Photoelectric Sensors Market Size, Share & Industry Analysis, By Type (Retroreflective, Thru-Beam, and Diffused), By Light Source (Laser Beam, Infrared, and LED), By Range (Less than 300 mm, 300 mm to 1,000 mm, 1,001 mm to 10,000 mm, and More than 10,000 mm), By End-User (Consumer Electronics, Industrial Manufacturing, Food and Beverages, Automotive and Transportation, Building Automation, and Others), and Regional Forecast, 2026 - 2034

PHOTOELECTRIC SENSORS MARKET OVERVIEW AND FUTURE OUTLOOK

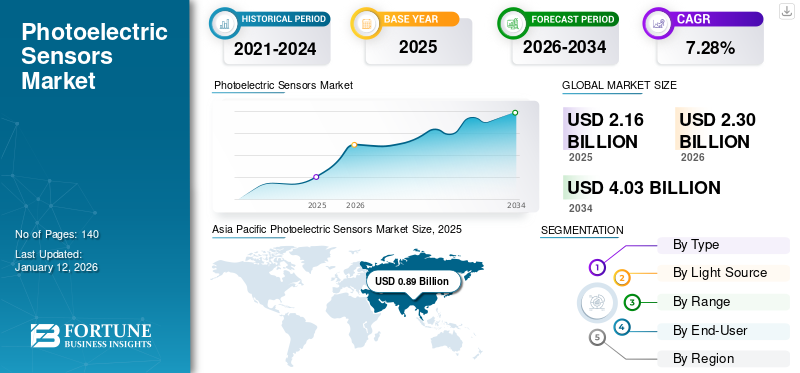

The global photoelectric sensors market size was valued at USD 2.16 billion in 2025 and is projected to grow from USD 2.30 billion in 2026 to USD 4.03 billion by 2034, exhibiting a CAGR of 7.28% during the forecast period. Asia Pacific dominated the market with a share of 41.05% in 2025.

A photoelectric sensor is a device designed to sense the presence or absence of objects and measure distance by utilizing the principles of light reflection. These sensors are employed in various industries for applications such as contour and edge detection, film thickness measurement, collision avoidance, safety monitoring, human detection, and height and level assessment. Their use enhances efficiency and precision across different sectors.

The demand for photoelectric sensors is rising as a result of advancements in automation across numerous industries. The surged adoption of industrial robots along with the rise of smart technologies, and the Industrial Internet of Things (IIoT), is also driving market growth. Incorporating sensors into manufacturing systems allows data evaluation and real-time tracking while improving operational efficacy. As per IoT analytics, the global count of connected Internet of Things (IoT) devices increased by 13% in 2024, reaching 18.8 billion, and is projected to reach around 40 billion by 2030.

Major players operating in the market include Keyence Corporation, Schneider Electric, SICK AG, Rockwell Automation Inc., and Tri-Tronics, and others. These companies are at the forefront of the photoelectric sensors market, shaping its growth and technological advancements through continuous innovation and strategic expansion.

The COVID-19 pandemic negatively impacted the market due to disruptions in global supply chain operations. The market is experiencing a speedy recovery, driven by renewed demand for automation, a rise in IIoT adoption, and developments in photonic technologies.

Download Free sample to learn more about this report.

Photoelectric Sensors Market KEY TAKEAWAYS

- 2025 Market Size: USD 2.16 billion

- 2026 Market Size: USD 2.30 billion

- 2034 Forecast Market Size: USD 4.03 billion

- CAGR: 7.28% from 2026–2034

- Asia Pacific dominated the photoelectric sensors market with a 41.05% share in 2025.

- The retroreflective segment is expected to account for the largest market share of 50.60% in 2026.

- The infrared segment is projected to capture 39.98% of the market share in 2026.

Asia Pacific

Asia Pacific held a 41.05% market share in 2025, valued at USD 0.89 billion, and is projected to reach USD 0.94 billion in 2026.

Asia Pacific

Europe accounted for USD 0.45 billion in 2025 and is expected to grow to USD 0.48 billion in 2026.

North America

North America generated USD 0.66 billion in 2025 and is projected to reach USD 0.71 billion in 2026.

U.S.

U.S. The market is projected to reach USD 0.53 billion by 2026.

Japan

Japan The market is expected to attain a valuation of USD 0.21 billion by 2026.

Read More

IMPACT OF GENERATIVE AI

Integration of Generative AI with Photoelectric Sensors by Enhancing Capabilities to Fuel Market Growth

Generative AI is poised to revolutionize sensor technology through automation, predictive analytics, and integration with advanced computational platforms such as across photonic chips. These developments will expand the scope of photoelectric sensors in industrial, environmental, and IoT applications while improving efficiency and promoting sustainability.

