"Smart Strategies, Giving Speed to your Growth Trajectory"

Data Center Market Size, Share & Industry Analysis, By Component (Hardware, DCIM (Data Center Infrastructure Management) Software, and Services), By Data Center Type (Colocation, Hyperscale, Edge, and Others), By Tier Level (Tier 1 and Tier 2, Tier 3, and Tier 4), By Data Center Size (Small, Medium, and Large), By Industry (BFSI, IT & Telecom, Healthcare, Government, Manufacturing, Retail & E-commerce, and Others), and Regional Forecast, 2026-2034

Last Updated: July 20, 2026

| Format: PDF

| Report ID:

FBI109851

Thank you for your interest in the

"United States Medical Devices Market!"

To receive a sample report, please provide the following details:

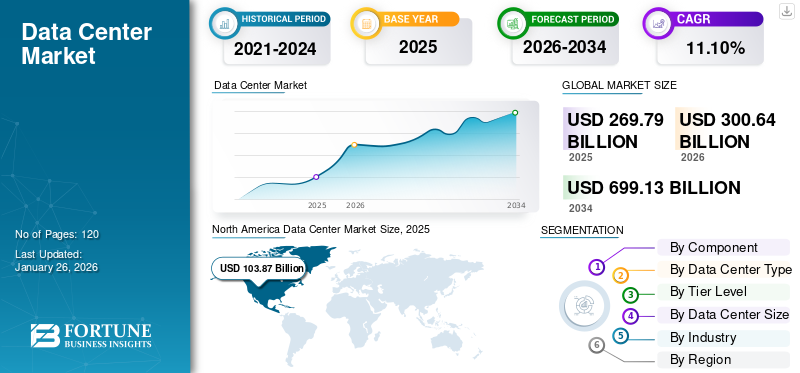

The global data center market is projected to reach around $699.13 billion by 2034, growing from $269.79 billion in 2025 and about $300.64 billion in 2026, reflecting a compound annual growth rate (CAGR) of about 11.10% during the forecast period.

Growth of the data center market is expected to accelerate as organizations increasingly adopt digital technologies, cloud computing, and large-scale data processing infrastructure across industries.

Data centers have become a critical backbone of the digital economy, supporting data storage, computing power, and connectivity for enterprises and online services worldwide.

North America currently leads the global data center market, accounting for about 38.5% of the market share in 2025, driven by strong technology infrastructure and the presence of major cloud and technology companies.

The global data center market size was valued at USD 269.79 billion in 2025 and is projected to grow from USD 300.64 billion in 2026 to USD 699.13 billion by 2034, exhibiting a CAGR of 11.10% during the forecast period. North America dominated the global data center market, accounting for 38.50% market share in 2025. Industry growth is driven by hyperscale expansion, AI infrastructure demand, accelerated cloud adoption, and enterprise digital transformation investments across emerging and mature economies.

A data center is an ecosystem of technologies, businesses, and services involved in the development, utilization, and operation of data center facilities. It encompasses various components, including hardware, software, and services. The hardware includes server storage devices, racks, networking equipment, and other hardware used to store and distribute digital data and services. The market is dynamic and competitive, with continuous innovation in designs, operational practices, and technologies, such as cloud computing and edge computing, to meet the evolving needs of organizations and businesses across industries.

Data center market growth is underpinned by structural demand for high-density computing environments. Artificial intelligence model training and inference workloads are accelerating rack power density requirements beyond legacy configurations. Capital expenditure cycles remain elevated due to facility modernization, renewable energy integration, and advanced cooling deployment. Investors evaluate long-term lease structures, power availability, and network connectivity depth when assessing asset viability.

The data center market share distribution continues to shift toward hyperscale cloud providers and large colocation platforms. Consolidation activity supports scale advantages in procurement, energy sourcing, and operational optimization. Enterprise-owned facilities are gradually transitioning toward hybrid and outsourced models to improve cost efficiency and resiliency. Regionally, North America maintains leadership in installed capacity. Asia-Pacific demonstrates the fastest incremental additions due to digitalization and population scale. Europe emphasizes sustainability compliance and transparency in carbon reporting.

