Modular Data Center Market Size, Share & Industry Analysis, By Component (Solutions (Integrated All-in-One, IT Modules, Power Modules, and Cooling Modules) and Services), By Data Center Size (Small and Medium Data Center and Large Data Center), By Capacity (Below 250 kW, 250 kW to Below 1 MW, and 1 MW and Above), By Industry (BFSI, IT & Telecom, Government, Healthcare, Media & Entertainment, and Others), and Regional Forecast, 2026 – 2034

Modular Data Center Market Size & Outlook

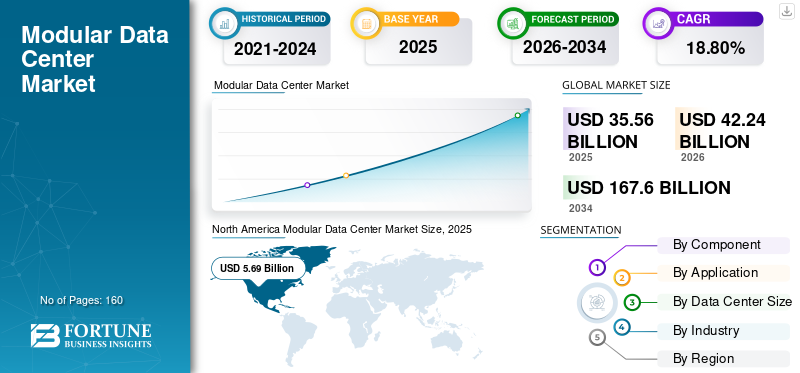

The global modular data center market size was valued at USD 31.24 billion in 2025. The market is projected to grow from USD 35.44 billion in 2026 to USD 116.53 billion by 2034, exhibiting a CAGR of 16.0% during the forecast period. North America dominated the modular data center market with a market share of 37.04% in 2025.

A modular data center is a prefabricated facility that integrates IT apparatus, data center energy supply, cooling, security, and monitoring systems into a standardized module. Modular data centers can be installed and enlarged faster than traditional data centers. The growing demand for cloud services and AI creates more interest in modular data centers, as they provide quicker installation, greater flexibility, and a less complex building process.

Key market players, such as Schneider Electric SE, Vertiv Holdings Co., Huawei Technologies Co., Ltd., Dell Technologies Inc., and Hewlett Packard Enterprise Development LP operating in the market, are focusing on developing new products, creating partnerships, and acquiring other companies in order to broaden their high density modules, boost their speed of implementation, position themselves effectively in regards to hyperscale, colocation, and AI-driven data center development.

Download Free sample to learn more about this report.

IMPACT OF GENERATIVE AI

Expansion of AI Infrastructure to Accelerate Industry Development

AI is driving demand for modular data center solutions due to the growing need for high-performance GPU clusters among companies and cloud service providers that require infrastructure that can be deployed quickly. Moreover, such computing systems function better when supported by a sufficient power supply, cooling supplied in liquid form, and advanced thermal management mechanisms, which has led to an increased need for integrated power and cooling solutions. Modular data centers also allow the step-by-step installation of AI-related solutions, while speeding up construction. For instance,

- In July 2024, Vertiv launched the MegaMod CoolChip, a prefabricated modular data center solution equipped with high-density liquid cooling for AI computing. This solution delivers AI-critical infrastructure up to 50% faster than conventional on-site construction.

MODULAR DATA CENTER MARKET TRENDS

Rising Focus on Development of Large-Scale Modular Campuses Fuels Market Growth

Modern modular data centers are transforming from tiny edge operations to multiple-megawatt campuses that perform hyperscale, colocation, AI, and high-performance computing tasks. Businesses can deploy modules containing standardized IT, power, and cooling components in stages, allowing them to install additional equipment in correspondence to the requirements of customers and the infrastructure. Since these modules are manufactured and tested beforehand, on-site construction is not complicated and creates the same working environment for a different number of locations. Thus, this approach enables quicker expansion and minimizes the risks associated with traditional construction. For instance,

