Managed Services Market Size, Share & Industry Analysis, By Service Type (Managed IT Infrastructure & Data Center Services, Managed Network Services, Managed Mobility Services, Managed Communication & Collaboration Services, Managed Information Services, Managed Security Services, Managed Backup & Recovery Services and Others), By Enterprise Type (SMEs and Large Enterprises), By Industry (BFSI, IT & Telecom, Government, Retail & E-commerce, Energy & Utility, Healthcare, Manufacturing, and Others), and Regional Forecast, 2026-2034

Managed Services Market Size & Industry Overview

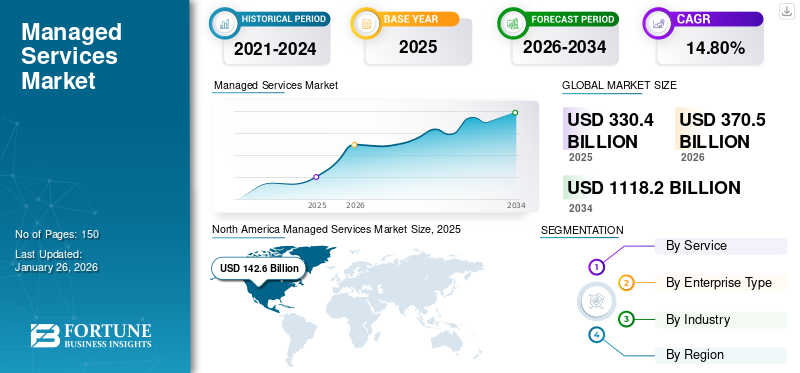

The global managed services market size was valued at USD 330.4 billion in 2025 and is projected to grow from USD 370.5 billion in 2026 to USD 1118.2

billion by 2034, exhibiting a CAGR of 14.80% during the forecast period. North America dominated the managed services industry with a market share of 43.20% in 2025. This growth is driven by enterprises increasingly outsourcing IT operations, strengthening cybersecurity postures, modernizing infrastructure, and optimizing multi-cloud environments to enhance service reliability, performance visibility, and long-term technology cost efficiency supporting steady expansion of the global managed services market.

This report studies services offered by market players, such as Atos SE, which offers managed detection & response services and managed security services. Similarly, Fujitsu offers managed infrastructure services & multi-cloud managed services, and Capgemini SE offers application-managed & professional services, managed public cloud services, and many other solutions.

The global market is driven by the rising adoption of these services among enterprises in various sectors, such as IT & telecommunications, BFSI, and healthcare, among others. Enterprises are implementing these services in their business units to digitize their business processes, upgrade and innovate their infrastructure, and enhance productivity and scalability. Moreover, businesses around the world are shifting toward cloud computing and embracing managed IT services to reduce their infrastructure expenditure. Professional and managed services assist businesses in keeping up with the rapid digital transformation in a more efficient manner. Market participants are concentrating on introducing cutting-edge managed services for enterprises to capture a substantial portion of this promising market.

- In April 2023, Aeries Technology launched cybersecurity managed services for enterprises to meet the regulations and compliance framework. The company is offering significant support to firms in their digital transformation with a safe and secured infrastructure.

The global managed services market covers recurring outsourcing contracts for IT infrastructure, networks, cloud platforms, workplace applications, and security operations. Organizations rely on managed service providers to deliver continuous monitoring, lifecycle support, and performance optimization across complex hybrid technology environments.

Several forces shape this expansion. Enterprise digital transformation initiatives accelerate the replacement of legacy systems and drive demand for workload migration, hybrid cloud governance, and automated configuration. Persistent cybersecurity threats increase requirements for managed detection and response, zero-trust enforcement, and vulnerability monitoring. Distributed workforces place additional pressure on networks, identity management, and collaboration platforms, reinforcing demand for managed endpoint and communication services.

Organizations favor predictable operating expenditure models that shift responsibility for availability, patching, and incident resolution to trusted providers. This shift enables internal teams to focus on innovation initiatives rather than routine maintenance tasks. Buyers evaluate managed services based on service-level guarantees, security maturity, automation depth, and industry-specific compliance capabilities.

Large enterprises account for a significant share of spending due to multi-site operations and complex regulatory requirements. However, small and medium-sized enterprises represent an important growth segment because they often lack internal staffing capacity and seek modular, scalable services.

Competitive intensity remains high. Capabilities increasingly differentiate providers, including AI-driven workflow automation, cloud-native service delivery, resilience engineering, and unified observability. Providers that demonstrate measurable performance improvements, transparency in cost models, and smooth integration with existing systems gain a strategic advantage.

