Micro-LED Display Market Size, Share & Industry Analysis, By Technology (Active Matrix Micro LED, Passive Matrix Micro LED, Reflective Micro LED, and Transparent Micro LED), By Application (Micro LED TVs, Wearable Displays, Smartphone & Tablet Displays, Automotive Displays, and Others), By End User (Residential, Commercial, Healthcare, Industrial, and Others (Transportation, etc.), and Regional Forecast, 2026-2034

MICRO-LED DISPLAY MARKET SIZE AND FUTURE OUTLOOK

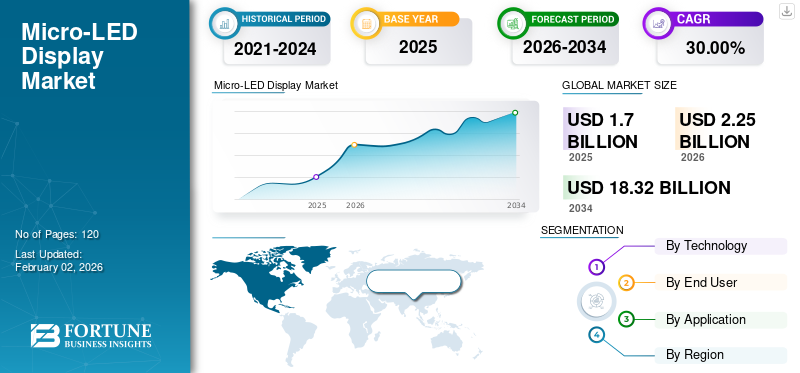

The global micro-LED display market size was valued at USD 1.70 billion in 2025 and is projected to grow from USD 2.25 billion in 2026 to USD 18.32 billion by 2034, exhibiting a CAGR of 30.00% during the forecast period. Asia Pacific dominated the micro-LED display market with a market share of 33.60% in 2025.

A Micro-light emitting diodes (LED) display is referred to an advanced flat panel display technology that utilizes microscopic light-emitting diodes (LEDs) to form an individual pixel. Unlike the conventional LCD or OLED displays, Micro-LED display technology offers a superior brightness, rapid response times, enhanced energy efficiency, and longer lifespan.

The market is growing steadily due to the increasing need for energy efficient and high quality display technologies across consumer electronics including smartwatches, smartphones and televisions. Additionally, its growing adoption in wearable applications and automotive due to superior brightness and low power consumption, further fueling the market growth.

Key players operating in the market include Samsung Electronics, LG Display, Sony Corporation, BOE Technology Group, TCL, Sharp Corporation and others. These players are focusing on strategic partnerships, acquisitions, and mergers to strengthen their technological capabilities.

Download Free sample to learn more about this report.

Micro-LED Display Market Key Takeaways

- 2025 Market Size: USD 1.70 billion

- 2026 Market Size: USD 2.25 billion

- 2034 Forecast Market Size: USD 18.32 billion

- CAGR: 30.00% from 2026–2034

- Asia Pacific dominated the micro-LED display market with a 33.60% share in 2025.

- Reflective Micro LED technology accounted for a 46.79% market share in 2026.

- Wearable displays held a 38.52% share of the global market in 2026.

North America

North America was valued at USD 0.59 Billion in 2025 and is projected to reach USD 0.80 Billion in 2026, driven by strong adoption of premium TVs and AR/XR technologies.

Europe

Europe was valued at USD 0.36 Billion in 2025 and is projected to reach USD 0.47 Billion in 2026, supported by rising demand for energy-efficient displays across automotive and retail sectors.

Asia Pacific

Asia Pacific was valued at USD 0.57 Billion in 2025 and is projected to reach USD 0.73 Billion in 2026, supported by the strong presence of display manufacturing ecosystems across the region.

U.S.

The U.S. market is projected to reach USD 0.56 Billion in 2026, fueled by investments in AR/XR technologies and premium consumer electronics.

Japan

The Japan market is projected to reach USD 0.14 Billion in 2026, supported by strong electronics manufacturing capabilities and growing adoption of advanced display technologies.