- In August 2025, Vertiv launched Vertiv OneCore, a factory-assembled modular infrastructure solution that integrates power, thermal management, and IT systems for AI, HPC, and high-density data centers with capacities of 5 MW and above.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rapid Advances in Generative AI and High-Performance Computing Drive Market Growth

Rapid advances in generative AI, machine learning, and high-performance computing have led to a huge surge in demand for data centers that can handle multiple GPU clusters and execute parallel processing on a larger scale. This process requires more power distribution, network channels, and thermal management than conventional enterprise computing. Modular systems help operators to utilize factory-integrated units equipped with electrical power, liquid cooling, and containment systems. Therefore, the growing adoption of AI and HPC requests is driving demand for modular systems that are scalable and can be deployed quickly.

- For instance, in March 2025, Vertiv launched Vertiv SmartRun, a prefabricated modular overhead infrastructure system integrating high-density power distribution, liquid-cooling piping, hot-aisle containment, and network infrastructure.

|

Rank |

Market Drivers |

Overall Impact Rank |

CAGR Contribution (2026-2034) |

Impact 2026-2028 |

Impact 2029-2031 |

Impact 2032-2034 |

|

1 |

Rapid Expansion of AI and High-Performance Computing |

High |

+5.0% |

High |

High |

High |

|

2 |

Need for Faster Data Center Deployment |

High |

+4.3% |

High |

High |

High |

|

3 |

Growth of Hyperscale and Colocation Capacity |

High |

+3.7% |

High |

High |

High |

|

4 |

Increasing adoption of edge computing, 5G, IoT, and latency-sensitive applications |

Medium-High |

+3.0% |

Medium-High |

High |

High |

|

5 |

Growing preference for phased capacity expansion |

Medium |

+2.6% |

Medium-High |

High |

High |

|

6 |

Others (Expansion of cloud regions, Rising power and cooling requirements, etc.) |

Medium-Low |

+1.8% |

Medium |

Medium-High |

Medium |

|

Total Positive Growth Contribution |

+20.4% |

MARKET RESTRAINTS

Limited Power Availability and Grid Constraints May Hinder Market Growth

Modular data centers can be constructed and set up quickly, but their commissioning depends on the availability of sufficient and reliable electricity from local utility companies. A congested grid, limited substation capacity, and long interconnection approval processes can delay projects by years, diminishing the time-to-market advantages of modular construction. In addition, technologies such as artificial intelligence (AI) and high-density computing workloads further complicate the issue due to significantly higher power requirements, particularly at the rack level. Operators may need to invest in on-site power generation, battery storage, green energy, and additional grid infrastructure. Thus, low power availability can inhibit deployment and limit market expansion in power-constrained data center hubs.

|

Rank |

Market Restraints |

Overall Impact Rank |

Negative CAGR Contribution (2026-2034) |

Impact 2026-2028 |

Impact 2029-2031 |

Impact 2032-2034 |

|

1 |

Limited Power Availability and Grid Constraints |

High |

-0.7% |

High |

High |

Medium-High |

|

2 |

High Initial Investment Requirements |

High |

-1.0% |

High |

Medium-High |

Medium |

|

3 |

Transportation and Site-Integration Challenges |

Medium-High |

-1.2% |

High |

Medium-High |

Medium |

|

4 |

Others (Limited Customization of Standardized Modules, Shortage of Skilled Technical Personnel, etc.) |

Medium |

-1.5% |

Medium |

Medium |

Medium-Low |

|

Total Negative Growth Impact |

-4.4% |

MARKET OPPORTUNITIES

Expanding Digital Infrastructure in Emerging Economies Creates New Opportunities for Market Growth

Emerging economies in the Asia Pacific region, the Middle East, Africa, and Latin America are creating significant opportunities as a result of rising cloud adoption, digital government, and telecommunications, and data localization regulations. Modular data centers enable operators to quickly deploy capacity in areas where skilled construction labor, appropriate buildings, and established supply chains are scarce. Owing to their pre-manufactured and scalable designs, these centers also lower upfront costs, allowing operators to build capacity gradually as demand evolves. Thus, modular facilities are ideal for new cloud regions, telecom networks, government infrastructures, and local co-location hubs. For instance,

- In February 2026, Vertiv deployed its SmartMod Max DX prefabricated modular data center for a connectivity and managed services provider expanding across West Africa. The solution was delivered in 24 weeks, compared with the typical 52 to 72 weeks required for conventional construction.