The COVID-19 pandemic impacted the world economy and forced many enterprises to implement spending cuts and contingency plans in the short term. However, the adoption of cloud-based solutions, Artificial Intelligence (AI), security solutions, and Big Data surged considerably during this period. This growth allowed cloud giants to switch their services to deal with the increased load. MSPs adopted the new norms of working remotely to curb the virus spread, which further helped the market grow.

Download Free sample to learn more about this report.

Managed Services Market Key Takeaways

- 2025 Market Size: USD 330.4 billion

- 2026 Market Size: USD 370.5 billion

- 2034 Forecast Market Size: USD 1118.2 billion

- CAGR: 14.80% from 2026–2034

- North America dominated the managed services market with a 43.20% share in 2025.

- The managed network services segment is expected to account for 20.01% of the market in 2026.

- The large enterprises segment is projected to hold 68.88% of the total market share in 2026.

North America

North America led the global market with a valuation of USD 142.6 billion in 2025.

Asia Pacific

Asia Pacific accounted for USD 74.1 billion in 2025, representing 22.40% of global revenue.

Europe

Europe generated USD 63.2 billion in 2025, capturing 19.10% of the global market.

U.S.

The managed services market is projected to reach USD 106.8 billion by 2026.

Japan

The managed services market is projected to reach USD 18.8 billion by 2026.

Read More

Managed Services Market Trends

Increasing Adoption of Cloud-based Managed Security Services MSPS will Contribute to Market Growth.

The increasing adoption of cloud-based services is a major global trend. The rising demand for securing IT infrastructure against cyber threats has pushed organizations to adopt Managed Security Services (MSSs) in their business models. Cyber threats are evolving in both enterprises and government sectors, thus forcing MSPs to develop advanced offerings that can detect and address cyber risks. Various companies are focused on adopting cloud-based managed security services to boost their security against various email viruses, Distributed Denial of Service (DDOS) attacks, and firewall intrusions. Key players are offering advanced cloud-based security services to cater to rising security needs. For instance,

- In May 2023, Ireland-based Ernst & Young Global Limited introduced managed security services for small and medium-sized enterprises facing cyberattack challenges. The company aims to offer cost-effective services to secure cloud-based infrastructure and modern tools.

The adoption of managed security services enables various organizations to handle an incident, monitor & manage ongoing cybersecurity risks, and detect threats. Therefore, the demand for cloud-based services will grow in the forthcoming years.

Organizations increasingly deploy AI-enabled automation tools to reduce manual intervention, accelerate incident response, and improve system observability. Predictive analytics enhances capacity planning and security threat prevention. Cloud-native managed services expand rapidly as enterprises shift application workloads to container orchestration platforms and serverless environments.

Hybrid work and device proliferation push demand for managed endpoint, identity, and collaboration services. Zero-trust security architectures spread across industries, driving the integration of identity governance, micro-segmentation, and continuous authentication within managed offerings.

Managed detection and response adoption accelerates as organizations seek stronger cybersecurity resilience. Automation of vulnerability management, log analytics, and configuration enforcement becomes standard within service portfolios. Service contracts increasingly incorporate business outcome metrics rather than simple uptime thresholds. Organizations measure provider value through cost optimization, compliance reporting quality, and reduced mean time to resolution.

Commercial models evolve toward tiered subscription models and service bundling aligned with vertical requirements. Industry-specific managed services emerge in healthcare, financial services, and manufacturing, addressing regulatory, privacy, and operational constraints. Partnerships between cloud platforms, security vendors, and managed providers deepen integration and expand ecosystem reach.

Download Free sample to learn more about this report.

Market Drivers

Growing Adoption of Bring Your Own Device (BYOD) Among Organizations to Aid Market Growth

Bring Your Own Device (BYOD) is one of the primary components of digital technology and productivity across various sectors in the current technology-driven business environment. Using a BYOD program enables employees to use their own devices for work purposes, leading to cost savings and increased flexibility for organizations. Syntonic reports that 87% of businesses depend on their employees’ personal mobile devices to access company apps.

The increased use of BYOD has increased the number of intelligent devices in the workplace, such as tablets, smartphones, laptops, and other gadgets. This would raise the risk of data integrity and security as the data moves across smart devices. As a result, many companies are turning to these services to monitor the security of these smart devices, thereby promoting the managed services market growth in the forthcoming years.

