Attack Helicopter Market Size, Share & Industry Analysis, By Weight Class (Light, Medium, and Heavy), By Component (Airframe, Engines, Avionics, Weapon Systems, Countermeasure Systems, and Sensors), By Engine Configuration (Single Engine and Twin Engine), By Mission Type (Close Air Support (CAS), Anti-Tank, Escort, Intelligence, Surveillance, and Reconnaissance (ISR), Search and Rescue (SAR), Counter-UAS, and Others), By End User (Army Aviation, Naval Aviation, Air Force, and Special Operations Forces), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

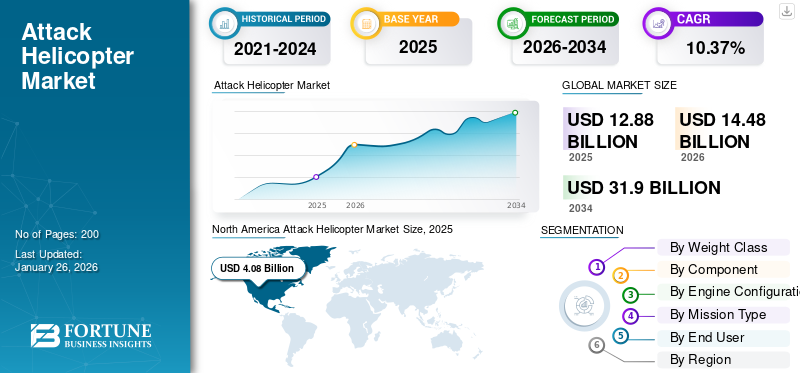

The global attack helicopter market size was valued at USD 12.88 billion in 2025 and is projected to grow from USD 14.48 billion in 2026 to USD 31.90 billion by 2034, exhibiting a CAGR of 10.37% during the forecast period. North America dominated the global market with a share of 31.66% in 2025.

Attack helicopters are specialized aircraft designed for offensive ground operations. They are heavily armed and equipped to engage enemy infantry, vehicles, and fortifications. These helicopters provide direct air support to ground troops and are capable of countering armored units. Such helicopters are equipped with various weapon systems such as machine guns, rockets, missiles, and even bombs. These helicopters are designed to deliver effective fire support, survive heavy attacks, and cause major damage to enemy vehicles.

Key players in the market, such as Airbus, Boeing, Bell Helicopter, and others, are focused on the development of helicopters to meet evolving military requirements. For instance, in December 2024, Airbus Helicopters delivered the first H145M light helicopter to Germany’s military as part of a deal for up to 82 units to replace older helicopters. The H145M will be used for training, reconnaissance, special operations, and light attack missions. Manufacturers are also designing helicopters that meet the quality standards, demanded by military customers all over the globe. This involves assembling robust airframes, installing sophisticated weapon systems, and integrating electronic technologies. For instance, Boeing is advancing the Apache helicopter through ongoing modernization efforts, including integrating “Launched Effects” to boost sensing and lethality. The company is also conducting flight tests of the latest Version 6.5, which features enhanced software and improved pilot interfaces, aimed at providing a dominant, adaptable platform.

Download Free sample to learn more about this report.

Impact of the Russia-Ukraine War

Increased Demand for Modern Helicopters During the War Has Driven the Market Development

The Russia-Ukraine war has significantly impacted the market as it has increased the demand for modernized and advanced helicopters across the globe. The ongoing conflict has highlighted the importance of aerial firepower and close air support in modern warfare. This situation has encouraged numerous countries to accelerate their procurement and modernization programs. For instance, in May 2025, Ukraine collaborated with Sweden in an attempt to strengthen efforts aimed at modernizing its air force. Such joint modernization initiatives are expected to increase future aircraft and helicopter procurement, thereby driving the attack helicopter market growth.

Several nations are investing in advanced helicopters to enhance their defense capabilities and deter potential threats. The war has also emphasized the need for helicopters with improved survivability, lethality, and multi-mission flexibility. This has led to widespread upgrades of existing fleets and increased interest in new-generation models. Countries are increasingly seeking helicopters equipped with advanced targeting systems, integrated weaponry, and enhanced communication systems to ensure operational effectiveness in complex combat environments.