The COVID-19 pandemic swiftly transitioned to online education, remote work, digital entertainment, e-commerce, and telehealth. This rise in online activity led to increased demand for data center services to support the growing volume of digital data, services, and applications. Also, the pandemic sped up the adoption of cloud computing services, as organizations wanted to scale and adapt their IT infrastructure to meet changing business needs. In the scope of work, we have included solutions offered by Schneider Electric, ABB Ltd., IBM Corporation, Cisco Systems, Inc., Huawei Technologies Co., Ltd., Hitachi Ltd, and others.

North America dominated the data center market with a 38.50% share in 2025.

The hardware segment is projected to account for 51.28% of the market in 2026.

The colocation segment is projected to hold a 34.46% market share in 2026.

Key Regional Highlights

North America

North America generated USD 103.87 billion in 2025 and remained the largest regional market, driven by hyperscale, AI, and cloud investments.

Asia Pacific

Asia Pacific reached USD 61.02 billion in 2025 and is expected to record the fastest growth due to rapid digitalization and hyperscale expansion.

Europe

Europe accounted for USD 68.98 billion in 2025, supported by strong network infrastructure and sustainability-focused data center investments.

U.S.

The data center market is projected to reach USD 79.25 billion by 2026, fueled by AI workloads, cloud adoption, and hyperscale development.

Japan

The data center market is projected to reach USD 14.17 billion by 2026, supported by enterprise modernization and cloud migration initiatives.

Read More

IMPACT OF GENERATIVE AI ON THE DATA CENTER MARKET

Mounting Demand for Computational Power in Data Centers to Drive Market Development

Generative AI models, especially those based on deep learning, require significant computational resources for training and inference. This can lead to increased demand for high-performance computing infrastructure, driving the need for more powerful data centers. Generative AI models often require large data sets for training, which necessitates robust data storage and management solutions. Data centers will need to provide scalable and efficient storage solutions to handle the growing volume of training data. The incorporation of generative AI technology enables data storage centers with high accuracy, minimal interventions, consistent performance, and predictable outcomes.

MARKET DYNAMICS

Data Center Market Trends

Increasing Focus on Adoption of Hybrid and Multi-Cloud Strategies Fuels Market Growth

The data center market is continuously evolving, driven by advancements in technology, changing businesses, and emerging industry requirements. Organizations are increasingly adopting hybrid and multi-cloud strategies to leverage the benefits of public cloud services, private cloud environments, and on-premise infrastructure. This trend is driving the demand for interconnection platforms, colocation services, and hybrid cloud management solutions that enable seamless integration, workload mobility, and data portability across diverse cloud environments. Moreover, modular and prefabricated data center solutions are gaining popularity due to their flexibility, scalability, and rapid deployment capabilities. These pre-engineered modules can be quickly assembled and deployed to meet changing capacity requirements, enhance operational efficiency compared to traditional brick-and-mortar facilities, and reduce construction costs and time. For instance,

September 2022: Dell Technologies and Red Hat entered into a partnership to simplify the deployment and management of on-premise infrastructure in multi-cloud environments and across data centers.

One prominent trend in the data center market is the acceleration of hyperscale campus development in secondary cities. Operators seek lower land costs and improved grid access while maintaining fiber connectivity to major hubs. This decentralization supports capacity diversification. High-density rack deployment is becoming standard practice. Artificial intelligence workloads require rack power levels exceeding traditional enterprise thresholds. Liquid cooling solutions are increasingly integrated to manage thermal intensity efficiently.

Sustainability reporting has transitioned from optional to mandatory in several jurisdictions. Operators invest in renewable power purchase agreements, onsite solar installations, and battery energy storage systems. Power usage effectiveness optimization remains central to competitive positioning. Modular construction techniques are gaining traction. Prefabricated data hall components reduce deployment timelines and mitigate labor shortages. This approach enhances scalability and capital discipline.

Edge data center expansion supports latency-sensitive applications such as autonomous systems, real-time analytics, and industrial automation. Smaller distributed facilities complement centralized hyperscale hubs.

