Wood Adhesives Market Size, Share, and Industry Analysis, By Product (Urea-Formaldehyde (UF), Melamine urea-formaldehyde (MUF), Phenol-formaldehyde (PF), Isocyanates, Polyurethane, Polyvinyl acetate (PVA), and Others), By Technology (Solvent-Based, Water-Based, and Others), By Application (Flooring, Furniture, and Others), and Regional Forecast, 2026-2034

Wood Adhesives Market Overview

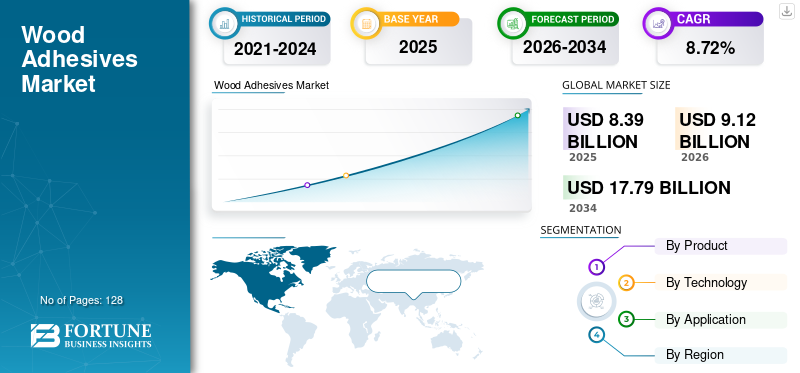

The global wood adhesives market size was valued at USD 8.39 billion in 2025. The market is projected to grow from USD 9.12 billion in 2026 to USD 17.79 billion by 2034, exhibiting a CAGR of 8.72% during the forecast period. The market in North America dominated with a revenue share of 21% in 2025.

The Wood Adhesives Market represents a critical component of the global materials and construction ecosystem, supporting bonding solutions for furniture, construction panels, flooring, cabinetry, and engineered wood products. Wood adhesives are formulated to provide strong bonding, durability, moisture resistance, and thermal stability across multiple wood substrates. The Wood Adhesives Market Analysis indicates strong alignment with trends in sustainable construction, engineered wood usage, and interior renovation activities. Manufacturers continue to invest in performance-enhancing formulations while responding to regulatory pressures on emissions and chemical safety. The Wood Adhesives Industry Report highlights rising adoption across residential, commercial, and industrial woodworking, driven by demand for reliable bonding solutions compatible with modern manufacturing processes.

The United States Wood Adhesives Market plays a pivotal role in the global industry due to its large-scale furniture manufacturing, housing renovation, and engineered wood production base. The Wood Adhesives Market Size in the USA is supported by strong domestic demand for plywood, particleboard, MDF, and laminated wood products. Adoption of water-based and low-emission adhesive solutions is accelerating due to environmental regulations and green building standards. The Wood Adhesives Market Insights for the USA emphasize strong penetration across construction, modular housing, and DIY woodworking segments, with innovation focused on durability, curing efficiency, and compatibility with automated production lines.

Download Free sample to learn more about this report.

Wood Adhesives Market KEY Takeaways

- 2025 Market Size: USD 8.39 Billion

- 2026 Market Size: USD 9.12 Billion

- 2034 Forecast Market Size: USD 17.79 Billion

- CAGR: 8.72% from 2026–2034

- The market in Asia-Pacific dominated with a revenue share of 42% in 2025.

- The North America market accounted for 21% of the global revenue in 2025.

- The Europe market held a 25% revenue share in 2025.

Asia-Pacific

Asia-Pacific led the global market with a 42% revenue share in 2025.

Europe

Europe accounted for a 25% share of the global market in 2025.

North America

North America captured a 21% share of the global market in 2025.

U.S

The U.S. remains a major contributor to the North American market growth.

Japan

Japan accounted for 6% of the Asia-Pacific market in 2025.

Read More

Wood Adhesives Market Latest Trends

The Wood Adhesives Market Trends reflect a shift toward sustainable, high-performance, and regulation-compliant bonding solutions. One of the most prominent trends in the Wood Adhesives Industry Analysis is the rapid adoption of water-based and bio-based adhesive technologies to meet environmental and indoor air quality standards. Manufacturers are increasingly developing low-formaldehyde and formaldehyde-free products to address emission concerns across furniture and construction sectors.