MARKET DYNAMICS

Photoelectric Sensors Market Trends

Increased Smart Manufacturing Practices to Emerge as a Key Market Trend

The global market is experiencing a significant shift with the adoption of smart manufacturing technologies. This transformation enables the integration of advanced systems, such as the IoT, AI, and automation, to enhance production efficiency. In this scenario, precise photoelectric sensors play an essential role in detection and measurement systems for real-time surveillance. As more manufacturers are adopting these innovative practices, the demand for these sensors is expected to rise, further driving market growth. Leading companies such as Siemens and Bosch are incorporating photoelectric sensors into their smart manufacturing systems to improve operational performance, minimized downtime, and maximized productivity.

Market Drivers

Rising Industrial Automation to Aid Market Growth

The increasing incorporation of smart automation and advanced technologies across industries has made industrial automation a key driving factor in the market. These sensors are important in manufacturing and assembly processes that offer accurate object detection. Furthermore, these sensors play an important role in automated packaging systems by guaranteeing accurate product alignment, label application, and package detection. According to the International Federation of Robotics, worldwide industrial robot sales rose by 7% in 2023, underscoring the increasing dependence on automation. With these compelling factors driving market growth, the photoelectric sensors market is posed for significant expansion in the upcoming years.

Market Restraints

High Maintenance Costs to Hinder Market Expansion

High upkeep expenses associated with photoelectric sensors are obstructing market expansion. Substantial funds are needed to maintain these advanced technologies effectively. Implementing sensor-driven automation systems demand significant financial outlays, including the cost of acquiring hardware, integrating it with current machinery, and developing software for efficient management and data analysis. Furthermore, the availability of alternative sensor technologies could restrict uptake and slow the growth of the global photoelectric sensors market throughout the forecast period.

Market Opportunities

Growing Automation Needs to Create Lucrative Market Opportunities

The food and beverage industry relies on several key elements, including tracking and monitoring objects, maintaining product quality, and ensuring safety during the packaging process. Additionally, there is growing demand for sensors capable of handling loads on conveyor belts, accurately detecting the positions of loaded carts, and maintaining cleanliness. The escalating demand for packaging solutions in this industry has boosted productivity, thereby driving the need for advanced smart sensors in manufacturing environments.

SEGMENTATION Analysis

By Type

Rising Need for Affordable Sensing Option Boosted Retroreflective Segment Growth

Based on type, the market is segmented into retroreflective, thru-beam, and diffused.

In terms of share, the retroreflective segment is set to dominate the market in 2026 at 50.60%, owing to its affordability compared to other photoelectric sensor types. The rising need for industrial automation and greater use of nanotechnology are also contributing to the increasing popularity of retroreflective in the market.

The thru-beam segment is anticipated to experience the highest compound annual growth rate (CAGR) during the forecast period, attributed to its extensive sensing range and enhanced accuracy in object detection. These sensors consist of separate transmitter and receiver units that form a direct light beam, enabling reliable detection over greater distances.

By Light Source

Laser Beam Segment Dominated due to its Applications

Based on light source, the market is segmented into laser beam, infrared, and LED.

The laser beam segment captured the highest revenue in 2025, driven by an increase in the use of laser beam source photoelectric sensors in the market. These sensors generate extremely small and highly precise laser spots that can detect minuscule objects. Moreover, since they do not require reflectors, laser beams offer greater installation and require less upkeep. As a result, their use is expanding across applications such as plant management, security, and surveillance, contributing significantly to market expansion.

The Infrared segment is expected to capture 39.98% of the market share in 2026.

The LED segment is anticipated to register the highest CAGR of 9.84% during the forecast period, driven by its energy efficiency, long lifespan, and versatility in applications. LED technology has been widely adopted in industries such as automotive, consumer electronics, and industrial automation. These sectors often integrate LED-based systems into sensors and devices due to their precision and reliability.

By Range

Rising Support for Small-scale Application Boosted Less Than 300 mm Segment Growth

Based on range, the market is segmented into less than 300 mm, 300 mm to 1,000 mm, 1,001 mm to 10,000 mm, and more than 10,000 mm. In terms of share, the less than 300 mm segment lead the market in 2026. The segment is poised to hold 33.74% of the market share. This segment is important for certain applications that require highly accurate detection in confined spaces, including semiconductor manufacturing and small-scale automation. It plays a key role in enabling precision-driven processes within industries that demand elevated levels of accuracy in restricted environments.

The 1,001 to 10,000 mm segment is anticipated to register the highest CAGR of 10.92% during the forecast period. The growth of this segment can be linked to the rising need for photoelectric sensors ranging from 1,001 to 10,000 mm across different end-use industries. These sensors are capable of detecting both long-range and short-range objects, regardless of their materials. Moreover, this category of sensors is both compact and budget-friendly, further contributing to its growing adoption.

