Maritime Simulator Market Size, Share & Industry Analysis, By Solution (Product and Service), By Type (Navigation Simulator – Desktop / Classroom (major), Navigation Simulator – Full Mission (major), Engine Room Simulator (ERS) – Desktop / Classroom (major), Engine Room Simulator (ERS) – Full Mission (major), Dynamic Positioning (DP) Simulator – Certified/High-fidelity (major), Cargo Operations Simulator – High-fidelity (major), and Others), By Application (Merchant Deep-Sea Vessels, Tankers, Gas Carriers, & and Others), By Platform, By End User, and Regional Forecast, 2026-2034

Maritime Simulator Market Size and Future Outlook

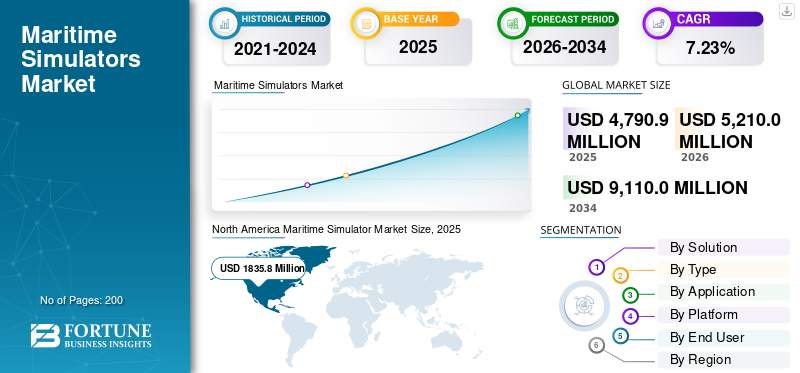

The global maritime simulator market size was valued at USD 4,790.9 million in 2025 and is projected to grow from USD 5,210.0 million in 2026 to USD 9,110.0 million by 2034, exhibiting a CAGR of 7.23% during the forecast period. North America dominated the global market with a market share of 38.31% in 2025.

Maritime simulators encompass advanced systems replicating ship bridge operations, engine rooms, cargo handling simulators, dynamic positioning, vessel traffic services, and safety scenarios for realistic training, research, design, and operational planning. Deployed in maritime training centers, academies, shipping fleets, naval forces, and port facilities globally, they serve seafarers, officers, engineers, and operators seeking competency without real-world risks. Key driving factors include stringent international safety regulations such as those from IMO, demand for cost-effective crew training amid rising maritime trade complexities, fatigue and human error mitigation, and the integration of VR/AR for enhanced adaptability.

Key players such as Kongsberg Digital (delivering digital twin-based full-mission suites for commercial and defense training), Wärtsilä (providing immersive navigation and engine simulators), alongside CAE, L3Harris, Seagull Maritime, and Northrop Grumman (focusing on tactical defense and compliance platforms), actively provide certified, modular solutions through partnerships and tech upgrades.

Download Free sample to learn more about this report.

Maritime Simulator Market Takeaways

- 2025 Market Size: USD 4,790.9 million

- 2026 Market Size: USD 5,210.0 million

- 2034 Forecast Market Size: USD 9,110.0 million

- CAGR: 7.23% from 2026–2034

- North America dominated the maritime simulator market with a 38.31% share in 2025.

- The Dynamic Positioning (DP) Simulator – Certified/High-fidelity segment is projected to grow at a 7.87% CAGR during the forecast period.

- The gas carriers segment is projected to expand at a 7.86% CAGR during the forecast period.

North America

North America led the market with USD 1,835.8 million in 2025 and is projected to maintain its dominant position through the forecast period.

Europe

Europe is projected to reach USD 1,259.8 million by 2026, supported by a 7.37% CAGR during the forecast period.

Asia Pacific

Asia Pacific is expected to reach USD 1,608.9 million by 2026, emerging as the fastest-growing regional market.

U.S.

The U.S. maritime simulator market is estimated to reach USD 1,278.6 million by 2026, growing at an approximate 7.30% CAGR.

Japan

The Japan market is projected to reach USD 307.9 million by 2026, registering an estimated 7.45% CAGR during the forecast period.