Download Free sample to learn more about this report.

Another key trend shaping the Wood Adhesives Market Outlook is the integration of advanced polymer chemistry, enabling faster curing times and improved resistance to heat and moisture. Automation in furniture manufacturing has further increased demand for adhesives compatible with high-speed processing and robotic application systems. Additionally, growth in engineered wood products such as cross-laminated timber and laminated veneer lumber is driving specialized adhesive formulations. The Wood Adhesives Market Research Report also notes rising demand from modular construction and prefabrication industries, reinforcing long-term growth potential and innovation-driven competition.

Wood Adhesives Market Dynamics

DRIVER

Expansion of Engineered Wood and Furniture Manufacturing

The primary driver of Wood Adhesives Market Growth is the expanding use of engineered wood products and large-scale furniture manufacturing. Engineered wood materials require reliable adhesive bonding to ensure structural integrity, durability, and dimensional stability. The Wood Adhesives Industry Report highlights increased production of MDF, plywood, and laminated boards across residential and commercial construction. Rising urbanization and interior remodeling activities further strengthen demand. Manufacturers benefit from consistent bulk consumption by furniture makers, flooring producers, and panel manufacturers, reinforcing stable market expansion across developed and emerging economies.

RESTRAINT

Environmental Regulations and Emission Standards

Environmental regulations remain a significant restraint within the Wood Adhesives Market. Restrictions on volatile organic compounds and formaldehyde emissions have increased compliance costs for manufacturers. The Wood Adhesives Market Analysis indicates that transitioning to compliant formulations requires investment in R&D, reformulation, and testing. Smaller producers face challenges adapting to regulatory changes, particularly in regions with strict indoor air quality standards. These constraints can delay product launches and increase operational complexity, affecting competitive positioning within the Wood Adhesives Industry.

OPPORTUNITY

Growth in Sustainable and Bio-Based Adhesives

An emerging opportunity within the Wood Adhesives Market lies in the development of sustainable and bio-based adhesive solutions. Demand for green building materials has accelerated interest in renewable raw materials and low-emission adhesives. The Wood Adhesives Market Opportunities section emphasizes increasing adoption across furniture, packaging, and construction sectors seeking sustainability certifications. Companies investing in plant-based polymers and recyclable adhesive systems are gaining competitive advantage. This opportunity aligns with long-term environmental goals and evolving consumer preferences.

CHALLENGE

Volatility in Raw Material Supply

Raw material price volatility represents a key challenge in the Wood Adhesives Market. Dependence on petrochemical derivatives and specialty resins exposes manufacturers to supply chain disruptions. The Wood Adhesives Market Insights highlight fluctuating costs impacting pricing strategies and profit margins. Managing inventory and securing alternative raw material sources has become critical. These challenges require strategic sourcing, supplier diversification, and long-term contracts to maintain operational stability.

Wood Adhesives Market Segmentation

By Product

To know how our report can help streamline your business, Speak to Analyst

Urea-formaldehyde adhesives account for 28% of the Wood Adhesives Market share, making them the most widely used adhesive type globally. These adhesives are extensively applied in particleboard, MDF, plywood, and interior furniture manufacturing. UF adhesives are preferred due to their low cost, fast curing time, and high production efficiency. They provide strong and rigid bonding suitable for flat wood panels. The Wood Adhesives Industry Analysis highlights consistent demand from large-scale panel manufacturers. UF formulations are compatible with automated and high-speed production lines. Modified low-emission UF variants support regulatory compliance. Their availability in powder and liquid forms enhances flexibility for manufacturers. Price-sensitive markets rely heavily on UF adhesives. Despite environmental scrutiny, UF remains dominant. Supply chain stability further supports adoption. UF adhesives are a core component of industrial woodworking.

