Medical Device Contract Manufacturing Market Size, Share & Industry Analysis, By Device Class (Class I, Class II, and Class III), By Service Type (Component & Accessories Manufacturing, Device Manufacturing, Packaging and Labeling, and Others), By Device Type (Cardiovascular Devices, Orthopedic Devices, Drug Delivery Devices, Diagnostic Imaging Devices, Respiratory Devices, and Others), By End-user (Original Equipment Manufacturers (OEMs), Pharmaceutical & Biopharmaceutical Companies, and Others), and Regional Forecast, 2026-2034

Medical Device Contract Manufacturing Market Size and Future Outlook

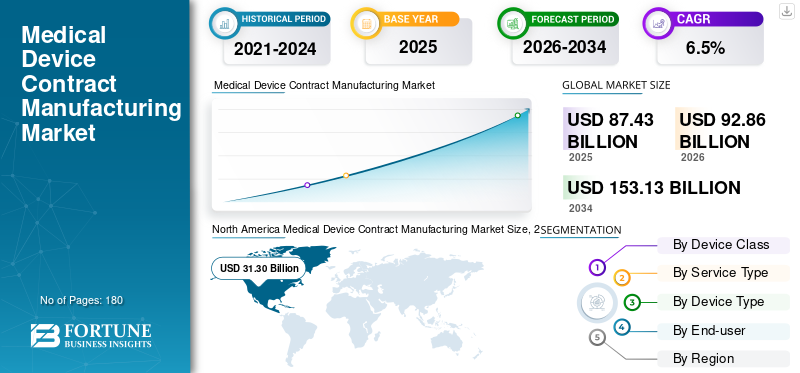

The global medical device contract manufacturing market size was valued at USD 87.43 billion in 2025. The market is projected to grow from USD 92.86 billion in 2026 to USD 153.13 billion by 2034, exhibiting a CAGR of 6.5% during the forecast period.

The medical device contract manufacturing services include outsourced design support, component manufacturing, device assembly, packaging, testing, sterilization support, and full-scale manufacturing services for medical device OEMs. Moreover, the market is witnessing significant growth as OEMs are increasingly preferring specialized partners to reduce capital investment in tooling, automation, cleanrooms, regulatory systems, and skilled manufacturing teams.

Furthermore, Jabil Inc., Integer Holdings Corporation, and TE Connectivity held the highest market share in 2025, driven by strong global footprints in specialized manufacturing services and an emphasis on service expansions.

Download Free sample to learn more about this report.

MEDICAL DEVICE CONTRACT MANUFACTURING MARKET TRENDS

Consolidation and Capability Expansion across Global Manufacturing Network to Emerge as a Key Trend

Currently, many CDMOs and strategic investors are acquiring specialized manufacturers to expand capabilities, geographies, and technology depth in their services. This expansion is the most common across micro-molding, metal processing, catheter assembly, additive manufacturing, coatings, and cardiovascular device manufacturing.

- For instance, in June 2024, DuPont announced the acquisition of Donatelle Plastics to deepen healthcare offerings in medical device solutions.

Moreover, contract manufacturers are moving from single-capability suppliers toward vertically integrated platforms that can serve complex OEM requirements across components, subassemblies, and finished devices.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

OEMs Focus on Cost Reduction and Faster Time-To-Market to Fuel the Market Expansion

In recent years, OEMs have increasingly outsourced to reduce manufacturing costs and accelerate commercialization. Contract manufacturers possess capabilities such as building in-house capacity, validation, cleanrooms, regulatory documentation, supply-chain systems, and trained operators. As a result, outsourcing to contract manufacturers allows OEMs to focus on R&D, branding, clinical strategy, and commercialization. Such a scenario is anticipated to drive the global medical device contract manufacturing market growth.

MARKET RESTRAINTS

Stringent Regulatory and Quality Compliance Requirements to Restrict Market Growth

Although the demand for medical device contract manufacturing services has been increasing, the market growth is constrained by stringent regulatory and quality requirements. This is particularly for Class II and Class III devices, where documentation, biocompatibility, traceability, process validation, risk management, and post-market quality controls are critical. For instance, Class II devices are subject to special controls and many require 510(k) premarket notification in the U.S., which increases compliance burden for both OEMs and contract manufacturers.

Moreover, any deviation in component quality, packaging, sterilization, or process validation delays approvals, triggers recalls, or damages OEM-CMO relationships, which is anticipated to hinder market growth during the forecast period.

MARKET OPPORTUNITIES

End-to-End CDMO Partnerships and Specialized Technology Platforms to Create Significant Growth Opportunities

In recent years, there has been an increase in end-to-end partnerships and acquisitions to support OEMs from concept through prototyping, design, validation, manufacturing, regulatory support, assembly, and packaging, and into scale-up. This has become the most attractive to start-ups and large OEMs seeking faster design transfer, fewer suppliers, and better supply-chain control, which is expected to create significant opportunities for key players.

