Medical Gas Equipment Market Size, Share & Industry Analysis, By Product Type (Instruments [Source & Generation Instruments, Control & Regulation Instruments, and Delivery Instruments] and Accessories), By Gas Type (Oxygen, Carbon Dioxide, Nitrogen, and Others), By Application (Therapeutic Applications, Pharmaceutical & Research Applications, and Others), By End User (Hospitals & Clinics, Pharmaceutical & Biotechnology Companies, Homecare Settings, and Others), and Regional Forecast, 2026-2034

Medical Gas Equipment Market Size and Future Outlook

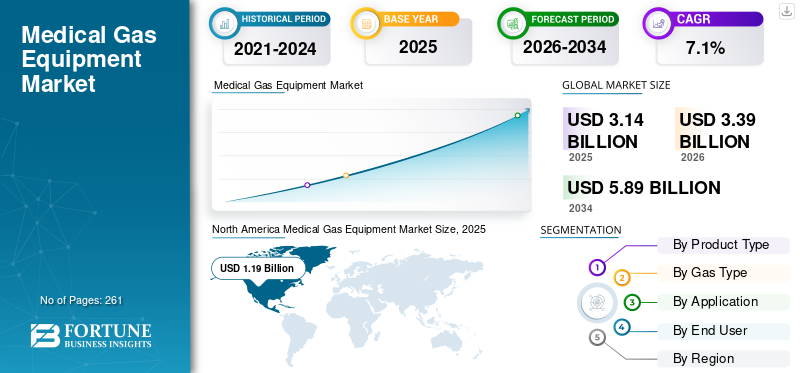

The global medical gas equipment market size was valued at USD 3.14 billion in 2025 and is projected to grow from USD 3.39 billion in 2026 to USD 5.89 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period. North America dominated the medical gas equipment market with a market share of 37.90% in 2025.

Medical gas equipment refers to devices used to produce, store, and distribute medical gases, including oxygen, in healthcare facilities. The increasing demand for medical gases such as oxygen for therapeutic applications, the growing number of surgeries, and the expansion of healthcare infrastructure are resulting in an increasing penetration rate of this equipment in the market. The aging population and rising adoption of home care and long-term oxygen therapy are further increasing the adoption rate of medical gas equipment in the market.

- For instance, according to the 2020 data published by the National Center of Biotechnology Information (NCBI), about 310 million major surgical procedures are performed each year globally.

Rapid incorporation of technological innovations in these devices by key players such as Drägerwerk AG & Co. KGaA and Linde PLC is further contributing to market expansion.

Download Free sample to learn more about this report.

Medical Gas Equipment Market Key Takeaways

- 2025 Market Size: USD 3.14 Billion

- 2026 Market Size: USD 3.39 Billion

- 2034 Forecast Market Size: USD 5.89 Billion

- CAGR: 7.1% from 2026–2034

- North America dominated the medical gas equipment market with a 37.90% share in 2025.

- The instruments segment accounted for the largest market share in 2025.

- The oxygen segment dominated the market with a 57.4% share in 2025.

Asia Pacific

Asia Pacific is expected to reach USD 0.80 billion in 2026.

North America

North America reached USD 1.19 billion in 2025.

Europe

Europe is projected to reach USD 1.02 billion in 2026.

U.S.

The medical gas equipment market is projected to reach USD 1.14 billion in 2026.

Japan

The medical gas equipment market is projected to reach USD 0.14 billion in 2026.

Read More

Medical Gas Equipment Market Trends

Integration of Technology in Medical Gas Equipment is a Key Market Trend

There is increasing demand among healthcare providers for safer, more efficient, and more resilient systems, driving advances in medical gas equipment. The market is shifting toward advanced PSA-based onsite oxygen generation systems, oxygen concentrators, smart alarms, digital monitoring, and devices designed to perform reliably in challenging operating environments.

Increasing demand for strengthening oxygen ecosystems, especially after the pandemic, improving hospital preparedness, and reducing dependence on conventional cylinder-based supply models is also driving growing R&D to develop advanced equipment for the market. Furthermore, technological advancements are contributing to the expansion of decentralized care settings, as advanced, portable, and resilient oxygen systems are better suited for remote clinics, home care, and resource-constrained facilities.