Attack Helicopter Market Trends

Integration of Advanced Weaponry and Targeting Systems to Emerge as New Trend

The increasing integration of advanced weaponry and targeting systems in helicopters is shaping the future of aerial combat. Modern helicopters are now equipped with sophisticated sensors, radar systems, and precision-guided munitions. These enhancements allow them to perform multiple roles, such as close air support, anti-armor, and reconnaissance, with greater effectiveness. Improved targeting systems enable pilots to identify and engage targets with higher accuracy, even in complex and contested environments. These advancements also include the integration of electronic countermeasures and stealth features, which improve survivability against modern threats. As warfare becomes more technologically advanced, these capabilities are vital for maintaining tactical superiority. This trend supports the development of versatile, resilient, and lethal helicopters, reflecting a broader effort to adapt to rapidly evolving battlefield conditions.

Download Free sample to learn more about this report.

Market Dynamics

Market Driver

Increase in Defense Expenditure and Rising Geopolitical Conflicts and Border Tension to Propel Market Growth

Growing defense budgets and escalating geopolitical tensions are pushing countries to invest more in their military capabilities, particularly in helicopters. As nations face increasing threats from regional conflicts, terrorism, and rival states, they recognize the need to modernize their armed forces to ensure national security. For instance, according to SIPRI, in 2024, global military spending reached USD 2.718 trillion, marking a 9.4% increase from 2023 and the largest rise since the Cold War era. This surge reflects heightened international tensions and shifting defense priorities, which are expected to promote the procurement of helicopters as part of broader efforts to maintain national security. As a result, the market is projected to experience significant growth in line with the defense budget.

Countries are investing heavily in modernizing their armed forces to enhance their capabilities and maintain a competitive edge. Particularly, countries are prioritizing the modernization of combat helicopters with the help of various programs to enhance their military capabilities. For instance, in June 2025, the French Army in Djibouti started replacing aging SA330 Puma helicopters with modern NH90 Caïman TTH aircraft to enhance tactical mobility and combat readiness amid growing regional strategic competition. Such developments are driving continuous investment and innovation in helicopter technologies, positioning them as vital assets in modern defense strategies.

Market Restraint

High Procurement and Maintenance Costs to Hinder Market Growth

High procurement and maintenance costs are significant barriers for many countries seeking to modernize their armed forces. Purchasing advanced military equipment, such as new aircraft, ships, or weapon systems, often requires substantial financial resources that may be beyond the reach of some nations. These costs include the initial purchase price and ongoing expenses for upkeep, repairs, and spare parts. Maintenance costs can be particularly high, especially for complex systems that require specialized personnel and parts. As a result, some countries delay or scale back their modernization programs to manage budgets effectively. Therefore, all these factors are expected to hamper the market in certain regions.

Market Challenges

Regulatory & Political Challenges Pose a Significant Challenge for the Market Development

The market for attack helicopters faces unique regulatory and political challenges that affect sales and deployment. One major issue is the strict export controls and licensing regulations imposed by governments to safeguard military technologies. Countries often restrict the transfer of helicopter technology to prevent proliferation, which can limit international sales opportunities for manufacturers.

Market Opportunity

Technological Advancements in the Attack Helicopters Design to Present Growth Opportunities

Technological advancements and continuous upgrades present significant opportunities for growth and competitiveness in the market. As military requirements evolve, the integration of advanced technologies can enhance the effectiveness, survivability, and versatility of helicopters. For instance, in May 2025, Elbit Systems secured a USD 55 million contract to upgrade the Israeli Air Force’s Black Hawk and Apache helicopters with advanced protection systems. The upgrades will include cutting-edge DIRCM technology to enhance survivability against emerging threats.

Moreover, there is a rise in the trend toward incorporating advanced weapons systems, such as precision-guided munitions, missile technology, and anti-aircraft systems into helicopters. This allows in engaging of a wider range of targets more effectively. Therefore, technological advancements and ongoing upgrades allow manufacturers to develop more capable, flexible, and cost-effective helicopter systems, which are expected to present significant opportunities for the growth of the market.

Segmentation Analysis

By Weight Class

Medium Segment Held the Largest Market Share Due to its Suitability in Various Operational Roles

On the basis of weight class, the market is classified into light, medium, and heavy.

The medium segment is projected to dominate the market with a share of 45.62% in 2026. This growth is driven by the balance it offers in terms of firepower, maneuverability, and cost-efficiency, making it suitable for a variety of operational roles. Countries seeking to modernize their armed forces prefer medium-weight helicopters such as the AH-64 Apache or Eurocopter Tiger as they can carry advanced weaponry and sensors while being more affordable and easier to maintain than heavy attack helicopters.

The light segment holds the second-largest share in the market. Lightweight helicopters are becoming popular across the globe due to their cost-effectiveness and high maneuverability. Lightweight helicopters are less expensive to procure and operate, which makes them an affordable option. Moreover, these helicopters are extensively used in counterinsurgency missions, border patrol, and anti-terror operations. Such advantages are expected to drive demand for lightweight helicopters during the forecast period.

