Medical Automation Market Size, Share & Industry Analysis, By Product & Service Type (Equipment & Systems {Automated Medication Dispensing Systems, Automated Laboratory Systems, Automated Imaging & Diagnostic Systems, and Others}, Software & Platforms, and Others), By Application (Diagnostics & Laboratory Automation, Pharmacy & Medication Management, Therapeutic & Surgical Automation, and Others), By End-user (Hospitals & Ambulatory Surgical Centers, Diagnostic Laboratories, Pharmacies & Compounding Centers, Research & Academic Institutes, and Others), and Regional Forecast, 2026-2034

Medical Automation Market Size and Future Outlook

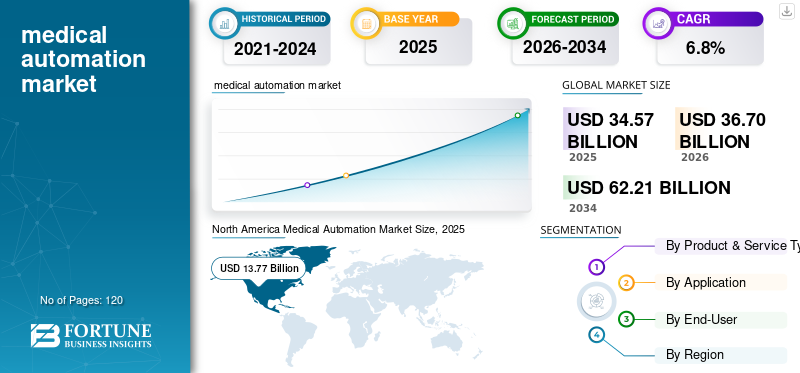

The global medical automation market size was valued at USD 34.57 billion in 2025. The market is projected to grow from USD 36.70 billion in 2026 to USD 62.21 billion by 2034, exhibiting a CAGR of 6.8% during the forecast period. North America dominated the medical automation market with a market share of 39.83% in 2025.

Medical automation refers to the use of automated equipment, software, robotics, AI, connected platforms, and workflow systems to reduce manual work across hospitals, laboratories, pharmacies, diagnostics, surgery, and patient care. The market growth is attributed to the rising prevalence of chronic diseases, increasing patient volumes globally, consistent workforce shortages across the healthcare sector, and growing demand for precision in diagnostics, therapeutics, and laboratory operations. Moreover, technological advancements in robotic-assisted surgery, AI-powered diagnostics, automated medication dispensing, and laboratory automation are further accelerating the adoption in the market. In addition, the shift toward value-based care and growing government investments in healthcare digitalization are also projected to have a significant positive impact on the market.

- For instance, in April 2021, Siemens Healthineers AG completed the acquisition of Varian Medical Systems Inc., with the aim to advance automation and precision medicine across oncology care pathways globally.

Furthermore, many key industry players, such as BD, Omnicell, Inc., Capsa Healthcare, ARxIUM, and ScriptPro LLC operating in the market, are focusing on developing various innovative technologies to offer better products with improved accuracy and efficiency.

Download Free sample to learn more about this report.

MEDICAL AUTOMATION MARKET TRENDS

Growing Adoption of AI-Enabled Medical Devices and Robotic-Assisted Surgery is One of the Significant Trends Observed in the Market

The market is witnessing a significant shift towards AI-enabled medical devices and robotic-assisted surgical platforms, with healthcare providers increasingly deploying intelligent automation tools that can support real-time clinical decision-making, reduce procedural variability, and improve patient safety. AI-powered imaging systems, automated pathology platforms, and robotic surgery ecosystems are being integrated into hospital workflows at an accelerating pace, supported by a growing body of clinical evidence and increasingly favorable regulatory pathways. In addition, companies are focusing on developing interoperable, cloud-connected automation platforms that can scale across multiple care settings, from flagship academic hospitals to community and ambulatory surgical centers, creating broader market penetration opportunities.