Read More

MARITIME SIMULATOR MARKET TRENDS

Integration of Virtual Reality (VR) and Augmented Reality (AR) is a Market Trend

The integration of virtual reality (VR) and augmented reality (AR) represents a pivotal trend in maritime operations, overlaying digital ship dynamics, hazards, and navigational cues onto real or virtual environments for hyper-realistic training. This fusion enables seafarers to practice complex maneuvers such as collision avoidance, engine troubleshooting, and emergency drills in fully immersive scenarios, enhancing situational awareness and decision making without physical risks. Furthermore, onboard and remote applications blend AR overlays with live operations for maintenance guidance and collaborative remote expertise, while VR supports self-paced modules for crew upskilling.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Escalating Global Maritime Trade Volumes and Vessel Complexity to Drive Market Growth

Escalating global maritime trade volumes and increasing vessel complexity drive maritime simulator market growth by necessitating advanced crew training for modern shipping demands. For instance, according to UNCTAD's Review of Maritime Transport 2025, seaborne trade reached 12,720 million tons loaded in 2024. Moreover, larger container ships, LNG carriers, and offshore support vessels demand proficiency in dynamic positioning, heavy weather handling, and multi-system integration, which simulators replicate risk-free. Operators and navies adopt simulators to upskill amid labor shortages, ensuring compliance with evolving IMO standards for safer, efficient global logistics.

MARKET RESTRAINTS

High Initial Acquisition to Restrain Market Expansion

High costs associated with initial acquisition serve as a primary market restraint for maritime simulators, limiting accessibility for smaller shipping firms, regional training academies, and operators in emerging economies. Sophisticated full-mission systems demand substantial investments in hardware such as high-resolution visuals, motion platforms, and multiscreen bridges, alongside custom software tailored to specific vessel types. The ongoing expenditures for periodic calibration, scenario updates, and compliance recertification compound financial barriers, diverting budgets from operational needs.

MARKET OPPORTUNITIES

Rise in Offshore Renewable Energy Projects to Create New Market Opportunities

A surge in offshore renewable energy projects presents a significant market opportunity for maritime simulators, as floating wind farms, wave energy converters, and tidal installations demand specialized training for support vessels navigating harsh conditions. Simulators replicate dynamic positioning amid turbulent currents, heavy-lift crane operations for turbine installation, and emergency response in remote ocean sites, building crew proficiency without weather dependent disruptions. Crews require modules for station keeping near massive substructures, cable-lay coordination, and ROV deployment for maintenance, addressing skills gaps in this nascent sector.

MARKET CHALLENGES

Cybersecurity Vulnerabilities to Present a Major Market Challenge

Cybersecurity vulnerabilities present a major challenge for the market, as networked platforms handling sensitive training data, vessel models, and real time scenarios become prime targets for cyberattacks. Cloud-connected systems enable remote access but expose them to ransomware, data interception, and manipulation of critical navigation algorithms during sessions. Integration with shipboard IoT and digital twins amplifies risks, potentially compromising proprietary fleet operations and maneuvers or defense tactics shared in simulations.

Segmentation Analysis

By Solution

Regulatory Compliance and Mandatory Training to Boost the Service Segmental Growth

Based on solution, the market is bifurcated into product and service.

The service segment is anticipated to account for the largest maritime simulator market share. The International Maritime Organization (IMO) has strict international laws that require maritime workers to complete thorough, approved training. To satisfy these requirements, services from accredited training facilities are crucial, which is a major factor propelling the segmental growth.

The product segment is anticipated to rise with a CAGR of 6.87% over the forecast period.

By Type

Maximum Fidelity to Boost Navigation Simulator – Full Mission (major) Segment Growth

Based on type, the market is segmented into Navigation Simulator – Desktop / Classroom (major), Navigation Simulator – Full Mission (major), Engine Room Simulator (ERS) – Desktop / Classroom (major), Engine Room Simulators (ERS) – Full Mission (major), Dynamic Positioning (DP) Simulator – Certified/High-fidelity (major), Cargo Operations Simulator – High-fidelity (major), and others.

In 2025, the Navigation Simulator – Full Mission (major) segment dominated the global market. These simulators offer the maximum level of realism (Class A), incorporating reproductions of real-world bridge equipment, which is a key factor driving segment growth.

The Dynamic Positioning (DP) Simulator – Certified/High-fidelity (major) segment is projected to grow at a high CAGR of 7.87% over the forecast period.

By Application

Rising Vessel Complexity and Technology to Boost Merchant Deep-Sea Vessels Segment Growth

Based on application, the market is segmented into merchant deep-sea vessels, tankers, gas carriers, passenger vessels, offshore vessels, and others.

The merchant deep-sea vessels segment is anticipated to witness a dominating market share over the forecast period. As modern merchant ships are equipped with complex, automated, and digital systems (integrated bridges, advanced engine rooms), simulators are crucial to train staff on these cutting-edge technology and avoid human error. This is a significant factor propelling the segmental dominance.

The gas carriers segment is projected to grow at a high CAGR of 7.86% over the forecast period.