By Component

Airframe Segment Holds the Largest Share Due to Advancement in Lightweight Materials

On the basis of component, the market is classified into airframe, engines, avionics, weapon systems, countermeasure systems, and sensors.

Airframe segment is projected to dominate the market with a share of 25.33% in 2026. The segment is growing due to the adoption of lightweight composites and advanced alloys in airframe construction, which reduces overall helicopter weight. This led to the enhancement of payload capacity, maneuverability, and fuel efficiency. For instance, in April 2024, Netherlands modified the Apache AH-64E helicopters with an upgraded fuselage. The modifications include the use of composite materials to improve the durability and resistance of helicopter design.

The engines segment is the second-largest segment in the market. The segment is growing significantly owing to the need for more powerful, fuel-efficient, reliable, and maintainable engines. For instance, in 2023, the Chinese WZ-10 attack helicopter received a new engine that will boost its climb rate by 20% and acceleration by 10%, enhancing its overall performance. The upgrade addressed previous power limitations and improved the operational capabilities in complex combat environments. Moreover, the push toward more reliable, efficient, and lower-maintenance engines is expected to drive the growth of the segment.

To know how our report can help streamline your business, Speak to Analyst

By Engine Configuration

Twin Engine Segment Holds the Largest Market Share Due to its Enhanced Safety and Improved Operational Capability

On the basis of engine configuration, the market is classified into single engine and twin engine.

The twin engine segment is projected to dominate the market with a share of 68.97% in 2026 and is expected to grow fastest during the forecast period. Twin-engine helicopters offer increased safety margins, especially in challenging operational environments. Their ability to continue flight on a single engine in the event of engine failure reduces the risk of accidents, making them more attractive for military and critical missions. For instance, in 2024, Nigeria announced its plans to purchase four twin-engine Light Combat Helicopters (LCH) from India, with a soft credit arrangement reportedly in place for the country's first export order, according to sources cited by Financial Express. The LCH, an advanced variant of the Dhruv helicopter, is designed for high-altitude and extreme weather operations and is armed with missiles, guns, and advanced electronic warfare systems.

By Mission Type

Close Air Support (CAS) Segment Leads Due to Emergence of Multi-Role Helicopters

On the basis of mission type, the market is classified into Close Air Support (CAS), Anti-Tank, Escort, Intelligence, Surveillance, and Reconnaissance (ISR), Search and Rescue (SAR), Counter-UAS, and others.

The Close Air Support (CAS) segment is projected to dominate the market with a share of 22.87% in 2026 and is expected to grow with the highest CAGR during the study period, due to the increasing need for precise and effective battlefield assistance. As modern militaries confront challenges such as counterinsurgency, urban warfare, and asymmetric threats, the demand for specialized aircraft capable of supporting ground forces has risen. Advances in avionics, weapon systems, and targeting accuracy have made CAS platforms more effective and adaptable to complex combat environments. Furthermore, the emergence of multi-role helicopters that can perform CAS missions alongside other tactical roles has enhanced their operational value. Countries are investing in modernizing their armed forces with advanced CAS-capable helicopters to improve battlefield responsiveness and survivability.

By End User

Army Aviation Segment Holds the Largest Market Share Due to the Increasing Demand for Combat Helicopters in Battlefield & Tactical Support

On the basis of end user, the market is classified into army aviation, naval aviation, air force, and special operations forces.

The army aviation range segment holds the largest share in the market, driven by the increasing need for rapid deployment, battlefield mobility, and tactical support. Modern armies are focusing on enhancing their operational flexibility through versatile rotary-wing platforms that can perform a wide range of missions, including reconnaissance, attack, troop transport, and logistics support. Moreover, many countries are investing in modernizing their armed forces to counter emerging threats and maintain strategic superiority, which fuels demand for advanced army aviation assets.

The air force segment is expected to grow significantly due to increasing defense spending across various countries in response to geopolitical tensions and evolving security threats. This trend has led to investments in modernizing and expanding military capabilities, including helicopters. The rise of asymmetric warfare and counterinsurgency operations has highlighted the need for agile and effective air support. Attack helicopters provide close air support, reconnaissance, and strike capabilities, making them essential for modern military operations.

Attack Helicopter Market Regional Outlook

On the basis of region, the market is studied across North America, Europe, Asia Pacific, Middle East, and the Rest of the World.