- For instance, in December 2024, GE HealthCare exhibited over 40 AI-enabled innovations at the Radiological Society of North America (RSNA) 2024 Annual Meeting, including new automated imaging analysis tools designed to optimize diagnostic accuracy and operational efficiency.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Chronic Disease Burden and Growing Patient Volumes to Accelerate Market Growth

A major driver of this market is the increasing burden of chronic diseases globally including cancer, cardiovascular disorders, diabetes, and neurological conditions, which is generating sustained and growing demand for automated diagnostic, therapeutic, and monitoring systems. As patient volumes rise and complexity in the healthcare sector increases, providers are facing mounting pressure to deliver faster, more accurate, and cost-efficient care, making automation a strategic necessity rather than an operational preference. According to the American Hospital Association, the U.S. alone recorded 33.69 million hospital admissions in 2023 due to rising chronic diseases, directly driving adoption of automation in hospitals and diagnostic centers.

MARKET RESTRAINTS

High Installation and Maintenance Costs of Automated Systems to Deter Market Growth

High cost of designing, developing, and installing fully automated healthcare systems is one of the prominent factors deterring the global medical automation market growth. It costs approximately USD 400,000 to implement a fully integrated automated system, placing significant financial pressure on smaller hospitals, diagnostic centers, and healthcare facilities in low- and middle-income countries where capital budgets are constrained. In addition to acquisition costs, ongoing maintenance expenses, software upgrades, and the requirement for specialized technical staff to operate and service complex automation platforms add substantially to the total cost of ownership. Furthermore, concerns around cybersecurity vulnerabilities, data privacy, and the risk of system failures in clinical environments are also limiting broader adoption, particularly in critical care and surgical settings where system reliability is non-negotiable.

MARKET OPPORTUNITIES

Increasing Integration of Artificial Intelligence and Robotics in Surgical and Diagnostic Workflows to Offer Lucrative Market Growth Opportunities

Increasing convergence of artificial intelligence, machine learning, and robotic systems with medical automation platforms is estimated to offer lucrative market growth opportunities. AI-driven diagnostic tools, autonomous robotic surgical systems, and intelligent laboratory automation platforms are demonstrating clinically validated improvements in terms of accuracy, throughput, and patient outcomes, making them increasingly attractive for healthcare institutions seeking to modernize care delivery. This creates significant opportunities for companies to develop integrated automation ecosystems that combine AI decision support, robotic execution, and real-time data analytics under unified platforms.

- For instance, in December 2024, GE HealthCare announced an agreement to acquire MIM Software, a global provider of medical imaging analysis and artificial intelligence solutions, with the aim to enhance its ability to deliver advanced imaging analytics, visualization, and workflow automation solutions across radiology, radiation therapy, and nuclear medicine applications.

MARKET CHALLENGES

Cybersecurity Risks and Regulatory Compliance Across Interconnected Automation Systems to Pose a Critical Challenge to Market Growth

Managing cybersecurity risks and ensuring regulatory compliance across increasingly interconnected medical automation systems is posing a critical challenge to the global market. As healthcare facilities deploy greater numbers of networked robotic devices, AI-powered diagnostic platforms, and automated data management systems, the attack surface for malware, ransomware, and unauthorized data access expands significantly, placing patient safety and institutional data integrity at risk. Regulatory frameworks for AI-enabled and automated medical devices are also evolving rapidly and inconsistently across markets, creating compliance uncertainty for manufacturers seeking global market access. Additionally, integrating disparate automation systems from multiple vendors into coherent and interoperable hospital workflows remains technically complex and resource-intensive, particularly for healthcare facilities with legacy IT infrastructure.

Segmentation Analysis

By Product & Service Type

Equipment & Systems Segment Dominated Due To Extensive Deployment Of Physical Automation Across Healthcare

Based on the product & service type, the market is divided into equipment & systems, software & platforms, and services.

The equipment & systems segment accounted for the largest medical automation market share in 2025. The segment growth is attributed to the extensive and diverse range of physical automation hardware deployed across healthcare settings, including robotic surgical systems, automated laboratory analyzers, automated medication dispensing units, diagnostic imaging equipment with embedded AI, and patient monitoring systems. Equipment and systems represent the foundational layer of medical automation infrastructure, and have high unit value, large installed base, and continuous upgrade and replacement cycles generating substantial and recurring revenue.

