Metal Recycling Market Size, Share & Industry Analysis, By Metal Type (Ferrous Metals and Non-ferrous Metals), By End-use Industry (Building & Construction, Automotive, Electrical & Electronics, Packaging, and Others), and Regional Forecast, 2026-2034

METAL RECYCLING MARKET SIZE and FUTURE OUTLOOK

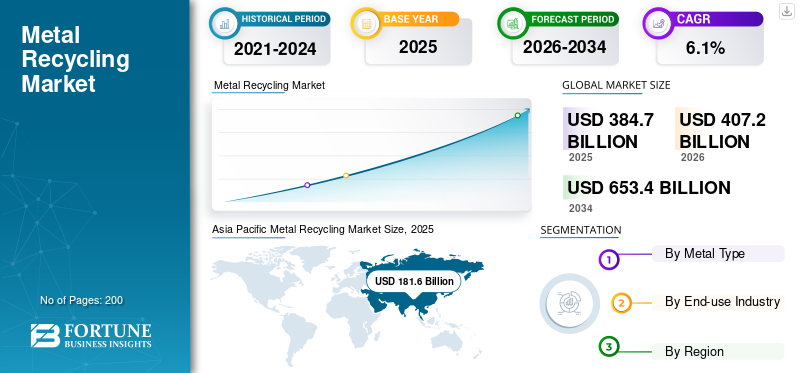

The global metal recycling market size was valued at USD 384.7 billion in 2025. The market is projected to grow from USD 407.2 billion in 2026 to USD 653.4 billion by 2034 at a CAGR of 6.1% during the forecast period. Asia Pacific dominated the metal recycling market with a market share of 47.21% in 2025.

The metal recycling market comprises the collection, sorting, processing, and reuse of ferrous and non-ferrous metal scrap generated from end-of-life products, industrial waste, construction debris, vehicles, packaging, electrical equipment, machinery, and other sources containing metal.

The global market is growing due to rising demand for low-carbon secondary metals across building & construction, automotive, packaging, electrical & electronics, and industrial applications. Growth is also supported by increased scrap-based steelmaking, strong aluminum and copper recycling demand, expanding circular-economy policies, and manufacturers’ efforts to reduce dependence on virgin ore extraction and lower carbon emissions.

Key players in the market include Sims Limited, Radius Recycling, Inc., European Metal Recycling Ltd., Aurubis AG, and Nucor Corporation.

Download Free sample to learn more about this report.

METAL RECYCLING MARKET TRENDS

Shift Toward Scrap-Based Steelmaking, and Circular Manufacturing to Shape Market Growth

A major trend in the global market is the shift from conventional waste recovery toward circular production systems. Steelmakers, aluminum producers, automotive companies, packaging manufacturers, and electrical equipment producers are increasingly using recycled metals to reduce energy intensity and improve raw-material security. This trend is particularly strong in steel, where scrap-based electric arc furnace production is gaining importance as companies seek lower-carbon alternatives to ore-based steelmaking. USGS states that iron and steel scrap is used with pig iron and direct-reduced iron to produce steel products for construction, containers, machinery, oil & gas, transportation, appliances, and other industries.

At the same time, non-ferrous recycling is gaining strategic importance due to rising demand for aluminum and copper across lightweight vehicles, electrical systems, packaging, buildings, renewable energy, and electronics.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Demand for Low-Carbon Secondary Metals Across End-use Industries to Drive Market Growth

One of the strongest drivers for the metal recycling market growth is the growing use of recycled steel, aluminum, copper, lead, zinc, and other industrial non-ferrous metals across construction, automotive, packaging, electrical & electronics, and industrial end-use industries. Recycled metals help reduce dependence on virgin ore extraction and support manufacturers in meeting sustainability, circularity, and carbon-reduction targets. This is especially important for steel and aluminum, where secondary metal use can significantly reduce energy consumption compared with primary production.

This driver is further supported by the expansion of scrap-intensive steelmaking and rising demand for recycled aluminum and copper. Ferrous scrap remains the largest recycled metal stream globally, while aluminum and copper contribute significantly to market value due to their higher unit prices and broad downstream use. Aluminum recycling supports beverage cans, automotive parts, building products, and consumer goods, while copper recycling supports wiring, power transmission, electronics, electrical equipment, and building systems.

MARKET RESTRAINTS

Scrap Quality Variation, Contamination, and Informal Collection Networks to Restrict Market Growth

A major market restraint is the inconsistent quality of scrap metal. Scrap streams often include mixed alloys, coatings, plastics, rubber, oils, paints, insulation, and other contaminants, which increase sorting and processing costs. This issue is particularly important in non-ferrous recycling, where metal purity directly affects pricing, recovery yield, and downstream usability. Poorly sorted scrap can reduce the value of recovered metal and limit its use in high-quality end-use industries.

