maintaining continuous protection across distributed assets. Budget constraints can delay deployment, especially among smaller fleets and regional operators. Limited internal cybersecurity expertise further slows adoption, making implementation more complex and increasing dependence on specialized vendors and service providers.

MARKET OPPORTUNITIES

Expansion of Digital Ship and Port Protection to Create Strong Market Opportunity

The maritime cybersecurity market holds strong opportunity as shipping fleets, ports, and offshore assets become more connected and software-dependent. New openings exist in retrofitting legacy vessels, securing operational technology environments, protecting remote access systems, and offering continuous monitoring for fleets operating across global trade routes. There is also growing demand for scalable solutions that can be deployed across small operators, large commercial fleets, and defense platforms. Providers that combine compliance support, threat intelligence, and maritime-specific protection can capture expanding demand.

MARKET CHALLENGES

Securing Connected Operations without Disrupting Performance are Major Market Challenges

A major challenge in the market is protecting highly connected operations without affecting navigation, communications, or cargo handling efficiency. Maritime environments often involve mixed legacy and digital systems, which makes integration and monitoring difficult. Operators must also manage evolving threats while meeting regulatory and operational requirements across different jurisdictions. Another challenge is reducing false alerts and ensuring that cyber defenses remain effective in harsh, remote, and operationally demanding marine conditions.

Segmentation Analysis

By Component

Rising Vessel Digitalization and Compliance Pressure to Drive Solutions Segment

Based on component, the market is segmented into solutions and services.

The solutions segment is anticipated to account for the largest maritime cybersecurity market share. The solutions demand is rising as maritime operators need integrated tools to secure shipboard networks, port systems, cloud platforms, and operational technology. Firewalls, endpoint protection, intrusion detection, vulnerability management, and OT monitoring are becoming essential as connected vessels and terminals face ransomware, spoofing, malware, and supply-chain cyber risks worldwide.

The services segment is anticipated to rise at a CAGR of 12.4% over the forecast period.

By Security Type

Increasing Ship-to-Shore Connectivity to Drive Network Security Segment Growth

Based on security type, the market is segmented into network security, endpoint security, application security, cloud security, and operational technology (OT) security.

In 2025, the network security segment dominated the global market. The demand for network security solutions is rising as vessels, ports, terminals, and offshore assets increasingly depend on interconnected communication systems. Operators need secure gateways, firewalls, segmentation, intrusion prevention, and traffic monitoring to protect navigation data, cargo systems, fleet communications, and shore-side networks from unauthorized access, malware movement, and operational disruption.

The operational technology (OT) security segment is projected to grow at a CAGR of 12.8% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment

Safety-Critical Maritime Operations to Drive the On-Premise Segment Growth

Based on deployment, the market is segmented into on-premise and cloud.

The on-premise segment is anticipated to witness a dominating market share over the forecast period. The demand for on-premise services is rising as many maritime cybersecurity functions must protect mission-critical systems close to operations. Ports, naval platforms, offshore facilities, and vessels often require local control, low-latency protection, data sovereignty, and secure OT isolation, making on-premise deployment important for safety-critical and regulation-sensitive maritime environments.

The cloud segment is projected to grow at a CAGR of 12.5% over the forecast period.

By Organization Size

Larger Attack Surfaces and Compliance Pressure to Drive Large Enterprises Segment Growth

Based on organization size, the market is segmented into large enterprises and small and medium-sized enterprises (SMEs).

The large enterprises segment dominated the market share in 2025. The segment is expanding as major shipping lines, port authorities, naval organizations, and offshore operators manage complex, high-value maritime networks. These users face larger attack surfaces, stricter compliance pressure, and higher disruption costs, pushing investment in enterprise-wide monitoring, managed security, OT protection, incident response, and cyber-resilience programs.

In addition, the small and medium-sized enterprises (SMEs) segment is projected to grow at a CAGR of 12.6% during the analysis period.

By End User

Connected Fleet Operations to Drive Commercial Shipping Segment Growth

Based on end user, the market is segmented into commercial shipping, naval and defense, port operators, offshore operations, and others.

The commercial shipping segment dominated the market share in 2025. The segment is expanding as fleets are becoming more connected through digital navigation, cargo management, remote monitoring, and cloud-based fleet operations. Shipowners need cybersecurity to protect vessel networks, crew systems, cargo data, and ship-to-shore communications while reducing downtime, compliance risk, and financial losses from cyber incidents.

In addition, the port operators segment is projected to grow at a CAGR of 13.0% during the analysis period.

Maritime Cybersecurity Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, and the rest of the world.

North America

North America Maritime Cybersecurity Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 1.52 billion, and also maintained the leading share in 2025, with USD 1.73 billion. The cybersecurity service demand is rising as ports, naval assets, offshore facilities, and commercial shipping networks face stronger cyber compliance pressure and higher investment in maritime infrastructure protection.

U.S. Maritime Cybersecurity Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1.61 billion in 2026. The U.S. market is anticipated to depict a CAGR of roughly 11.7% during the forecast period. Demand in the country is rising as naval modernization, port cybersecurity rules, offshore infrastructure protection, and commercial shipping digitalization are pushing higher cybersecurity investment.

Europe

The Europe market is estimated to reach a value of USD 1.49 billion in 2026 and secure the position of the second largest region in the market. The product demand is growing due to stricter cybersecurity regulation, advanced port automation, naval modernization, and rising protection needs across shipping, offshore energy, and maritime logistics networks.

