Micro-Pumps Market Size, Share & Industry Analysis, By Product Type (Mechanical Micro-pumps {Piezoelectric Micro-pumps, Peristaltic Micro-pumps, and Others} and Non-Mechanical Micro-pumps), By Application (Drug Delivery, Dialysis & Renal Care Devices, Diagnostics & Analytical Devices, and Others), By End User (Hospitals & Specialty Clinics, Biotechnology & Pharmaceutical Companies, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

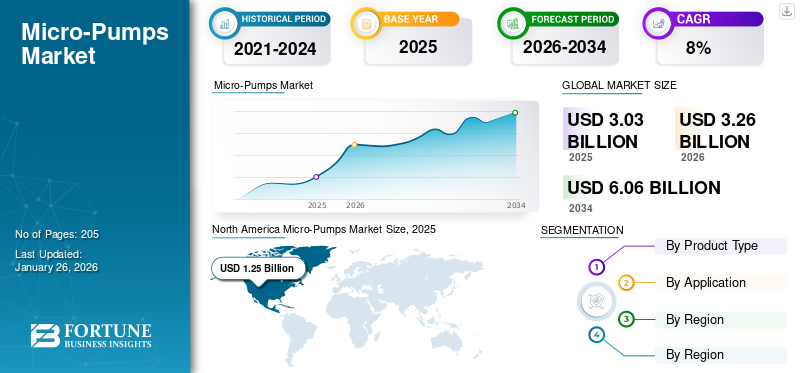

The global micro-pumps market size was valued at USD 3.03 billion in 2025 and market is projected to grow from USD 3.26 billion in 2026 to USD 6.06 billion by 2034, exhibiting a CAGR of 8% during the forecast period. North America dominated the micro-pumps market with a market share of 33.57% in 2025.

Micro pumps are small, package-sized fluid management devices that are capable of precisely controlling and conveying very low volumes of liquids or gases, usually within the microliter to milliliter range. These pumps are extensively used in drug delivery, devices used in dialysis and renal care, diagnostic instruments, and analytical instruments. Micro-pumps enable high dosing accuracy, compatibility with miniaturization, smaller reagent consumption, as well as integration across wearable and portable medical technologies. The market’s growth is attributed to increasing demand for point-of-care diagnostics, a rising shift of preference for wearable devices, and growing investments in pharmaceutical and biotechnology research.

The market is highly competitive with major players such as KNF Neuberger GmbH, TTP Ventus Ltd., Bartels Mikrotechnik GmbH, and Xavitech AB holding considerable market share. Broad product portfolios, strong partnerships, and continuous investment in innovation have enabled these companies to maintain their dominance in the global market.

Download Free sample to learn more about this report.

Micro-Pumps MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.03 billion

- 2026 Market Size: USD 3.26 billion

- 2034 Forecast Market Size: USD 6.06 billion

- CAGR: 8% from 2026–2034

- North America dominated the micro-pumps market with a 33.57% share in 2025.

- Mechanical segment led the market with a 70.64% share in 2026 due to high precision and reliability in healthcare applications.

- Drug delivery segment held a 66.58% share in 2026 driven by rising demand for chronic disease management therapies.

North American

North America led the market with USD 1.35 billion in 2026, supported by strong adoption of advanced drug delivery systems and product approvals.

Europe

Europe reached USD 0.84 billion in 2025, driven by strong healthcare infrastructure and increasing adoption of wearable drug delivery systems.

Asia Pacific

Asia Pacific is a high-growth region, supported by expanding healthcare infrastructure and rapid adoption of connected medical devices.

U.S.

Market estimated at USD 1.21 billion in 2026, driven by strong insulin pump adoption and advanced biotech innovations.

Japan

Market estimated at USD 0.14 billion in 2026, supported by aging population needs and advanced healthcare technology adoption.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Growth Miniaturization of Life-Science Instruments and Point-of-Care Expansion to Propel Market Growth

The growing move toward compact, portable, and automated life-science systems is a major driver for the use of micro pumps. Handheld drug-delivery units, benchtop analyzers, wearable diagnostics, and microfluidic pump systems rely on highly precise, low-flow pumping with minimal pulsation, and strong chemical compatibility. Moreover, as manufacturers redesign equipment for home use and decentralized care, micro-pumps make it possible to achieve accurate dosing, conserve reagents, and maintain consistent flow at microliter to milliliter levels.

