Metal Casting Market Size, Share & Industry Analysis, By Material (Iron, Steel, Aluminum), By Application (Automotive, Industrial, Building & Construction), and Regional Forecast, 2026–2034

Metal Casting Market Overview

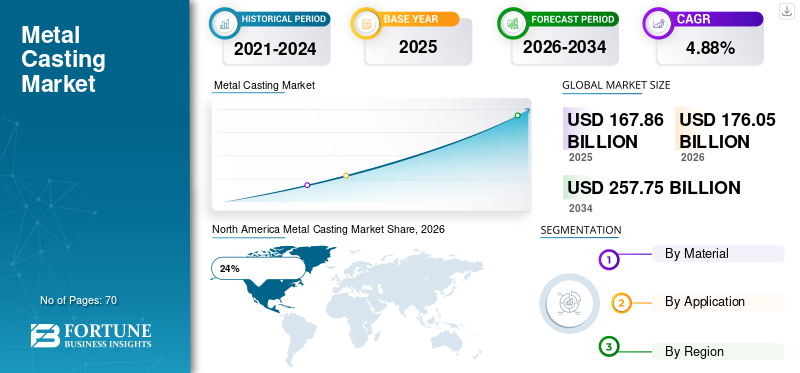

The global metal casting market size was valued at USD 167.86 billion in 2025. The market is projected to grow from USD 176.05 billion in 2026 to USD 257.75 billion by 2034, exhibiting a CAGR of 4.88% during the forecast period.

The global metal casting market continues to expand due to rising demand from automotive manufacturing, industrial machinery production, heavy engineering operations, renewable energy infrastructure, and transportation equipment fabrication. Metal casting processes are widely used for producing complex metal components with high dimensional accuracy, durability, and cost efficiency. The metal casting market Report indicates strong adoption of iron, steel, and aluminum casting across manufacturing hubs because of increasing demand for lightweight structures, heat-resistant components, and precision-engineered industrial parts. metal casting market Analysis also highlights the growing use of automated foundries, robotic molding systems, and digital simulation technologies that improve productivity, reduce scrap generation, and support large-scale manufacturing operations worldwide.

The United States metal casting market remains one of the most technologically advanced manufacturing sectors, supported by aerospace production, defense manufacturing, automotive assembly plants, and industrial equipment fabrication. More than 1,800 foundries operate across the country, supplying precision cast parts for engines, turbines, pumps, rail systems, and agricultural machinery. The USA Metal Casting Industry Report identifies aluminum and steel casting as major production categories due to increasing electric vehicle manufacturing and industrial automation investments. Domestic manufacturers are also integrating artificial intelligence-enabled quality inspection systems and energy-efficient melting technologies to improve operational efficiency. Demand for locally manufactured components continues to strengthen the metal casting market Outlook in the United States.

Download Free sample to learn more about this report.

Key Takeaways

Market Size & Growth

- Global market size 2025: USD 167.85 billion

- Global market size 2034: USD 257.75 billion

- CAGR (2025–2034): 4.88%

Market Share – Regionals

- North America: 24%

- Europe: 22%

- Asia-Pacific: 43%

- Rest of World: 11%

Country-Level Shares

- Germany: 31% of Europe’s market

- United Kingdom: 18% of Europe’s market

- Japan: 21% of Asia-Pacific market

- China: 39% of Asia-Pacific market

Metal Casting Market Latest Trends

The metal casting market Trends indicate rapid modernization of foundry operations through automation, digital manufacturing platforms, and advanced simulation software. Manufacturers are increasingly adopting robotic pouring systems, automated molding equipment, and smart furnace monitoring technologies to reduce production defects and improve casting precision. Around 48% of medium and large foundries worldwide have implemented some form of automated quality inspection technology to increase productivity and reduce operational downtime. metal casting market Insights also show that predictive maintenance software is becoming an essential tool in modern foundries to minimize equipment failures and enhance production consistency.