Increased Digitalization and Cloud Adoption among Industries Drives Market Growth

The rapid shift toward digital transformation across industries is driving the demand for data centers. Organizations are increasingly adopting cloud services for flexibility, scalability, and cost efficiency. The growth of cloud computing, including private, public, and hybrid clouds, is significantly boosting data center investments.

In addition, the rollout of 5G networks and the growing demand for high-bandwidth, low-latency applications are driving the deployment of edge data centers among small businesses. These facilities bring computing resources closer to end-users and devices, supporting real-time processing and reducing latency for applications, such as smart cities, autonomous vehicles, and AR/VR.

The primary driver of the market is sustained cloud computing adoption across the enterprise and government sectors. Organizations increasingly migrate workloads to hybrid and multi-cloud environments to enhance scalability and operational resilience. This structural shift directly increases hyperscale and colocation demand. Artificial intelligence and high-performance computing workloads represent a second major catalyst. Advanced model training requires significant graphics processing unit clusters and high-density power distribution. Facilities must support elevated thermal loads and optimized airflow management. This requirement stimulates infrastructure upgrades and greenfield construction.

Data localization regulations also influence the data center market growth trajectory. Governments mandate domestic data processing for critical sectors, driving in-country capacity expansion. Compliance considerations encourage enterprises to deploy region-specific infrastructure. Digital transformation initiatives across banking, financial services, and insurance (BFSI), healthcare, manufacturing, and retail sectors expand transactional data volumes. Real-time analytics, Internet of Things (IoT) connectivity, and 5G network deployment increase edge processing requirements.

Market Restraints

Significant Initial Investments and Operational Costs May Stifle Market Growth

The data center requires a significant initial investment in infrastructure, including power and cooling systems, real estate, IT hardware, and network equipment. This initial high investment can be a barrier for SMEs or startup businesses with limited financial resources. Moreover, this facility requires high operational costs for electricity, cooling, security, staffing, and maintenance. These costs can be substantial for large businesses, as increasing operational costs can strain the budget and reduce profitability for data center operations.

Power availability remains the most significant constraint within the market. Grid interconnection timelines often extend multiple years, limiting near-term capacity commissioning. In high-demand metropolitan areas, transmission bottlenecks restrict expansion feasibility. Energy cost volatility introduces financial uncertainty for operators. Elevated electricity pricing compresses operating margins, particularly for facilities without long-term renewable procurement contracts. Environmental compliance obligations further increase capital requirements.

Land acquisition challenges affect large-scale developments. Urban zoning restrictions and community opposition can delay permitting. Water usage concerns, particularly for evaporative cooling systems, intensify regulatory scrutiny in drought-prone regions. Supply chain constraints persist across electrical equipment, switchgear, transformers, and high-capacity cooling systems. Lead times for specialized components may extend project delivery schedules. Semiconductor shortages influence server deployment cycles.

Cybersecurity risk also represents a structural concern as the data center infrastructure becomes more interconnected, and threat exposure increases. Operators must allocate resources toward security architecture, increasing operational expenditure.

Market Opportunities

Artificial intelligence infrastructure presents a substantial opportunity within the market. As enterprise adoption of generative models expands, operators capable of delivering high-density environments will capture premium lease rates. Facilities optimized for advanced graphics processing clusters command differentiated value. Emerging markets offer long-term expansion potential. Digital penetration growth across Southeast Asia, Latin America, and Africa increases demand for regional compute capacity. Strategic partnerships with local telecommunications providers facilitate entry.

Edge computing deployment creates additional revenue streams. Industrial Internet of Things applications, smart cities, and autonomous logistics require distributed processing nodes. Operators that integrate centralized and edge offerings enhance service portfolios. Sustainable infrastructure development represents another opportunity. Enterprises increasingly prioritize low-carbon data hosting environments—facilities powered by renewable energy secure competitive differentiation. Green financing instruments further reduce capital costs for compliant projects.

