Optical Communication Systems and Networking Market Size, Share & Industry Analysis, By Component (Optical Fiber, Optical Transceivers, Optical Amplifiers, Optical Switches, Optical Circulators, Optical Sensors, and Others), By Technology (WDM, SONET/SDH, Fiber Channel, and Others), By Data Range (Up to 40 GBPS, 40 to 100 GBPS, and > 100 GBPS) By Vertical (Marine, Space Exploration, Aviation, Defense, Energy & Utilities, and Others) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

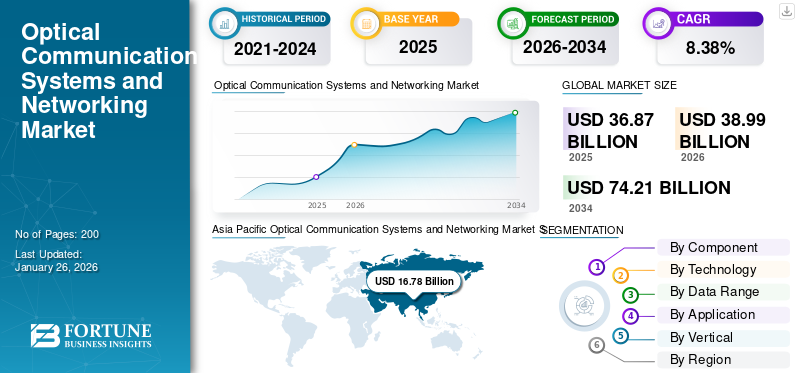

The global optical communication systems and networking market size was valued at USD 36.87 billion in 2025 and is projected to grow from USD 38.99 billion in 2026 to USD 74.21 billion by 2034, exhibiting a CAGR of 8.38% during the forecast period. Asia Pacific dominated the optical communication systems and networking market with a market share of 45.52.% in 2025.

Optical communication system and networking refers to the process of sending information from one location to another by utilizing light as a medium for the signal. In this setup, the information is converted into an optical signal through a light source, such as a laser diode or Light-emitting Diode (LED), and subsequently transmitted via an optical fiber cable to attain high-speed data rates over long distances. The optical signal is then received and converted back into its original form of information at the destination.

The system includes hardware components, such as fiber-optic cables, optical transceivers, optical amplifiers, multiplexers, and optical switches, alongside software and networking protocols to oversee and regulate the flow of data. These systems are employed in a diverse array of applications encompassing telecommunications, data centers, enterprise networking, healthcare, and aerospace & defense. Additionally, there are various technologies, such as synchronous optical network sonet & fiber channel and dense wavelength division multiplexing wdm to optimize the data transfer and networking infrastructure for various applications in fiber optics communication.

The COVID-19 pandemic caused supply chain disturbances, resulting in postponements in project execution and decreased funding for new initiatives. For example, in March 2020, Huawei Technologies announced a shortage in the availability of its optical components due to the lockdown in China, which interrupted its international supply chain.

Download Free sample to learn more about this report.

Global Optical Communication Systems and Networking Market KEY TAKEAWAYS

- 2025 Market Size: USD 36.87 billion

- 2026 Market Size: USD 38.99 billion

- 2034 Forecast Market Size: USD 74.21 billion

- CAGR: 8.38% from 2026–2034

- Asia Pacific dominated the optical communication systems and networking market with a 45.52% share in 2025.

- The optical transceiver segment is projected to dominate the market with a 31.92% share in 2026.

- The WDM technology segment is projected to dominate the market with a 45.24% share in 2026.

Asia Pacific

The market was valued at USD 16.78 billion in 2025 and is projected to reach USD 17.78 billion in 2026.

North America

The market was valued at USD 8.99 billion in 2025 and is projected to reach USD 9.53 billion in 2026.

Europe

The market was valued at USD 7.66 billion in 2025 and is expected to reach USD 8.09 billion in 2026.

U.S.

The market is projected to reach USD 8.15 billion by 2026.

Japan

The market is projected to reach USD 8.72 billion by 2026.