- In October 2020, TTP Ventus and Sensirion AG entered into a strategic collaboration for the development of a cutting-edge microfluidic driver. The companies are developing this new technology for applications in laboratory and analytical testing.

MARKET RESTRAINTS

Cost and Integration Complexity to Deter Market Growth

The cost of the product coupled with their integration complexity is prominently expected to hamper the micro-pumps market growth. Despite technical advantages, the total cost of ownership and integration effort can slow adoption, especially for price-sensitive, high-volume devices. In addition, ensuring long life under aggressive solvents, biofouling, and sterilization cycles adds design complexity.

- In March 2024, InfuTronix recalled its estimated 52,000 infusion pumps from the market due to micro pump malfunctioning. Moreover, the device also faced irregular flow rates along with leakages.

In order to deal with such a situation, it has become critical to integrate advanced micro pump technology in the medical devices, which further leads to an increase in overall cost.

MARKET OPPORTUNITIES

Rising Adoption of Wearables and Connected Drug Delivery Devices Offer Lucrative Opportunity

Increasing adoption of wearable and connected devices worldwide is estimated to offer a substantial opportunity for market growth. These solutions require highly precise miniature pumps that can deliver accurate doses of medication safely in home or outpatient settings. Moreover, these pumps are well-suited for this role due to their compact design, precision, and adaptability. At the same time, diagnostic tools and biotech laboratories are increasingly adopting single-use fluid pathways to minimize contamination and accelerate testing, further boosting the need for micro pump modules.

MARKET CHALLENGES

Stringent Government Regulations to Offer Substantial Challenge for the Market

One of the biggest challenges for the micro pumps market is the strict regulatory requirements for medical devices. Micro pumps are often part of drug delivery systems or diagnostic equipment, making them mandatory to meet tough standards for safety, quality, and reliability. This extra testing for biocompatibility, sterilization, and electronic safety, makes the development process longer and expensive for manufacturers. Smaller companies, in particular, face difficulties because of the high cost and time needed to meet these requirements.

MICRO-PUMPS MARKET TRENDS

Shift toward Adoption of Smart, Miniaturized, and Integrated Pumps is a Key Market Trend

One of the most notable trends in the global micro pumps market is the preference for the adoption of fully integrated smart pumping systems. Instead of distributing only pumps alone, manufacturers are delivering pre-engineered subsystems that include the pump, sensors, control electronics, and ready-to-use software interfaces. This approach shortens integration timelines for OEMs, cuts development expenses, and enhances reliability by validating system-level performance before deployment. In healthcare, the shift is especially evident with the rise of wearable and smart drug delivery pumps and point-of-care diagnostics, both of which demand compact, energy-efficient, and intelligent pumps capable of precise dosing and fluid management in real-world applications.

- In August 2023, CEME Group and Micropump announced a partnership agreement to offer an integrated and advanced fluid control system, which can be utilized in a wide range of industrial as well as healthcare applications.

Download Free sample to learn more about this report.

Segmentation Analysis

By Product Type

Superior Accuracy and Durability of Mechanical Pumps Positively Impact Segment Growth

On the basis of product type, the market is divided into mechanical and non-mechanical pumps.

To know how our report can help streamline your business, Speak to Analyst

The mechanical segment accounted for the highest micro-pumps market share in 2026, representing 70.64% of the total market share, supported by its strong presence in healthcare and reputation for accuracy, durability, and versatility. Moreover, their proven capability to manage diverse fluids, from viscous medications to biological solutions, makes them the preferred option for device manufacturers. Further, their widespread applications in insulin pumps, dialysis systems, and laboratory analyzers fuel their adoption across hospitals and clinics.