Another major trend in the Metal Casting Industry Analysis is the rising preference for lightweight cast components in electric vehicles, renewable energy equipment, and aerospace systems. Aluminum casting demand has increased significantly because lightweight materials improve fuel efficiency and reduce overall equipment weight. Sustainable manufacturing practices are also shaping the metal casting market Forecast, as foundries increasingly use recycled scrap metal and energy-efficient furnaces. Nearly 62% of manufacturers are investing in environmentally sustainable casting processes to meet industrial emission standards and corporate sustainability goals. Additive manufacturing-assisted casting and 3D printed molds are further transforming prototype development and low-volume production activities across the global market.

Download Free sample to learn more about this report.

Metal Casting Market Dynamics

DRIVER

Rising demand from automotive and industrial manufacturing sectors

The primary growth driver in the metal casting market Growth is the increasing production of automobiles, industrial machinery, heavy equipment, and transportation systems worldwide. Cast metal components remain essential in manufacturing engine blocks, transmission housings, brake systems, turbines, construction machinery parts, and railway components. More than 54% of cast products are consumed by the automotive and transportation industries due to continuous vehicle production expansion and increasing demand for electric mobility solutions. The metal casting market Research Report highlights that manufacturers are shifting toward precision casting techniques to improve product quality and reduce machining costs.

Industrial infrastructure expansion across emerging economies is also accelerating demand for high-strength cast components. Governments are investing heavily in transportation infrastructure, smart cities, manufacturing zones, and renewable energy projects, increasing the need for durable metal products. Heavy industrial machinery manufacturers are increasingly dependent on steel and iron castings for mining equipment, agricultural machinery, and power generation systems. The growing integration of automation in industrial facilities further supports the metal casting market Opportunities by driving demand for precision-engineered machine components with superior mechanical properties and extended operational life.

RESTRAINT

High energy consumption and environmental compliance costs

One of the major restraints affecting the metal casting market Size is the high operational cost associated with energy-intensive foundry processes. Metal melting, mold preparation, and heat treatment operations require substantial electricity and fuel consumption, increasing production expenses for foundry operators. Energy costs account for nearly 32% of operational expenditure in many medium-scale foundries. Rising electricity prices and stricter industrial emission regulations are putting financial pressure on small and medium-sized casting manufacturers across developed and developing economies.

Environmental compliance requirements are becoming increasingly stringent due to concerns regarding carbon emissions, industrial waste generation, and air pollution. Foundries must invest in advanced filtration systems, waste recycling infrastructure, and emission-control technologies to comply with environmental regulations. These additional investments raise production costs and reduce profitability for smaller manufacturers. The metal casting market Analysis also reveals that skilled labor shortages in traditional foundry operations are limiting production efficiency in several regions. Many manufacturers face difficulties in recruiting experienced technicians capable of operating advanced casting systems and automated production equipment.

OPPORTUNITY

Expansion of electric vehicles and renewable energy infrastructure

The growing adoption of electric vehicles and renewable energy systems presents major opportunities for the metal casting market Outlook. Electric vehicles require lightweight cast aluminum components for battery housings, motor casings, suspension systems, and structural frames. Global electric vehicle production volumes continue to increase as governments implement stricter emission standards and provide incentives for clean mobility adoption. Aluminum casting demand in electric mobility applications has increased substantially because manufacturers aim to improve vehicle efficiency and reduce overall weight.

Renewable energy infrastructure development is another important growth opportunity in the Metal Casting Industry Report. Wind turbines, solar power systems, hydroelectric equipment, and energy storage installations require high-strength cast components capable of operating in extreme conditions. Nearly 41% of renewable energy equipment manufacturers now use precision-cast steel and iron parts for turbine housings, gearboxes, and structural support systems. The increasing use of 3D printed molds and digital casting simulation tools also creates opportunities for customized low-volume production, rapid prototyping, and improved product development cycles across industrial manufacturing sectors.

