Radar Market Size, Share and Industry Analysis, By Radar Type (Pulsed Radar, Continuous Wave (CW) Radar, Synthetic Aperture Radar (SAR), Phased Array Radar, 3D/4D Radar, and Others), By Frequency Band (HF/VHF/UHF, L-Band, S-Band, C-Band, X-Band, and Ku/Ka/K-Band), By Component (Antennas, Transmitters, Receivers, Power Amplifiers, & Others), By Platform (Ground-based Radars, Airborne Radars, Naval/Shipborne Radars, Spaceborne Radars, & Others), By Vertical (Defense and Security, Commercial Aviation, Maritime Navigation, Automotive, & Others), By End User, and Regional Forecast 2026-2034

Radar Market Size and Future Outlook

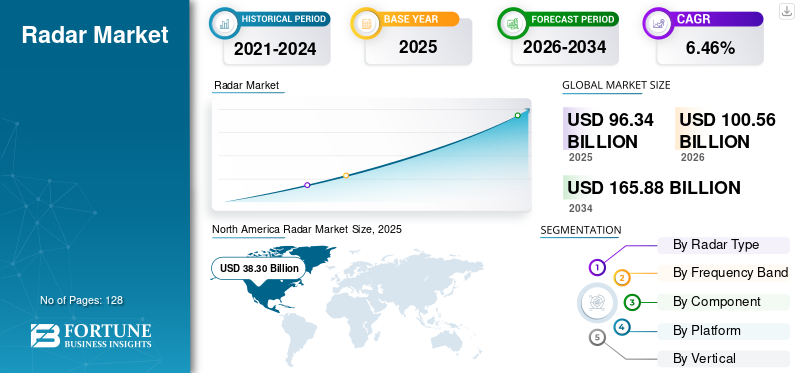

The global radar market size was valued at USD 96.34 billion in 2025. The market is projected to grow from USD 100.56 billion in 2026 to USD 165.88 billion by 2034, exhibiting a CAGR of 6.46% during the forecast period. North America dominated the global radar market with a market share of 39.75% in 2025.

Radar is an acronym for Radio Detection and Ranging, a basic detection technology using electromagnetic waves to locate and track targets in different environments. Various sectors employing radar systems include defense and aerospace, automotive safety systems that use ADAS, air traffic control, air defense systems, maritime navigation, weather forecasting and meteorology, and industrial automation. Its adaptability arises due to the fact that it can work under any condition of weather, time of day, or visibility, thus making it imperative in many commercial, civil, and military applications across the world.

The market is characterized by a concentrated competitive structure, with the leading players comprising established defence contractors and specialized technology providers. Major players include RTX Corporation, Lockheed Martin, Northrop Grumman, Thales Group, BAE Systems, Leonardo S.p.A., L3Harris Technologies, Saab AB, and Hensoldt AG. Competition is increasing by way of strategic investments in AI-enabled signal processing, modular radar architectures, and dual-use commercial-military platforms.

Download Free sample to learn more about this report.

RADAR MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 96.34 billion

- 2026 Market Size: USD 100.56 billion

- 2034 Forecast Market Size: USD 165.88 billion

- CAGR: 6.46% from 2026–2034

- North America dominated the radar market with a 39.75% share in 2025.

- X-band accounted for the largest share among frequency band segments in 2025.

- Power amplifiers held the largest component segment share at 20.15% in 2025.

North America

North America maintained market leadership, supported by strong defense spending and the presence of major radar manufacturers and defense contractors.

Europe

Europe accounted for 21.38% of the global market and is projected to be one of the fastest-growing regions due to strong participation from established defense and technology companies.

Asia Pacific

Asia Pacific is expected to witness robust growth, driven by indigenous radar development programs, expanding defense modernization initiatives, and increasing automotive radar adoption.

U.S.

The country remains the largest contributor to regional demand, supported by leading defense contractors, extensive military procurement programs, and continuous investments in advanced radar technologies.

Japan

Market growth is supported by the integration of radar technologies into automotive platforms and ongoing advancements by domestic electronics manufacturers.

Read More

Market Dynamics

Market Drivers

Automotive Autonomous Driving Adoption and Regulatory Mandates Catalyze Market Growth

The automotive segment is the fastest growing application domain, driven by converging regulatory mandates, consumer demands for safety, and accelerating autonomous vehicle development initiatives in major automotive industry catalyze the radar market growth. Regulations for advanced driver assistance systems (ADAS) advance radar based assistance system, have made the transition from optional premium features to mandatory safety features, as regulatory authorities continue raising the performance benchmark for active safety features such as Automatic Emergency Braking and pedestrian detection systems.