Read More

Optical Communication Systems and Networking Market Trends

Introduction of Software-Defined Networking (SDN) Technologies is a Prominent Market Trend

Software-Defined Networking (SDN) represents a significant trend that is becoming more popular within the market. SDN refers to a method of networking that utilizes software-driven controllers or Application Programming Interfaces (APIs) to engage with the foundational hardware infrastructure and regulate the traffic flow across a network. SDN is utilized to oversee and direct the movement of data through optical networks. Additionally, governmental initiatives, cloud-centric optical communication systems, advancements & innovations in products, and strategic partnerships & collaborations are also important trends within the market.

One of the key advantages of SDN in optical communication is its ability to optimize network performance through centralized control. Traditional optical networks often rely on distributed control mechanisms, which can lead to inefficiencies and slower response times during network disruptions. In contrast, SDN provides a global view of the network, enabling operators to monitor conditions in real-time and make conversant decisions about resource distribution and traffic management. This capability not only enhances the reliability of optical networks, but also allows for more sophisticated restoration strategies in case of failures. For instance, SDN can automate restoration processes based on learned patterns of failure, significantly improving the overall resilience of the network.

Furthermore, the integration of SDN with emerging technologies, such as Network Function Virtualization (NFV) is expected to further drive innovation in optical networking. This combination allows for greater flexibility and scalability, enabling operators to deploy new services quickly without extensive hardware changes. As organizations increasingly adopt cloud-based services and seek to enhance their digital infrastructures, SDN's role in facilitating efficient optical communication will become even more critical.

Optical Fiber Technology in Weapon Systems

The integration of optical fiber technology in weapon systems, particularly in fiber optic-guided missiles, represents a significant advancement in military precision and communication. This technology enhances the operator’s ability to guide munitions more accurately toward their targets by providing a high-bandwidth data link between the missile and its operator. Unlike traditional wire-guided systems, which are limited by electrical interference and bandwidth constraints, fiber optic systems allow for faster and more reliable communication, enabling real-time updates and adjustments during flight. The fiber optic link is also less susceptible to electrical interference, which is crucial for maintaining communication integrity in combat scenarios where electronic warfare tactics may be employed.

A notable example of this technology is the FOG-M (Fiber Optic Guided Multiple Purpose Missile) developed by Brazilian company Avibras. This missile utilizes optical fiber technology for guidance, allowing it to engage various targets, such as tanks and helicopters with high precision. The FOG-M has a range of approximately 60 kilometers and can be launched from multiple platforms, including ground vehicles and helicopters. Its design provides operators with a flexible and effective weapon system that is immune to electronic countermeasures.

Download Free sample to learn more about this report.

Market Dynamics

Market Drivers

Increasing Demand for High-Speed Data Transfer to Drive Global Market

The increasing use of 5G networks is predicted to propel the market’s expansion. 5G networks necessitate fast connectivity and minimal latency, which can be realized through optical communication technologies. For example, in December 2022, as per a report by 5G Americas, a U. S.-based telecommunications trade association, by Q3 2022, 75 nations had established 5G connections. The count of 5G connections rose by 433 million since Q3 2021, leading to a cumulative total of 922 million. Quarterly growth from quarter 2 to quarter 3 2022 was 14.4%, culminating in an overall total of 921 million connections.

The growing requirement for cloud-based services and the rising influx of IoT devices have significantly heightened the necessity for sophisticated optical communication systems and networking technologies. Moreover, the minimal latency and rapid-speed features of 5G networks are essential for many uses, including fixed-mobile replacement, collaborative AI, self-driving vehicles, virtual & augmented reality (AR), cloud gaming, healthcare, automotive, drones, video monitoring, education, smart cities & residences, wearable technology, infrastructure supervision, production, farming, and more. These extensive uses of 5G networks are expected to propel the market’s expansion.

Growing Investment in Network Infrastructure to Drive Market Growth

Governments and private sector companies are increasingly investing in upgrading and expanding their network infrastructure to support next-generation communication technologies. Initiatives aimed at enhancing broadband access and connectivity, especially in underserved regions, are driving the deployment of optical communication systems. For instance, investments in fiber-to-the-home (FTTH) projects are becoming more prevalent as they provide high-speed internet access directly to residential areas, significantly improving service quality. Furthermore, the integration of Software-Defined Networking (SDN) with optical networks is facilitating more flexible and efficient management of network resources, allowing operators to dynamically adjust to the changing traffic patterns and optimize performance. This trend toward modernization is expected to continue fueling growth of the optical communication systems and networking market.