CHALLENGE

Volatility in raw material prices and supply chain disruptions

Fluctuating prices of raw materials such as iron ore, aluminum, steel scrap, and alloying metals remain a major challenge for the metal casting market Forecast. Sudden increases in raw material costs directly impact production expenses and reduce profit margins for foundry operators. Supply chain instability caused by geopolitical tensions, transportation bottlenecks, and trade restrictions has further complicated procurement operations for casting manufacturers. Many foundries struggle to maintain stable production schedules due to inconsistent raw material availability and delayed shipment deliveries.

Another critical challenge in the metal casting market Research Report is maintaining consistent product quality while meeting high-volume production requirements. Casting defects such as porosity, shrinkage, cracks, and dimensional inaccuracies can increase rejection rates and operational losses. Advanced quality control systems require substantial investments in digital monitoring technologies, simulation software, and automated inspection systems. Additionally, increasing competition from alternative manufacturing technologies such as additive manufacturing and precision machining creates pricing pressure within the global metal casting industry. Manufacturers must continuously invest in innovation and process modernization to remain competitive in the evolving industrial landscape.

Metal Casting Market Segmentation

By Type

Iron casting remains one of the largest segments in the metal casting market Share due to its widespread use in automotive components, industrial machinery, pipes, valves, and heavy engineering structures. Iron castings account for nearly 46% of total global casting production because of their excellent wear resistance, durability, and cost efficiency. Gray iron and ductile iron are extensively used in manufacturing engine blocks, brake components, agricultural machinery parts, and construction equipment. The metal casting market Analysis indicates that demand for iron casting remains particularly strong in infrastructure development and industrial manufacturing sectors where high mechanical strength is essential.

Modern foundries are increasingly adopting automated sand molding systems and induction furnace technologies to improve iron casting productivity and reduce operational waste. Iron casting manufacturers are also integrating recycled scrap materials into production processes to improve sustainability and reduce raw material dependence. Around 58% of large-scale iron foundries have implemented advanced quality control systems to improve dimensional precision and reduce defect rates. The metal casting market Trends further reveal that industrial automation and renewable energy equipment manufacturing continue to create strong long-term demand for iron cast products across global markets.

Steel casting represents a significant portion of the metal casting market Size because of its superior tensile strength, impact resistance, and high-temperature performance. Steel castings are widely used in mining equipment, railway systems, turbines, defense applications, heavy transportation machinery, and power generation facilities. This segment contributes approximately 29% of global casting demand due to increasing industrialization and infrastructure modernization projects worldwide. The Metal Casting Industry Analysis highlights rising demand for stainless steel and alloy steel castings in corrosive industrial environments and energy infrastructure applications.

Steel casting manufacturers are investing heavily in vacuum casting systems, computer-aided simulation software, and robotic finishing technologies to improve product consistency and production efficiency. Heavy engineering industries continue to rely on steel castings because of their ability to withstand extreme operational loads and harsh environmental conditions. The increasing expansion of rail transportation networks, offshore energy infrastructure, and industrial processing plants is supporting strong growth in this segment. The metal casting market Forecast also indicates rising adoption of precision steel casting in aerospace and defense manufacturing applications where structural integrity and reliability are critical operational requirements.

Aluminum casting has become one of the fastest-growing segments in the metal casting market Opportunities due to increasing demand for lightweight and corrosion-resistant components. Aluminum castings account for approximately 25% of global casting production and are extensively used in electric vehicles, aerospace systems, consumer electronics, and renewable energy equipment. Automotive manufacturers are rapidly shifting toward aluminum cast parts to reduce vehicle weight and improve energy efficiency. The metal casting market Insights show that aluminum engine blocks, transmission housings, battery enclosures, and suspension components are witnessing substantial demand growth.

