Master Data Management Market Size, Share & Industry Analysis, By Deployment (Cloud and On-premise), By Enterprise Type (Large Enterprises and SMEs), By Industry (BFSI, IT & Telecom, Manufacturing, Healthcare, Retail & E-commerce, and Others), and Regional Forecast, 2026-2034

MASTER DATA MANAGEMENT MARKET SIZE AND FUTURE OUTLOOK

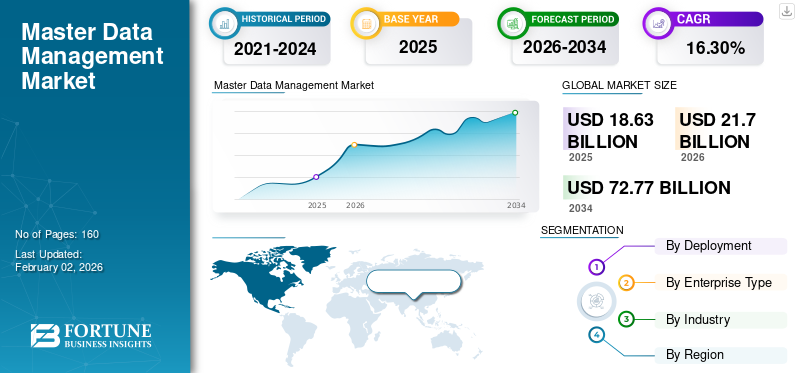

The global master data management market size was valued at USD 18.63 billion in 2025 and is projected to grow from USD 21.70 billion in 2026 to USD 72.77 billion by 2034, exhibiting a CAGR of 16.30% during the forecast period. North America dominated the master data management market with a market share of 37.40% in 2025.

Master data management is a comprehensive approach used by companies to standardize, define and manage their critical data assets across different systems. This aids in ensuring data consistency, accuracy and accessibility. It plays a significant role in data analytics and governance, thus allowing for informed decision making.

The market is significantly growing due to surge in digital technologies and reliance on data driven insights for decision making. Moreover, the regulatory compliance needs, and demand for seamless data integration across various on premise and cloud systems also promotes market expansion globally.

Prominent key market players including Informatica, IBM Corporation, SAP SE, Oracle Corporation, Stibo Systems and others are integrating strategies including cloud based master data management programs, AI powered automation, and strategic collaboration to optimize their product offerings.

Download Free sample to learn more about this report.

Master Data Management Market KEY TAKEAWAYS

- 2025 Market Size: USD 18.63 billion

- 2026 Market Size: USD 21.70 billion

- 2034 Forecast Market Size: USD 72.77 billion

- CAGR: 16.30% from 2026–2034

- North America dominated the master data management market with a 37.40% share in 2025.

- The IT & telecom industry segment is expected to account for the largest market share of 26.32% in 2026.

- The large enterprises segment is projected to lead with a 62.22% share in 2026.

North America

North America held a 37.40% market share in 2025, valued at USD 6.97 billion, and is projected to reach USD 7.96 billion in 2026.

Asia Pacific

Europe accounted for 22.60% of the global market in 2025, with a valuation of USD 4.2 billion, rising to USD 4.81 billion in 2026.

Asia Pacific

Asia Pacific represented 28.00% of global revenue in 2025, reaching USD 5.22 billion and is projected to grow to USD 6.31 billion in 2026.

U.S.

U.S. The market led global revenue with USD 4.98 billion in 2025, supported by strong enterprise adoption of data management solutions.

Japan

Japan The market is projected to reach USD 1.23 billion by 2026, driven by increasing digital transformation initiatives across industries.

Read More

IMPACT OF GENERATIVE AI

Increasing Reliance of Generative AI on Governed and High Quality Data Leads to Market Growth

Generative AI’s dependency on governed and higher quality data drives the overall market growth. To avoid large language models from generating incorrect or wrong insights, companies need to ground them in a trusted and single source of master data. This generated the need for master data management from back office purpose to a strategic AI enabler.

Additionally, generative AI also augments Master data management demand as it automates data matching and stewardship, thus improving operational efficiency and ensuring data accuracy. This technology aids firms in meeting advanced AI needs and compliance demands.

MARKET DYNAMICS

Market Drivers

Growing Adoption of Digital Transformation & Cloud Migration Drives Market Development

The increasing adoption of innovative digital technologies and cloud migration significantly drives the master data management market growth. With companies moving toward modernizing their ERP and CRM systems, they face challenges in managing distributed and vast data sources. This is creating a strong demand for consistent and single data sources which aids in ensuring reliability, accuracy, and seamless integration across various systems.

Additionally, master data management aids in combining product, customer and supplier data, thus allowing for improved operational efficiency and real time insights. Cloud based master data management provides increased flexibility and scalability, enabling businesses to handle their data across hybrid environments efficiently. Similarly, businesses also adopt master data management to enhance their digital strategies and maintain governance in growing IT landscape.