U.K. Maritime Cybersecurity Market

The U.K. market is estimated to touch around USD 0.31 billion in 2026 and is poised to expand at a CAGR of roughly 11.5% over the forecast period. Demand in the U.K. is growing due to its strong maritime services ecosystem, naval programs, port security upgrades, and cyber-risk exposure across shipping and insurance operations.

Germany Maritime Cybersecurity Market

The Germany market is projected to reach approximately USD 0.27 billion in 2026. The product demand in Germany is rising as automated ports, industrial maritime systems, shipbuilding activity, and logistics networks require stronger protection against cyber disruption and OT attacks.

Asia Pacific

Asia Pacific is projected to record a CAGR of 12.9% during the forecast period, which is the highest among all regions, and reach a valuation of USD 1.36 billion by 2026. Demand in the region is increasing as China, India, Japan, and Southeast Asian economies expand port digitization, shipbuilding, naval modernization, and connected maritime trade infrastructure.

China Maritime Cybersecurity Market

The China market is projected to be one of the largest markets in the Asia Pacific region, with 2026 revenues estimated at around USD 0.50 billion. Demand in China is increasing as large ports, shipyards, shipping fleets, and naval modernization programs require stronger cybersecurity for connected maritime infrastructure and digital operations.

Japan Maritime Cybersecurity Market

The Japan market share is estimated to touch a value of around USD 0.25 billion in 2026, showcasing a CAGR of roughly 12.1% during the forecast period. The product demand in Japan is growing as advanced shipping operations, high-value port infrastructure, naval security needs, and maritime technology adoption require reliable cybersecurity protection.

India Maritime Cybersecurity Market

The India market is estimated to touch around USD 0.23 billion in 2026. Demand in India is rising as port modernization, naval expansion, coastal surveillance, and shipping digitalization are increasing the need for secure maritime networks and cyber resilience.

Rest of the World

The rest of the world includes the Middle East & Africa and Latin America. These regional markets are expected to witness moderate growth during the forecast period. The Middle East & Africa and Latin America markets are set to reach USD 0.31 billion and USD 0.17 billion, respectively, in 2026. Demand in the rest of the world is rising as Middle Eastern ports, offshore energy assets, and Latin American trade corridors are increasing their spending on maritime cyber resilience.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Focus on Integrated and Mission-Ready Cybersecurity Solutions to Strengthen their Market Positions

The maritime cybersecurity market landscape is being strengthened by key players that are shifting maritime protection from basic IT security toward integrated, mission-ready cyber resilience across vessels, ports, offshore assets, and naval platforms. Companies such as Naval Dome Ltd., Cydome Security Ltd., CyberOwl Ltd., ABS Group of Companies, Waterfall Security Solutions, Kongsberg Gruppen, and others are focusing on OT security, fleet-wide cyber monitoring, vulnerability management, managed detection and response, secure communications, network segmentation, compliance support, and resilient naval digital architectures. Naval Dome is positioning its maritime OT cyber-defense solutions around shipboard, port, and offshore systems, while Cydome and CyberOwl are strengthening demand through real-time fleet visibility, threat detection, cyber-risk monitoring, and compliance support for connected vessels. ABS Group is contributing through maritime risk, compliance, and cybersecurity services, while Waterfall is emphasizing hardware-enforced OT protection for critical industrial networks.

LIST OF KEY MARITIME CYBERSECURITY COMPANIES PROFILED IN REPORT

- Naval Dome Ltd. (Israel)

- Cydome Security Ltd. (Israel)

- CyberOwl Ltd. (U.K.)

- ABS Group of Companies, Inc. (U.S.)

- Waterfall Security Solutions Ltd. (Israel)

- Kongsberg Gruppen ASA (Norway)

- Northrop Grumman Corporation (U.S.)

- Thales Group (France)

- BAE Systems plc (U.K.)

- Honeywell International Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2025: Thales highlighted enhancements to its naval cybersecurity portfolio by incorporating AI-enabled threat detection and secure digital architectures into naval defense systems. This strengthened cyber resilience for modern maritime combat operations.

- June 2024: Speedcast integrated Cydome’s capabilities into its SIGMA platform, including real-time threat detection, AI-based analytics, vulnerability scanning, and SIEM functionality. The combined solution supports fleet-wide cybersecurity monitoring, regulatory compliance, and managed SOC services, helping maritime operators align with requirements such as IACS E26, IMO guidance, and NIS2.

- April 2023: ABS Wavesight entered a strategic partnership with ActZero to provide AI-powered cybersecurity solutions for the maritime sector. The collaboration aimed to improve threat detection, response, and cyber protection across fleet and port operations.

REPORT COVERAGE

This research offers a detailed analysis of emerging trends and rapidly adopted technologies in the industry across key regions. The report outlines key drivers of market growth and challenges to expansion, delivering a detailed overview of the maritime industry landscape. The study highlights recent advancements to boost industry insights and support stakeholders in making well-informed decisions.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 12.0% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, By Security Type, By Deployment, By Organization Size, By End User, and Region |

| By Component |

|

| By Security Type |

|

| By Deployment |

|

| By Organization Size |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4.68 billion in 2025 and is projected to reach USD 13.06 billion by 2034.

In 2025, the North America market value stood at USD 1.73 billion.

The market is expected to exhibit a CAGR of 12.0% during the forecast period of 2026-2034.

By end user, the commercial shipping segment dominated the market in 2025.

The rising cyber risk across maritime operations is a key factor supporting market expansion.

Naval Dome Ltd. (Israel), Cydome Security Ltd. (Israel), CyberOwl Ltd. (U.K.), ABS Group of Companies, Inc. (U.S.), Waterfall Security Solutions Ltd. (Israel), and Kongsberg Gruppen ASA (Norway) are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us