Advanced die casting technologies and high-pressure casting systems are improving production efficiency and reducing material waste in aluminum foundries. More than 44% of aluminum casting manufacturers now utilize automated robotic handling systems to improve production consistency and operational safety. Recyclability is another major factor driving aluminum casting demand because recycled aluminum requires significantly lower energy consumption compared to primary metal production. The metal casting market Report further highlights that increasing investments in electric mobility infrastructure and lightweight industrial equipment manufacturing will continue supporting expansion of the aluminum casting segment over the coming years.

To know how our report can help streamline your business, Speak to Analyst

By Application

The automotive sector dominates the metal casting market Growth with approximately 39% market share due to extensive use of cast components in engines, transmissions, braking systems, suspension assemblies, and electric vehicle platforms. Metal castings remain critical for achieving high-volume vehicle production with consistent dimensional accuracy and mechanical performance. The transition toward electric vehicles is significantly increasing demand for lightweight aluminum castings used in battery systems and structural vehicle components. Automotive manufacturers continue to invest in advanced die casting technologies to reduce assembly complexity and improve production efficiency.

The Metal Casting Industry Report indicates that integrated giga-casting technology is transforming automotive manufacturing processes by enabling production of large structural components with fewer assembly parts. Manufacturers are increasingly adopting automated casting lines and digital quality inspection systems to meet rising vehicle production demands. Around 52% of automotive casting facilities have implemented robotic handling systems to improve productivity and reduce labor dependency. Growing global demand for commercial vehicles, passenger cars, and electric mobility solutions continues to strengthen the automotive segment within the metal casting market Analysis.

Industrial applications represent a major segment of the metal casting market Share, contributing nearly 34% of global demand. Industrial machinery, mining equipment, agricultural systems, turbines, compressors, and manufacturing equipment require durable cast components capable of operating under high stress and extreme environmental conditions. Iron and steel castings remain widely preferred in industrial applications because of their superior strength and wear resistance. The metal casting market Outlook highlights increasing industrial automation and infrastructure development as major factors supporting segment growth.

Heavy machinery manufacturers rely extensively on precision casting processes to produce complex equipment components with high structural integrity. Industrial foundries are increasingly integrating simulation software and automated production technologies to reduce material waste and improve manufacturing efficiency. Demand for industrial castings is also increasing in renewable energy equipment manufacturing, particularly for wind turbine housings, gearbox systems, and hydroelectric infrastructure. The metal casting market Research Report indicates that rapid industrialization across Asia-Pacific and Middle Eastern countries continues to create strong long-term growth opportunities for industrial casting manufacturers.

The building and construction sector accounts for approximately 27% of the metal casting market Size due to increasing infrastructure development activities worldwide. Cast metal products are widely used in structural supports, pipelines, drainage systems, architectural hardware, bridges, transportation infrastructure, and heavy construction machinery. Iron casting remains particularly important in municipal infrastructure projects because of its durability, load-bearing capacity, and long operational lifespan. The metal casting market Trends indicate rising investments in urban infrastructure modernization and smart city development projects.

Construction equipment manufacturers increasingly require steel and iron castings for excavators, cranes, bulldozers, and heavy lifting machinery. Modern architectural projects are also utilizing decorative aluminum castings for building facades, railings, and customized structural components. Around 47% of infrastructure development projects globally depend on cast metal products for transportation and utility systems. The Metal Casting Industry Analysis further highlights that growing investments in industrial parks, commercial construction projects, and public transportation systems continue supporting strong demand for high-performance cast components across the global construction sector.

Metal Casting Market Regional Outlook

North America

North America Metal Casting Market Share, 2026 (%)

To get more information on the regional analysis of this market, Download Free sample

North America remains a technologically advanced region in the metal casting market Outlook, accounting for approximately 24% of global market share. The region benefits from strong automotive manufacturing capabilities, aerospace production facilities, industrial equipment manufacturing, and defense sector investments. The United States and Canada continue investing in advanced foundry automation technologies, digital manufacturing platforms, and energy-efficient furnace systems. Metal casting demand remains high across transportation equipment, agricultural machinery, mining equipment, and renewable energy infrastructure applications. Regional manufacturers are increasingly adopting robotic casting operations and artificial intelligence-enabled quality inspection systems to improve operational productivity and reduce manufacturing defects.