The managed services industry expands as enterprises transition from traditional on-premises infrastructure toward hybrid and multi-cloud environments. Increasing interdependencies among applications, networks, and data platforms raise operational complexity. Many organizations cannot maintain in-house expertise across all technology domains, prompting outsourcing to managed service providers offering scalable resources and specialized skills. Escalating cybersecurity risks represent a major catalyst. Attack surfaces widen as organizations deploy connected devices, remote access channels, and distributed workloads. Managed security services provide continuous threat detection, incident response, and compliance oversight, reducing exposure to breaches and financial loss.

Predictable operating expenditure models also motivate adoption. Outsourcing routine management and support functions converts capital expenditures into recurring service contracts, enabling organizations to modernize without large upfront investments. Performance guarantees and measurable service-level commitments support business continuity planning and risk management strategies.

Workforce constraints reinforce demand for managed services. IT talent shortages in areas such as cloud automation, cybersecurity, and data management limit internal capacity for modernization initiatives. Managed service providers deliver access to skilled professionals, toolsets, and automation platforms that accelerate transformation timelines.

Digital transformation programs require resilient infrastructure, consistent security enforcement, and continuous monitoring. Managed services allow organizations to sustain modernization momentum while optimizing operational efficiency and resource allocation. As these drivers compound, recurring demand strengthens through the forecast period.

RESTRAINING FACTORS

Lack of IT Security Professionals May Hamper Market Growth

The lack of availability of IT and cybersecurity professionals is one of the major limitations to the growth of this market. This factor can hinder organizations’ ability to meet their IT security needs. A lack of valued IT security skills can leave organizations open to cyberattacks, resulting in data loss and reputation damage. With the growth of several cybersecurity threats, the requirement for advanced security solutions to deal with cyberattacks is growing exponentially. This highlights the need for cybersecurity training to help close the skills gap, introduce new talent to the workforce, and make the organization more secure.

Moreover, many limitations, such as the demand for experienced professionals, ineffectiveness of the managed service model, data privacy & security issues, and requirement for large investments, are projected to hinder the market’s growth.

Despite strong growth, several structural restraints temper adoption in the managed services market. Concerns over loss of control remain prevalent among organizations with sensitive data or mission-critical systems. Decision makers may hesitate to relinquish operational oversight to external service providers, particularly where outsourcing intersects with regulatory mandates or national data-sovereignty requirements. Integration complexity also limits uptake. Legacy systems, proprietary applications, and fragmented architectures complicate managed services onboarding efforts, increasing the risk of disruption during transition phases.

Cost uncertainty presents another restraint. While managed services offer predictable operating expenses, hidden charges can surface when contracts require service adjustments, custom integrations, or expanded capacity. Organizations seek transparent pricing models and strong governance frameworks to mitigate such risks.

Vendor lock-in concerns affect decision-making, particularly in multi-cloud environments where organizations aim to maintain portability and negotiation leverage. Long-term dependency on a single provider may create commercial or operational constraints if performance degrades or strategic alignment shifts.

Inconsistencies in service delivery quality further challenge adoption. Providers vary widely in automation maturity, response times, and compliance readiness. Organizations often require rigorous due diligence and service-level benchmarking to confirm provider capability. Economic uncertainty may delay IT modernization timelines, slowing project approvals and deferring outsourcing decisions in certain industry verticals.

Market Opportunities

Expanding regulatory requirements and escalating cyber threats create high-value opportunities across the managed services market. Providers delivering security-centric services with measurable compliance outcomes gain a competitive advantage, particularly in financial services, healthcare, and energy sectors. Managed detection and response, identity management, encryption, and governance frameworks support rising enterprise risk-management priorities.

Small and medium-sized enterprises represent a substantial addressable market. Many lack dedicated IT teams and seek modular, consumption-based services to reduce operating expenses and improve resilience. Providers offering simplified onboarding, automated workflows, and transparent pricing capture adoption within this segment.

Cloud modernization initiatives continue to generate demand for migration, multi-cloud optimization, and workload governance. Opportunities expand in managed Kubernetes and container services as organizations adopt cloud-native architectures for performance and scalability.

Edge computing emerges as another frontier opportunity. Distributed edge nodes require continuous monitoring, lifecycle management, and secure integration with core applications. Managed edge services can extend provider portfolios and differentiate capabilities.

Industry-focused offerings deliver growth potential where regulatory oversight and operational complexity are high. Providers with deep vertical expertise can command premium pricing through tailored security controls, compliance reporting, and process automation aligned to sector requirements.