Market Restraints

High Installation Costs to Negatively Impact Market Growth

High cost of installation is anticipated to impede the expansion of the market. The upfront costs of optical communication systems, including fiber optic cables and associated infrastructure, are considerably greater than those of conventional systems. Moreover, these systems require specialized machinery, skilled professionals, and civil engineering efforts, which contribute to increased capital costs. The process of installation is also technically intricate, and any errors made during installation or maintenance can cause significant disruptions and losses for companies.

- In May 2023, the Swedish Space Corporation (SSC) was awarded a USD 2.38 million contract from the European Space Agency (ESA), supported by the Swedish National Space Agency, as part of its ARTES Scylight program for the next phase of the optical communication project NODES. This contract will facilitate the execution, testing, and demonstration of an optical network, scheduled for 2023-2025, encompassing the commissioning of an additional optical ground station within the network.

Segmentation Analysis

By Component

Optical Transceiver Segment Dominated Market Due to Rising Need for High-Speed Data Transmission

Based on component, the market is categorized into optical fiber, optical transceiver, optical amplifiers, optical switches, optical circulators, optical sensors, and others.

The optical transceiver segment is projected to dominate the market with a share of 31.92% in 2026. Optical transceivers are essential components in fiber optic networks, enabling efficient long-haul and last-mile connectivity. The global push for expanding fiber optic networks to meet the demand for high-speed connectivity has resulted in a corresponding increase in the adoption of optical transceivers, particularly those supporting higher data rates, such as above 100G. In December 2023, Coherent Corp. revealed the latest 800G ZR/ZR+ transceiver, which is available in compact QSFP-DD and OSFP form factors. This innovative transceiver is designed specifically for optical communication networks, enhancing their high-speed data transmission capabilities essential for the modern telecommunications infrastructure.

The optical fiber segment is anticipated to experience considerable growth throughout the forecast period owing to the increasing popularity of Fiber-to-the-Home (FTTH) solutions. An optical fiber serves as a kind of communication medium employed to convey data in the form of light pulses. It is made up of a slender thread of glass or plastic, which can carry light signals over long distances while causing minimal deterioration in signal quality.

By Technology

WDM Technology Segment Dominates Market With Increase in Demand for High Network and Wavelength

By technology, the market is classified into WDM, SONET/SDH, Fiber Channel, and others (dense wavelength division multiplexing WDM).

The WDM technology segment is projected to dominate the market with a share of 45.24% in 2026. WDM allows multiple optical signals to be transmitted at the same time over a single optical fiber by utilizing different wavelengths of light. This capability significantly enhances the capacity of optical networks, allowing service providers to meet the growing data demands driven by applications, such as cloud computing, high-definition video streaming, and the Internet of Things (IoT). The SONET/SDH segment is expected to hold a 17.5% share in 2024.

The fiber channel segment is anticipated to grow significantly during the forecast period. A fiber channel is primarily used in Storage Area Networks (SANs) to connect servers to storage devices, providing high-speed data transfer capabilities that are essential for modern data centers. As enterprises increasingly adopt virtualization and cloud computing strategies, the demand for high-performance storage solutions has surged, driving the need for the fiber channel technology.

To know how our report can help streamline your business, Speak to Analyst

By Date Range

40-100 GBPS Segment to Expand Significantly Due to Increasing Application Areas in Optical Communication

Based on data range, the market is divided into up to 40 GBPS, 40 to 100 GBPS and > 100 GBPS.

The 40 to 100 GBPS segment is projected to dominate the market with a share of 52.50% in 2026, recording a CAGR more than that of the other segments. The increasing reliance on bandwidth-intensive applications, such as video streaming, cloud computing, and big data analytics is one significant factor for the segment’s growth.

The 100 Gbps segment is experiencing robust growth as organizations strive for faster and more efficient data transmission solutions. This growth is primarily driven by advancements in technology that enable higher bandwidth capabilities and the increasing deployment of next-generation networks, such as 5G.

By Vertical

Growing Marine Infrastructure in Various Countries to Fuel Growth of Marine Segment

Based on vertical, the market is segmented into marine, space exploration, aviation, defense, energy & utilities, and others.