Read More

IMPACT OF GENERATIVE AI

Generative AI Drives Efficiency and Demand for Product Leading to Market Expansion

Generative AI is rapidly transforming the market by increasing the demand and production efficient of micro-LED displays. AI generated dynamics and customized or personalized content is growing its applications in AR/XR devices and digital signage, thus boosting the need for highly efficient micro-LED displays.

Additionally, the AI driven design, process optimization and inspection enhances the manufacturing precision, thus improving yield as well as reducing the costs and time to market. These factors strengthen the scalability and affordability, enabling rapid adoption and commercialization of Micro-LED displays.

MARKET DYNAMICS

Market Drivers

Growing Adoption of Ultra-High Brightness & Outdoor Readability Drives the Market Development

The surging adoption of ultra-high brightness and outdoor readability is a significant driver for Micro-LED Display market growth. Unlike the OLED or LCD technologies, Micro-LED displays offer excellent brightness levels and superior contrast, thus ensuring clear visibility even under the direct sunlight or in large outdoor venues. This would enable then an ideal for digital billboards, stadium screens, automotive displays and outdoor retail signage.

With businesses and consumers growingly demanding high performance displays that handle image quality in bright environments, Micro-LED technology stands out for its efficiency and durability. Its ability to offer a wide visual with minimal power consumption improves its appeal across consumer and commercial application. These factors, collaboratively contribute to the overall market growth.

Market Restraints

High Capex & Tooling Maturity Costs Hampers the Market Growth

One of the main restraints in the market include high capital expenditure and tooling maturity costs aligned with production. The manufacturing process includes complex steps including bonding, a precise transfer, and testing of microscopic LEDs that need a highly specialized and expensive equipment. Such processes are yet in early stage of technological maturity, thus leading to a low yield rates and increased operational expenses.

Additionally, the cost of inline testing and repair systems adds to the financial expenses. This would result in different manufacturers hesitate to invest in a large scale production facility, thus reducing the capacity expansion and limiting the widespread commercialization of these displays.

Market Opportunities

Rising Popularity of Transparent Displays to Offer Lucrative Market Growth Opportunities

The increasing awareness of transparent displays offers a significant growth opportunity for the market. Micro-LED technology’s ability to offer exceptional brightness, energy efficiency, and transparency makes it ideal for next generation applications including smart windows, AI integrated glass and retail facades. These displays can transform ordinary glass surfaces into an interactive digital platform, enhancing the brand visibility and user engagement.

Across retail sector, transparent Micro-LED panels enable dynamic advertising without blocking visibility, whereas in architecture sector, it supports in smart building designs with energy saving features. Moreover, the increasing need for mixed and augmented reality tend to experience enhanced adoption of transparent Micro-LED displays.

MICRO-LED DISPLAY MARKET TRENDS

Rising Demand for Premium TV with Halo Expanding Effects Has Emerged as a Prominent Market Trend

The market is noticing a prominent trend owing to the increase in consumer demand for premium televisions integrated with halo expanding effects, thus pushing the adoption of micro-LED displays beyond the commercial showcases to ultra-high end residential use. End users are growingly looking for a superior picture quality, longevity, and brightness, which fuels the need for micro-LED technology.

Additionally, the falling cost per pixel and advancements in micro-LED technology and modular tile designs has allowed it to be more scalable and customizable. This has further encouraged the manufacturers to target luxury home entertainment segments.

Download Free sample to learn more about this report.

IMPACT OF RECIPROCAL TARIFF

Reciprocal Traffic Increases Production Cost, Hindering Market Growth

Reciprocal tariffs significantly impact the market as it increases the cost of importing crucial components and manufacturing equipment. As most of the supply of these products is based in Asia, these tariffs tend to disrupt the trade flow and raise production expenses for global producers.

Higher costs for importing could reduce the profit margins and force companies to absorb losses or pass expenses to the consumers, resulting in an elevated product prices. Additionally, this also reduces the price competitiveness and slower the widespread adoption of micro-LED technology.

SEGMENTATION ANALYSIS

By Technology

Growing Demand for Reflective Micro LED Across AR/XR Headsets Boosts Segment Growth

Based on technology, the market is segmented into Active Matrix Micro LED, Passive Matrix Micro LED, Reflective Micro LED, and Transparent Micro LED.