By Platform

Reliability and Independence from Connectivity to Boost On-Premise Simulator Center Segment Growth

Based on platform, the market is segmented into on-premise simulator center, remote/networked instructor-led simulation, mobile deployable simulator, cloud-enabled / subscription simulation labs, and others.

The on-premise simulator center segment is anticipated to witness a dominating market share over the forecast period. As on premise simulator solutions function without the need for high speed internet, this eliminates latency issues or downtime caused by connectivity failures, driving the dominance of the segment.

The cloud-enabled / subscription simulation labs segment is projected to grow at a CAGR of 7.70% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By End User

Increased Demand for Crew Training to boost the Shipping Companies Segment

Based on end user, the market is segmented into maritime academies & universities, private maritime training centers, shipping companies, coast guard, and others.

The shipping companies segment dominated the global market share in 2025. Shipping businesses are investing extensively in in-house or hired simulator training due to the need for a skilled and well-trained personnel with the expansion of global seaborne trade. This is a significant factor driving the dominance of the segment.

In addition, the private maritime training centers segment is projected to grow at a high CAGR of 7.81% during the study period.

Maritime Simulator Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

North America

North America Maritime Simulator Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 1,737.6 million, and also maintained the leading share in 2025, with USD 1,835.8 million. Robust maritime infrastructure and U.S. Coast Guard mandates drive growth through advanced training for LNG carriers and offshore operations. Key players such as CAE dominate with full-mission simulators at major ports such as Houston and Long Beach, amid port modernization and naval contracts.

U.S. Maritime Simulator Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 1278.6 million in 2026, accounting for a CAGR of roughly 7.30% over the forecast period. The U.S. leads via stringent safety regulations and expanding LNG exports, fueling simulator demand at academies such as Massachusetts Maritime. CAE and L3Harris hold strong presence, supporting Great Lakes and Gulf Coast trade with VR-enhanced naval training.

Europe

Europe is projected to record a steady growth rate of 7.37% during the forecast period, which is the second highest among all regions, and reach a valuation of USD 1259.8 million by 2026. EU Green Deal and STCW compliance fuel the demand for eco-propulsion training across Rotterdam and Hamburg. Kongsberg Digital and Wärtsilä lead with certified centers.

U.K. Maritime Simulator Market

The U.K. market is estimated to touch a value of around USD 412.8 million in 2026, depicting a CAGR of 7.80% during the study period. Brexit-driven supply chain resilience and offshore wind projects enhance simulator needs at Felixstowe. CAE strengthens presence with dynamic positioning modules.

Germany Maritime Simulator Market

Germany’s market is projected to reach approximately USD 362.2 million in 2026. Shipbuilding expertise and Baltic trade routes drive VR integration at Hamburg ports. Rheinmetall partners for naval simulators.

Asia Pacific

The Asia Pacific region is estimated to reach USD 1608.9 million in 2026 and secure the position of the third-largest region, growing at the fastest pace during the study period. Rapid port development in Singapore and Shanghai hubs accelerates adoption for congested waterway navigation training. Kongsberg and Wärtsilä expand via regional partnerships, addressing crew shortages from booming container trade.

Japan Maritime Simulator Market

The Japan market is estimated to touch around USD 307.9 million in 2026, accounting for a CAGR of roughly 7.45% during the forecast period. Advanced shipbuilding innovation and aging workforce drive simulator use for automated vessel trials.

China Maritime Simulator Market

The China market is projected to be one of the largest in the Asia Pacific region, with 2026 revenues estimated at around USD 526.7 million. State-backed shipbuilding surge and Belt & Road initiatives boost simulators for mega-vessel handling at ports such as Ningbo-Zhoushan.

India Maritime Simulator Market

The India market is estimated to hit around USD 460.2 million in 2026. Port expansions at Mundra and JNPT, plus naval modernization, spur growth amid rising coastal trade. New entrants partner with Wärtsilä for affordable bridge simulators targeting officer upskilling.

Rest of the World

The rest of the world includes Middle East and Africa and Latin America. While ports in the Middle East such as Jebel Ali grow via oil/gas training, Latin America shows advancement at Santos with new Wärtsilä installs, driven by Panama Canal traffic and energy transitions. The Middle East & Africa and Latin America markets are set to reach USD 214.3 million and USD 136.3 million, respectively, in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Players Deploy Strategic Collaborations to Gain Edge over Competitors

Maritime simulator market remains consolidated, with dominant players such as Kongsberg Digital, Wärtsilä, CAE, L3Harris, Transas, Thales, Northrop Grumman, Seagull Maritime, and Rheinmetall commanding shares through certified training platforms.