Segmentation Analysis

By Component

Growing Investment in Integrated Infrastructure Strengthened Solutions Segment

Based on component, the market is categorized into solutions (integrated all-in-one, IT modules, power modules, and cooling modules) and services.

Solutions accounted for the largest market share in 2025. This is owing to high investments in integrated IT, power supply, cooling, enclosure, monitoring, and security infrastructure. Demand is also fueled by hyperscale, colocation, AI, and edge deployments relying on prefabricated and factory-tested systems for faster deployment and capacity expansion.

Services is anticipated to grow at the highest CAGR of 18.4% over the forecast period, driven by the rising adoption of modular data centers, increasing demand for consulting, system integration, installation, commissioning, maintenance, remote monitoring, and capacity expansion support.

By Data Center Size

Rising Investment by Hyperscale Facilities and Growing AI and High-density Computing Needs Strengthened Large Data Center Segment Growth

Based on data center size, the market is categorized into small and medium data center and large data center.

The large data center segment accounted for the largest market share in 2025 and is expected to grow at the highest CAGR of 17.1% during the forecast period. This is owing to the significant investments made by hyperscale cloud service providers, colocation suppliers, and telecommunications firms in the creation of multi-megawatt facilities. These facilities are utilizing standardized modules such as electrical power systems, cooling systems, and IT modules to accelerate deployment and meet the high-density AI workloads.

The small and medium data center segment is anticipated to grow at a moderate CAGR of 14.5% over the forecast period. This is owing to steady demand from enterprises, telecom operators, government agencies, and edge applications, although growth is partly offset by faster investment in large hyperscale and AI-focused facilities.

By Capacity

Rising Investments in Hyperscale and AI Data Centers Boosted 1 MW and Above Segment Growth

Based on capacity, the market is divided into below 250 kW, 250 kW to below 1 MW, and 1 MW and above.

The 1 MW and above segment accounted for the largest market share in 2025 and is expected to grow at the highest CAGR of 16.9% during the forecast period. This is owing to rising investments in hyperscale, colocation, cloud, and AI data centers requiring multi-megawatt computing capacity. Large modular deployments enable operators to integrate high-density power and cooling systems while expanding capacity through standardized and prefabricated infrastructure blocks.

The 250 kW to below 1 MW segment is anticipated to grow at a moderate CAGR of 15.8% over the forecast period. This is owing to steady demand from enterprises, telecom operators, government agencies, and regional edge facilities, while faster investment in multi-megawatt hyperscale and AI data centers limits its relative growth.

To know how our report can help streamline your business, Speak to Analyst

By Industry

Strong Investment in Cloud and Telecom Infrastructure Strengthened IT & Telecom Segment Growth

Based on industry, the market is classified into BFSI, IT & telecom, government, healthcare, media & entertainment, and others (manufacturing, retail, etc.).

IT & telecom held the dominant modular data center market share in 2025, as cloud service providers, telecommunication companies, colocation service providers, and internet service providers are investing heavily in on-demand computing. Growth in data traffic, the rollout of 5G technology, edge computing, and AI-related workloads also increased the need for modular data centers with integrated power, cooling systems, and network infrastructure.

The healthcare segment is anticipated to grow at the highest CAGR of 18.7% during the forecast period. This is owing to the expansion of digital health platforms, medical imaging, genomics, AI-enabled diagnostics, and electronic health records, which are increasing demand for secure, scalable, and rapidly deployable modular data center infrastructure.

Modular Data Center Market Regional Outlook

By geography, the market is categorized into North America, South America, Europe, the Middle East & Africa, and Asia Pacific.