The reflective micro-LED technology segment is projected to dominate the micro-LED display market, accounting for 46.79% of the global market share in 2026. This dominance is attributed to its crucial role in micro displays that are used across AR/XR headsets and smart glasses. It offers a high brightness level, superior optical efficiency on the silicon backplanes, requires low power and is the first segment to reach the commercial volume. These factors collectively contribute to the segment’s dominance.

Transparent micro-LED segment grew at a highest CAGR of 10.16% in 2024. Such technology aids in emerging advanced and next generation automotive HUDS, smart windows as well as retail displays. As the demand for high-brightness, energy efficiency and see through display is increasing from a low base, the segment is noticing a surge in growth.

By Application

Commercial Viability of Micro-LED Across High-Brightness, Small and Low Power Screens Drives Wearable Displays Segment Growth

The market is divided into micro LED TVs, wearable displays, smartphone & tablet displays, automotive displays, and others, based on application.

Among these, the wearable displays application segment is projected to reach the market, contributing 38.52% globally in 2026. With micro-LED technology securing a commercial viability across high-brightness, small and low power screens, the demand for micro-LED displays across wearable displays is growing. These are used in AR glasses and smart watches, thus aligning with the wearable device performance and size needs.

Additionally, the smartphone & tablet displays segment grew with a highest CAGR of 9.52% in 2024. This growth is owing to the ultra-bright, durable and power efficient panels offered by Micro-LED. This makes it ideal for next generation premium mobile devices with effective mass transfer and maturity in cost structures.

To know how our report can help streamline your business, Speak to Analyst

By End-User

Expanding Demand for B2B Sector Augments the Commercial Segment Growth

Based on the end user, the market is divided into residential, commercial, healthcare, industrial, and others.

The commercial end-user segment will remain the largest category, accounting for 47.85% of the global market share in 2026. This growth is majorly due to the early demand for micro-LED displays across B2B sector. Additionally, the demand for digital signage, corporate walls, and retail or venue displays with a larger format deployments and higher budgets also boosts the segment growth in the market.

On the other hand, the residential segment held highest CAGR of 9.52% in 2024. Decreasing costs and increase in availability of Micro-LED televisions and smart home displays has led to the growth of residential segment. These factors have allowed for rapid consumer adoption of micro-LED displays in homes for decor and entertainment applications.

MICRO-LED DISPLAY MARKET REGIONAL OUTLOOK

Geographically the market is segmented into North America, Europe, Asia Pacific, South America and Middle East & Africa.

Asia Pacific Micro-LED Display Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The market in North America reached USD 0.59 billion in 2025, representing 34.50% of total market revenue, and is projected to reach USD 0.8 billion in 2026. The region is expected to reach USD 0.59 million in 2025. This growth is due to the rapid adoption of premium televisions, upgradation in enterprise and retail signage and investments in heavyweight AR/XR technology by companies such as Apple and meta prominently across the U.S. The U.S. market is projected to reach USD 0.56 billion by 2026.

Europe

Europe contributed approximately USD 0.36 billion to the global market in 2025, accounting for 21.10% share, and is expected to reach USD 0.47 billion in 2026. This growth is attributed to the rising need for high resolution and energy efficient displays across different luxury automotive, consumer electronics, and retail sector. The UK market is projected to reach USD 0.09 billion by 2026 and the Germany market is estimated to reach USD 0.09 billion by 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 0.57 billion, representing 33.60% of global demand, and is projected to grow to USD 0.73 billion in 2026. This growth is attributed to the higher concentration of core micro-LED display supply chain including chips, panels, epitaxy and assembly in South Korea, Japan, China, Taiwan, and others. This drives the early deployment and strong regional demand of Micro-LED displays.

The Japan market is projected to reach USD 0.14 billion by 2026, the China market is estimated to reach USD 0.15 billion by 2026, and the India market is projected to reach USD 0.10 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

South America and Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 0.11 billion in 2025, accounting for 6.60% share, and is expected to reach USD 0.15 billion in 2026. This growth is driven by the increasing investments across smart city projects and adoption of advanced display technology across different sectors in the region. GCC countries are predicted to have a market share of USD 0.04 million by 2025.