- For instance, in January 2025, Intuitive Surgical announced plans to establish a direct presence in Italy, Spain, Portugal, Malta, and San Marino by acquiring the da Vinci and Ion distribution businesses from its existing distributors, representing a combined installed base of over 470 da Vinci surgical systems across these countries.

The software & platforms segment is anticipated to rise with a CAGR of 6.7% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

High Test Volumes Of Accuracy-Critical Tasks in Healthcare by Laboratories to Drive the Leadership of Diagnostics & Laboratory Automation Segment

Based on application, the market is segmented into diagnostics & laboratory automation, pharmacy & medication management, therapeutic & surgical automation, patient monitoring & care automation, and others.

In 2025, the diagnostics & laboratory automation segment dominated the global market. Diagnostics and laboratory automation holds the largest share because laboratories and diagnostic centers process the highest volume of repetitive, accuracy-critical tasks in healthcare including sample preparation, specimen transport, reagent handling, test analysis, and result reporting. Automation delivers measurable improvements in throughput, error reduction, and turnaround time.

- For instance, in September 2024, Abbott launched its GLP systems track to enhance laboratory automation in India, deploying the systems across multiple cities to improve diagnostic efficiency, reduce operational costs, and enhance patient care quality through streamlined laboratory workflows.

Automated imaging & diagnostic systems segment is expected to register CAGR of 7.8% during the forecast period.

By End-User

Ability to Manage Complex Range of Automated Medical Processes in Hospitals & ASCs to Boost Segment Growth

Based on end-user, the market is segmented into hospitals & ambulatory surgical centers, diagnostic laboratories, pharmacies & compounding centers, research & academic institutes, and others.

In 2025, hospitals & ambulatory surgical centers held highest market share as they manage the broadest and most complex range of automated medical processes, encompassing robotic-assisted surgery, automated medication dispensing, AI-driven diagnostic imaging, patient monitoring automation, and administrative workflow automation across a single institutional setting. Hospitals collectively manage the highest patient volumes, a wide ranging mix of clinical procedures, and the most demanding clinical quality and safety requirements, all of which necessitate extensive and integrated automation solutions. Furthermore, the segment is set to hold 58.9% share in 2026.

In addition, diagnostic laboratories segment is projected to grow at a CAGR of 6.8% during the forecast period.

Medical Automation Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Automation Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024, valuing at USD 13.02 billion, and also maintained the leading share in 2025, with USD 13.77 billion. The market in North America is expected to grow due to advanced healthcare infrastructure, substantial adoption of surgical robotics systems, and strong government support for healthcare digitization.

U.S Medical Automation Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market can be analytically approximated at around USD 12.44 billion in 2026, accounting for roughly 33.9% of global market sales.

Europe

Europe is projected to record a growth rate of 6.3% in the coming years, which is the second highest among all regions, and reach a valuation of USD 10.27 billion by 2026. The region is estimated to witness considerable market growth due to rising investments for new product development and strong focus on improved workflow efficiency.

U.K Medical Automation Market

The U.K. market in 2026 is estimated at around USD 1.67 billion, representing roughly 4.5% of global market revenues.

Germany Medical Automation Market

Germany’s market is projected to reach approximately USD 2.31 billion in 2026, equivalent to around 6.3% of global market sales.

Asia Pacific

Asia Pacific is estimated to reach USD 8.69 billion in 2026 and secure the position of the third-largest region in the market. The market growth is attributed to rising number of healthcare institutions and increasing number of hospital visits.

Japan Medical Automation Market

The Japan market in 2026 is estimated at around USD 1.51 billion, accounting for roughly 4.6% of global market revenues.

China Medical Automation Market

China’s market is projected to be one of the largest worldwide, with 2026 revenues estimated at around USD 2.89 billion, representing roughly 7.9% of global market sales.