Managed Services Market Segmentation Analysis

Segmentation in the managed services market reflects shifting enterprise priorities, modernization drivers, and varying operating models across industries. Buyers are increasingly selecting providers based on their service automation maturity, cybersecurity integration, and ability to support hybrid and multi-cloud environments. The segmentation below examines service adoption rationale, demand characteristics, and expected developments through the forecast period.

By Service Type Analysis

Rapid Growth in Technological Infrastructure to Boost Demand for Managed IT Infrastructure & Data Center Services

Based on service type, the market is classified into managed IT infrastructure & data center, managed network services, managed mobility, managed communication & collaboration, managed information, managed security, managed backup & recovery, and others.

Managed IT Infrastructure & Data Center Services

The managed network services segment is expected to represent 20.01% of the market share in 2026. Investing in IT incurs substantial operating expenses, so companies outsource IT services as managed service providers operate with fixed monthly rates and help reduce capital cost expenditure for managing systems in-house. Also, the managed service model allows companies to minimize downtime by providing proactive maintenance and monitoring, and effective solutions for IT support and infrastructure management.

Managed IT infrastructure and data center services form the foundation of the market. Providers deliver lifecycle management for compute, storage, and virtualization layers across on-premises, colocation, private cloud, and hybrid deployments. These services address uptime, capacity planning, configuration consistency, and remote monitoring. Infrastructure management evolves toward software-defined automation, predictive maintenance, and AI-assisted orchestration tools that reduce manual effort.

Organizations modernize legacy assets gradually, often through co-managed hybrid partnerships rather than full outsourcing. Data center modernization initiatives expand demand for workload migration, platform upgrades, and optimized hosting architectures.

Reliability remains a primary driver, especially in industries requiring strict service continuity. Infrastructure complexity grows as enterprises integrate container platforms, distributed architectures, and edge nodes, creating a long-term need for expert support. Providers differentiate through automation depth, compliance alignment, and service-level guarantees linked to workload performance.

Managed Network Services

Managed network services cover WAN, LAN, wireless, SD-WAN configuration, and connectivity performance assurance. Adoption accelerates as organizations support distributed workforces, cloud connectivity, and performance-sensitive applications. Modern managed network offerings integrate intelligent routing, machine-assisted fault detection, and network telemetry analytics. Organizations seek consistent policy enforcement and traffic visibility across hybrid networks.

Network modernization creates sustained service demand. MPLS replacement, edge routing upgrades, and SD-WAN rollouts require managed orchestration and lifecycle support. As networks converge with security, identity, and application performance management, providers offering unified service models gain stronger competitive positioning.

Managed Mobility Services

Managed mobility services support employee mobile devices, endpoint security, and lifecycle operations. Growth stems from hybrid workforce models, device proliferation, and security risk tied to unmanaged endpoints. Providers deliver mobile device enrollment, identity management integration, and remote patch and policy enforcement.

Organizations often use managed mobility to standardize device fleets, reduce helpdesk burden, and strengthen compliance posture. Automation of onboarding workflows and self-service enrollment increases scalability. Providers expand capabilities to include mobile threat defense and endpoint detection and response as security expectations rise.

Managed Communication & Collaboration Services

This segment supports unified communications, telephony, video conferencing, messaging platforms, and collaboration applications. Hybrid and remote work expand demand significantly as enterprises require reliable, scalable communication platforms integrated with identity and access controls. Providers deliver onboarding, configuration, license optimization, and performance monitoring.

Organizations evaluate managed collaboration services based on user experience metrics, adoption programs, and integration maturity across productivity applications. Service delivery shifts toward analytics-driven optimization and proactive incident prevention to maintain workforce productivity.

Managed Information Services

Managed information services encompass application support, data lifecycle oversight, managed analytics platforms, and business process outsourcing. Adoption grows as enterprises digitize workflows and migrate legacy applications to modern architectures. Providers deliver application performance monitoring, dependency mapping, and release management integrated with ITSM platforms.

Increased data volumes and compliance requirements create demand for managed governance, retention, and archival services. Providers expand capabilities to include observability tooling, API management, and workflow automation aligned to digital transformation priorities.

Managed Security Services

Managed security is estimated to showcase the highest CAGR during the forecast period, as managed security service providers provide ongoing threat intelligence to keep defenses up to date and protect businesses against emerging threats. Additionally, MSSPs can help companies avoid the costs associated with data breaches, such as legal fees, fines, and reputational damage.