North America

North America Modular Data Center Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest modular data center market share in 2024, valued at USD 10.40 billion, and also maintained its leading position, reaching USD 11.57 billion in 2025. The growth is owing to the availability of many hyperscale cloud vendors, colocation service providers, investments in AI infrastructure, and well-established data center supply chains across the region. As per Jones Lang LaSalle IP, Inc. (JLL) report 2025, North America had more than 35 GW of data center capacity under construction, of which 92% was already precommitted to satisfy the demand for modular infrastructure solutions.

- For instance, in April 2025, Eaton completed its USD 1.4 billion acquisition of Fibrebond, a Louisiana-based manufacturer of pre-integrated modular power enclosures, to strengthen its offerings for multi-tenant and hyperscale data center

U.S. Modular Data Center Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market is expected to reach around USD 10.62 billion in 2026, accounting for roughly 30.0% of global sales.

To know how our report can help streamline your business, Speak to Analyst

Europe

In Europe, the market is projected to record a growth rate of 14.6% during the forecast period, the fourth-highest among all regions. The market is expected to reach a valuation of USD 9.61 billion in 2026. The market in Europe is experiencing growth owing to the increasing requirements for cloud computing, artificial intelligence, colocation, and data sovereignty across the major and newer data center hubs. Factors such as issues related to grid and availability of construction space, sustainability considerations, and pressures to shorten time to market are forcing operators to adopt factory-built modules for power and cooling and IT infrastructure that can be deployed in phases.

- For instance, in June 2025, Schneider Electric launched its Prefabricated Modular EcoStruxure Pod Data Center, integrating high-power distribution, liquid cooling, containment, and high-density racks for AI and HPC clusters with capacities of 1 MW and above.

U.K. Modular Data Center Market

The U.K. market is estimated to reach around USD 2.15 billion in 2026, representing roughly 6.1% of global revenues.

Germany Modular Data Center Market

Germany’s market is projected to reach approximately USD 1.77 billion in 2026, equivalent to around 5.0% of global sales.

Asia Pacific

The Asia Pacific region is estimated to reach USD 9.68 billion in 2026 and is expected to grow at the highest CAGR of 20.4% during the forecast period. This is owing to rapid digital transformation, increased cloud adoption, and the widespread adoption of AI-driven collaborative tools in China, India, Japan, and South Korea. Moreover, demand for modular data center solutions continues to grow rapidly due to the expansion of the IT service sector, a growing remote workforce, and increased investment in enterprise AI platforms.

- For instance, in March 2026, Jones Lang LaSalle IP, Inc. (JLL) projected that Asia Pacific would add approximately 24 GW of data center capacity between 2025 and 2030, creating an estimated USD 286 billion in real estate value, which supports substantial demand for scalable modular infrastructure.

China Modular Data Center Market

China’s market is projected to be one of the largest worldwide. The market is expected to reach around USD 2.73 billion in 2026, representing roughly 7.7% of global sales. This is owing to the rapid expansion of cloud services, AI computing, 5G networks, and national computing infrastructure, which increases demand for scalable, energy-efficient, and quickly deployable data center capacity.

Japan Modular Data Center Market

The Japan market is estimated to reach around USD 1.93 billion in 2026, accounting for roughly 5.4% of global revenues.

India Modular Data Center Market

The Indian market is estimated to reach around USD 1.48 billion in 2026, accounting for roughly 4.2% of global revenues.

South America

South America is expected to witness moderate growth in this market during the forecast period. The South America market is set to reach a valuation of USD 1.44 billion in 2026. Modular data center market growth is owing to increasing adoption of cloud, colocation investment, data-localization requirements, and improved digital connectivity, which accelerate capacity expansion across Brazil, Chile, and Colombia, increasing demand for rapidly deployable and scalable infrastructure. In South America, Brazil is set to reach USD 0.73 billion in 2026.