Hybrid cloud enablement services support enterprise migration strategies. Colocation providers offering integrated connectivity ecosystems strengthen customer retention. Cross-connect density and carrier neutrality enhance asset attractiveness. Government digital modernization programs stimulate public sector demand. Secure sovereign cloud deployments require localized infrastructure capacity. Collectively, these opportunities reinforce positive market growth prospects across developed and emerging economies.

Data Center Market Segmentation Analysis

By Component Analysis

The Growing Need for Reliable and High-Performance Infrastructure has boosted the Demand for Hardware Equipment.

Based on component, the market is divided into hardware (power systems, cooling systems, servers, networking devices, and others), DCIM (data center infrastructure management) software (on-premises and cloud), and services.

Hardware

The hardware segment is projected to dominate the data center market, accounting for 51.28% of the global market share in 2026, as it provides the foundation for building reliable, high-performance infrastructure to support modern computing needs, ranging from traditional enterprise applications to emerging technologies, such as artificial intelligence and big data analytics. Also, this hardware can be scaled up or down to meet changing demands, allowing organizations to expand their computing resources as needed without significant downtime.

Hardware remains the largest contributor to the overall market size. This segment includes servers, storage systems, networking equipment, power distribution units, cooling systems, racks, uninterruptible power supply infrastructure, and backup generators. Rising compute density driven by artificial intelligence, cloud workloads, and high-performance computing increases hardware investment per megawatt.

Power and cooling infrastructure account for a growing proportion of capital expenditure. Advanced thermal management solutions, including liquid cooling and containment systems, are deployed to support high-density racks. Hardware competition focuses on efficiency, reliability, and scalability. While margins are influenced by procurement cycles and supply constraints, hardware continues to anchor overall data center market share.

DCIM (Data Center Infrastructure Management) Software

The DCIM (data center infrastructure management) software segment is expected to grow at the highest CAGR during the forecast period, as it provides a centralized platform for managing and monitoring all aspects of data center infrastructure, including networking equipment, cooling systems, storage devices, servers, and power distribution units. This centralized view enhances control and visibility, enabling supervisors to oversee and coordinate operations efficiently.

DCIM software is becoming increasingly strategic within the data center industry. These platforms provide real-time monitoring of power consumption, environmental conditions, asset utilization, and capacity planning. Operators rely on DCIM tools to optimize power usage effectiveness and enhance operational visibility.

As sustainability reporting becomes mandatory in several regions, software-driven energy analytics gains importance. Integration with predictive maintenance models reduces downtime risk and improves cost efficiency. Although smaller in absolute revenue compared to hardware, DCIM software contributes disproportionately to margin expansion and operational optimization within the data center market.

Services

Services include design, engineering, commissioning, system integration, managed hosting, and maintenance contracts. As enterprises migrate from owned infrastructure toward colocation and hybrid cloud models, managed services adoption increases. Long-term service agreements enhance revenue stability and strengthen customer retention.

Consulting and deployment services are particularly relevant for hyperscale expansion and Tier 3 or Tier 4 builds. Recurring operations and maintenance contracts support predictable cash flow generation. Services, therefore, represent a structurally important growth layer within the broader data center market growth trajectory.

By Data Center Type Analysis

Growing Demand for Cost-Effective Solutions among Enterprises Fueled Demand for Colocation Facilities

Based on data center type, the market is categorized into colocation, hyperscale, edge, and others (managed and modular).

Colocation

The colocation segment is expected to lead by type, contributing 34.46% of the global market share in 2026. Colocation facilities offer flexible scalability options, allowing tenants to quickly and easily scale their IT infrastructure according to changing business needs. Sharing infrastructure resources with other tenants reduces upfront capital expenditure for building and maintaining a private data storage facility. Additionally, economies of scale enable colocation providers to offer cost-effective solutions for security and connectivity, resulting in lower operational expenses for tenants.

Colocation facilities represent a significant portion of the global data center market share: enterprises lease rack space and connectivity to reduce capital intensity and enhance scalability. Carrier-neutral ecosystems and dense interconnection environments provide competitive differentiation. Colocation demand is driven by hybrid cloud strategies and regulatory compliance requirements. Multi-tenant facilities diversify revenue exposure and reduce dependency on single customers. The segment demonstrates steady absorption rates across mature and emerging markets.