The marine segment is projected to dominate the market during the forecast period. This growth is fueled by investments from telecom operators and technology companies seeking to expand their submarine cable networks to meet rising data traffic demands and improve connectivity between regions. In November 2024, L3Harris Technologies obtained an indefinite delivery, quantity contract from the U. S. Navy, valued at up to USD 999 million, to supply the U.S. and its coalition forces with robust communications technology. Over the next five years, L3Harris will supply its Multifunctional Information Distribution System Joint Tactical Radio System Terminals (MIDS JTRS). The company is one of two suppliers of the MIDS JTRS solution, which serves as an essential, software-defined Link 16 resilient communication radio for multiple air, ground, and maritime platforms.

The defense segment is projected to dominate the market with a share of 27.38% in 2026. Optical communication systems offer high bandwidth, low latency, and improved security features, making them ideal for defense applications, such as battlefield communications, surveillance, and reconnaissance.

Optical Communication Systems and Networking Market Regional Outlook

The global market regions are segmented into North America, Europe, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Optical Communication Systems and Networking Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, Asia Pacific generated USD 16.78 billion, contributing 45.52% to global market revenue, and is projected to grow to USD 17.78 billion in 2026. The region is experiencing rapid growth in cloud computing, leading to an increased number of data centers that rely on optical communication technologies for efficient operations. In October 2024, NEC was awarded a contract to provide optical communication solutions for a defense project in Japan, thereby focusing on enhancing network resilience and security for military communications. The Japan market is projected to reach USD 8.72 billion by 2026, the China market is projected to reach USD 4.69 billion by 2026, and the India market is projected to reach USD 0.81 billion by 2026.

North America

The North America region captured 24.40% of the global market in 2025, generating USD 8.99 billion in revenue, and is projected to reach USD 9.53 billion in 2026. The rapid rollout of 5G networks in the region necessitates high-capacity optical communication solutions to support low-latency and high-speed data transmission. This transition is essential for enabling advanced applications, such as autonomous vehicles, smart cities, and IoT devices and is anticipated to boost the regional market’s growth. For example, in February 2023, Frontier Communications Parent, Inc., a telecommunications firm based in the U.S., initiated Fiber Innovation Labs, which are designed to create and test new patents, technologies, and methods that will improve its fiber-optic network. The U.S. market is projected to reach USD 8.15 billion by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 7.66 billion in 2025, accounting for 20.78% share, and is expected to reach USD 8.09 billion in 2026. European countries are heavily investing in digital transformation initiatives, including the expansion of broadband networks and adoption of advanced optical technologies. In April 2023, BT Group plc entered a contract to upgrade its optical fiber network across the U.K., thereby focusing on increasing capacity and reliability for broadband services. The UK market is projected to reach USD 0.88 billion by 2026, while the Germany market is projected to reach USD 3.93 billion by 2026.

Rest Of The World

The market in the rest of the world is anticipated to show moderate growth during the forecast period. Emerging markets, such as Middle East and Africa are witnessing increased investments in their telecommunications infrastructure, driven by the demand for improved internet connectivity and digital services for both commercial and military applications. In October 2024, eand, also known as e&, a prominent global technology organization, signed a Memorandum of Understanding (MOU) with ZTE Corporation, a world-leading supplier of integrated information and communication technology solutions. This strategic alliance signified an important advancement toward promoting innovation and cooperation in the telecommunications industry.

Competitive Landscape

List of Key Industry Players

Key Market Players are Focusing On Technological Progress and Product Developments

The global market is made up of major players, including Cisco Systems Inc., Corning Incorporated, Huawei Technologies Co. Ltd., Ciena Corporation, Nokia, Adva Optical Networking SE, and Arista Networks, among others. These players are concentrating on technological advancements, product innovations, and growth in emerging markets to enhance their market share. In March 2023, Ayar Labs, Inc., a company based in the U.S. that creates an optical I/O solution, introduced the first bidirectional Wavelength Division Multiplexing (WDM) optical solution in the industry, achieving 4 terabits per second (Tbps). This innovation is anticipated to lead to advancements in next-generation AI and data center architectures.

List of Key Companies Profiled

- Huawei Technologies Co. Ltd. (China)

- Corning Incorporated (U.S.)

- Ciena Corporation (U.S.)