The metal casting market Research Report highlights that reshoring initiatives and domestic supply chain strengthening are supporting regional manufacturing expansion. Automotive production facilities continue increasing demand for lightweight aluminum castings used in electric vehicle platforms and structural automotive components. North American foundries are also emphasizing sustainable manufacturing practices through recycled metal utilization and emission reduction technologies. Investments in industrial modernization and aerospace manufacturing are expected to maintain stable growth across the regional casting industry over the coming years.

Europe

Europe represents a major manufacturing hub in the metal casting market Analysis with nearly 22% market share driven by automotive engineering, industrial machinery production, railway infrastructure, and renewable energy equipment manufacturing. Germany, Italy, France, and the United Kingdom remain major contributors to regional foundry operations. European manufacturers are increasingly adopting environmentally sustainable casting technologies and automated production systems to comply with industrial emission regulations and improve operational efficiency. The region is witnessing increasing adoption of lightweight aluminum and precision steel castings across automotive and aerospace industries.

The metal casting market Forecast indicates strong demand for high-performance cast components used in wind turbines, electric vehicles, and industrial automation systems. European foundries continue investing in digital twin technologies, simulation software, and advanced molding systems to improve manufacturing precision and reduce production waste. Infrastructure modernization projects and expansion of electric mobility manufacturing facilities are further supporting regional market growth. The transition toward low-emission industrial operations remains a central trend influencing the European metal casting sector.

Germany Metal Casting Market market

Germany remains the largest contributor within the European metal casting market Share, holding approximately 31% of regional production activity. The country’s advanced automotive manufacturing industry plays a major role in driving casting demand for engine systems, transmission housings, structural vehicle parts, and electric mobility components. German foundries are recognized for high-precision steel and aluminum casting technologies used in industrial machinery, aerospace systems, and renewable energy infrastructure. Advanced automation and robotic manufacturing technologies are widely integrated into German foundry operations to improve efficiency and maintain high product quality standards.

Industrial machinery production and engineering excellence continue strengthening the Germany Metal Casting Industry Report. The country also benefits from strong export demand for heavy industrial equipment and transportation systems. Aluminum casting demand is increasing rapidly due to growth in electric vehicle production and lightweight manufacturing initiatives. German manufacturers are focusing heavily on energy-efficient furnace systems, digital quality inspection technologies, and recycled metal utilization to improve sustainability performance. Infrastructure modernization and industrial automation investments continue supporting long-term expansion of the country’s metal casting sector.

United Kingdom Metal Casting Market

The United Kingdom metal casting market Insights reflect steady growth driven by aerospace engineering, automotive manufacturing, railway infrastructure development, and industrial machinery production. The country contributes nearly 18% of the European casting industry due to increasing investments in precision manufacturing technologies and advanced engineering applications. Steel and aluminum castings are widely used in aerospace systems, defense equipment, offshore energy infrastructure, and electric mobility solutions. UK manufacturers are increasingly investing in automated casting operations and digital process monitoring systems to improve manufacturing efficiency and reduce operational waste.

The British manufacturing sector continues emphasizing sustainability and energy-efficient production technologies across foundry operations. Aerospace and defense industries remain major consumers of precision steel and aluminum cast components because of stringent quality and structural reliability requirements. Infrastructure redevelopment projects and transportation modernization programs are also creating demand for high-strength cast products. The metal casting market Report highlights that local foundries are increasingly adopting additive manufacturing-assisted casting methods to improve prototype development capabilities and support customized industrial production requirements.

Asia-Pacific

Asia-Pacific dominates the global metal casting market Size with approximately 43% market share due to rapid industrialization, automotive manufacturing expansion, infrastructure development, and large-scale industrial equipment production. China, Japan, India, and South Korea remain major contributors to regional foundry output. The region benefits from abundant raw material availability, cost-effective labor, and expanding manufacturing ecosystems. Automotive production continues driving substantial demand for iron, steel, and aluminum castings across passenger vehicles, commercial transportation, and electric mobility platforms.