Sensor fusion methodologies that combine radar, camera, LiDAR, and ultrasonic technologies have become the industry-standard architectural approaches, as leading automotive manufacturers have standardized multisensor configurations across vehicle platforms and market segments

- For instance, in May 2025, Continental produced 200 million radar sensors and simultaneously announced major orders from several automotive manufacturers for production, which will start in 2026 and 2027; these include premium 4D long-range imaging radars and mass-produced front/corner radar configurations.

Market Restraints

Fragile Microelectronics and Critical Minerals Supply Chain Vulnerabilities Can Hamper Market Growth

Modern radar systems rely on specialized semiconductor components and rare earth materials whose supply chains have grown increasingly politicized and geographically concentrated, introducing significant cost volatility and production schedule risk into industry operations. Modern radar architectures depend on specialized semiconductors, including Gallium Nitride (GaN) devices and infrared subsystem components that contain gallium and germanium materials, the production capacity for which remains concentrated among a handful of suppliers highly susceptible to geopolitical manipulation.

Market Opportunities

4D Imaging Radar and Advanced Sensor Fusion Integration can Anticipate Market Growth Opportunities

Four-dimensional imaging radar technology introduces the elevation dimension to traditional range, azimuth, and Doppler measures for a transformative opportunity vector in enabling next-generation autonomous vehicle platforms, among other advanced military detection systems. 4D imaging radar significantly raises object resolution and classification capabilities compared to conventional 3D radar architectures; it delivers high-resolution point clouds that match LiDAR performance while maintaining radar's inherent all-weather operational reliability and reduced power consumption profiles.

According to market penetration trajectories, 4D radar will reach 11.4% penetration in automotive radar markets by 2025, transitioning from a niche premium technology to mainstream platform implementation within a 2-3 year horizon.

In April 2024, Uhnder launched the S81 mass-market 4D imaging radar leveraging DCM - a technology that significantly reduces the manufacturing cost for 96+ MIMO channel configurations with high-contrast resolution capabilities, targeting broad ADAS adoption across cost-sensitive vehicle segments.

Radar Market Trends

Artificial Intelligence and Machine Learning Integration for Signal Processing and Threat Classification Technologies Cater Market Growth

Artificial intelligence and machine learning technologies are increasingly acting to transform capabilities in radar signal processing, allowing for autonomous threat classification, object differentiation, and trajectory prediction capabilities that greatly enhance effectiveness while reducing the cognitive burden on human operators.

AI-driven signal processing methods bring substantially improved target differentiation through effective filtering of background noise and clutter, allowing detection systems to discern actual threats from environmental disturbances with far greater precision, especially in the most complex operational environments with high electromagnetic interference and ambiguous sensor observations.

- For instance, in May 2025, the NXP S32R47 third-generation imaging radar processor family integrates high-performance multi-core processing systems to support denser point cloud output and advanced algorithms that enable the next generation of ADAS implementation with enhanced object separation and improved pedestrian detection reliability.

Market Challenges

Electromagnetic Interference, Signal Degradation, and Performance Limitations in Complex Operational Environments to Challenge Market Growth

Performance degradation of radar systems due to electromagnetic interference, signal propagation challenges, and environmental impediments remains a continuing technical challenge. Electromagnetic spectrum congestion, especially within millimeter-wave frequency bands increasingly allocated for commercial wireless communications (5G/6G systems), introduces substantial interference risks for radar operations, requiring sophisticated signal processing techniques, frequency coordination mechanisms, and spectral sharing architectures to maintain operational reliability.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Radar Type

Defense Modernization and Next-Generation Platform Integration Drives Market Growth

The market is segmented by radar type into pulsed radar, continuous wave (CW) radar, synthetic aperture radar (SAR), phased array radar, 3D/4D radar, and others.

The phased array radar sub-segment dominated and is estimated to be the fastest growing with highest CAGR of 7.99% through forecast period of 2026-2034. It is structurally underpinned by global defense modernization programs where AESA technology is favored for its superior electronic beam steering, with the elimination of mechanical failure points and near-instantaneous target tracking across multiple domains simultaneously.

The 3D/4D radar sub-segment is estimated to be the second fastest growing with a CAGR of 7.06%.

By Frequency Band

Satellite Communication Expansion and High-Throughput Satellite Proliferation Anticipate Market Growth

The market is segmented by frequency band into HF/VHF/UHF, L-band, S-band, C-band, X-band, and Ku/Ka/K-band.