North America

North America Attack Helicopter Market Size, 2025 (USD Billion) To get more information on the regional analysis of this market, Download Free sample

The North America market generated USD 4.08 billion in 2025, representing 31.66% of the global market landscape, and is expected to reach USD 4.62 billion in 2026. North America currently holds the largest market share in the attack helicopter market due to the extensive military modernization efforts and high defense spending. The U.S. Army is actively upgrading its attack helicopter fleet, including the development and procurement of advanced platforms such as the AH-64E Apache Guardian and future programs such as the Future Attack Reconnaissance Aircraft (FARA). For instance, in 2023, Boeing secured a contract to produce 184 AH-64E Apache helicopters for the U.S. Army and international military customers.

This order reflects ongoing modernization efforts and demand for advanced helicopters in North America. These initiatives are driven by the need to maintain technological superiority and operational readiness in complex combat environments, which is expected to drive the growth of the market in the region. The U.S. government’s focus on modernizing its armed forces, coupled with ongoing procurement of new attack helicopters, propels country’s market growth. Additionally, the U.S. defense industry is a global leader in helicopter technology, investing heavily in research & development to improve weapon systems, avionics, and survivability features, which further fuels market growth. The U.S. market is projected to reach USD 2.99 billion by 2026.

Canada also contributes to regional growth through its procurement and upgrade programs for attack and reconnaissance helicopters, supporting its defense strategy and operational requirements. For instance, in May 2025, Canada announced plans to acquire new helicopters valued at over USD 13.18 billion to support future F-35 deployments and to replace the aging CH-146 Griffon fleet in the Arctic. These new helicopters will enhance Canada's capability to operate in extreme polar conditions and respond to potential security incidents.

Europe

Europe is witnessing steady growth in the market owing to various reasons such as increasing military spending and renewed focus on military readiness across the region. Countries such as the U.K., France, and Germany are investing in modernizing their military fleets with advanced combat helicopters. For instance, in December 2023, Germany ordered 62 Airbus H145M helicopters, with some equipped for anti-tank missions using Spike LR missiles, reflecting lessons from Ukraine's conflict. The deal worth USD 2.40 billion includes 57 helicopters for the Army and 5 for special forces, with deliveries starting in 2024. The rise in regional security threats and geopolitical tensions has boosted demand for versatile rotorcraft for surveillance and rapid deployment. The UK market is projected to reach USD 0.77 billion by 2026, and the Germany market is projected to reach USD 0.72 billion by 2026. Europe contributed 25.23% to the global market in 2025, with a valuation of USD 3.25 billion, and is projected to reach USD 3.66 billion in 2026.

Asia Pacific

The Asia Pacific region is experiencing robust growth, driven by an increase in geopolitical tension across the globe and a rise in defense modernization efforts. Countries such as China, India, and Australia are investing heavily in advanced helicopters to bolster their military capabilities. For instance, in March 2025, India's government approved a USD 723.08 million deal to buy 156 indigenous Light Combat Helicopters (LCH) from HAL, marking the largest order for the company. These helicopters will be deployed along India’s borders with China and Pakistan, with production taking place in Karnataka. The rising threat perception from neighboring countries encourages regional militaries to expand their attack helicopter fleets. Governments across the region are allocating substantial budgets for indigenous production and procurement of helicopters, which is expected to propel market growth. The Japan market is projected to reach USD 0.44 billion by 2026, the China market is projected to reach USD 0.55 billion by 2026, and the India market is projected to reach USD 0.47 billion by 2026.

Middle East

The Middle East market is dominated by the AH‑64E Apache, with major buyers including the UAE, Qatar, Kuwait, Saudi Arabia, and Israel upgrading or procuring E-models. Russia’s Ka‑52 and other platforms appear in Egypt and Iraq, but face export/support constraints. Growing mission demands—especially counter-UAS, networked weapons and local integration—are driving not only new aircraft buys but also training, sustainment, and upgrade contracts. In 2025, Middle East & Africa held 14.73% of the global market, reaching a valuation of USD 1.9 billion, and is projected to grow to USD 2.12 billion in 2026.

Rest of the World

The market in the Rest of the World, including Latin America and Africa, is expanding steadily due to increasing defense spending and modernization efforts. Countries in the Latin America and Africa are investing in advanced helicopters to counter regional threats and enhance their aerial combat capabilities. In Africa, several nations are working to upgrade their defense systems, often through the import of helicopters, to address ongoing security challenges and border security issues. In 2025, the Rest of the World market stood at USD 1.44 billion, representing 11.18% of global demand, and is projected to grow to USD 1.59 billion in 2026.