Managed Backup & Recovery Services

Managed backup and recovery services address business continuity and resilience priorities. Providers oversee backup scheduling, air-gapped storage integration, encryption, and rapid restoration workflows. Demand rises as ransomware and data-integrity risk escalate.

Modern offerings integrate automated policy enforcement, immutable storage, and hybrid cloud replication. Organizations focus on recovery point and recovery time objectives, requiring coordinated response across infrastructure and application layers. Lifecycle modernization of backup environments drives recurring service demand.

By Enterprise Type Analysis

Adoption of Managed Services Rises Among Large Enterprises to Improve Scalability

Based on enterprise type, the market is divided into SMEs and large enterprises.

Large Enterprises

The large enterprises segment is projected to account for 68.88% of the total market share in 2026. Managed services help large enterprises in proactive monitoring, improve scalability, and provide specialized expertise. Also, MSSP helps in managing and analyzing the financial requirements through financial reporting, bookkeeping services, and more.

Large enterprises represent the dominant revenue share due to expansive application portfolios, hybrid infrastructure, and complex regulatory requirements. Providers deliver co-managed service frameworks integrating automation platforms, service orchestration, and centralized governance.

Large enterprise adoption reflects a shift from transactional outsourcing toward strategic managed partnerships, emphasizing transformation outcomes, integrated risk management, and business-aligned service-level agreements.

Small and Medium-Sized Enterprises (SMEs)

SMEs are expected to grow with the highest CAGR during the forecast period. Managed service providers help SMEs to manage their IT infrastructure, including data backup and recovery, network management, cybersecurity, and software updates. Also, helps to improve productivity by providing access to the latest technology and tools, ongoing support & maintenance.

SMEs increasingly adopt managed services to access enterprise-grade capabilities at predictable cost levels. Skills shortages and limited capital budgets constrain in-house modernization capacity. Providers offer modular, scalable bundles aligned to SME requirements, including managed endpoint support, network monitoring, security services, and collaboration platform administration.

SME adoption patterns emphasize cost transparency, simplified onboarding, automation-driven support, and shared service models. Providers invest in self-service portals, standardized service catalogs, and remote resolution capabilities to deliver affordable service margins.

By Industry Analysis

To know how our report can help streamline your business, Speak to Analyst

Early Adoption of Advanced Technologies to Propel Product Usage in the IT & Telecom Sector

Based on industry, the market is divided into BFSI, IT & telecom, government, retail & e-commerce, energy & utility, healthcare, manufacturing, and others (education, travel, and more).

IT & Telecom

The IT and telecom industry segment is anticipated to account for 18.01% of the market share in 2026. The increased need for these services to manage and maintain highly complex IT infrastructures is expected to fuel the segment’s market growth during the forecast period. IT and telecom organizations adopt managed network, infrastructure, and application services to support automation, network transformation, and service reliability requirements.

Banking, Financial Services, and Insurance (BFSI)

The BFSI segment is estimated to be the fastest-growing segment over the forecast period. Businesses in this sector require a sophisticated IT infrastructure to preserve and manage data, ranging from trading instruments to record-keeping, reporting & computation, and others. IT services are critical to the success of financial transactions that require the exchange of information with customers or internal employees.

BFSI institutions outsource managed security, identity management, core-system performance, and compliance workflows to reduce operational and regulatory risk. Managed services support resilience objectives and faster response to threat activity.

Furthermore, the BFSI sector faces numerous cybersecurity threats due to the sensitive nature of financial data. Managed security services offer proactive monitoring, threat detection, and incident response, thereby minimizing the risk of breaches and ensuring regulatory compliance, such as GDPR or HIPAA.

Government

Government demand centers on secure cloud enablement, identity governance, and modernization of legacy systems while adhering to strict compliance frameworks and procurement controls.

Retail & E-commerce

The retail & e-commerce segment is set to showcase steady growth, considering the robust increase in online customers and shopping. Retailers rely on managed services for omnichannel platform availability, point-of-sale security, and peak-traffic performance.

Energy & Utility

Energy and utility operators delegate operational technology security, asset monitoring, and metering infrastructure support to managed service providers.

Healthcare

Healthcare organizations outsource managed applications, identity access, and endpoint security to safeguard patient data and maintain regulatory compliance. In addition, the healthcare and manufacturing segments are predicted to witness a significant increase in their CAGR. The rise in usage of IoT solutions in different applications, such as patient service, automated surgeries, nanotechnology, and others, is driving the segment’s growth.

Manufacturing

Manufacturers integrate managed services into smart factory systems, endpoint protection, and industrial control environments.