Hyperscale

The hyperscale segment is expected to grow at the highest CAGR during the forecast period, as they are designed to scale rapidly and efficiently to support massive amounts of data and workloads. Their architecture allows for seamless expansion of computing, storage, and networking resources to accommodate growing demand without sacrificing performance or reliability.

Hyperscale data centers account for the majority of incremental capacity additions globally. These large-scale campuses support cloud service providers and digital platforms. Standardized design templates, modular expansion models, and renewable energy procurement enhance cost efficiency. Hyperscale expansion materially influences global data center market growth metrics. Capital expenditure intensity is high, but long-term occupancy commitments and scale advantages support durable returns.

Edge

Edge data centers address latency-sensitive workloads, including 5G networks, industrial automation, and real-time analytics. These facilities are smaller and distributed closer to end users. Although individually limited in capacity, aggregated deployments contribute meaningfully to data center market size expansion. Edge infrastructure complements hyperscale campuses rather than replacing centralized architectures. Growth remains closely linked to telecommunications investment and digital infrastructure rollout.

To know how our report can help streamline your business, Speak to Analyst

By Tier Level Analysis

Increasing Demand for Redundant Connectivity Drives Demand for Tier 3 Data Centers

Based on tier level, the market is classified into tier 1 and tier 2, tier 3, and tier 4.

Tier 1 and Tier 2

Tier 1 and Tier 2 facilities provide limited redundancy and support non-critical workloads. These facilities remain relevant in cost-sensitive regions and emerging markets. However, new builds in mature economies increasingly favor higher-tier standards.

Tier 3

The tier 3 segment captured the largest share of the market in 2024, as it has redundant network connectivity with multiple carriers and internet service providers, ensuring diverse and resilient communication pathways. This helps minimize the risk of network outages and provides reliable connectivity for mission-critical applications and services. Tier 3 facilities dominate new construction activity. They offer concurrently maintainable infrastructure and high availability. Enterprises favor Tier 3 certification for balanced cost and reliability. This tier represents a substantial share of the global market size.

Tier 4

The tier 4 segment accounted for 39.46% of the global market share in 2026, reflecting strong demand for high-reliability infrastructure. It implements advanced physical security measures, such as biometric access controls, intrusion detection systems, surveillance cameras, and security portals, to protect infrastructure assets from unauthorized access or theft. Tier 4 centers also employ cybersecurity measures to safeguard against cyber threats and data breaches.

Tier 4 facilities provide fault-tolerant architecture with multiple independent power and cooling paths. These environments support mission-critical operations in banking, government, and hyperscale cloud platforms. Although capital-intensive, Tier 4 certification commands premium lease pricing and strengthens market positioning.

By Data Center Size Analysis

Increasing Focus on Adoption of Diverse Connectivity Options Boosted Demand for Large Data Centers

Based on data center size, the market is divided into small, medium, and large.

Large

The large data center segment held a 44.32% share of the global market in 2026, driven by hyperscale and enterprise deployments as they offer access to a wide range of network service providers, cloud providers, and internet exchanges, enabling tenants to establish low-latency, high-speed connections to their preferred carriers and cloud platforms. This enhances connectivity options, improves network performance, and supports hybrid cloud and multi-cloud deployments.

Large facilities exceed 20 megawatts and are characteristic of hyperscale operators. Multi-building campuses benefit from procurement leverage and renewable energy sourcing advantages. Large-scale projects significantly influence overall market growth metrics.

Small

Small data centers are expected to grow at the highest CAGR during the forecast period, as they are more cost-effective to build, operate, and maintain compared to large-scale facilities. They require less initial investment in real estate, equipment, and infrastructure, making them an attractive option for businesses with limited budgets or smaller IT requirements. Small facilities typically operate below 5 megawatts and support localized or edge workloads. They offer lower capital requirements but limited scalability. This segment is often deployed in regional or distributed architectures.