Competitive Landscape

Key Market Players

Key Players Focus on Investments to Meet Diverse Industry Needs

The market is highly competitive, with several major global defense manufacturers vying for attack helicopter market share. Leading companies are focused on developing advanced, multi-mission capable helicopters with cutting-edge technology, such as improved avionics, stealth features, and weapon systems. Competition in the market is driven by innovation, cost-effectiveness, and the ability to meet diverse military needs across different regions. Strategic alliances, regional defense contracts, and government procurement policies significantly influence market dynamics. Many manufacturers are investing in R&D to develop next-generation attack helicopters that incorporate modern warfare capabilities such as network-centric operations and enhanced survivability.

LIST OF KEY ATTACK HELICOPTER COMPANIES PROFILED

- Lockheed Martin Corporation (U.S.)

- Boeing (U.S.)

- Airbus Helicopters (France)

- Rostec (Russia)

- Leonardo S.p.A. (Italy)

- Hindustan Aeronautics Limited (India)

- China Aerospace Science and Industry Corporation (CASIC) (China)

- KAI (Korea Aerospace Industries) (South Korea)

- TAI (Turkish Aerospace Industries) (Turkey)

- Denel Aeonautics (South Africa)

KEY INDUSTRY DEVELOPMENTS

- May 2025- Boeing’s Global Services division received a USD 101.6 million contract to provide maintenance, spare parts, and technical support for the U.S. Army’s AH-64 Apache helicopters, ensuring their operational readiness. The support includes key components such as fuselages, rotor systems, avionics, and structural parts.

- March 2025- Morocco received its first six AH-64E Apache helicopters from the U.S. as part of a 2019 contract for 36 units, with deliveries ongoing through 2024. The procurement program, initiated in 2010 and approved by the U.S. in 2019, aims to modernize Morocco's military capabilities.

- January 2025- Babcock and Airbus Helicopters secured a 12-year contract to support France’s EC145 helicopter fleet used by the Gendarmerie Nationale and Civil Security, including phased replacement with Airbus H145 helicopters.

- October 2024- The first Boeing AH-6i helicopter for Thailand completed its first flight in Arizona, marking the start of a USD 103.8 million deal to replace its aging Cobra fleet. The helicopters would enhance Thailand’s reconnaissance and attack capabilities, with deliveries expected by May 2025.

- March 2024- Bell Textron was awarded a USD 455 million contract to produce and deliver 12 AH-1Z Viper helicopters to Nigeria, with work expected to finish by July 2028. The deal includes engineering, logistics, and support, following U.S. approval in 2022 amid previous concerns over human rights.

REPORT COVERAGE

The report provides a detailed analysis of the sector and focuses on important aspects such as key players, technology, application, propulsion depending on various regions. Moreover, the research report offers deep insights into the attack helicopters market trends, competitive landscape, market competition, and market status and highlights key industry developments. Additionally, it encompasses several direct and indirect factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) |

|

Growth Rate |

CAGR of 10.37% from 2026 to 2034 |

|

Segmentation |

By Weight Class · Light · Medium · Heavy |

|

By Component · Airframe · Engines · Avionics · Weapon Systems · Countermeasure Systems · Sensors |

|

|

By Engine Configuration · Single Engine · Twin Engine |

|

|

By Mission Type · Close Air Support (CAS) · Anti-Tank · Escort · Intelligence, Surveillance, and Reconnaissance (ISR) · Search and Rescue (SAR) · Counter-UAS · Others |

|

|

By End User · Army Aviation · Naval Aviation · Air Force · Special Operations Forces |

|

|

By Region

· U.S. (By End User) · Canada (By End User)

· U.K. (By End User) · Germany (By End User) · France (By End User) · Russia (By End User) · Italy (By End User) · Rest of Europe (By End User)

· China (By End User) · India (By End User) · South Korea (By End User) · Australia (By End User) · South East Asia (By End User)

· Saudi Arabia (By End User) · UAE (By End User) · Turkey (By End User) · Israel (By End User) · Rest of Middle East (By End User)

· Africa (By Type) · Latin America (By End User) |

Frequently Asked Questions

Fortune Business Insights says that the global market stood at USD 14.48 billion in 2026 and is projected to reach USD 31.90 billion by 2034.

Registering a CAGR of 10.37%, the market will exhibit significant growth during the forecast period.

By weight class, the medium segment led the market.

Airbus, Boeing, and Bell are some of the leading players in the market.

North America dominates the market in terms of share.

North America dominated the global market with a share of 31.66% in 2025.

The key factors driving the market are an increase in defense expenditure and rising geopolitical conflicts and border tension.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us