By End-User

Consumer Electronics Segment Dominated Due to Integration of Smart Devices

Based on end-user, the market is categorized into consumer electronics, industrial manufacturing, food and beverages, automotive and transportation, building automation, and others.

In terms of share, the consumer electronics segment dominated the market in 2024. Photoelectric sensors are widely used in devices such as tablets, smartphones, smartwatches, and cameras. They enable real-time data monitoring and control, enhancing device functionality and user experience. Automated systems in consumer electronics, such as doors and gates in elevators or garages also rely on these sensors for precise operation. The segment is anticipated to gain 27.54% of the market share in 2026.

The automotive and transportation segment is expected to record the highest CAGR of 10.39% during the forecast period due to the rise in global automotive production, enhancing logistics, and increasing adoption of autonomous vehicles. Additionally, the integration of photoelectric sensors into smart cities and infrastructure further supports the growth of this segment.

To know how our report can help streamline your business, Speak to Analyst

PHOTOELECTRIC SENSORS MARKET REGIONAL OUTLOOK

Asia Pacific

Asia Pacific Photoelectric Sensors Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific recorded a market size of USD 0.89 billion in 2025, capturing 41.05% of the global market share, and is projected to reach USD 0.94 billion in 2026. The expansion of the region can be linked to the presence of major market players, swift advancements in industrialization, the growing implementation of IIoT across various industrial facilities, and the quick adoption of advanced technologies aimed at enhancing safety requirements. Additional contributing factors include the strong development of the automotive sector, heightened research and development efforts, increasing awareness of advanced technologies, strict government regulatory policies, and the rising application of nanotechnology, all of which create significant opportunities for the photoelectric sensors market growth.

Download Free sample to learn more about this report.

China's industry expansion is largely due to significant investments in automation and smart manufacturing technologies, enhancing productivity in industries such as automotive and electronics. China is estimated to acquire USD 0.33 billion in 2026. Government initiatives aimed at upgrading industrial processes and encouraging technological progress also play a significant role in strengthening the market. India is likely to gain USD 0.13 billion in 2026, while Japan is set to grow with a valuation of USD 0.21 billion in the same year.

To know how our report can help streamline your business, Speak to Analyst

South America

The market for photoelectric sensors in South America is experiencing steady growth due to recent shifts in the local economy and enhanced government funding for research initiatives. As automation continues to gain traction across various industries in South America, the need for dependable and efficient photoelectric sensors is anticipated to grow at a constant pace. Latin America accounted for USD 0.07 billion in 2025, representing 3.09% of the global market share, and is projected to reach USD 0.07 billion in 2026.

Europe

The Europe market accounted for USD 0.45 billion in 2025, representing 20.93% of the global industry, and is expected to reach USD 0.48 billion in 2026. The region is estimated to grow at the highest rate during the forecast period due to growing investments in cutting-edge technology, supportive government regulations, the rising application of nanotechnology, and heightened awareness of safety protocols. The U.K. market continues to grow, projected to reach a value of USD 0.10 billion in 2026. European nations such as Spain, the U.K., France, Germany, and Italy play a significant role in generating revenue for the market in this area. Leading companies in the region are focusing on expanding their product portfolios through various strategic methods. Germany is set to be valued at USD 0.10 billion in 2026, while France is poised to stand at USD 0.06 billion in 2025.

Middle East and Africa

The Middle East & Africa market generated USD 0.09 billion in 2025, representing 4.27% of the global market landscape, and is expected to reach USD 0.1 billion in 2026. The region holds a smaller photoelectric sensors market share. However, latest technological developments and increased funding to embrace smart manufacturing practices will create business opportunities in the future. The GCC market is foreseen to hold USD 0.04 billion in 2025.

North America

In 2025, North America generated USD 0.66 billion, contributing 30.66% to global market revenue, and is projected to grow to USD 0.71 billion in 2026. The market for photoelectric sensors in this region is witnessing substantial growth opportunities, driven by improvements in technology and a strong focus on automation. These factors are propelling digital transformation and attracting significant investments. The increasing need for these sensors is linked to their use in personal protective equipment, packaging machinery, robotics, and conveyor belts.

The U.S. is strengthening its market position through innovation. Leaders in the industry are creating auto-adjusting solutions for a variety of applications. Multispectral photoelectric sensors offer detection capabilities based on color and material type for manufacturers. Some manufacturing facilities are utilizing AI to enhance sensor functionalities. The U.S. market is poised to reach USD 0.53 billion in 2026.

Competitive Landscape

KEY INDUSTRY PLAYERS

Companies Concentrate on Introducing Innovative Products to Gain Strong Foothold

Industry participants are offering photoelectric sensors for enhancing sensing quality and efficiency by identifying objects without direct contact, thereby ensuring a longer operating life. Moreover, these leading firms are planning to expand their activities by acquiring domestic businesses. In addition, significant investments, collaborating, acquisitions, and mergers will propel product demand.

