Electronic Warfare (EW) Market Size, Share & Russia-Ukraine War Impact Analysis, By End User (Landforce, Air, and Naval), By Platform (Aircraft, Weapon, Naval Ship, Vehicle, and Others), By Type (Electronic Support, Electronic Protection, Electronic Attack, and Others), By Technology (Antennas, Anti-Jam Electronic Protection System, Directed Energy Weapon, IR Missile Warning System, Optical Attack Solutions, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

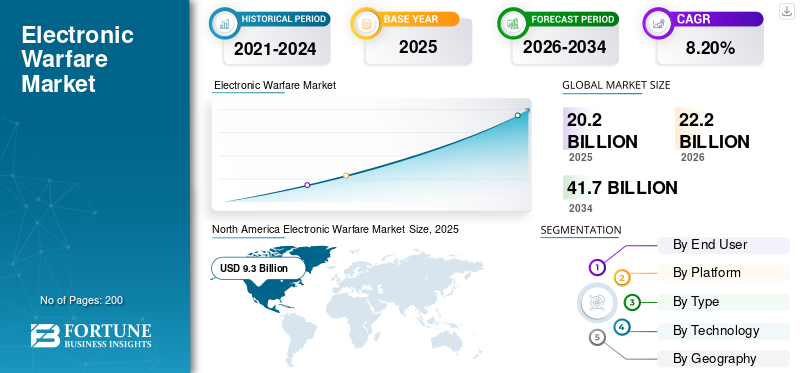

The global electronic warfare (EW) market size was valued at USD 20.20 billion in 2025 and is projected to grow from USD 22.20 billion in 2026 to USD 41.70 billion by 2034, exhibiting a CAGR of 8.20% over the forecast period. North America dominated the electronic warfare market with a market share of 46.10% in 2025. Moreover, the electronic warfare market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 11,411.08 million by 2032, driven by rising aircraft refurbishment drive market size Growth by extending lifespan of older aircraft.

Electronic Warfare (EW) refers to the use of electromagnetic spectrum, such as radio frequency and signals. It involves activities such as jamming, intercepting, and deciphering signals. It provides situational awareness to a country and its allies and helps them take defensive measures, get diplomatic insights, and prepare for offensive situations at every level before conflicts arise. The rise in geopolitical tensions and regional conflicts necessitated the adoption of advanced warfare methods.

Advanced warfare techniques can also intercept, identify, and decode adversaries' data. They can even project directed energy to disrupt enemy operations. This factor changes the battlespace, offering the capacity to reinforce mission success and survivability at every stage, prevent armed conflicts before they begin, or reduce the impact and scope of conflicts underway. The rise in the use of technology in warfare has positively driven the electronic warfare market growth.

Download Free sample to learn more about this report.

RUSSIA-UKRAINE WAR IMPACT

Russia-Ukraine War has a Positive Impact on the Market due to Increasing Tactical Combat Operations

The Russian government invested heavily in EW systems, which were used to jam GPS signals, detect smart bombs supplied by Western nations, and others. The war has showcased the evolving role of EW in modern conflicts and highlighted the strategies and technologies employed by both sides. A few of the Russian deployed electronic warfare systems were 1RL257 Krasukha-4, 1L269 Krasukha-2, RB-341V Leer-3, RH-330Zh Zhitel, Murmansk-BN, R-934B, and SPN-2, 3, 4. In addition, Russia's use of electronic warfare has severely affected Ukraine's ability to respond by jamming Ukraine's missile defense systems and allowing Russian forces to launch an aerial attack. In March 2022, 18 EW and radar systems of the Russian army were destroyed by the Ukrainian force, which preceded the Kyiv and Kharkiv counter-offensive operations.

Moreover, the Russia-Ukraine war was closely linked with cyber operations. The conflict has seen an increase in cyberattacks such as Distributed Denial-of-Service (DDoS) attacks and malware campaigns. Thus, the conflict has driven both countries to invest in the modernization of their EW capabilities. Such developments catalyze the applications of EW in modern-day conflicts.