The Ku/Ka/K-band estimated to be the fastest growing with 8.52% CAGR. This remarkable growth trajectory is basically driven by the proliferation of commercial satellite constellations such as Starlink, OneWeb, and Amazon Kuiper, strategically deploying Ka-band and Ku-band technologies to deliver high-speed broadband connectivity to previously underserved global markets, particularly addressing the digital divide affecting rural communities and remote regions.

X-band sub-segment is accounted for the largest market share in radar market.

By Component

Artificial Intelligence and Machine Learning-Driven Signal Processing Evolution Propels Segmental Growth

The market is segmented by component into antennas, transmitters, receivers, power amplifiers, signal processors, displays, and software/algorithms.

The software/algorithms sub-segment is estimated to be the fastest growing during the forecast period of 2026-2034 with a highest CAGR of 8.37%. This demonstrates an explosive growth trajectory, fundamentally catalyzed by the transformative integration of artificial intelligence and machine learning techniques into radar signal processing workflows, enabling paradigmatic shifts toward autonomous decision-making capabilities that substantially enhance detection accuracy, reduce operator cognitive burden, and expand operational effectiveness across contested environments.

The power amplifiers sub-segment is accounted for the largest market share in the global market with 20.15% market share.

To know how our report can help streamline your business, Speak to Analyst

By Platform

Fifth-Generation and Sixth-Generation Fighter Aircraft Development Acceleration Drives Market Growth

The market is segmented by platform into ground-based radars, airborne radars, naval/shipborne radars, spaceborne/satellite radars, vehicle-mounted radars, and portable/manpack radars.

The airborne radars sub-segment is estimated to be the fastest growing during the forecast period. The incremental growth, signaling sustained momentum as next-generation AESA technologies achieve widespread adoption across military aviation communities. The main driver contributing to such an exceptional growth trajectory is the gradual modernization of combat aircraft fleets across the world, with a focus on fifth-generation fighter aircraft.

The ground-based radars sub-segment accounted for the largest market share in global market share.

By Vertical

Advanced Driver Assistance Systems Mandate and Regulatory Acceleration Catalyze Segmental Growth

The market is segmented by vertical into defense and security, commercial aviation, maritime navigation, automotive, space applications, weather monitoring & meteorology, and others.

The automotive sub-segment is estimated to be the fastest growing during the forecast period with 8.06% CAGR through 2026-2034. The rapid acceleration is basically catalyzed by stringent regulatory mandates that establish the mandatory integration of advanced safety systems, including AEB, FCW, and BSD functionalities that are progressively being implemented across developed and emerging automotive markets.

The defense and security sub-segment accounted for the largest market share in global market.

By End User

Sustained Military Modernization and Geopolitical Escalation Anticipate Segmental Growth

The market is segmented by end user into government & defense and commercial & civil.

The government & defense sub-segment is estimated to be the fastest growing during the forecast period of 2026-2034. The substantial increase in government defense sectors is fundamentally supported by global military expenditures, which are projected to rise further due to geopolitical tensions, ongoing regional disputes, and heightened demands for defense modernization in both advanced and developing defense markets.

The commercial & civil sub-segment is estimated to be the second fastest growing during the forecast period.

Radar Market Regional Outlook

By geographic, the market is categorized into North America, Europe, Asia Pacific, and Rest of World.

NORTH AMERICA

To get more information on the regional analysis of this market, Download Free sample

North America accounts for around 39.76% of global radar market share in 2025 and continues to be dominated by the leading positions of US-headquartered major defense contractors such as RTX, Lockheed Martin, and Northrop Grumman, holding around 60-75% of the market share for regional defense radar due to well-established government procurement relationships, military certification credentials, and extensive capital investment in leadership in radar technology.

ASIA PACIFIC

The Asia Pacific region emerges to be growing significantly, with compound annual growth rates surpassing 7.02% in the period of 2026 to 2035. The regional market reveals marked competitive fragmentation with arising indigenous supplier participation such as Chinese manufacturers are progressively establishing cost-competitive manufacturing capabilities, Indian defense enterprises are pursuing indigenous radar development programs, while Japanese electronics manufacturers are integrating radar technologies into automotive platforms.

EUROPE

Europe captures 21.38% of global market share and is estimated to be the fastest-growing global radar market, with the competitive landscape typified by a balanced mix of international majors-these include Thales, Leonardo, BAE Systems, Hensoldt, and Saab-commanding about 40-50% regional market share, and diverse mid-sized specialists, emerging companies, and technology startups competing for the rest of the market opportunity.