Melamine urea-formaldehyde adhesives hold approximately 14% of the global Wood Adhesives Market share. MUF adhesives offer improved moisture and heat resistance compared to UF adhesives. They are widely used in exterior-grade plywood, laminated beams, and construction panels. The Wood Adhesives Market Analysis indicates strong demand from structural wood applications. MUF adhesives perform reliably under varying climatic conditions. Furniture and construction manufacturers value their durability. These adhesives balance performance and cost efficiency. MUF is commonly used where enhanced water resistance is required. Adoption is strong in residential and commercial construction. Manufacturers favor MUF for engineered wood products. Regulatory compliance supports steady market presence. MUF adhesives serve both interior and semi-exterior applications.

Phenol-formaldehyde adhesives represent nearly 12% of the Wood Adhesives Market share. PF adhesives are known for excellent water resistance and long-term durability. They are commonly used in exterior plywood, marine panels, and load-bearing structures. The Wood Adhesives Industry Report highlights PF adhesives as critical for structural applications. These adhesives maintain bonding strength under extreme conditions. PF adhesives support high-performance construction requirements. Their dark bond line limits decorative use but ensures strength. Demand is strong in infrastructure-related wood products. PF adhesives are suitable for outdoor exposure. Manufacturers value their reliability and longevity. Compliance with performance standards drives adoption. PF remains essential in heavy-duty woodworking.

Isocyanate-based adhesives account for approximately 10% of the Wood Adhesives Market share. These adhesives are formaldehyde-free, aligning with strict emission regulations. They are widely used in oriented strand board and engineered wood panels. The Wood Adhesives Market Insights highlight rising adoption due to environmental compliance. Isocyanates offer strong bonding and moisture resistance. They cure quickly and enhance production efficiency. Manufacturers favor them for high-performance applications. Worker safety requirements influence handling protocols. Demand is increasing in green building projects. Isocyanates support advanced wood composites. Cost remains higher than UF adhesives. Long-term sustainability drives growth.

Polyurethane adhesives hold nearly 15% of the global Wood Adhesives Market share. These adhesives provide flexible bonding and excellent moisture resistance. Polyurethane is widely used in flooring, furniture, and laminated wood products. The Wood Adhesives Market Growth in this segment is driven by versatility. These adhesives perform well across multiple substrates. Manufacturers value their strong adhesion and elasticity. Polyurethane adhesives support both interior and exterior applications. Demand is strong in premium furniture manufacturing. They are suitable for complex bonding requirements. Curing efficiency supports automated processes. Regulatory compliance strengthens adoption. Polyurethane remains a high-performance choice.

Polyvinyl acetate adhesives account for approximately 16% of the Wood Adhesives Market share. PVA adhesives are widely used in interior woodworking and furniture assembly. They are water-based, non-toxic, and easy to apply. The Wood Adhesives Market Analysis highlights strong use in DIY and small-scale manufacturing. PVA adhesives offer clean bonding and quick setting. They are preferred for indoor applications with low moisture exposure. Cost efficiency supports broad adoption. Availability in multiple grades enhances usability. PVA is compatible with manual and automated systems. Furniture workshops rely heavily on PVA adhesives. Environmental safety boosts demand. PVA remains a staple adhesive type.

The “Others” category represents approximately 5% of the Wood Adhesives Market share. This segment includes epoxy, hot-melt, and hybrid adhesive systems. These adhesives are used in specialized and niche applications. The Wood Adhesives Market Research Report highlights demand from high-performance projects. Hot-melt adhesives support fast production cycles. Epoxy adhesives offer exceptional strength for structural bonding. Hybrid systems combine flexibility and durability. Adoption is driven by customization needs. These adhesives serve industrial and specialty woodworking. Higher costs limit mass adoption. Performance reliability supports niche demand. Innovation continues in this segment. Others complement mainstream adhesive types.

By Technology

Solvent-based adhesives account for nearly 40% of the Wood Adhesives Market share. These adhesives provide strong bonding and fast setting times. They are used in demanding industrial applications. The Wood Adhesives Industry Analysis highlights continued relevance despite environmental concerns. Solvent-based systems perform well in high-stress environments. Moisture resistance supports exterior applications. Manufacturers rely on them for reliability. Regulatory pressure influences gradual substitution. Industrial buyers value performance consistency. Solvent-based adhesives support high-speed production. Cost efficiency supports adoption. Transition to alternatives is gradual. They remain critical in specific use cases.