MANAGED SERVICES MARKET REGIONAL INSIGHTS

Geographically, the market is classified across five major regions - North America, Europe, Asia Pacific, the Middle East & Africa, and South America.

North America Managed Services Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America Managed Services Industry Analysis

The managed services industry in North America is expected to dominate the managed services market share in terms of revenue. The market’s growth in this region is mainly due to the robust presence of many MSPs, such as IBM Corporation, Accenture, and Cognizant, among others. The managed services industry in the U.S. holds a majority share of the North American market owing to the rising adoption of these services among small and medium-sized enterprises and the provision of substantial IT budgets. Thus, key players in this market are focused on merger and acquisition strategies to prevent cybersecurity breaches. The U.S. market is projected to reach USD 106.8 billion by 2026. In 2025, North America held 43.20% of the global market share, reaching a valuation of USD 142.6 billion, and is projected to grow to USD 157.1 billion in 2026.

North America maintains significant managed services adoption driven by complex enterprise IT environments and modernization needs. Organizations embrace co-managed models for infrastructure, cloud, and cybersecurity functions. Market maturity deepens as service automation and AI operations platforms improve performance visibility. Regulatory scrutiny and increasing threat levels reinforce investment in managed security and compliance services. The region demonstrates steady long-term service contract renewals.

The United States represents the largest share of the regional managed services market due to expansive enterprise technology footprints and ongoing cloud transformation programs. Organizations pursue managed services to improve resilience, reduce internal burden, and accelerate modernization. Providers integrate automation and unified observability for scalable service delivery. Government, energy, and financial sectors maintain strong spending supported by cybersecurity and compliance priorities across critical systems and infrastructure.

Europe

Europe demonstrates growing managed services penetration as organizations modernize infrastructure while complying with evolving data-protection mandates. Cloud adoption and hybrid workplace demands generate requirements for managed network and identity services. Security posture improvement remains central to outsourcing decisions. Providers emphasize service localization, audit readiness, and governance integration. Multi-year service contracts support digital transformation, though procurement complexity and regulatory oversight extend evaluation cycles in several industries. The UK market is projected to reach USD 16 billion by 2026, while the Germany market is projected to reach USD 12.8 billion by 2026. The market in Europe reached USD 63.2 billion in 2025, representing 19.10% of total market revenue, and is projected to reach USD 67.9 billion in 2026.

Asia-Pacific Managed Services Industry Analysis

The managed services industry in the Asia Pacific is expected to record the highest CAGR during the forecast period. The regional market’s strong growth is owing to the increasing investments in data security and the rising adoption of cloud-based solutions among several organizations. Growing economies, such as China, India, Singapore, Australia, and New Zealand, provide massive opportunities to adopt these managed outsourcing services. Besides, various other service providers in this region are developing an integrated cloud storage platform for sectors such as retail, BFSI, manufacturing, and others. Additionally, the Indian government's continuous investments in physical infrastructures, such as smart cities, are anticipated to generate opportunities for implementing managed services, such as data storage, security, and network management in the nation. The Japan market is projected to reach USD 18.8 billion by 2026, the China market is projected to reach USD 32.9 billion by 2026, and the India market is projected to reach USD 17.9 billion by 2026. Asia Pacific contributed approximately USD 74.1 billion to the global market in 2025, accounting for 22.40% share, and is expected to reach USD 87.9 billion in 2026.

Asia-Pacific demonstrates the fastest managed services market expansion as organizations modernize digital infrastructure and invest in cloud adoption. Rapid enterprise growth increases demand for scalable managed network and security capabilities. Hybrid cloud deployment across evolving regulatory frameworks drives co-managed governance requirements. Providers develop regional service hubs and automation platforms to meet performance expectations. Expanding manufacturing and financial services sectors reinforce recurring spending on managed services contracts.

Japan adopts managed services to modernize aging IT environments and support productivity improvement initiatives. Organizations emphasize reliability, operational continuity, and secure remote access. Service demand spans managed security, infrastructure performance, and automation of routine tasks. Providers must deliver strong documentation, lifecycle support, and service transparency aligned to local expectations. Workforce constraints and modernization programs accelerate ongoing migration toward managed operational models in critical sectors.

China’s managed services expansion aligns with digital transformation, cloud adoption, and investment in industrial modernization. Organizations migrate workloads to hybrid environments, requiring coordinated governance and security oversight. Managed network, infrastructure, and threat monitoring services see rising demand. Providers integrate automation and centralized orchestration to scale service delivery. Regulatory constraints and data localization requirements influence outsourcing models and provider selection across the enterprise and government sectors.