Collection infrastructure also remains uneven across regions. Developed markets including Europe, North America, Japan, and South Korea have mature scrap collection and processing systems. In contrast, many emerging markets still depend on informal collection networks and lower levels of automated sorting. This restricts the supply of clean, traceable, and specification-grade scrap, thereby reducing the value captured from available end-of-life metal products.

MARKET OPPORTUNITIES

Expansion of EAF Steelmaking, Urban Mining, and Recycled-Content Demand to Create Growth Opportunities

A major market opportunity is the expansion of electric arc furnace steelmaking, which relies heavily on ferrous scrap. As steel producers move toward lower-emission production methods, demand for clean, high-quality steel scrap is expected to increase. This creates opportunities for scrap processors, shredders, sorters, and recyclers that can supply consistent material to steelmakers.

Another important opportunity lies in urban mining and recovery of non-ferrous metals from vehicles, buildings, electrical infrastructure, industrial equipment, and electronic waste. Copper and aluminum recovery are especially attractive as both metals have high value and strong demand from electrification, renewable energy, construction, transport, and packaging. The International Copper Association refers to copper contained in end-use stocks as an “urban mine,” indicating the long-term recovery potential from products already in use.

MARKET CHALLENGES

Price Volatility, Trade Restrictions, and Rising Processing Costs Challenge Market Growth

A major challenge for the market is the volatility of scrap metal prices. Prices of ferrous and non-ferrous scrap are closely linked to global steel, aluminum, copper, zinc, nickel, and energy markets. When primary metal prices decline or industrial demand weakens, scrap prices can fall rapidly, affecting recycler margins and inventory values. This creates financial pressure, especially for companies holding large scrap inventories.

Trade restrictions and export controls also create market uncertainty. Several countries increasingly view scrap as a strategic domestic raw material for green steel, aluminum production, and industrial decarbonization. While this can support domestic recycling investment, it can also disrupt global scrap flows and create regional price differences. At the same time, recyclers face higher costs related to labor, energy, environmental compliance, and investment in advanced sorting technology.

RESEARCH AND DEVELOPMENT (R&D) TRENDS

R&D in the global market is increasingly focused on advanced sorting, sensor-based separation, robotics, artificial intelligence, and improved purification technologies. These innovations help recyclers identify different alloys, separate ferrous and non-ferrous metals more efficiently, and improve recovery rates from complex scrap streams, including automotive shredder residue, mixed industrial scrap, e-waste, and end-of-life appliances.

Innovation is also moving toward closed-loop recycling systems, especially in the aluminum, automotive, packaging, and electronics end-use industries. Producers are increasingly working to recover high-quality process scrap and post-consumer scrap for reuse in similar end-use industries. This supports circular manufacturing and helps downstream customers increase recycled content while maintaining material performance.

SEGMENTATION ANALYSIS

By Metal Type

Ferrous Metals Dominate Due to Large Steel Scrap and Strong Consumption Across Construction, Transportation, and Machinery

Based on metal type, the market is segmented into ferrous metals and non-ferrous metals.

The ferrous metals segment holds the dominant metal recycling market share. Its dominance is mainly supported by the large volume of iron and steel scrap generated from construction, automotive, machinery, appliances, containers, and industrial equipment. USGS states that iron and steel scrap is used to produce steel products for appliances, construction, containers, machinery, oil & gas, transportation, and other consumer industries.

The non-ferrous metals segment accounts for a significant share, with a 5.8% CAGR during the forecast period. Aluminum and copper are the key contributors, supported by demand from packaging, construction, automotive, electrical systems, electronics, and industrial end-use industries.

By End-use Industry

To know how our report can help streamline your business, Speak to Analyst

Building & Construction Leads Due to High Use of Recycled Steel, Aluminum, Copper, and Zinc in Infrastructure and Building Systems

Based on end-use industry, the market is segmented into building & construction, automotive, electrical & electronics, packaging, and others.

The building & construction segment holds the leading share of the global market. The dominance is supported by extensive use of recycled steel in structural frames, reinforcement bars, bridges, and infrastructure, along with recycled aluminum and copper in windows, facades, wiring, plumbing, roofing, and HVAC systems. Worldsteel and USGS data both indicate the strong linkage between steel consumption and construction-related applications.

The automotive segment holds a significant share due to the recycling of end-of-life vehicles, steel body structures, aluminum components, copper wiring, lead-acid batteries, and other metal parts.

Packaging segment growth is supported mainly by aluminum and steel cans, closures, containers, and food and beverage packaging. The segment is expected to grow at a CAGR of 5.1% during the forecast period.

Others segment include industrial machinery, appliances, oil & gas equipment, shipbuilding, rail, and consumer goods.