REST OF THE WORLD

The rest of world consist the Middle East & Africa radar market was valued at USD 8.19 billion in 2025 and is expected to witness a growth at 1.64% CAGR from 2026 to 2034, reaching USD 9.38 billion by 2034. The Latin America radar market represents a moderate-growth regional opportunity, with the overall market forecast projecting continued expansion. Segmentation in the Latin America radar market is very marked between military and commercial applications.

COMPETATIVE LANDSCAPE

Key Industry Players

The global radar market has a competitive structure that can best be described as being moderately consolidated, basically characterized by classified market dynamics with distinct structural characteristics across defense and commercial segments. It is highly competitive overall, fueled by converging technological advancements cycles, increased defense spending worldwide, and rapid growth in automotive sector adoption of radar-based safety systems, thereby sustaining the competitive pressure of continuous innovation and product differentiation.

Strategic merger and acquisition activity is gradually consolidating the structures of the radar industry, with recent notable transactions including RTX's integration of complementary capabilities in the defense sector, and ongoing development of cross-sector partnerships among semiconductor specialists, tier-one automotive suppliers, and software specialists looking for comprehensive perception stack integration capability.

List of Key Radar Companies Profiled in Report:-

- RTX Corporation (U.S.)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- Thales S.A. (France)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- BAE Systems plc (U.K.)

- HENSOLDT AG (Germany)

- Mitsubishi Electric Corporation (Japan)

- Continental AG (Germany)

- Bharat Electronics Limited (BEL) (India)

- Israel Aerospace Industries Ltd. (Israel)

- Indra Sistemas, S.A. (Spain)

- Robert Bosch GmbH (Germany)

- Terma A/S (Denmark)

KEY INDUSTRY DEVELOPMENTS

- October 2025: EWR Radar Systems has received a contract to deliver six more containerized E800LP solid-state dual-polarization weather radar systems to a defense client in Southeast Asia. With this contract, the total number of container-based E800LP radar systems in the region reaches 13.

- September 2025: Raytheon, a subsidiary of RTX, has received a contract from the U.S. Army worth USD 1.7 billion to supply the Lower Tier Air and Missile Defense Sensor, known as LTAMDS. This contract encompasses nine radars for both the U.S. Army and Poland, the inaugural international customer for LTAMDS, along with engineering services, spare parts, support, and development and testing.

- August 2025: Astra Microwave Products increased by 2.30 percent following the acquisition of a defense contract valued at USD 135.67 million from the Defence Research and Development Organisation (DRDO) for enhancing a ground-based radar system.

- July 2025: The Ministry of Defence has finalized an USD 194.6 million agreement with Bharat Electronics Limited (BEL) to acquire air defense fire control radars for the Indian Army. These radars, designed domestically with a minimum of 70% local content, are capable of detecting a range of aerial threats such as fighter jets, helicopters, and drones. This acquisition will enhance air defence capabilities and improve the Army's operational readiness.

- March 2025: The Ministry of Defence (MoD) of the Union has entered into a contract worth USD 29 million with Bharat Electronics Limited (BEL) in Ghaziabad for the acquisition of Low-level Transportable Radar, LLTR (Ashwini).

REPORT COVERAGE

The global radar market analysis provides an in-depth study of market size, regional analysis & forecast by all the market segments included in the report. It includes details on the radar market trends and market dynamics expected to drive the market over the forecast period. It offers information on the technological innovations, new product launches, key industry developments, and details on partnerships, mergers & acquisitions. The market research report also encompasses detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

| Global Radar Market | |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.46% from 2026-2034 |

| Unit | USD Billion |

| Segmentation |

By Radar Type

By Frequency Band

By Component

By Platform

By Vertical

|

| By Region |

North America (By Radar Type, By Frequency Band, By Component, By Platform, By Vertical, By Country)

Europe (By Radar Type, By Frequency Band, By Component, By Platform, By Vertical, By Country)

Asia Pacific (By Radar Type, By Frequency Band, By Component, By Platform, By Vertical, By Country)

Rest of World (By Radar Type, By Frequency Band, By Component, By Platform, By Vertical, By Sub-Region)

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 96.34 billion in 2025 and is projected to reach USD 165.88 billion by 2034.

In 2025, the market value stood at USD 20.60 billion

The market is expected to exhibit a CAGR of 6.46% during the forecast period of 2026-2034.

The Government & Defense segment is expected to hold the highest CAGR over the forecast period.

Automotive Autonomous Driving Adoption and Regulatory Mandates Catalyze the Market Growth

RTX Corporation (U.S.), Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), Thales S.A. (France), Leonardo S.p.A. (Italy), Saab AB (Sweden) and among others are top players in the market.

North America dominated the market in 2024.

- 2021-2034

- 2025

- 2021-2024

- 128

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us