- For instance, in June 2022, Resonetics acquired Agile MV, a Montreal-based product development and turnkey device assembly leader focused on electrophysiology and interventional cardiology catheters. The move is centered on expanding Resonetics’ development and finished-device assembly capabilities.

MARKET CHALLENGES

Supply-Chain Complexity and Capacity Balancing to Challenge Market Expansion

Managing global supply chain complexity while protecting OEM intellectual property and maintaining consistent quality across multiple manufacturing locations is a major challenge for service providers. Moreover, capacity planning poses a significant challenge given that the medical device demand can fluctuate due to product approvals, hospital purchasing cycles, regulatory delays, and component shortages.

In such a scenario, contract manufacturers need to balance automation investments, material sourcing, labor availability, and regionalization strategies. This is expected to limit market expansion over the forecast period. Furthermore, recent challenges have prompted medical device manufacturers to reassess their outsourcing strategies and strengthen collaborations with strategic partners.

Segmentation Analysis

By Device Class

More Regulations for Class II Devices over Other Classes to Boost the Segment Growth

Based on device class, the market is segmented into class I, class II, and class III.

To know how our report can help streamline your business, Speak to Analyst

The class II segment accounted for the largest global market share in 2025. Class II covers a broad range of moderate-risk medical devices widely used in diagnostics, cardiovascular care, surgical procedures, monitoring, and drug delivery, and typically require more controls. As a result, this is driving the demand for their outsourcing, contributing to segment growth.

- For instance, as of May 2026, Class II devices are subject to special controls and often follow the 510(k) pathway in the U.S. This creates the demand for contract manufacturers with validated quality systems, documentation expertise, and repeatable production capabilities.

Additionally, the class III segment is projected to grow at a CAGR of 7.3% during the forecast period.

By Service Type

Higher Need for Device Manufacturing with Expertise to Drive the Segment’s Growth

By service type, the market is segmented into component & accessories manufacturing, device manufacturing, packaging and labeling, and others.

The device manufacturing segment accounted for the largest market share in 2025. Device manufacturing is the core outsourcing need for OEMs, encompassing the production of components, subassemblies, and finished devices. This outsourcing is mainly due to the need to reduce fixed costs, improve flexibility, and access specialized equipment. Moreover, the segment is estimated to hold a share of 45.2% in 2026.

Additionally, the component & accessories manufacturing segment is anticipated to grow at a CAGR of 5.9% over the forecast period.

By Device Type

High Burden of Heart Conditions to Boost Cardiovascular Devices Segment Growth

By device type, the market is classified into cardiovascular devices, orthopedic devices, drug delivery devices, diagnostic imaging devices, respiratory devices, and others.

The cardiovascular devices segment accounted for the largest medical device contract manufacturing market share in 2025. The segment growth is attributed to the rising burden of heart conditions, which is driving the sustained demand for stents, catheters, guidewires, heart valves, electrophysiology devices, and structural heart devices, as well as the outsourcing of medical devices due to greater need. Moreover, the segment is projected to hold a 26.7% share in 2026.

- For instance, according to data from the British Heart Foundation in January 2024, around 2.3 million people in the U.K. are living with coronary heart disease.

Additionally, the orthopedic devices segment is expected to grow at a CAGR of 6.0% during the forecast period.

By End-user

Key Capabilities of Contract Manufacturers to Increase OEMs’ Outsourcing Propelling Segment Growth

On the basis of end-user, the market is segmented into original equipment manufacturers (OEMs), pharmaceutical & biopharmaceutical companies, and others.

In 2025, original equipment manufacturers (OEMs) segment dominated the market by end-user. OEMs own product design, regulatory submissions, brand strategy, and commercial channels. Further, they outsource their products to CDMOs for cost efficiency, capacity flexibility, and specialized technical capabilities, helping them meet the global demand and avoid delays in the product’s market entry. This is expected to fuel the segment’s growth. Furthermore, the segment is set to hold 75.3% share in 2026.

In addition, the pharmaceutical & biopharmaceutical companies segment is projected to grow at a CAGR of 8.3% during the forecast period.

Medical Device Contract Manufacturing Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Device Contract Manufacturing Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 29.57 billion, and touched a value of USD 31.30 billion in 2025. The strong presence of major medical device OEMs, advanced healthcare infrastructure, high R&D spending, and the early adoption of complex medical technologies is expected to support the regional market growth.

U.S. Medical Device Contract Manufacturing Market

In 2026, the U.S. is anticipated to reach USD 31.43 billion, accounting for approximately 33.8% of the global market.

Europe

The Europe market is projected to record a growth rate of 5.8% during the forecast period, the third-highest globally, reaching USD 23.97 billion by 2026. The region benefits from the higher concentration of medtech contract manufacturing sites in Germany, Ireland, Switzerland, France, and the U.K.