Medium

Medium facilities range from 5 to 20 megawatts and serve regional colocation demand. Phased expansion strategies allow operators to align capital deployment with absorption rates. Many emerging markets prioritize medium-scale developments.

By Industry Analysis

Increasing Popularity of Digital Transformation Initiatives in IT & Telecom Propel Market Growth

Based on industry, the market is categorized into BFSI, IT & telecom, healthcare, government, manufacturing, retail & e-commerce, and others (media & entertainment).

IT & Telecom

The IT & telecom segment captured the highest market share in 2024. IT & telecom companies are undergoing digital transformation initiatives to modernize their infrastructure, applications, and services. Data centers play an important role in supporting these initiatives by providing the computing power, storage capacity, and networking capabilities needed to deploy new technologies and deliver innovative digital services.

IT and Telecom represent the most compute-intensive vertical. Cloud platform expansion, content delivery, and network virtualization drive hyperscale development. This segment materially influences market share distribution.

BFSI

The BFSI segment is expected to grow at the highest CAGR in the coming years, as the BFSI sector deals with sensitive financial and personal data, making security and compliance paramount. Data centers offer secure environments equipped with robust physical and cybersecurity measures to protect against data breaches and ensure compliance with industry regulations, such as the General Data Protection Regulation (GDPR) and various financial regulations.

Banking, financial services, and insurance require secure, high-availability environments for transaction processing and regulatory compliance. Hybrid deployment models sustain demand for Tier 3 and Tier 4 facilities.

Healthcare

Healthcare demand is increasing due to electronic health records, medical imaging analytics, and telemedicine systems. Data security standards necessitate a high-reliability infrastructure.

Government

Government agencies require sovereign hosting environments for administrative and defense applications. Data localization mandates reinforce domestic capacity expansion.

Manufacturing

Manufacturing adoption reflects industrial automation, predictive maintenance, and supply chain analytics integration. These workloads increasingly rely on hybrid and edge deployments.

Retail & E-commerce

Retail and e-commerce platforms require scalable infrastructure to manage peak demand cycles and real-time transaction processing. Seasonal traffic volatility influences capacity planning strategies.

REGIONAL INSIGHTS

By region, the market has been analyzed across five major regions: North America, Europe, Asia Pacific, the Middle East & Africa, and South America.

North America Data Center Market Size, 2025 (USD Billion)

The North America region captured 38.50% of the global market in 2025, generating USD 103.87 billion in revenue, and is projected to reach USD 114.67 billion in 2026. The rapid adoption of cloud services, AI, and big data applications has fueled a surge in data center demand in the region. Enterprises are increasingly utilizing generative AI and other advanced technologies, which necessitate enhanced data processing capabilities and robust infrastructure. Substantial investments from key players, such as Schneider Electric, IBM, Cisco, and others, fuel market expansion. The U.S. market is expected to reach USD 79.25 billion by 2026.

North America leads the global data center market due to hyperscale concentration, mature cloud adoption, and deep capital availability. Strong fiber connectivity, renewable procurement frameworks, and enterprise outsourcing support sustained capacity expansion. Power constraints in key metropolitan hubs influence site selection toward secondary markets. The region maintains a dominant market share, supported by long-term hyperscale lease commitments.

United States Data Center Market:

The United States data center market reflects significant hyperscale campus development and colocation expansion. Cloud providers continue multi-megawatt deployments across established and emerging regions. Grid interconnection timelines and power availability increasingly influence construction sequencing. Artificial intelligence workload density accelerates hardware upgrades. The United States remains the primary contributor to the global market size.

Asia-Pacific Data Center Market Analysis:

In 2025, Asia Pacific generated USD 61.02 billion, contributing 22.60% to global market revenue, and is projected to grow to USD 69.45 billion in 2026. The region experienced higher growth that fueled demand for data center capacity globally, and is expected to continue, with total supply projected to increase from 11.1 GW in 2023 to 26.7 GW by 2028. The Japan market is estimated to reach USD 14.17 billion by 2026, the China market is estimated to reach USD 15.50 billion by 2026, and the India market is estimated to reach USD 11.49 billion by 2026. Furthermore, with a growing population and growing digital demands, Indonesia has become a key market. Major investments are being made to develop hyperscale data centers, particularly in Jakarta and Eastern Java. For instance,

In May 2024, Cisco Systems launched its first edge data centers to expand its security footprint in Indonesia. This facility helps customers in financial services and the public sector to align with local data regulations and compliance requirements.