Water-based adhesives dominate the Wood Adhesives Market with approximately 50% market share. These adhesives are favored due to low VOC emissions and regulatory compliance. They are widely used in furniture, cabinetry, and interior construction. The Wood Adhesives Market Outlook highlights strong sustainability alignment. Water-based systems are easy to handle and safe for workers. Adoption is driven by green building standards. These adhesives support consistent bonding performance. Compatibility with automated lines enhances usage. Drying efficiency continues to improve. Cost stability supports large-scale adoption. Furniture OEMs prefer water-based solutions. Demand continues to expand globally.

Other applications represent approximately 10% of the Wood Adhesives Market share. This segment includes hot-melt and reactive adhesive technologies. These adhesives support rapid curing and automation. The Wood Adhesives Market Insights highlight rising demand in prefabrication. Hot-melt adhesives reduce processing time. Reactive systems offer superior bonding strength. Adoption is growing in advanced manufacturing. These adhesives support high-speed assembly lines. Custom applications drive niche demand. Higher cost limits widespread use. Performance benefits outweigh limitations. Innovation supports gradual expansion. This segment enhances market diversity.

By Application

The flooring segment accounts for approximately 34% of the global Wood Adhesives Market share, making it one of the most significant end-use categories. Wood adhesives are extensively used in the installation and manufacturing of hardwood flooring, engineered wood flooring, laminate flooring, and parquet systems. Flooring applications require adhesives with high bonding strength, flexibility, and resistance to moisture and temperature fluctuations. The Wood Adhesives Market Analysis highlights strong demand from residential construction, commercial buildings, and renovation projects. Polyurethane and water-based adhesives are widely preferred in flooring due to their durability and low emissions. Rapid growth in modular housing and interior refurbishment further supports adhesive consumption. Flooring manufacturers prioritize adhesives that ensure long-term stability and noise reduction. Compatibility with underfloor heating systems is also a key requirement. The Wood Adhesives Market Outlook for flooring remains strong due to ongoing urbanization and real estate development.

Furniture represents the largest end-user segment in the Wood Adhesives Market, accounting for approximately 46% market share. Wood adhesives are critical in the production of residential, office, and commercial furniture, including cabinets, tables, chairs, wardrobes, and upholstered items. The Wood Adhesives Industry Analysis indicates that furniture manufacturers require adhesives offering fast curing, clean bonding, and high load-bearing capacity. Water-based, PVA, and polyurethane adhesives are widely used due to their safety, versatility, and compliance with emission regulations. Rising demand for ready-to-assemble and modular furniture has increased reliance on efficient adhesive solutions. Automation in furniture production further drives demand for adhesives compatible with high-speed manufacturing lines. Export-oriented furniture production significantly contributes to adhesive consumption. The Wood Adhesives Market Insights highlight consistent bulk procurement by furniture OEMs and contract manufacturers. Design innovation and customization trends continue to expand application scope.

The “Others” category accounts for approximately 20% of the global Wood Adhesives Market share, encompassing applications such as construction panels, doors and windows, packaging, interior fit-outs, and specialty woodworking. This segment includes usage in plywood, particleboard, MDF panels, staircases, and decorative wood components. The Wood Adhesives Market Research Report highlights steady demand from commercial construction, hospitality projects, and industrial woodworking. Adhesives used in this segment must deliver durability, moisture resistance, and compatibility with diverse substrates. Phenol-formaldehyde, MUF, and isocyanate adhesives are commonly used for structural and semi-structural applications. Growth in prefabricated buildings and interior architectural solutions supports demand. B2B buyers in this segment focus on performance reliability and compliance with building standards. The Wood Adhesives Market Growth in this category is supported by infrastructure expansion and interior modernization trends.