Middle East & Africa

The Middle East & Africa region is estimated to reach USD 1.78 billion in 2026 and is expected to grow at a growth rate of 18.0% during the forecast period. This is owing to investments in sovereign cloud, Artificial Intelligence (AI), smart city initiatives, telecom modernization, and government-backed digital transformation efforts, particularly across the GCC and South Africa. In the Middle East & Africa, the GCC is set to reach USD 0.70 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Key Players Investing in Factory-Tested Data Center and Prefabricated Solutions to Support Faster Deployment

The global modular data center market holds a semi-consolidated structure, with prominent players such as Schneider Electric SE, Vertiv Holdings Co., Huawei Technologies Co., Ltd., Dell Technologies Inc., and Hewlett Packard Enterprise Development LP holding significant market positions. These companies are investing in prefabricated and factory-tested data center solutions that integrate IT systems, power distribution, liquid cooling, monitoring, and security infrastructure to support faster deployment, high-density AI workloads, and phased capacity expansion.

Other notable players in the global market include Eaton Corporation plc, Rittal GmbH & Co. KG, Delta Electronics, Inc., STULZ GmbH, and BladeRoom Group Limited. These companies are strengthening their market positions through product launches, strategic partnerships, acquisitions, manufacturing capacity expansion, and the development of customized modular solutions for hyperscale, colocation, edge, telecom, government, and enterprise applications, which are expected to accelerate market demand over the forecast period.

LIST OF KEY MODULAR DATA CENTER COMPANIES PROFILED

- Schneider Electric SE (France)

- Vertiv Holdings Co. (U.S.)

- Huawei Technologies Co., Ltd. (China)

- Dell Technologies Inc. (U.S.)

- Hewlett Packard Enterprise Development LP (U.S.)

- Eaton Corporation plc (Ireland)

- Rittal GmbH & Co. KG (Germany)

- Delta Electronics, Inc. (Taiwan)

- STULZ GmbH (Germany)

- BladeRoom Group Limited (U.K.)

KEY INDUSTRY DEVELOPMENTS

- June 2026: Delta Electronics launched a prefabricated AI modular data center solution at COMPUTEX 2026 for high-density and megawatt-scale computing environments. The factory-integrated solution is designed to reduce data center deployment time by up to 60%.

- March 2026: Rittal and Siemens entered into a strategic partnership to develop standardized and energy-efficient power distribution infrastructure for AI and modular data centers. The initial developments include a scalable sidecar power rack and low-voltage distribution systems for modular and containerized facilities.

- June 2025: Eaton partnered with Siemens Energy to develop standardized modular data centers integrated with on-site power generation. The collaboration combines Eaton’s skidded electrical infrastructure with Siemens Energy’s modular power plants to reduce deployment timelines and address grid-connection constraints.

- June 2024: Hewlett Packard Enterprise partnered with Danfoss to develop energy-efficient modular data centers that recover and reuse excess heat. The offering combines HPE’s modular data center architecture with Danfoss heat exchangers, compressors, chillers, and heat-reuse modules, improving cooling efficiency by up to 30%.

- May 2024: Dell Technologies launched the PowerEdge R670 and R770 CSP Edition servers, marking the introduction of the Data Center Modular Hardware System architecture within its PowerEdge portfolio.

REPORT COVERAGE

The global modular data center market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, pipeline candidates, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, and key industry developments. The global market research report also provides a detailed competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 16.0% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Component, Data Center Size, Capacity, Industry, and Region |

| By Component |

|

| By Data Center Size |

|

| By Capacity |

|

| By Industry |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 31.24 billion in 2025 and is projected to reach USD 116.53 billion by 2034.

The market is growing at a CAGR of 16.0% during the forecast period.

In 2025, the market value stood at USD 11.57 billion.

By capacity, the 1 MW and above segment is expected to lead the market.

Rapid expansion of AI and high-performance computing are the key factors driving market growth.

Schneider Electric SE, Vertiv Holdings Co., Huawei Technologies Co., Ltd., Dell Technologies Inc., and Hewlett Packard Enterprise Development LP are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us