Europe Managed Services Industry Analysis

The managed services industry in Europe holds a significant position in this market. The growth of the regional market is owing to the rising adoption of cloud platforms and the high demand for managing confidential enterprise data. The managed services industry in Germany, the U.K., and France is expected to showcase strong growth opportunities in the region, considering the increasing number of small and medium-sized enterprises and their investments in advanced technologies.

Europe demonstrates growing managed services penetration as organizations modernize infrastructure while complying with evolving data-protection mandates. Cloud adoption and hybrid workplace demands generate requirements for managed network and identity services. Security posture improvement remains central to outsourcing decisions. Providers emphasize service localization, audit readiness, and governance integration. Multi-year service contracts support digital transformation, though procurement complexity and regulatory oversight extend evaluation cycles in several industries.

Germany’s managed services adoption aligns with industrial modernization priorities. Manufacturers pursue managed infrastructure and network resilience to support automation initiatives. Organizations require strict privacy, documentation, and integration standards for mission-critical workloads. Providers offering co-managed governance, strong security capabilities, and reliable service levels gain an advantage. Migrating legacy automation and operational systems toward connected platforms reinforces demand for long-term managed support and regulatory alignment across industrial environments.

The United Kingdom’s managed services growth is supported by cloud migration initiatives, modernization of legacy IT estates, and tightening cybersecurity requirements. Financial services, government, and healthcare organizations depend on managed identity, network, and compliance services. Providers focus on automation, resilient operations, and cost optimization. Skills shortages in security, cloud engineering, and workload automation strengthen demand for trusted outsourcing partners with proven service delivery maturity.

Latin America and Middle East & Africa Managed Services Industry Analysis

Latin America’s managed services market develops steadily as enterprises modernize networks and adopt cloud platforms. Organizations prioritize outsourcing to reduce operational burdens and address skills shortages. Managed security and infrastructure services experience rising demand across energy, banking, and government sectors. Economic cycles influence procurement decisions, but critical modernization initiatives progress. Providers offering flexible pricing, strong support, and automated service delivery capabilities strengthen competitive positioning. In 2025, Latin America generated USD 27.8 billion, contributing 8.40% to global market revenue, and is projected to grow to USD 31 billion in 2026.

Middle East & Africa

The Middle East & Africa region shows growing managed services as energy, utilities, and government sectors digitalize operations. Security incidents and workforce constraints catalyze outsourcing for cybersecurity, network resilience, and identity services. Infrastructure modernization and smart city initiatives fuel adoption. Service providers with regional delivery capacity and automation maturity capture long-term contracts supporting modernization goals across distributed operating environments. The Middle East & Africa region captured 6.90% of the global market in 2025, generating USD 22.7 billion in revenue, and is projected to reach USD 26.5 billion in 2026.

This growth is due to the increasing ICT spending, rising government initiatives, growing trend of big data & analytics, and technological advancements in these regions. For instance, the governments of GCC countries are focusing on pursuing pioneering national development projects, such as the UAE’s Vision 2021 and Saudi Arabia’s Vision 2030. These projects will help improve cloud-based services and boost economic diversification through the expansion of IT infrastructures. This is expected to boost the growth of the market in these regions during the forecast period.

Competitive Landscape

Leading Market Players Are Focusing On Strengthening Their Market Positions

Companies operating in the market are focusing on offering services that drive business growth and enhance customer experience. The services offered by these companies are easy to deploy and operate. These services drive efficiency, enhance customer experience, and pave the way for innovation on next-generation network services. Also, the key players in the market are keen on offering innovative services to support the adoption of various technological infrastructures and digital transformation. Through strategic partnerships and collaborations, key market players are expanding their global presence.

- April 2023 - VMware, Inc. launched VMware Cross-Cloud managed services to help customers and partners expand their services and practices in a secured multi-cloud environment. It will also help enterprises accelerate their digital transformation with the implementation of a smart cloud strategy.

- April 2023 – Sinch AB announced its strategic collaboration with Microsoft Teams and Synoptek to provide managed and professional services. The company will offer voice services for Teams using Operator Connect, which enables users to make calls to anyone and anywhere.

The competitive landscape reflects a diverse ecosystem of global technology firms, regional service providers, and specialist managed security organizations. Competition intensifies around automation maturity, platform integration depth, and the ability to deliver consistent outcomes across hybrid and multi-cloud environments. Larger providers leverage broad service portfolios, standardized operating models, and automation frameworks to scale delivery. Their strengths include service orchestration, proactive monitoring, governance alignment, and structured lifecycle management.