Wood Adhesives Market Regional Outlook

North America

North America Wood Adhesives Market Share, 2025 (%)

To get more information on the regional analysis of this market, Download Free sample

The North America Wood Adhesives Market accounts for approximately 22% of the global market share, driven by strong demand from construction, furniture manufacturing, and engineered wood industries. The United States dominates regional consumption due to widespread residential remodeling and commercial infrastructure upgrades. Increased use of plywood, MDF, and laminated wood panels supports consistent adhesive demand. Regulatory pressure from environmental agencies has accelerated adoption of low-VOC and water-based wood adhesives. Manufacturers focus on high-performance bonding solutions compatible with automated production lines. Growth in modular housing and prefabricated buildings further strengthens demand. The region benefits from advanced R&D capabilities and well-established supply chains. The Wood Adhesives Market Outlook indicates stable procurement from B2B buyers, including furniture OEMs and panel manufacturers. Technological innovation and sustainability initiatives remain core competitive drivers.

Europe

Europe holds nearly 25% of the global Wood Adhesives Market share, reflecting a mature and regulation-driven industry landscape. Strong demand arises from furniture exports, interior fittings, and engineered wood panel production. Environmental compliance plays a decisive role, with strict emission standards influencing adhesive formulation strategies. Bio-based and low-formaldehyde adhesives are increasingly preferred across the region. The Wood Adhesives Industry Analysis highlights consistent consumption from residential renovation and commercial fit-out projects. Manufacturers prioritize energy-efficient production and circular economy alignment. Europe’s strong woodworking tradition supports steady B2B demand from furniture clusters. Innovation in sustainable adhesive chemistry enhances long-term market resilience. Supply chain localization further strengthens regional competitiveness.

Germany Wood Adhesives Market

Germany contributes approximately 8% of the global Wood Adhesives Market share, making it one of the most influential markets in Europe. The country’s advanced furniture manufacturing and engineered wood industries drive high-volume adhesive consumption. Demand is supported by strong exports of premium furniture and construction materials. German manufacturers emphasize precision bonding, durability, and environmental compliance. Water-based and polyurethane adhesives see rising adoption due to stringent emission regulations. The Wood Adhesives Market Insights indicate steady procurement from industrial buyers seeking consistent quality. Automation and Industry 4.0 integration increase demand for fast-curing adhesive solutions. Sustainability certification remains a critical purchasing criterion across the German market.

United Kingdom Wood Adhesives Market

The United Kingdom accounts for nearly 5% of the global Wood Adhesives Market share, supported by renovation activity and modular construction projects. Demand is driven by residential refurbishment, cabinetry, and interior furniture manufacturing. The UK market favors easy-to-apply, compliant adhesive solutions suitable for small and mid-scale manufacturers. Increasing adoption of water-based adhesives reflects regulatory alignment and sustainability goals. The Wood Adhesives Market Analysis highlights steady consumption from panel producers and joinery businesses. Growth in prefabricated housing supports long-term adhesive demand. Supply reliability and performance consistency are key B2B purchasing factors. Innovation focuses on moisture-resistant and fast-setting formulations.

Asia-Pacific

Asia-Pacific dominates the global Wood Adhesives Market with approximately 42% market share, making it the largest regional contributor. Rapid urbanization, infrastructure development, and large-scale furniture manufacturing fuel strong demand. Countries across the region serve both domestic consumption and export-oriented production. Cost-effective manufacturing and high-volume panel production support adhesive consumption growth. The Wood Adhesives Market Research Report highlights rising adoption of water-based and polyurethane adhesives. Increasing middle-class housing demand further strengthens the market outlook. Local manufacturers focus on scalable production and cost optimization. B2B buyers prioritize bulk supply, consistency, and competitive pricing. The region remains central to global supply chains.

Japan Wood Adhesives Market

Japan represents approximately 6% of the global Wood Adhesives Market share, characterized by precision manufacturing and high-quality standards. Demand is driven by engineered wood products, furniture, and interior architectural applications. Japanese manufacturers emphasize durability, clean bonding, and performance reliability. Adhesive formulations must meet strict quality and safety regulations. The Wood Adhesives Market Insights indicate strong preference for advanced polymer-based and water-based solutions. Innovation focuses on improved curing efficiency and thermal resistance. Automation and lean manufacturing increase demand for consistent adhesive performance. Sustainability and waste reduction initiatives further shape product development strategies.