Electronic Warfare (EW) Market Key Takeaways

- 2025 Market Size: USD 20.20 billion

- 2026 Market Size: USD 22.20 billion

- 2034 Forecast Market Size: USD 41.70 billion

- CAGR: 8.20% from 2026–2034

- North America dominated the electronic warfare market with a 46.10% share in 2025.

- The naval segment is projected to account for the largest market share of 44.14% in 2026.

- The naval ships segment is projected to hold a 39.05% share in 2026.

North America

North America held a 46.10% market share in 2025, valued at USD 9.3 billion, and is projected to reach USD 10.3 billion in 2026.

Europe

Europe market was valued at USD 3.4 billion in 2025, representing 16.90% of global revenue, and is estimated to reach USD 3.8 billion in 2026.

Asia Pacific

Asia Pacific accounted for 21.40% of the global market in 2025, valued at USD 4 billion, and is projected to reach USD 5 billion in 2026.

U.S.

U.S. The electronic warfare market is projected to reach USD 5.88 billion by 2026.

Japan

Japan The electronic warfare market is projected to reach USD 0.41 billion by 2026.

Read More

Electronic Warfare (EW) Market Trends

Main Trends are Growth of Digital Transformation and Networked Warfare

To increase efficiency, agility, and effectiveness, the use of a variety of cutting-edge technologies in various areas of operation is referred to as 'digital transformation.' Modern electronic warfare systems are becoming more digitized and integrated with broader capabilities of the NetworkCentric Warfare or NCW. This enables real-time data sharing and enhanced situational awareness & coordination in the face of threats.

In November 2023, Airbus announced plans to equip 15 German Eurofighters with electronic warfare equipment and the "AARGM" antiradar missile system of the U.S.-based company Northrop Grumman. They will be equipped with a transmitter location and a self-protection system from SAAB. By 2030, the Eurofighter EK will be NATO-certified and replace the Tornado in the SEAD role in the fight against enemy air defense.

To achieve a decisive advantage on the battlefield, NCW stresses the importance of networking and information exchange between different military units and platforms. Information sharing, decentralised command & control, improved targeting, and interoperability are the key components of the NCW in EW.

In July 2023, Raytheon Technologies signed a contract with the naval air systems command to support Next-Generation Jammer (NGJ) Mid-Band (MB). The contract was worth USD 26.6 million and included the design, development, and testing of NGJ-MB software.

- North America witnessed electronic warfare (EW) market growth from USD 6.90 Billion in 2022 to USD 7.60 Billion in 2023.

Download Free sample to learn more about this report.

Electronic Warfare (EW) Market Growth Factors

Advancements in Technology for Development of More Sophisticated EW Systems to Drive Market Growth

Technology developments will sdrive the growth of the electronic warfare market. These advances have led to the development of more sophisticated and capable electronic warfare systems, which offers greater accuracy, range, and flexibility. Furthermore, high-sensitivity sensors capable of identifying and classifying a wide range of electrical signals, such as radar emissions, communication transmission or others are being incorporated into today's Electronic Countermeasure Systems (ECS). The sensors are becoming smaller, more energy efficient, and able to operate across several frequency ranges.

In addition, EW has improved as a result of advances in digital signal processing and machine learning algorithms. These technologies enable rapid identification and discrimination of threats from various sources, allowing for accurate analysis of complicated signals. In June 2023, CACI signed a USD 1.2 billion indefinite-quantity contract with the U.S. Navy. CACI will develop and deploy the next generation of shipborne weapon systems for intelligence, surveillance, and information operations in cooperation with the U.S. Navy.