Regional providers differentiate through responsiveness, localized expertise, and tailored service bundling. They target mid-sized enterprises requiring co-managed models and direct engagement. Niche specialists focus on managed detection and response, identity governance, and cloud-native workload protection. These providers compete through advanced analytics and rapid response capabilities.

Service convergence increases competition. Network, cloud, and security domains merge through shared telemetry, automation workflows, and centralized orchestration dashboards. Providers that unify cross-domain observability improve efficiency and incident response. Contract structures evolve toward consumption-based pricing, outcome alignment, and measurable service-level commitments tied to risk and performance indicators.

Mergers and acquisitions continue as providers expand capabilities, diversify portfolios, and gain regional market access. Investments in security operations centers, automation platforms, and AI-driven analytics strengthen competitive positioning. Providers increasingly collaborate with software and hardware vendors to embed integrated toolsets, improving service automation and reducing operational friction.

Organizations evaluate providers through criteria including service reliability, transparency, automation depth, compliance readiness, and resilience engineering practices. Providers demonstrating measurable improvements in risk reduction, cost efficiency, and system performance gain market share. Workforce training, documentation quality, and onboarding experience influence customer retention. The competitive landscape remains dynamic, shaped by modernization requirements, regulatory oversight, and the acceleration of cybersecurity threats.

List of Top Managed Services Companies:

- IBM Corporation (U.S.)

- Accenture plc (Ireland)

- Fujitsu Ltd. (Japan)

- Microsoft Corporation (U.S.)

- NTT DATA Corporation (Japan)

- Amazon Inc. (U.S.)

- DXC Technology (U.S.)

- Tata Communication Services Limited (India)

- Capgemini SE (France)

- Atos SE (France)

Managed Services Industry Key Developments:

- March 2025: NTT DATA was named a Global Managed Service Provider in the SAP PartnerEdge “Run” Program. Through this, NTT DATA now delivers managed services for RISE with SAP, GROW with SAP, and SAP Business AI, strengthening its role as a global partner for enterprise cloud transformation.

- March 2025: Globalgig introduced Premier SSE Management, a managed Secure Service Edge solution built on Palo Alto Networks Prisma Access. The service combines 24/7 SOC support with network intelligence from its Orchestra Insight platform to improve threat detection and security operations.

- May 2025: EY launched its Integrated Finance Managed Service based on SAP S/4HANA Cloud. The new service applies automation and cloud technologies across finance, HR, treasury, payroll, and tax functions, helping companies modernize and scale back-office operations.

- February 2025: First Focus, an Australian managed services provider, acquired Tie Networks, a South Australian–based communications company. The deal broadens First Focus’s offerings in unified communications and strengthens its local market position.

- October 2023 – Logicalis, a technology services provider, introduced an Intelligent Connectivity suite. This suite comprised solutions, such as SASE, SSE, SD-WAN, and Private 5G, all powered by Cisco Systems, Inc. With this suite, Logicalis’ customers could easily access digitally managed services supported by the Logicalis Digital Fabric Platform and developed using Cisco technology.

- September 2023 – Cloud5 Communications, a provider of communication and technology solutions, introduced its new division for managed services. This division aims to cater to the IT needs and challenges of different industries, including hospitality, student housing, and senior living. By offering assistance in managing IT operations, technology infrastructures, and security, this division will help consumers streamline their processes effectively.

REPORT COVERAGE

The research report provides an in-depth managed services market analysis. It focuses on key aspects, such as leading companies, top end-users, and prominent product applications. Besides this, it offers insights into the latest market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several key factors that have contributed to the market's growth in recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021–2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021–2024 |

|

Growth Rate |

CAGR of 43.20% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Service Type

|

|

By Enterprise Type

|

|

|

By Industry

|

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value is expected to reach USD 1118.2 billion by 2034.

Fortune Business Insights says that the market size was valued at USD 330.4 billion in 2025.

The market is expected to record a CAGR of 14.80% during the forecast period of 2026-2034.

Based on service, the IT managed services segment is expected to lead the market during the forecast period.

The growing adoption of Bring Your Own Device (BYOD) system among organizations is one of the key drivers for this market’s growth.

IBM Corporation, Accenture plc, Fujitsu Ltd., Microsoft Corporation, NTT DATA Corporation, Amazon Inc., and DXC Technology are the top companies in the market.

The IT & telecom segment is expected to hold the major market share.

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us