China Wood Adhesives Market

China accounts for around 20% of the global Wood Adhesives Market share, making it the single largest national market. Massive furniture manufacturing capacity and panel production drive exceptional adhesive demand. The country serves as a global export hub for wood-based products. Domestic construction and housing projects further support consumption. The Wood Adhesives Market Size in China benefits from economies of scale and localized supply chains. Increasing regulatory oversight promotes gradual transition toward low-emission adhesives. B2B buyers prioritize cost efficiency, supply stability, and production scalability. Continuous capacity expansion strengthens China’s global market influence.

Rest of the World

Rest of the World contributes approximately 11% of the global Wood Adhesives Market share, supported by construction and interior development projects. Demand arises from residential housing, commercial buildings, and hospitality infrastructure. Growth in modern furniture adoption boosts adhesive consumption. The region increasingly imports engineered wood products, supporting adhesive application demand. The Wood Adhesives Market Outlook highlights rising interest in durable and moisture-resistant formulations. Urban expansion and real estate development remain key demand drivers. B2B buyers focus on performance reliability under varying climate conditions. Market penetration continues to improve through distributor-led expansion strategies.

List of Top Wood Adhesives Companies

- Pidilite Industries Limited

- Asian Paints

- Sika AG

- H.B. Fuller

- Henkel AG & Co. KGaA

- Bostik S.A.

- Follmann GmbH & Co. KG

- The 3M Company

- Dow

- Others

Top Two Companies by Market Share

- Henkel AG & Co. KGaA – 14% Market Share

- Pidilite Industries Limited – 11% Market Share

Investment Analysis and Opportunities

Investment in the Wood Adhesives Market is driven by innovation, sustainability, and capacity expansion. Manufacturers are allocating capital toward developing low-emission and bio-based adhesive technologies to meet regulatory and customer requirements. The Wood Adhesives Market Opportunities include modernization of production facilities and adoption of digital quality control systems. Strategic partnerships with furniture and construction companies enhance long-term supply agreements. Emerging markets offer attractive investment potential due to expanding construction activity and industrialization. Private equity interest is increasing as companies seek scale and technology differentiation.

New Product Development

New product development within the Wood Adhesives Market focuses on performance enhancement and environmental compliance. Manufacturers are launching fast-curing adhesives compatible with automated application systems. Innovations include moisture-resistant water-based formulations and hybrid polymer adhesives offering superior bonding strength. The Wood Adhesives Industry Analysis highlights emphasis on reduced emissions and improved shelf life. Custom formulations for engineered wood products and prefabrication applications are gaining traction. Continuous R&D investment supports competitive differentiation and long-term market positioning.

Five Recent Developments (2023–2025)

- Introduction of bio-based wood adhesive formulations by leading manufacturers

- Expansion of production capacity in Asia-Pacific to meet furniture export demand

- Launch of low-formaldehyde adhesive solutions for engineered wood

- Strategic acquisitions to strengthen regional distribution networks

- Development of high-speed curing adhesives for automated manufacturing

Report Coverage of Wood Adhesives Market

The Wood Adhesives Market Report provides comprehensive analysis across product types, applications, and regional markets. Coverage includes competitive landscape assessment, technological advancements, regulatory impact evaluation, and demand drivers. The Wood Adhesives Market Research Report examines market share distribution and strategic initiatives by key players.

Request for Customization to gain extensive market insights.

It offers insights into investment trends, innovation pipelines, and emerging opportunities. The report supports decision-making for manufacturers, suppliers, investors, and B2B stakeholders seeking detailed Wood Adhesives Market Insights and industry positioning strategies.

Segmentation

|

By Product |

By Technology |

By Application |

By Geography |

|

|

|

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 8.39 billion in 2025 and is projected to reach USD 17.79 billion by 2034.

The market is expected to exhibit a CAGR of 8.72% during the forecast period of 2026-2034.

The Furniture segment led the market with around 46% share due to strong demand for residential, office, and commercial furniture manufacturing.

Key players include Pidilite Industries Limited, Asian Paints, Sika AG, H.B. Fuller, Henkel AG & Co. KGaA, and Bostik S.A.

Major trends include rising adoption of bio-based and low-emission adhesives and fast-curing formulations; Asia-Pacific leads due to strong furniture manufacturing demand.

- 2021-2034

- 2025

- 2021-2024

- 128

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us