Strategic collaborations accelerate expansion as Kongsberg Digital partners with global academies on K-Sim Navigation suites for autonomous vessel drills and Wärtsilä delivers VR-enhanced engine simulators to European training hubs alongside port authorities. Another instance is CAE’s partnership with offshore operators for dynamic positioning systems supporting renewable energy projects. Furthermore, L3Harris advances naval tactical simulators with defense forces, while Thales integrates AR modules for vessel traffic services. These alliances strengthen compliance with IMO standards amid complex trade routes and green transition demands.

LIST OF KEY MARITIME SIMULATOR COMPANIES PROFILED

- Kongsberg Maritime (Norway)

- Wärtsilä Voyage (Finland)

- CAE Inc. (Canada)

- L3Harris Technologies Inc. (U.S.)

- Transas (Russia)

- Thales Group (France)

- Northrop Grumman Corporation (U.S.)

- Seagull Maritime AS (Norway)

- Rheinmetall AG (Germany)

- VSTEP B.V. (Netherlands)

KEY INDUSTRY DEVELOPMENTS

- September 2025: Aboa Mare solidified its position as a top supplier of maritime training by purchasing a cutting-edge K-Sim Engine Full Mission and Desktop Simulator system from Kongsberg Maritime.

- March 2025: Kongsberg Maritime rolled out the K-Sim Offshore DP3 Anchor Handling Simulator. The simulator focuses on enhancing maritime safety and has been designed to train personnel for complex offshore operations.

- April 2024: Wärtsilä and Mevea improved their simulation collaboration by establishing a Strategic Supply and Purchase Agreement (SSPA). Wärtsilä would add port and ship crane training simulators to their existing portfolio of maritime training simulator as part of the global deal.

- November 2023: Svitzer selected Kongsberg Digital to supply cutting-edge simulators to enhance crew training at its Australian facility in Port of Newcastle. The agreement with Kongsberg would contribute to the establishment of a top-notch training facility for the use of Svitzer's cutting-edge, brand-new TRAnsverse tugboats, which would go into service in Newcastle in early 2025.

- November 2023: A new maritime training facility in Finland would receive its most recent simulator equipment from the technology business Wärtsilä. The Joint Authority of Education of Kotka-Hamina Region (Ekami) and the South-Eastern Finland University of Applied Sciences (Xamk) issued the directive.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.23% from 2026-2034 |

|

Unit |

Value (USD Million) |

|

Segmentation |

By Solution, Type, Application, Platform, End User, and Region |

|

By Solution |

· Product · Service |

|

By Type |

· Navigation Simulator – Desktop / Classroom (major) · Navigation Simulator – Full Mission (major) · Engine Room Simulator (ERS) – Desktop / Classroom (major) · Engine Room Simulator (ERS) – Full Mission (major) · Dynamic Positioning (DP) Simulator – Certified/High-fidelity (major) · Cargo Operations Simulator – High-fidelity (major) · Others |

|

By Application |

· Merchant deep-sea vessels · Tankers · Gas carriers · Passenger vessels · Offshore vessels · Others |

|

By Platform |

· On-premise simulator center · Remote/networked instructor-led simulation · Mobile deployable simulator · Cloud-enabled / subscription simulation labs · Others |

|

By End User |

· Maritime academies & universities · Private maritime training centers · Shipping companies · Coast guard · Others |

|

By Region |

· North America (By Solution, Type, Application, Platform, End User and Country) o U.S. (End User) o Canada (End User) · Europe (By Solution, Type, Application, Platform, End User and Country/Sub-region) o U.K. (End User) o Germany (End User) o France (End User) o Russia (End User) o Rest of Europe (End User) · Asia Pacific (By Solution, Type, Application, Platform, End User and Country/Sub-region) o China (End User) o India (End User) o Japan (End User) o South Korea (End User) o Rest of Asia Pacific (End User) · Rest of the World (By Solution, Type, Application, Platform, End User, and Country/Sub-region) o Middle East & Africa (End User) o Latin America (End User) |

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 4,790.9 million in 2025 and is projected to reach USD 9,110.0 million by 2034.

In 2025, the North America market value stood at USD 1,835.8 million.

The market is expected to exhibit a CAGR of 7.23% during the forecast period of 2026-2034.

By type, the service segment is expected to dominate the market.

Escalating global maritime trade volumes and vessel complexity are key factors anticipated to drive market growth

Kongsberg Digital, Wärtsilä, CAE, L3Harris, Transas, Thales, Northrop Grumman, Seagull Maritime, and Rheinmetall are few key players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us