Asia-Pacific exhibits the fastest incremental data center market growth due to digitalization and population scale. Hyperscale expansion across metropolitan corridors drives large-scale campus development. Regulatory diversity influences site selection strategies. Connectivity infrastructure and land availability vary significantly across markets. The region continues to increase its share of the global market.

Japan Data Center Market:

Japan’s data center market prioritizes seismic resilience and operational reliability. Enterprise modernization and cloud migration support steady demand. Space constraints in urban centers encourage efficient vertical design. Renewable energy integration remains a strategic focus. Japan maintains stable growth within the broader Asia-Pacific data center industry.

China Data Center Market:

China’s data center market is driven by domestic cloud providers and digital platform expansion. Government data localization policies reinforce in-country infrastructure deployment. Large-scale hyperscale campuses are concentrated in designated digital zones. Power sourcing and regulatory oversight influence development patterns. China contributes materially to the regional market growth.

Europe Data Center Market Analysis:

Europe is expected to grow at a robust CAGR over the coming years and has an extensive, advanced network infrastructure, including widespread fiber-optic networks and high-speed internet connectivity. Europe maintained a strong presence in the global market, reaching USD 68.98 billion in 2025, accounting for 25.60% share, and is expected to reach USD 76.6 billion in 2026. This ensures low latency and high-speed data transmission, which is crucial for modern applications, such as real-time data processing and cloud computing. Germany, Ireland, and the Netherlands host major data center hubs with cutting-edge technologies and high-performance computing capabilities, fostering innovation and supporting digital transformation initiatives. The region attracts substantial investments from global technology providers and local players, owing to its central location globally, which continuously drives the market growth. The UK market is estimated to reach USD 14.76 billion by 2026, and the German market is estimated to reach USD 14.17 billion by 2026. For instance,

In June 2023, IBM Corporation developed its first European Quantum Data Center facility in Ehningen, Germany. It is designed to match the requirements of companies, research institutions, and government agencies.

Europe emphasizes sustainability compliance and energy efficiency across the data center industry. Regulatory mandates drive renewable integration and carbon reporting transparency. Major markets prioritize Tier 3 and Tier 4 builds to support enterprise and hyperscale demand. Power pricing volatility affects operating cost structures. Europe maintains a stable but policy-influenced data center market growth trajectory.

Germany Data Center Market:

Germany’s data center market benefits from strong industrial demand and regulatory clarity. Frankfurt remains a key interconnection hub within continental Europe. Data sovereignty requirements and enterprise digitization support steady colocation absorption. Renewable procurement strategies influence development economics. Germany continues to represent a significant share of the regional market capacity.

United Kingdom Data Center Market:

The United Kingdom data center market remains anchored by London’s connectivity ecosystem. Hyperscale and financial services demand sustainable Tier 3 and Tier 4 investment. Planning regulations and grid capacity constraints affect expansion timelines. Edge deployment is increasing outside major hubs. The market demonstrates resilient absorption despite energy cost fluctuations.

Middle East & Africa Data Center Market Analysis:

The Middle East & Africa are expected to showcase noteworthy growth during the forecast period. Middle East & Africa recorded a market size of USD 22.74 billion in 2025, capturing 8.40% of the global market share, and is projected to reach USD 25.43 billion in 2026. The region is undergoing a significant digital transformation, which is enhancing economic development. Investments in data centers support this by providing critical infrastructure for AI, cloud computing, and IoT technologies. For instance, Microsoft’s new data centers in the UAE and South Africa are expected to create significant economic opportunities, including local innovation and job creation.

The Middle East and Africa data center market reflects early-stage but accelerating development. Digital government initiatives and cloud partnerships stimulate demand. Infrastructure concentration in key metropolitan hubs supports initial hyperscale entry. Power reliability and regulatory alignment remain development considerations. Long-term growth prospects align with regional digital transformation strategies.