Increasing Use of Warfare Equipment Due to Deployment of Cyber Operations to Propel Market Growth

A networked information communication system using an electromagnetic spectrum or a wired connection is an important feature of cyberspace. These systems are characterized by a number of electronic information management processes, e.g. data gathering, processing, storage, and communication. Cyberspace plays an important role in national security across domains, such as land, sea, air, and space. A common operating environment called the cyber electromagnetic domain, is created by cyberspace and the electromagnetic spectrum.

Moreover, adversaries are increasingly integrating cyber capabilities with traditional EW tactics. This has increased the demand for a comprehensive electronic warfare system that can detect, analyze, and respond to both electronic and cyber threats. In March 2023, Lockheed Martin was awarded a contract worth more than USD 33 million to provide the U.S. military with a tactical vehicle capable of intelligence gathering, cyber-attacks, and combat electronic warfare capabilities.

RESTRAINING FACTORS

Complexity Related to the Integration of EW Systems is a Major Restraining Factor

Electronic countermeasure systems are intricate and require seamless integration with various platforms, sensors, and communication networks. Modern military operations often involve multiple domains such as air, land, sea, cyberspace, and others. EW systems must be integrated across these domains for comprehensive situational awareness and effective response. Achieving seamless integration is a challenge that may hamper the market growth.

Furthermore, different military platforms have different power limitations and operational requirements. Designing an EW system that can adapt to such diverse platforms imposes a major challenge on tier 1 suppliers. Moreover, the presence of multiple singles in a close environment can interfere with the systems, which can affect the accuracy and reliability of EW systems.

Electronic Warfare (EW) Market Segmentation Analysis

By End User Analysis

Naval Segment Dominated the Market owing to Technological Advancements.

By end user, the market is segmented into landforce, air, and naval. The naval segment dominated the market and is estimated to be the fastest-growing segment during the forecast period. The growth of the segment is attributed to several factors, such as advancements in naval EW technologies and the growing importance of dominating the sea by various countries. The need for better electronic warfare capabilities to protect naval assets in maritime operations is another factor driving the segment growth. The naval segment is projected to dominate the market with a share of 44.14% in 2026.

The landforce segment is anticipated to witness significant growth during the forecast period. The growth of the segment is due to rising investments in countermeasure technologies, situational awareness, communication systems, and others. Various other factors include increased dependence on technology for Intelligence, Surveillance, and Reconnaissance (ISR) activities on the battlefield.

By Platform Analysis

Naval Ship Segment Dominated the Market Owing to Evolving Threats in Sea Operations

Based on the platform, the market is segmented into aircraft, weapons, naval ships, vehicles, and others. The naval ships segment is projected to dominate the market with a share of 39.05% in 2026 and is expected to be the fastest-growing segment during the forecast period due to evolving threats, the need for information dominance, and protection against missiles, drones, and others.

- The weapons segment is expected to hold a 15.73% share in 2023.

The vehicle segment is estimated to witness significant growth during the forecast period. The segmental growth is attributed to increased applications of tactical EW systems to have protection against guided weapons and unmanned systems.

To know how our report can help streamline your business, Speak to Analyst

By Type Analysis

Usage of Electronic Attacks for Destroying Targets to Drive Segment Expansion

By type, the market is segmented into electronic support, electronic protection, electronic attack, and others. The electronic attack segment is anticipated to dominate the market and is projected to be the fastest-growing segment during the forecast period. Electronic attacks are used to disrupt, destroy, or deceive targets. With technological advancements and increased reliance on electronic systems for tactical operations, the segment is anticipated to grow at the fastest rate during the forecast period. The others segment is expected to lead the market, contributing 99.91% globally in 2026.

The electronic protection segment is estimated to witness significant growth during the forecast period. Electronic protection refers to the protection of a nation’s assets, personnel, and equipment from the threat of an Electronic Attack (EA) by enemy forces that would neutralize or disable the nation’s combat capabilities. Owing to the rise in tensions between countries, the segment is anticipated to witness substantial growth during the study period.