- Nokia (Finland)

- Cisco Systems Inc. (U.S.)

- Fujitsu (Japan)

- ADVA Optical Networking SE (Germany)

- NEC Corporation (Japan)

- Infinera Corporation (U.S.)

- Juniper Networks Inc. (U.S.)

- Thales Group (France)

- General Atomics (U.S.)

- Space Photonics Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2024 – Nokia secured an agreement with Deutsche Telekom to implement an extensive commercial O-RAN network in Germany. Nokia granted over 3,000 locations backing Deutsche Telekom’s Open RAN network goals. The firm emphasizes robust, wide-ranging multi-vendor Open RAN network deployment.

- January 2024 – General Atomics was awarded a contract to develop Optical Communication Terminals (OCTs) for satellite communications in Low Earth Orbit (LEO). This initiative aims to enhance secure data transmission capabilities for military applications.

- September 2024 – Huawei introduced the first railway optical communication network solution in the industry that conforms to the fine-grain OTN (fgOTN) standard. The objective is to guarantee secure and stable operation within the railway sector. The solution facilitates unified access to a range of services including E1, PDH, SDH, MPLS-TP, and fgOTN. Furthermore, it delivers high bandwidth, exceptional reliability, minimal latency, and straightforward OandM, which can completely satisfy current railway service needs. Additionally, the solution allows for a seamless transition of the railways’ wireless train control system from GSM-R to FRMCS, thereby ensuring secure and stable operation.

- March 2023 – Sunwalk (Pvt.) Ltd, a telecom & technology firm located in China, aimed to invest USD 2 billion in Pakistan’s telecom industry to establish an optical fiber network that will eventually span 100,000 km. Following an investment of approximately USD 5 million in the first phase, the company intends to lay Optical Fiber Cables (OFCs) at long distances of 5,000 km in the subsequent stage.

- February 2023 – Cisco Systems Inc., a digital technology firm located in the U. S., declared that it had joined forces with V. tal to speed up the rollout of 5G services. V. tal is a Brazil-based comprehensive fiber-optic neutral network firm and possesses the most extensive infrastructure in the nation, with over 450,000 kilometers of terrestrial optical fiber linking more than 2,380 municipalities.

REPORT COVERAGE

The report offers in-depth details about the market, highlighting top companies, diverse product types, and key product applications. Moreover, it provides valuable insights into market trends, market segmentation, technological advancements, and the competitive landscape. It also delves into the demand for optical communication systems and networking solutions while highlighting key industry developments.

Request for Customization to gain extensive market insights.

REPORT SCOPE AND SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8.38% during 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Component

|

|

By Technology

|

|

|

By Data Range

|

|

|

By Vertical

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global optical communication systems and networking market was valued at USD 36.87 billion in 2025 and is projected to reach USD 74.21 billion by 2034, exhibiting a CAGR of 8.38% during the forecast period.

Registering a CAGR of 8.38%, the market will show rapid growth during the study period.

Growth is primarily driven by the rapid deployment of 5G networks, increased data traffic from cloud computing, and the widespread use of IoT devices, all of which demand faster and more reliable data transmission infrastructure.

Essential components include fiber optic cables, optical transceivers, amplifiers, WDM systems, optical switches, and network management software, all working together to ensure efficient data transmission.

Key applications span across telecommunications, data centers, defense and aerospace, submarine communications, and industrial automation, where high-speed, secure data transfer is critical.

5G requires ultra-low latency and high bandwidth, which can only be supported by fiber-optic backhaul infrastructure, making optical communication systems a foundational technology for 5G deployment worldwide.

Notable trends include AI-driven network optimization, FTTx (Fiber-to-the-x) deployments, SDN integration, low-power optical components, and rising demand for secure military-grade communication systems.

Asia Pacific dominates the market due to heavy investments in 5G infrastructure, large-scale data center growth, and strong demand from telecom providers in countries like China, India, and Japan.

Leading companies include Huawei Technologies, Cisco Systems, Ciena Corporation, Corning Inc., Nokia, Infinera Corporation, and ADVA Optical Networking, known for their innovation and large-scale deployments.

Wavelength Division Multiplexing (WDM) allows multiple data channels to travel simultaneously over a single fiber by using different light wavelengths, drastically increasing the capacity and efficiency of optical networks.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us