- In July 2025, GCE launched DUPLEX PNP200, an advanced medical gas manifold designed to ensure continuous, safe gas delivery in hospital pipeline systems and to support three independent gas sources, thereby streamlining the supply of critical medical gases across healthcare environments.

Market Dynamics

Market Drivers

Download Free sample to learn more about this report.

Rising Number of Surgeries and Introduction of Novel Medical Gas Equipment to Fuel Market Growth

The increasing prevalence of acute and chronic diseases, including cardiovascular disorders, respiratory disorders, and others, is resulting in a growing number of surgeries. This is increasing the reliance on vacuum systems, oxygen supply systems, and others among the patient population, consequently driving the demand for medical gas equipment in the market.

- For instance, according to 2024 statistics published by the Centers for Disease Control & Prevention (CDC), approximately 1 in 20 adults has coronary artery disease in the U.S.

This, along with increasing healthcare access and stringent safety standards in hospitals, is further augmenting the adoption rate of these devices in the market. Therefore, the factors above, along with the rising focus of key companies on research and development activities to launch novel equipment, are anticipated to boost the adoption rate of these devices, thereby contributing to the global medical gas equipment market growth.

Market Restraints

High Capital Cost Associated with Advanced Equipment to Limit Market Growth

The high capital demand and long-term capital cost of medical gas infrastructure remain a key restraint for the global market. Medical gas equipment often requires substantial investment across the full ecosystem, including generation equipment, manifolds, pipeline distribution networks, storage, vacuum systems, alarm panels, valves, terminal units, testing, and installation.

Moreover, additional expenses, including ongoing electricity use, preventive maintenance, spare parts, periodic compliance testing, and technical staffing, further make purchasing decisions more difficult for resource-constrained healthcare facilities, small hospitals, and providers in emerging markets, where funding limitations may delay modernization or expansion of medical gas systems.

- For instance, according to the statistics published by Medical Gas Installers, the average cost for a Western AGM2-2 Manifold is about USD 3,791.59.

Market Opportunities

Expansion of Healthcare Infrastructure in Emerging Economies to Create Lucrative Growth Opportunities

There is a rapid expansion of healthcare settings in emerging nations, including India, China, and others. The growing prevalence of chronic diseases, rising surgical volumes, expansion of healthcare infrastructure, and growing number of hospitals and clinics are consequently driving the adoption of medical gas equipment in healthcare facilities.

The expansion of healthcare infrastructure is driving demand for in-hospital wings, ICU blocks, ambulatory facilities, surgical complexes, and specialty care centers to support reliable gas supply, regulation, distribution, and monitoring, thereby creating a lucrative market opportunity.

- According to 2026 data published by the American Hospital Association (AHA), there are about 6,100 hospitals in the U.S.

Market Challenges

Restricted Access to Healthcare Services in Emerging Economies to Limit Market Growth

With the global patient pool requiring surgical procedures expanding, limited healthcare access in developing regions remains a critical barrier. Factors, including fluctuating healthcare expenditures, inadequate infrastructure, supply chain inefficiencies, and strict regulatory compliance, are limiting the availability of clinical facilities.

A shortage of healthcare providers and reduced reimbursement frameworks for respiratory treatments are leading to postponed surgical procedures. These constraints are collectively dampening the adoption of medical gas devices, particularly in emerging nations such as India and South Africa.

- As reported by the World Bank Group (WBG) in 2023, nearly 4.5 billion people globally still lack adequate access to essential healthcare services.

SEGMENTATION ANALYSIS

By Product Type

Increasing Prevalence of Chronic Diseases Boosted Instruments Segment Growth

Based on product type, the market is divided into instruments and accessories. Instruments are further classified into source & generation instruments, control & regulation instruments, and delivery instruments.

The instruments segment accounted for the largest medical gas equipment market share in 2025. The segment growth is attributed to the rising incidence of respiratory disorders and the requirement for life-saving gas, resulting in a growing demand for innovative medical gas devices. The launch of innovative equipment by several leading players is fueling segment growth.

- For instance, according to 2024 statistics published by the Centers for Disease Control & Prevention (CDC), approximately 16 million adults have chronic obstructive pulmonary disease in the U.S.

The accessories segment is anticipated to rise at a CAGR of 7.6% in the coming years.