The metal casting market Trends in Asia-Pacific indicate increasing investments in automated foundries, smart manufacturing systems, and energy-efficient melting technologies. Infrastructure development projects, industrial machinery production, and renewable energy expansion continue strengthening regional casting demand. Many manufacturers are integrating robotic molding systems and digital process monitoring tools to improve product quality and production efficiency. Rapid urbanization and industrial growth across emerging economies are expected to maintain strong long-term growth opportunities for metal casting manufacturers throughout the Asia-Pacific region.

Japan Metal Casting Market

Japan remains a highly advanced manufacturing economy within the metal casting market Opportunities, contributing nearly 21% of Asia-Pacific casting production. The country specializes in high-precision casting technologies used in automotive engineering, robotics, aerospace systems, and industrial automation equipment. Japanese foundries are recognized for exceptional product quality standards, advanced process control systems, and efficient manufacturing operations. Aluminum casting demand remains particularly strong because Japanese automotive manufacturers continue prioritizing lightweight vehicle production and energy-efficient transportation technologies.

The Metal Casting Industry Analysis highlights increasing adoption of automated robotic casting systems and digital inspection technologies across Japanese foundries. Industrial robotics, semiconductor manufacturing equipment, and renewable energy infrastructure continue supporting demand for precision-cast components. Japan’s aging industrial workforce is also accelerating investments in automation technologies to maintain production efficiency and operational reliability. The country’s focus on sustainability and energy-efficient manufacturing practices further strengthens its position in advanced casting production technologies.

China Metal Casting Market

China represents the largest national market in the global metal casting market Growth, accounting for approximately 39% of Asia-Pacific production volume. Massive automotive manufacturing capacity, infrastructure development, heavy industrial machinery production, and construction activity continue driving enormous casting demand across the country. China remains a global leader in iron and steel casting production due to large-scale industrial manufacturing operations and strong domestic infrastructure investment programs. Aluminum casting demand is also expanding rapidly with increasing electric vehicle manufacturing activities.

Chinese foundries are investing aggressively in automated production lines, smart manufacturing systems, and high-capacity melting technologies to improve global competitiveness. Infrastructure expansion projects, railway development, renewable energy installations, and industrial modernization programs continue strengthening casting consumption. The metal casting market Research Report indicates that government support for advanced manufacturing and export-oriented industrial production remains a major factor supporting China’s leadership position in the global casting industry. Domestic manufacturers are also increasing adoption of environmentally sustainable production technologies and recycled metal utilization practices.

Rest of World

The Rest of World region holds approximately 11% share in the global metal casting market Forecast, supported by industrial development activities in Latin America, the Middle East, and Africa. Infrastructure construction, mining operations, oil and gas projects, and transportation system expansion continue driving demand for cast metal products across these regions. Iron and steel castings remain widely used in heavy industrial machinery, pipelines, construction equipment, and energy infrastructure applications. Governments are increasingly investing in industrial diversification and local manufacturing capabilities to reduce dependence on imported industrial components.

The metal casting market Opportunities across the Rest of World region are further supported by mining sector expansion and energy infrastructure modernization projects. Middle Eastern countries are increasing investments in industrial manufacturing zones and transportation infrastructure, creating demand for durable cast components. Latin American automotive manufacturing activities are also supporting growth in aluminum and steel casting production. Regional foundries are gradually adopting modern production technologies and automation systems to improve competitiveness and manufacturing efficiency in global industrial supply chains.

List of Top Metal Casting Companies

- Alcast Technologies Ltd.

- Ahresty Corporation

- Calmet Inc

- Dynacast Ltd

- Endurance Technologies Limited

- GF Casting Solutions

- MES, Inc.