Market Restraints

High Initial Investment Hampers the Market Growth

A major restraint for the market is growing initial investment for implementation. Establishing a strong master data management framework demands considerable costs aligned with software licensing, data integration, modeling and real time maintenance.

Moreover, companies also need to invest in skilled human workforce to manage and monitor the data quality, further surging the operational expenses. Particularly, for small and medium sized businesses, such upfront costs make gaining return on investment highly difficult. The complexity of integrating these frameworks with current systems adds to the technical and financial burden.

Market Opportunities

Packaged ROI Accelerators Offers Lucrative Growth Opportunities

Bundled Return on Investment accelerators offer a significant opportunity for market growth. These accelerators include playbooks, pre-built KPIs, and benchmarks, allowing firms to gain quick implementation, time to value and reduced costs through master data management solutions. Through standardized frameworks, these companies simplify the complex data integration and governance processes, making its adoption more accessible to small and mid-sized companies.

Different vendors leverage the advantage of such accelerators to distinguish themselves via faster deployment cycles and measurable business outcomes. With organizations rapidly demanding ROI and agility in data management, the presence of these pre-configured solutions enhance customer satisfaction and drives its adoption rate.

MASTER DATA MANAGEMENT MARKET TRENDS

Rising Popularity of AI-Augmented Master Data Management Has Emerged as a Prominent Market Trend

A major trend reshaping the market is growing adoption of AI based solutions that optimizes data accuracy, automation and governance. Machine learning algorithms are widely used for entity matching, enabling firms to automatically recognize and integrate the duplicate records across systems.

Consequently, AI based survivorship models determine the highly reliable data sources for generating a single source of truth. Anomaly detection based on machine learning aids in uncovering the errors and inconsistencies in real time and improve the data reliability.

Download Free sample to learn more about this report.

SEGMENTATION ANALYSIS

By Deployment

Growth of Demand for Scalable and Cost Effective Master Data Management Boosts Cloud Segment Growth

Based on the deployment, the market is segmented into cloud and on-premise.

The cloud deployment segment is projected to dominate the master data management market, accounting for 76.91% of the global market share in 2026. The segment also had the highest CAGR of 18.75% in 2024. This growth is attributed to the growing demand for scalable, cost-efficient, and easily integrated MDM solutions to back real-time data governance across hybrid and multi-cloud environments. Additionally, the rapid integration of SaaS-based MDM platforms which provides flexibility, reduced upfront costs, and seamless integration with enterprise cloud ecosystems, boosts the segment growth.

By Enterprise Type

Growing Need for Handling Complex and High Volume Data Has Driven Large Enterprise Segment Growth

The market is divided into large enterprises and SMEs, based on enterprise type.

The large enterprises segment is expected to lead by enterprise type, contributing 62.22% globally in 2026. This growth is driven by the need to handle high volume and complex data by large enterprises across different geographies and domains. This also drives the need for a comprehensive master data management framework for compliance and governance.

Consequently, the SMEs segment held highest CAGR of 19.48% in 2024. Smaller firms demand enhanced data quality and streamlined operations with the need to invest in higher infrastructure costs. This promotes the adoption of affordable and easily accessible cloud based master data management solutions.

By Industry

Wide Data Generation from Different Connected Sources Augmented IT & Telecom Segment Growth

Based on the industry, the market is divided into BFSI, IT & Telecom, manufacturing, healthcare, retail & e-commerce, and others.

The IT & telecom industry segment will remain the largest end-use category, accepted for 26.32% of the global market share in 2026. This growth is driven by its wide data generation from different connected devices, customers and services. This generated data demands a robust master data management solution which aids in data consistency and operational competence.

On the other hand, retail and e-commerce segment held highest CAGR of 20.37% in 2024. Omnichannel retail is growing in popularity, demanding a single and real time view of customers and products. This would enable personalization, cut returns and optimize inventory effectively, thus leading to the segment’s growth.

To know how our report can help streamline your business, Speak to Analyst

MASTER DATA MANAGEMENT MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

North America

North America Master Data Management Market Size, 2025 (USD billion)

To get more information on the regional analysis of this market, Download Free sample

The North America market was valued at USD 6.97 billion in 2025, capturing 37.40% of global revenue, and is estimated to reach USD 7.96 billion in 2026 and is owing to the increased adoption of these platforms across large enterprises. Moreover, strong government mandates, presence of major master data management vendors and advanced IT or cloud infrastructure across the U.S. drives the regional market growth. The U.S. leads the North American market with an expected revenue share of USD 4.98 billion in 2025.

To know how our report can help streamline your business, Speak to Analyst

Europe

In 2025, Europe held 22.60% of the global market, reaching a valuation of USD 4.2 billion, and is projected to grow to USD 4.81 billion in 2026. This is attributed to the increasing digital transformation across industries including retail, finance, manufacturing and telecommunication. Additionally, growing focus of companies on data quality, integration and analytics across the U.K. France and other countries promote the market growth. The UK market is projected to reach USD 0.92 billion by 2026 and the Germany market is estimated to reach USD 0.90 billion by 2026.