To know how our report can help streamline your business, Speak to Analyst

By Gas Type

Increasing Number of Surgical Procedures Propelled Oxygen Segment Growth

Based on gas type, the market is segmented into oxygen, carbon dioxide, nitrogen, and others.

The oxygen segment dominated the global market with a 57.4% share in 2025. The growth is due to the growing number of surgical procedures, resulting in increasing reliance on medical gases. Rising emphasis on R&D activities among the major companies to launch novel equipment is fueling the adoption of these devices in the market.

- For instance, according to a 2020 publication by the National Center for Biotechnology Information (NCBI), around 40 to 50 million major surgical procedures are performed each year in the U.S.

The nitrogen segment is expected to flourish with a CAGR of 5.9% during the projected period.

By Application

Increasing Product Adoption in Surgical Procedures Fostered Therapeutic Applications Segment Expansion

Based on application, the market is segmented into therapeutic applications, pharmaceutical & research applications, and others.

The therapeutic applications segment dominated the global market with a 74.4% share in 2025. The growth is due to the increasing volume of surgical procedures, resulting in a growing demand for oxygen gas in various procedures.

- For instance, according to 2024 data published by Science Direct, approximately 1 million cardiac surgical procedures were projected to occur yearly globally.

The pharmaceutical & research applications segment is set to flourish with a CAGR of 8.2% during the forecast period.

By End User

Rise in Patient Admissions in Hospitals & Clinics Led to Segmental Dominance

In terms of end user, the market is categorized into hospitals & clinics, pharmaceutical & biotechnology companies, homecare settings, and others.

The hospitals & clinics segment led the market in 2025. The growing incidence of chronic respiratory disorders, rising hospital admissions, the expansion of hospitals and ambulatory surgical centers, and the growing demand for innovative devices in healthcare facilities are fueling segment growth. Furthermore, the segment is set to hold a 72.1% share in 2026.

- For instance, according to 2025 data published by The Trustees of Princeton University, there are more than 8,000 hospitals in Japan.

Pharmaceutical & biotechnology companies are predicted to grow at a 7.7% CAGR over the projected period.

Medical Gas Equipment Market Regional Outlook

Based on region, the market has been studied across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Medical Gas Equipment Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America emerged as the leading regional market, reaching USD 1.10 billion in 2024 and further strengthening its position with USD 1.19 billion in 2025. This dominance is largely driven by the rising burden of chronic diseases, supportive reimbursement frameworks, and the continuous rollout of advanced medical gas equipment.

- For instance, data released in 2026 by the Asthma and Allergy Foundation of America indicates that 28 million individuals in the U.S. are affected by asthma, highlighting a key demand driver.

U.S. Medical Gas Equipment Market

Given North America’s strong foothold and the U.S.’s leadership within the region, the U.S. market is estimated to reach approximately USD 1.14 billion in 2026, contributing around 33.5% to global revenues.

Europe

Europe is projected to record a growth rate of 6.6% in the coming years, which is the second highest among all regions, and reach a valuation of USD 1.02 billion by 2026. The strong shift toward home healthcare treatment options and the adoption of advanced technology are likely to support the market growth.

U.K Medical Gas Equipment Market

The U.K. market in 2026 is estimated at around USD 0.12 billion, representing roughly 3.6% of global revenues.

Germany Medical Gas Equipment Market

Germany’s market is projected to reach approximately USD 0.20 billion in 2026, equivalent to around 6.0% of global sales.

Asia Pacific

Asia Pacific is estimated to reach USD 0.80 billion in 2026 and secure the position of the third-largest region in the market. The growing number of surgical procedures, increasing healthcare expenditure, among others, is anticipated to boost the market growth. In the region, India and China are both estimated to reach USD 0.11 billion and USD 0.28 billion, respectively, in 2026.

Japan Medical Gas Equipment Market

The Japan market in 2026 is estimated at around USD 0.14 billion, accounting for roughly 4.2% of global revenues. Japan has historically reported a relatively high prevalence of chronic disorders, with a strong adoption of medical gas devices.

China Medical Gas Equipment Market

China’s market is projected to be one of the largest globally, with 2026 revenues estimated at around USD 0.28 billion, representing roughly 8.2% of global sales.