By Technology Analysis

Linkage of IR Missile Warning System with EW System for Enhanced Countermeasure Capabilities to Impel Segment Growth

Based on technology, the market is segmented into antennas, anti-jam electronic protection systems, directed energy weapons, IR missile warning systems, optical attack solutions, and others. The IR missile warning system segment is anticipated to dominate the market and is projected to be the fastest-growing segment during the forecast period. The IR missile warning system supports various operations for Electronic Support Measures (ESM). In some cases, the IR missile warning system is linked with the EW system to enhance countermeasure capabilities. The IR missile warning system segment will account for 33.65% market share in 2026.

The directed energy weapon segment is projected to witness moderate growth during the study period. The rise in government funding for improved border security, threat detection, and others leads to the segment growth.

REGIONAL INSIGHTS

In terms of geography, the market is divided into North America, Europe, Asia Pacific, the Middle East & Africa, and Latin America.

North America

North America Electronic Warfare Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for USD 9.3 billion in 2025, representing 46.10% of the global market share, and is projected to reach USD 10.3 billion in 2026. The growth can be attributed to the highest defense spending from the U.S. Department of Defense in the last decade. The U.S. allocated a defense budget of USD 782 billion in 2022. In 2021, the U.S. government allocated USD 3.17 billion for 45 electronic warfare programs across the military service departments and other platforms. The U.S. market is estimated to reach USD 5.88 billion by 2026.

Europe

The Europe market was valued at USD 3.4 billion in 2025, capturing 16.90% of global revenue, and is estimated to reach USD 3.8 billion in 2026. The regional growth can also be attributed to the presence of prominent players such as the Thales Group. The rising defense expenditure from developed countries, such as the U.K., Germany, France, Russia, and others, is also boosting regional growth. In March 2023, Elbit Systems Ltd. was awarded a contract to supply EW self-defense sets for a fighter aircraft being supplied to a NATO member state in Europe. As part of the contract, Elbit Systems equipped the aircraft with an EW Self-Defense Kit, which includes a Radar Warning Receiver (RWR) and a Countermeasure Delivery System (CMDS). The UK market is expected to reach USD 0.82 billion by 2026, and the Germany market is anticipated to reach USD 0.65 billion by 2026.

Asia Pacific

In 2025, Asia Pacific held 21.40% of the global market, reaching a valuation of USD 4 billion, and is projected to grow to USD 5 billion in 2026. Asia Pacific market is estimated to grow with the highest CAGR over the forecast period. The growth in the region is attributed to increasing expenditure in the defense sector from India, China, Japan, and Australia. In March 2022, the Indian Air Force had planned to develop an advanced EW suite for its fighter jet fleet. The Indian defense ministry signed a contract worth USD 409 million with Bharat Electronics Limited (BEL) to supply the Indian Air Force with advanced fighter aircraft with these capabilities. The Japan market is forecast to reach USD 0.41 billion by 2026, the China market is estimated to reach USD 2.39 billion by 2026, and the India market is expected to reach USD 0.66 billion by 2026.

Middle East & Africa

Middle East & Africa is anticipated to witness moderate growth during the forecast period. The growth is due to various factors such as regional tensions, modernization of the military, emerging threats, and rising investments in electronic warfare systems, among others. In January 2022, Elbit Systems Ltd. announced that its subsidiary in the UAE has been awarded a contract worth approximately USD 53 million to provide infrared countermeasures for the Airbus A330 Multi-Role Tanker Transport aircraft of the UAE Air Force.

Latin America

The Latin America region captured 6.50% of the global market in 2025, generating USD 1.31 billion in revenue, and is projected to reach USD 1.41 billion in 2026. Latin America is expected to show moderate growth during the study period. The growth can be attributed to the region’s focus on enhancing defense capabilities and improving military readiness. In April 2023, the Brazilian Navy and EDGE signed an agreement to explore the development of long-range hypersonic and anti-ship missiles jointly. The deal would help the partners leverage their collective expertise in missiles and related military technologies to support their common goals.