Asia Pacific

The market in Asia Pacific reached USD 5.22 billion in 2025, representing 28.00% of total market revenue, and is projected to reach USD 6.31 billion in 2026. This growth is due to the increasing digitalization owing to the scale-ups, e-commerce, government push for data governance, and cloud based platform adoption across different enterprises and SMEs. This tends to enhance the demand for greenfield master data management solutions. The Japan market is projected to reach USD 1.23 billion by 2026, the China market is projected to reach USD 1.28 billion by 2026, and the India market is estimated to reach USD 0.90 billion by 2026.

South America and Middle East & Africa

In 2025, the Middle East & Africa market stood at USD 1.24 billion, representing 6.70% of global demand, and is projected to grow to USD 1.47 billion in 2026. The markets of South America and Middle East & Africa are growing with an expected share of USD 0.98 billion and USD 1.24 billion respectively in 2025. This growth is owing to the modernization of public sector and government digitization, majorly across Saudi Arabia and UAE. GCC countries are predicted to have a market share of USD 0.39 billion by 2025. Latin America maintained a strong presence in the global market, reaching USD 0.98 billion in 2025, accounting for 5.30% share, and is expected to reach USD 1.15 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Focus of Key Players on Innovation and New Launches Leads to their Dominating Market Positions

The global master data management industry is characterized by the presence of different large scale enterprises maintaining their strong presence through enterprise scale capabilities and wide product portfolio. Few key players operating in the market include Informatica, IBM Corporation, SAP SE, Oracle Corporation, Stibo Systems, TIBCO Software, Inc., Reltio, Semarchy, Ataccama, and others.

LIST OF KEY MASTER DATA MANAGEMENT COMPANIES PROFILED:

- Informatica (U.S.)

- IBM Corporation (U.S.)

- SAP SE (Germany)

- Oracle Corporation (U.S.)

- Stibo Systems (Denmark)

- TIBCO Software, Inc. (U.S.)

- Reltio (U.S.)

- Semarchy (France)

- Ataccama (Canada)

- Profisee (U.S.)

- Pimcore (Austria)

- Talend (U.S.)

- EnterWorks (U.S.)

- Salsify (U.S.)

- Uniserv (Germany)

KEY INDUSTRY DEVELOPMENTS:

- In October 2025, Digital Wave Technology, provider of the AI-native ONE Platform powered by a unified Master Data Management foundation, announced the launch of its AI-native Purchase Order Management solution, transforming one of the most underserved areas of the supply chain. By embedding AI directly into the purchase order (PO) process, Digital Wave Technology ensures data accuracy, streamlines workflows, and optimizes decision-making across global operations.

- In September 2025, Stibo Systems, a global leader in master data management (MDM) solutions, announced the availability of MDM SmartSync for Salesforce, a solution that brings governed, AI-ready customer data from Stibo Systems MDM platform directly into Salesforce. By preventing duplicates at the source, synchronizing golden records in real time, and surfacing MDM governance in the CRM workflow, SmartSync helps sales, service and marketing teams make better decisions with confidence.

- In June 2025, ZeroError, announced at Snowflake’s annual user conference, Snowflake Summit 2025, the launch of new advanced analytics capabilities to support supply chain optimization on the Snowflake AI Data Cloud. This new integration, powered by Snowflake, will enable organizations to tackle complex supply chain challenges such as master data, bill of materials (BOM), MRP planning, inventory management, carbon footprint and tax & tariff impact.

- In May 2025, Informatica, an AI-powered enterprise cloud data management leader, announced its comprehensive strategy for Agentic AI, building on the company's position as the industry's first AI-powered cloud data management platform. Informatica's strategic approach to Agentic AI expands on the company's AI innovation history, which includes the launch of CLAIRE GPT, CLAIRE Copilot and GenAI blueprints for major cloud ecosystem partners.

- In March 2025, Verdantis, a leader in AI-powered Master Data Management (MDM) solutions, announced the launch of Auto-Enrich AI and Auto-Spec AI, two cutting-edge autonomous AI agents designed to revolutionize data enrichment, normalization, and standardization for enterprises worldwide.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the master data management market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 16.30% from 2026-2034 |

| Historical Period | 2019-2023 |

| Unit | Value (USD Billion) |

| Segmentation | By Deployment, Enterprise Type, Industry, and Region |

| By Deployment |

|

| By Enterprise Type |

|

| By Industry |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size is projected to grow from USD 21.70 billion in 2026 to USD 72.77 billion by 2034, exhibiting a CAGR of 16.30% during the forecast period.

The market is expected to exhibit steady growth at a CAGR of 16.30% during the forecast period.

Growing adoption of digital transformation & cloud migration drives the market growth.

Informatica, IBM Corporation, SAP SE, Oracle Corporation, and Stibo Systems are some of the top players in the market.

The North America region held the largest market share.

North America was valued at USD 6.13 billion in 2024.

- 2021-2034

- 2025

- 2021-2024

- 160

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us