- Proterial, Ltd

- Rheinmetall AG

- Ryobi Limited

Top Two Companies by Market Share

- GF Casting Solutions – 9%

- Dynacast Ltd – 7%

Investment Analysis and Opportunities

Investment activity in the metal casting market continues increasing due to expansion of electric vehicle production, renewable energy infrastructure, and industrial automation systems. Foundry operators are investing heavily in robotic molding systems, automated pouring technologies, digital simulation software, and energy-efficient furnace equipment to improve productivity and reduce manufacturing defects. Nearly 46% of large foundries worldwide have announced modernization projects focused on smart manufacturing integration and sustainable production practices. metal casting market Opportunities are particularly strong in lightweight aluminum casting facilities supporting electric mobility and aerospace manufacturing sectors.

Private equity firms and industrial investors are increasingly targeting advanced casting companies specializing in precision engineering and automated manufacturing capabilities. Infrastructure modernization projects in emerging economies are creating long-term investment potential for steel and iron casting manufacturers supplying construction equipment and transportation systems. Renewable energy expansion is also supporting investments in turbine casting production and industrial machinery manufacturing. The metal casting market Outlook further indicates rising investment in recycled metal processing facilities and low-emission production technologies as sustainability becomes a critical competitive factor across global manufacturing industries.

New Product Development

New product development activities in the metal casting market are heavily focused on lightweight materials, precision engineering, and digitally integrated manufacturing systems. Manufacturers are introducing advanced aluminum alloy castings designed for electric vehicles, aerospace structures, and renewable energy equipment. High-pressure die casting technologies are enabling production of larger and more complex components with improved structural integrity and reduced assembly requirements. Around 38% of casting manufacturers are investing in research related to low-porosity and high-strength casting materials to improve product durability and operational performance.

The metal casting market Trends also highlight increasing use of additive manufacturing-assisted mold production and 3D printed sand molds for prototype development and customized industrial applications. Smart casting technologies equipped with sensor-enabled monitoring systems are improving real-time production quality and reducing operational waste. Steel casting manufacturers are developing heat-resistant and corrosion-resistant alloys for use in offshore energy systems, industrial processing plants, and defense equipment. Automation, digital inspection systems, and environmentally sustainable casting solutions remain central areas of innovation throughout the global metal casting industry.

Five Recent Developments (2023-2025)

- In 2023, GF Casting Solutions expanded lightweight aluminum casting production capacity for electric vehicle structural components in Europe.

- In 2023, Rheinmetall AG introduced advanced steel casting systems for defense and industrial mobility applications.

- In 2024, Dynacast Ltd upgraded automated die casting facilities with robotic process control and digital inspection technologies.

- In 2024, Ahresty Corporation expanded aluminum casting operations to support increasing electric vehicle component demand.

- In 2025, Endurance Technologies Limited invested in energy-efficient casting equipment and advanced machining systems for automotive production.

Report Coverage of Metal Casting Market

The metal casting market Report provides comprehensive analysis of production technologies, raw material utilization, industrial demand patterns, and regional manufacturing developments across global foundry operations. The report evaluates key casting materials including iron, steel, and aluminum while examining major applications across automotive, industrial machinery, construction equipment, aerospace systems, and renewable energy infrastructure. The metal casting market Research Report also includes detailed assessment of manufacturing automation trends, sustainability initiatives, digital foundry technologies, and supply chain developments influencing industry growth.

Request for Customization to gain extensive market insights.

The report coverage further includes competitive landscape analysis, company market share evaluation, investment trends, product innovation strategies, and regional production outlooks across North America, Europe, Asia-Pacific, and Rest of World markets. Detailed segmentation analysis identifies changing demand patterns for lightweight casting materials, precision engineering solutions, and environmentally sustainable production technologies. The metal casting market Insights section highlights major growth drivers, operational challenges, emerging opportunities, and technological advancements shaping the future of the global metal casting industry.

- 2021-2034

- 2025

- 2021-2024

- 70

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us