List of Key Photoelectric Sensors Companies Profiled:

- Keyence Corporation (Japan)

- Schneider Electric (France)

- SICK AG (Germany)

- Rockwell Automation Inc. (U.S.)

- Tri-Tronics (U.S.)

- Pepperl+Fuchs (Germany)

- Banner Engineering (U.S.)

- Panasonic Corporation (Japan)

- SENSATEC Co., Ltd. (Japan)

- OMRON Corporation (Japan)

- Balluff Inc. (Germany)

- ifm electronic GmbH (Germany)

- Eaton Corporation plc (Ireland)

- HTM Sensors (U.S.)

- Fargo Controls (U.S.)

- Leuze electronic Pvt. Ltd. (India)

- CNTD Electric Technology Co., Ltd. (China)

- Wenglor sensoric (Germany)

- PMP Automation Pvt Ltd (India)

- Dexerials Corporation (Japan)

KEY INDUSTRY DEVELOPMENTS:

- May 2024: Hikrobot launched its latest Machine Vision Photoelectric Sensors for different distance detection uses in India. These sensors are designed to facilitate a broader spectrum of applications across various sectors.

- December 2023: Mouser Electronics, Inc. revealed a distribution partnership with Panasonic Industrial Automation. As part of this agreement, Mouser would provide Panasonic’s range of integrated solutions tailored for diverse automation sectors, including automotive, semiconductor, packaging, and biomedical. Panasonic Industrial Automation boasts a comprehensive array of technologically sophisticated products, including the EX-10 ultra-slim photoelectric sensors, which are now accessible at Mouser.

- August 2023: Pepperl+Fuchs SE launched the R202 Series Cubic Photoelectric Sensors tailored for material handling. The R202 series introduces a fresh range of photoelectric sensors in a cubic shape from Pepperl+Fuchs. These sensors feature a red light LED and offer a straightforward switching function with two output options, concentrating on fundamental capabilities.

- August 2022: Rockwell Automation introduced new budget-friendly photoelectric sensors for a variety of global applications. The Allen‑Bradley 42EA RightSight S18 and 42JA VisiSight M20A sensors provide cost-effective and user-friendly sensing solutions with multiple sensing modes, versatile mounting options, and features suited for global operations.

- April 2022: Pepperl+Fuchs SE launched the M18 Series of cylindrical photoelectric sensors, featuring five operational principles across three designs, all with a consistent interface. The M18 sensors can be used as thru-beam photoelectric sensors, retroreflective photoelectric sensors for detecting transparency, and diffuse sensors.

INVESTMENT ANALYSIS AND OPPORTUNITIES

The photoelectric sensors market offers promising investment opportunities driven by technological advancements and increasing automation across various sectors Key investment trends include the adoption of advanced technologies such as LiDAR, time-of-flight sensors, wireless and battery-free sensor solutions, and 3D imaging for gesture recognition and environmental monitoring. Investing in sensors equipped with AI functionalities, wireless connectivity, and improved durability against environmental factors is expected to provide significant returns as these attributes become the norm in the industry. Furthermore, inductive and capacitive sensor technologies present opportunities, although photoelectric sensors continue to be favored for applications requiring long-range and versatility.

REPORT COVERAGE

The report provides a detailed analysis of the market and focuses on key aspects, such as leading companies, product types, and leading end-users. Besides, it offers insights into the market trends and highlights key industry developments. In addition to the factors mentioned above, the report encompasses several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 7.28% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

Type, Light Source, Range, End-User, and Region |

|

Segmentation |

By Type

By Light Source

By Range

By End-User

By Region

|

|

Companies Profiled in the Report |

Keyence Corporation (Japan) Schneider Electric (France) SICK AG (Germany) Rockwell Automation Inc. (U.S.) Tri-Tronics (U.S.) Pepperl+Fuchs (Germany) Banner Engineering (U.S.) Panasonic Corporation (Japan) SENSATEC Co., Ltd. (Japan) OMRON Corporation (Japan) |

Frequently Asked Questions

The market is projected to reach a valuation of USD 4.03 billion by 2034.

In 2025, the market was valued at USD 2.30 billion.

The market is projected to record a CAGR of 7.28% during the forecast period.

By type, the retroreflective segment led the market in 2025.

Rising industrial automation is a key factor driving market growth.

Keyence Corporation, Schneider Electric, SICK AG, Rockwell Automation Inc., Tri-Tronics, Pepperl+Fuchs, Banner Engineering, Panasonic Corporation, SENSATEC Co., Ltd., and OMRON Corporation are the top players in the market.

Asia Pacific held the highest market share in 2025.

By end-user, the automotive and transportation segment is expected to record the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us