Key Industry Players

Leading Players Focus on the Development of Technologically Advanced EW Systems for Integrated Platforms

The global market is relatively consolidated with key players, such as Leonardo SpA (Italy), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Raytheon Technologies Corporation (U.S.), SAAB AB (Sweden), and others. These players majorly focus on the development of advanced EW systems for military operations and business expansion through partnerships and contracts with defense forces. The companies are also focused on expanding their regional presence in the EW market. For instance, in April 2023, Elbit Systems was awarded a USD 100 million contract to convert a commercial aircraft into an intelligence and EW asset for an international client. Under the agreement, the company would modernize the aircraft by equipping it with advanced intelligence mission sets and related EW capabilities.

List of Top Electronic Warfare Companies:

- L3Harris Technologies Inc. (U.S.)

- Moog Inc. (U.S.)

- Northrop Grumman Corporation (U.S.)

- Elbit Systems Ltd (Israel)

- BAE Systems Plc. (U.S.)

- Lockheed Martin Corporation (U.S.)

- General Dynamics Corporation (U.S.)

- Raytheon Technologies Corporation (U.S.)

- Thales Group (France)

- Leonardo SPA (Italy)

KEY INDUSTRY DEVELOPMENTS:

- June 2023 – Elbit Systems won a new contract from Airbus Helicopters for the supply of airborne EW self-defense systems for the Luftwaffe CH-53 GS/GE transport helicopter. The contract included the delivery of a Digital Radar Warning Receiver (RWR), EW Controller (EWC), and Countermeasure Delivery System (CMDS), improving the helicopter's operational efficiency and mission success.

- March 2023 – The Indian Ministry of Defense signed a contract with Bharat Electronics Limited (BEL), Hyderabad, to purchase two Integrated EW Systems, "Project Himshakti," at a total cost of approximately USD 362.2 million.

- April 2023 – L3Harris Technologies was awarded a five-year, USD 584 million contract by the U.S. Air Force to manufacture, design, and repair a suite of tools to protect aircraft from electronic threats. The company would provide block-cycle software development services for its advanced integrated defensive EW suite.

- April 2023 – Lockheed Martin Corp's LMT Rotary and Mission Systems business signed a revised contract worth USD 63.3 million for the Electronic Surface Warfare Improvement Program (SEWIP). The Naval Sea Systems Command, Washington, DC presented the award. The company would participate in the comprehensive production of SEWIP AN/SLQ-32(V)6 and AN/SLQ-32C(V)6 systems.

- April 2023 – BAE Systems received a USD 491 million contract from Lockheed Martin to produce the AN/ASQ-239 EW kit for the Block 4 version of the F-35 fighter jet.

REPORT COVERAGE

The market research report provides a detailed market analysis. It comprises all major aspects, such as R&D capabilities, supply chain management, optimization of the capabilities, competitive landscape, and opportunities for the market. Moreover, the report offers insights into the latest trends, market share and highlights key industry developments. In addition, it mainly focuses on several factors that contributed to the global market growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.20% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By End User

|

|

By Platform

|

|

|

By Type

|

|

|

By Technology

|

|

|

By Geography

|

Frequently Asked Questions

As per a study by Fortune Business Insights, the market was valued at USD 20.20 billion in 2025.

The market is expected to record a CAGR of 8.20% during the forecast period of 2026-2034.

The naval segment is expected to lead the market owing to advanced naval technologies and procurement of naval grade sub-systems.

The market size in North America stood at USD 9.3 billion in 2025.

Advancements in technology for the development of more sophisticated EW systems are expected to drive the market growth.

Some of the top companies in the market are Leonardo SpA (Italy), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Raytheon Technologies Corporation (U.S.), SAAB AB (Sweden), and others.

The U.S. dominated the market in 2026.

Complexity related to the integration of EW systems is a major restraining factor.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us