METAL RECYCLING MARKET REGIONAL OUTLOOK

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Metal Recycling Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific holds the dominant share of the global market. The region leads due to its large steelmaking base, expanding manufacturing sector, strong construction activity, growing automotive production, and rising use of aluminum and copper across electrical, packaging, and industrial applications. China remains the largest contributor, supported by its large steel, aluminum, construction, automotive, and electronics industries.

China Metal Recycling Market

China’s market is one of the largest markets globally, with 2025 revenue valued at USD 96.3 billion, representing roughly 25.0% of global sales.

To know how our report can help streamline your business, Speak to Analyst

North America

North America accounted for a significant share of the global market. The region is supported by a mature scrap recycling ecosystem, strong automotive recycling, large construction and industrial scrap streams, and established aluminum can and steel recycling infrastructure. USGS states that iron and steel scrap is an important raw material in the U.S. steel industry and is used in products across construction, containers, machinery, oil & gas, transportation, and appliances.

U.S. Metal Recycling Market

In 2025, the U.S. market was valued at USD 62.4 billion, driven primarily by strong demand from the industrial sector. The U.S. accounts for roughly 16.2% of global market sales.

Europe

Europe registers significant growth during the forecast period. The region remains important due to its mature recycling infrastructure, circular-economy policies, strong automotive and construction industries, and advanced scrap-sorting and recovery systems. Europe also benefits from strong aluminum, copper, and steel recycling networks, supported by regulatory pressure to reduce waste and increase the use of secondary raw materials.

Germany Metal Recycling Market

The German market was valued at around USD 22.6 billion in 2025, representing roughly 5.9% of global market revenues.

U.K. Metal Recycling Market

The U.K. market was valued at around USD 11.9 billion in 2025, representing roughly 3.1% of global market revenues.

Latin America

The Latin America region’s growth is supported by steel, aluminum, copper, automotive, packaging, and construction-related recycling demand. Brazil and Mexico are the leading markets due to their relatively larger industrial bases, automotive production, construction activity, and scrap-processing networks.

Brazil Metal Recycling Market

Brazil’s market was valued at around USD 8.5 billion in 2025, representing roughly 2.2% of global market revenues.

Middle East & Africa

The Middle East & Africa region’s growth is supported by construction, infrastructure, energy, industrial equipment, and growing steel and aluminum demand. GCC countries lead the regional market due to infrastructure investments, industrial diversification, and aluminum and steel activity, while South Africa remains an important recycling market in Africa.

GCC Metal Recycling Market

The GCC market was valued at around USD 10.6 billion in 2025, representing roughly 2.8% of global market revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Key Players are Strengthening Scrap Processing Networks, Low-carbon Metal Production, and Circular Supply Chains to Defend their Market Positions

Competitive intensity in the global market is shaped by scrap sourcing scale, collection networks, processing capacity, sorting technology, downstream steel and non-ferrous metal integration, and the ability to supply clean secondary raw materials. Market leadership is increasingly tied to companies that can secure large scrap volumes, improve recovery yields, invest in advanced separation technologies, and align recycled-metal supply with low-carbon steel, aluminum, copper, and industrial manufacturing demand.

LIST OF KEY METAL RECYCLING COMPANIES PROFILED IN REPORT

- Sims Limited (Australia)

- Radius Recycling, Inc. (U.S.)

- European Metal Recycling Ltd. (U.K.)

- Aurubis AG (Germany)

- Nucor Corporation (U.S.)

- Commercial Metals Company (U.S.)

- ArcelorMittal S.A. (Luxembourg)

- Tata Steel Limited (India)

- Kuusakoski Group Oy (Finland)

- DOWA Holdings Co., Ltd. (Japan)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Tata Steel inaugurated its first scrap-based electric arc furnace facility at Hi-Tech Valley, Ludhiana, India. The plant is designed to use 100% steel scrap and achieve CO₂ emissions of less than 0.3 per ton of steel, strengthening the company’s low-carbon and circular steelmaking position.

- December 2025: Radius Recycling reported that it recycled 4.9 million metric tons of ferrous and non-ferrous metals and sold 509,000 tons of low-carbon emission finished steel products in its 2024 Sustainability Report, reinforcing its integrated recycling and steelmaking model.

REPORT COVERAGE

The global metal recycling market report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, type, and end-use industry. In addition, it offers insights into the market and current industry trends, and highlights key developments. In addition to the factors mentioned above, the report also covers several factors contributing to market growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Growth Rate | CAGR of 6.1% from 2026 to 2034 |

| Segmentation | By Metal Type, By End-use Industry, and By Region |

| By Metal Type |

|

| By End-use Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 384.7 billion in 2025 and is projected to reach USD 653.4 billion by 2034.

Recording a CAGR of 6.1%, the market is slated to exhibit steady growth during the forecast period of 2026-2034.

The building & construction segment leads the market during the forecast period.

Asia Pacific held the highest market share in 2025.

Rising demand for low-carbon secondary metals across end-use industries is expected to drive market growth.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us