India Medical Automation Market

The India market in 2026 is estimated at around USD 1.93 billion, accounting for roughly 5.3% of global market revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in the market space during the forecast period. The Latin America market is set to reach a valuation of USD 1.96 billion in 2026. In the Middle East & Africa, the GCC is set to reach USD 0.44 billion in 2026. The growth of Latin America market is attributed to expanding healthcare infrastructure, while in MEA, rising number of healthcare facilities will accelerate market growth.

South Africa Medical Automation Market

The South Africa market is projected to reach around USD 0.18 billion in 2026, representing roughly 0.49% of global market revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Increasing Number of Product Launches Coupled with Strong Focus on Collaborations by Key Players to Boost Market Progress

The global market holds a semi-consolidated market structure, constituting prominent players such BD, Omnicell, Inc., Capsa Healthcare, ARxIUM, and ScriptPro LLC. The significant global medical automation market share of these companies is due to numerous strategic activities, including distribution collaborations and implementation of new programs.

- For instance, in October 2023, Honeywell launched Product Quality Review Automation software for medical product manufacturers. The strategic step was taken to simplify and accelerate the annual product quality review process for healthcare and pharmaceutical manufacturers, improving compliance efficiency and reducing manual documentation burden.

Other notable players in the global market Swisslog Healthcare, Yuyama Co., Ltd., TOSHO Inc., JVM Co., Ltd., and RxSafe LLC. These companies are expected to prioritize collaborations to increase their global market share during the forecast period.

LIST OF KEY MEDICAL AUTOMATION COMPANIES PROFILED

- BD (U.S.)

- Omnicell, Inc. (U.S.)

- Capsa Healthcare (U.S.)

- ARxIUM (U.S.)

- ScriptPro LLC (U.S.)

- Swisslog Healthcare (Switzerland)

- Yuyama Co., Ltd. (Japan)

- TOSHO Inc. (Japan)

- JVM Co., Ltd. (South Korea)

- RxSafe LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- March 2026: Intuitive Surgical completed the acquisition of the da Vinci and Ion distribution businesses operated by ab medica, Abex, and Excelencia Robotica across Italy, Spain, Portugal, Malta, San Marino, and associated territories.

- September 2023: PROCEPT BioRobotics Corporation received Investigational Device Exemption (IDE) approval from the U.S. FDA for its Aquablation therapy robotic platform.

- February 2023: GE HealthCare acquired Caption Health, an AI-driven technology company specializing in real-time cardiac ultrasound scan guidance. The strategic step was taken to integrate Caption Health's AI guidance technology into GE HealthCare's ultrasound portfolio, enhancing diagnostic automation and accessibility for point-of-care imaging.

- August 2022: THINK Surgical, Inc. announced a collaboration and distribution agreement with Curexo, Inc., a South Korea-based medical robotics company. The strategic step was taken to expand the commercial reach of THINK's TSolution One orthopedic surgical robotics platform across the South Korean and Vietnamese markets.

- January 2022: Zimmer Biomet Holdings, Inc. partnered with American Hospital Dubai to provide advanced robotic-assisted surgical training for orthopedic surgeons across the U.A.E. and surrounding region.

REPORT COVERAGE

The global medical automation market analysis includes a comprehensive study of the market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market over the forecast period. It provides information on key aspects, including an overview of technological advancements, the regulatory environment, and product launches. Additionally, it details partnerships, mergers & acquisitions, as well as key industry developments and investments by key regions. The global market research report also provides a depth competitive landscape with information on the market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.8% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product & Service Type, Application, End-User, and Region |

| By Product & Service |

|

| By Application |

|

| By End-User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 34.57 billion in 2025 and is projected to reach USD 62.21 billion by 2034.

In 2025, the market value stood at USD 13.77 billion.

The market is expected to exhibit a CAGR of 6.8% during the forecast period.

By product & service type, the equipment & systems segment is expected to lead the market.

Rising emphasis advanced healthcare infrastructure and growing number of product launches are driving market expansion.

BD, Omnicell, Inc., Capsa Healthcare, ARxIUM, and ScriptPro LLC are the major players in the global market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us