India Medical Gas Equipment Market

The India market size in 2026 is estimated at around USD 0.11 billion, accounting for roughly 3.2% of global revenues.

Latin America and Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 0.16 billion in 2026. The growth is driven by the increasing adoption of medical gas devices in the region. The Middle East & Africa region is expected to grow due to the growing number of key companies focusing on acquisitions and mergers among other companies in the region. In the Middle East & Africa, the GCC is set to reach a value of USD 0.06 billion in 2026.

South Africa Medical Gas Equipment Market

The South Africa market is projected to reach around USD 0.03 billion in 2026, representing roughly 0.8% of global revenues.

Competitive Landscape

Key Industry Players

Establishment of New Production and Distribution Facilities by Top Players to Support Their Dominance

A comprehensive product offering paired with a strategic global outlook has been instrumental in driving the leadership of key players in the medical gas equipment market. Companies such as Drägerwerk AG & Co. KGaA and Linde PLC are at the forefront of the market in 2025. Their growing emphasis on establishing new production and distribution facilities in emerging regions is expected to enhance their international market share further.

- For instance, in September 2025, Linde PLC announced the commencement of commercial production at its new gas facility in Unnao, Lucknow. The facility is designed to improve storage, handling, and distribution of bulk industrial and medical gases, catering to critical hospital operations and industrial applications in India.

Other players, including POWEREX and others, are witnessing steady growth, driven by their increasing focus on strategic alliances and acquisitions to enhance their market presence.

List of Key Medical Gas Equipment Companies Profiled

- Drägerwerk AG & Co. KGaA (Germany)

- Linde PLC (U.K.)

- POWEREX (U.S.)

- Amico Group of Companies (UAE)

- Tritech (U.S.)

- Atlas Copco Compressors LLC (Sweden)

- NOVAIR (France)

- Ohio Medical (U.S.)

- GCE (Switzerland)

- Pattons Medical (U.S.)

KEY INDUSTRY DEVELOPMENTS

- April 2026: Hersill participated in the World Health Expo Miami 2026 (WHX Miami) with the aim of boosting medical technology in Latin America.

- July 2025: BeaconMedaes attended the ASHE Health Care Facilities Innovation Conference to promote their medical gas and alarm management technology. This helped the company to strengthen its presence.

- May 2025: BeaconMedaes collaborated with Medclair, a Swedish innovator in sustainable nitrous oxide management, to transform the healthcare industry’s approach to medical gas management in Australia.

- January 2025: GCE, an ESAB Corporation brand, showcased its full range of Health Technical Memoranda (HTM) and medical central gas solutions at the 50th Arab Health Medical Expo (Booth H1.C15) at the Dubai World Trade Center.

- June 2024: NOVAIR partnered with American Oxygen to develop and market ionic oxygen generators, which will revolutionize the oxygen market.

- October 2023: Atlas Copco acquired William G Frank Medical Gas Testing and Consulting, LLC, a service and verification supplier for medical gas systems, and Medical Gas Credentialing LLC, to strengthen its product channel.

- September 2023: BeaconMedaes launched its next-generation TMA Medical Air Supply System. The new TMA combines technology in a unique all-in-one package with an ultra-compact footprint.

REPORT COVERAGE

The report provides a detailed global medical gas equipment market analysis and focuses on key aspects such as leading companies and market segmentation, including product type, gas type, application, and end user. Besides this, the global report offers insights into the market growth trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth and advancement of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 7.1% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product Type, Gas Type, Application, End User, and Region |

| By Product Type |

|

| By Gas Type |

|

| By Application |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was USD 3.14 billion in 2025 and is projected to reach USD 5.89 billion by 2034.

In 2025, North America’s market value stood at USD 1.19 billion.

Growing at a CAGR of 7.1%, the market will exhibit steady growth over the forecast period (2026-2034).

By product type, the instruments segment led the market.

Rising number of surgeries and the introduction of novel medical gas equipment are expected to fuel market growth.

Drägerwerk AG & Co. KGaA and Linde PLC are the major players in the global market.

North America dominated the market share in 2025.

Expansion of healthcare infrastructure is expected to boost the adoption of these devices globally.

- 2021-2034

- 2025

- 2021-2024

- 261

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us