Latin America Data Center Market Analysis:

Latin America’s data center market is expanding gradually, led by Brazil and Mexico. The Latin America market generated USD 13.17 billion in 2025, representing 4.90% of the global market landscape, and is expected to reach USD 14.49 billion in 2026. Enterprise digitization and regional cloud adoption drive colocation demand. Infrastructure modernization and connectivity improvements support incremental capacity additions. Currency volatility and energy costs influence investment pacing. The region represents an emerging opportunity within the global data center industry.

Moreover, the market in South America is increasing steadily, owing to the growing demand for digital transformation initiatives, cloud services, and the expansion of e-commerce and online services.

Data Center Industry Competitive Landscape

Top Companies Emphasize Partnerships to Uphold Their Supremacy in the Market

Leading companies are concentrating on intensifying their geographical presence globally by offering industry-specific solutions. Major players are focusing on mergers and acquisitions with local players tactically to maintain their command across regions. Key players are introducing novel services to boost their consumer base. They are continuously investing in R&D efforts for product improvements. Therefore, prominent companies are quickly applying these tactics to maintain their competitiveness in the market.

The data center industry is characterized by scale concentration, capital intensity, and long-term lease structures. Competitive positioning depends on geographic footprint, power availability, interconnection density, and operational efficiency. Market participants include hyperscale cloud providers, global colocation operators, regional data center platforms, and infrastructure-focused real estate investment entities.

Hyperscale cloud companies command a significant share of incremental capacity additions. Their vertically integrated models enable standardized design, bulk procurement, and renewable energy sourcing advantages. These operators prioritize multi-megawatt campus expansion and automation-driven operational optimization. Capital deployment strategies focus on scalability and predictable demand forecasting. Colocation providers compete through carrier-neutral ecosystems, dense cross-connect infrastructure, and flexible lease models. Portfolio diversification across multiple metropolitan regions reduces exposure to localized power constraints. Strategic acquisitions strengthen global footprint and expand customer ecosystems.

Regional operators focus on secondary markets and regulatory-aligned sovereign infrastructure. These firms emphasize customer proximity and compliance capabilities. Competitive differentiation often centers on service responsiveness and localized connectivity partnerships. Technology integration is increasingly central to competition. Advanced cooling systems, liquid immersion deployment, and high-density rack configurations support artificial intelligence workloads. Operators investing in power usage effectiveness optimization enhance margin resilience.

Barriers to entry remain high due to land acquisition complexity, grid interconnection timelines, and capital requirements. Long-term lease commitments and hyperscale partnerships create structural advantages for established players.

March 2024: Eaton announced the launch of a novel modular data center solution for enterprises looking to meet requirements for machine learning, artificial intelligence, and edge computing technologies.

January 2024: Equinix announced expansion of hyperscale capacity across secondary North American markets to address artificial intelligence workload demand, integrating high-density liquid cooling infrastructure and enhanced renewable energy procurement agreements.

April 2024: Microsoft initiated development of new hyperscale campuses in Europe to support sovereign cloud requirements, emphasizing low-carbon power sourcing and advanced data center infrastructure management integration.

September 2024: Amazon Web Services expanded multi-megawatt campus deployment in Asia-Pacific, incorporating modular construction techniques and high-capacity electrical systems to accelerate commissioning timelines.

February 2025: Digital Realty launched a high-density colocation facility optimized for artificial intelligence clusters, deploying advanced cooling containment systems and expanded interconnection platforms.

June 2025: Google Cloud announced long-term renewable energy procurement agreements aligned with new data center campus builds, integrating battery storage systems and improved power usage effectiveness optimization frameworks.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product/service types, and leading applications of the product. Besides, the report offers insights into the market trends and highlights key industry developments. In addition to the factors above, the report encompasses several factors that contributed to the growth of the market in recent years.

The global data center market size is projected to grow from USD 300.64 billion in 2026 to USD 699.13 billion by 2034, at a CAGR of 11.10% during the forecast period of 2026-2034.