Latin America

The Latin America market accounted for USD 0.07 billion in 2025, representing 4.10% of the global industry, and is expected to reach USD 0.09 billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players

Growing Focus of Key Players on Innovation and New Launches Leads to their Dominating Market Positions

The global micro-LED display industry is highly competitive with market players including Samsung Electronics, LG Display, Sony Corporation, BOE Technology Group, TCL, Sharp Corporation, and others operating in the market. These companies are focusing on innovating, cost effective mass transfer techniques that helps in improving yield rates and expand production capabilities.

LIST OF KEY MICRO-LED DISPLAY COMPANIES PROFILED:

- Samsung Electronics (South Korea)

- LG Display (South Korea)

- Sony Corporation (Japan)

- BOE Technology Group (China)

- TCL (China)

- Sharp Corporation (Japan)

- Apple, Inc. (U.S.)

- Innolux (Taiwan)

- AUO Corporation (Taiwan)

- PlayNitride (Taiwan)

- asm OSRAM (Austria)

- Aledia (France)

- VueReal (Canada)

- Sanan Optoelectronics (China)

- Konka Group (China)

KEY INDUSTRY DEVELOPMENTS:

- In May 2025, the Display Week 2025 (SID 2025) officially opened at the San Jose McEnery Convention Center in California. Leading display industry giants, cutting-edge technology companies, and innovative startups around the world gathered to showcase the latest generation of display solutions and products.

- In November 2024, Smartkem, positioned to power the next generation of displays using its disruptive organic thin-film transistors (OTFTs), has partnered with AUO, the largest display manufacturer in Taiwan, to jointly develop the world's first advanced rollable, transparent micro-LED display using Smartkem's technology.

- In January 2024, AUO Corporation unveiled its transparent micro LED display series featuring a 60-inch display at a global professional audiovisual integration event, ISE 2024. This versatile technology seamlessly integrates into diverse settings, delivering an advanced visual experience for applications such as digital signage, commercial displays, corporate meeting rooms, and residential interiors.

- In January 2024, Samsung Electronics announced its latest QLED, MICRO LED, OLED and Lifestyle display lineups ahead of CES 2024. The announcement also served to kick off the AI screen era through the introduction of a next-generation AI processor poised to redefine the perception of smart display In addition to bringing improved picture and sound quality, the new lineups provide consumers with AI-powered features secured by Samsung Knox, focusing on inspiring and empowering individual lifestyles.

- In May 2023, LG Electronics (LG) announced the launch of its new LG MAGNIT (model LBAF) display for virtual production. A huge screen leveraging the company’s cutting-edge Micro LED technology, the new model delivers premium picture quality with deep blacks and vibrant, natural colors, helping directors to create immersive visual experiences. Ideal for film and media production, the new LG MAGNIT is capable of displaying digitally-rendered images in real time; synchronizing with monitors, cameras, camera trackers and production computers so that virtual and live-action elements can be seamlessly blended together.

REPORT COVERAGE

The global report provides a detailed analysis of the market and focuses on key aspects such as prominent companies, deployment modes, types, and end users of the product. Besides this, it offers insights into the market trends and highlights key industry developments and market share analysis for key companies. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Growth Rate | CAGR of 30.00% from 2026-2034 |

| Historical Period | 2021-2024 |

| Unit | Value (USD Billion) |

| Segmentation |

By Technology

By Application

By End User

By Region

|

Frequently Asked Questions

The global micro-LED display market size is projected to grow from USD 2.25 billion in 2026 to USD 18.32 billion by 2034, exhibiting a CAGR of 30.00% during the forecast period.

The market is expected to exhibit steady growth at a CAGR of 30.00% during the forecast period.

Growing adoption of ultra-high brightness & outdoor readability drives the market growth.

Samsung Electronics, LG Display, Sony Corporation, BOE Technology Group, TCL, and Sharp Corporation are some of the top players in the market.

The Asia Pacific region held the largest market share.

North America was valued at USD 0.57 billion in 2025.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us