U.K. Medical Device Contract Manufacturing Market

The U.K. market is projected to reach USD 3.03 billion by 2026, representing approximately 3.3% of global revenues.

Germany Medical Device Contract Manufacturing Market

The Germany market is expected to reach around USD 5.70 billion by 2026, accounting for approximately 6.1% of the global revenue.

Asia Pacific

By 2026, the Asia Pacific market is projected to reach approximately USD 24.16 billion, making it the second-largest market worldwide. The growth is driven by cost-efficient manufacturing, expanding healthcare infrastructure, increasing domestic medical device demand, and growing outsourcing by global OEMs from contract manufacturers in China, India, Japan, South Korea, Malaysia, and Singapore.

Japan Medical Device Contract Manufacturing Market

The Japan market is projected to generate approximately USD 5.57 billion in revenue by 2026, representing nearly 6.0% of the global market.

China Medical Device Contract Manufacturing Market

The China market is anticipated to reach around USD 8.42 billion by 2026, accounting for nearly 9.1% of global revenues.

India Medical Device Contract Manufacturing Market

The India market is expected to reach approximately USD 2.91 billion by 2026, accounting for around 3.1% of the global market revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa markets are anticipated to witness moderate growth. The Latin America market is estimated to reach approximately USD 6.22 billion by 2026. The growth is attributed to the expansion of contract manufacturers in Mexico, Brazil, the GCC countries, and other countries/sub-regions, driven by the growing demand for cardiovascular, diagnostic, orthopedic, and minimally invasive devices.

GCC Medical Device Contract Manufacturing Market

By 2026, the GCC market is estimated to reach approximately USD 2.88 billion, representing around 3.1% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Manufacturing Footprint and Key Strategic Initiatives to Strengthen the Market Position of Key Players

In 2025, Jabil Inc., Integer Holdings Corporation, and TE Connectivity held the majority of the global medical device contract manufacturing market share. This share is due to global manufacturing footprints, regulatory expertise, cleanroom infrastructure, and the ability to support OEMs from design transfer to commercial production.

Moreover, other major players are focusing on specialized areas such as catheter assembly, nitinol processing, micro-molding, coatings, orthopedic implants, and others. Furthermore, their involvement in acquisitions and collaborations is further expected to help them gain significant market share.

LIST OF KEY MEDICAL DEVICE CONTRACT MANUFACTURING COMPANIES PROFILED

- Jabil Inc. (U.S.)

- Sanmina Corporation (U.S.)

- Celestica LLC (Canada)

- Integer Holdings Corporation (U.S.)

- TE Connectivity (Ireland)

- Phillips Medisize (U.S.)

- Gerresheimer AG (Germany)

- Freudenberg Medical (U.S.)

- Viant (U.S.)

- SMC Ltd (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Freudenberg Medical acquired Fuji Seiko to strengthen precision micro-tubing and hypotube supply for minimally invasive devices.

- May 2025: Quasar Medical signed an agreement to acquire Nordson Medical’s design and development contract manufacturing businesses in Ireland and Mexico.

- June 2024: Freudenberg Medical announced more than USD 50.0 million investment in a new coatings production facility in Aachen, Germany.

- January 2024: Integer Holdings Corporation acquired Pulse Technologies, a contract manufacturer focused on complex micro-machined medical device components.

- October 2023: Freudenberg Medical opened its expanded manufacturing facility in Galway, increasing the site’s production footprint by 50.0% to support the growing demand for hypotubes and catheter components.

- June 2023: Arterex acquired NextPhase Medical Devices, creating a larger global medical device contract manufacturing platform.

- October 2022: F Viant expanded its Heredia, Costa Rica, manufacturing campus by adding three buildings, increasing the site from four to seven buildings and expanding the total footprint by about 43.0% to roughly 257,000 sq. ft., mainly to support the production of the complex interventional and minimally invasive devices.

REPORT COVERAGE

The report offers a comprehensive analysis of all market segments, outlining the key drivers, emerging trends, growth opportunities, major restraints, and potential challenges influencing the market landscape. It also examines advanced technological developments, regulatory requirements for medical device manufacturing, notable industry updates, company market share analysis, and the profiles of leading market participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.5% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Device Class, Service Type, Device Type, End-user, and Region |

| By Device Class |

|

| By Service Type |

|

| By Device Type |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 87.43 billion in 2025 and is projected to reach USD 153.13 billion by 2034.

In 2025, the North America market value stood at USD 31.30 billion.

The market is expected to exhibit a CAGR of 6.5% during the forecast period of 2026-2034.

The class II segment led the market by device class in 2025.

A key factor driving the market is the expansion of OEM focus on cost reduction and faster time-to-market.

Jabil Inc., Integer Holdings Corporation, and TE Connectivity are the prominent players in the market.

North America is the dominant region in the market.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us