- For instance, in December 2022, Micropump, Inc. announced a strategic collaboration with Kelair Pumps Australia Pty Ltd. to consolidate their distribution channel in Australia.

By Application

Increasing Adoption of Drug Delivery Devices Boost Segment’s Growth

Based on application, the market is segmented into drug delivery, dialysis & renal care devices, diagnostics & analytical devices, and others.

The drug delivery segment captured the largest share of the market in 2025. In 2026, the segment is anticipated to dominate with a 66.58% share. The growth of the drug delivery segment is attributed to an increasing prevalence of chronic conditions such as diabetes, cancer, and autoimmune diseases. Wearable insulin pumps, patch injectors for biologics, and implantable delivery systems majorly depend on micro pumps to provide highly accurate, repeatable dosing with minimal error. Further, rising demand for self-administered treatments and the transition from hospital-centered care to home-based therapy further strengthen the segment’s growth.

- According to the Association of Diabetes Care & Education Specialists, an estimated 0.35 to 0.51 million people in the U.S. use insulin pumps for drug delivery.

Also, the diagnostics & analytical devices segment is expected to grow at a CAGR of 9.5% over the forecast period.

By End User

Hospitals & Specialty Clinics are Leading End Users as they are Primary Customers for Micro-pump Enabled Medical Devices

Based on end user, the market is segmented into hospitals & specialty clinics, biotechnology & pharmaceutical companies, and others.

The hospitals & specialty clinics segment dominated the global micro-pumps market with a market share of 56.38% in 2026, due to a substantial installed base of dialysis machines, infusion pumps, and analytical instruments in these facilities. With the rising number of patients undergoing chronic therapies such as insulin delivery and renal care, hospitals remain the most important customers for micro pump-enabled medical devices. The ability to provide advanced monitoring, routine maintenance, and integrated services within these settings consolidates their market share. For 2026, the segment is set to hold 56.38% market share.

Biotechnology & pharmaceutical companies are projected to grow at a CAGR of 8.3% during the study period.

Micro-Pumps Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America Micro-Pumps Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the leading share of the market, valued at USD 1.25 billion in 2025, and continued its dominance in 2026, reaching USD 1.35 billion. The factors fostering the dominance of the region include considerable adoption of drug delivery devices, technological advancements, and product approvals. In 2026, the U.S. market is estimated to reach USD 1.21 billion.

- For instance, in November 2023, PSG Biotech announced the launch of Quattroflow QB2-SD, a single-use micropump.

Asia Pacific is expected to exhibit the fastest CAGR during the forecast period. Europe is also projected to witness a notable growth with a growth rate of 7.3%, and touch a valuation of USD 0.84 billion in 2025. This is primarily due to the extensive healthcare infrastructure and the growing adoption of wearable and connected drug delivery devices. Backed by these factors, the UK market is projected to reach USD 0.12 billion by 2026, while the Germany market is projected to reach USD 0.21 billion by 2026. The market in Asia Pacific is estimated to reach USD 0.65 billion in 2025. In the region, the Japan market is projected to reach USD 0.14 billion by 2026, the China market is projected to reach USD 0.28 billion by 2026, and the India market is projected to reach USD 0.1 billion by 2026.

Latin America and the Middle East & Africa are anticipated to record moderate growth. In 2025, Latin America will seize USD 0.14 billion due to the region’s developing healthcare infrastructure and rising demand for drug delivery devices. In the Middle East & Africa, GCC is set to capture USD 0.07 billion in 2025.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation, R&D, and Partnerships is Underpinning the Dominance of Leading Firms

The global market characterizes large companies with global presence and small and mid-size firms with a strong presence. R&D, innovation in micro pumps, and partnering with domestic organizations to expand regional presence are strategies opted by market participants for their development. Medtronic plc, Insulet Corporation, Tandem Diabetes Care, Debiotech SA, and Sensile Medical are few big names recognized for their innovation in the micro-pumps market.

Apart from these, TTP Ventus, Bartels Mikrotechnik GmbH, Dolomite Microfluidics, and Xavitech AB are also striving to cement their position via introduction of novel devices, early approvals from regulatory bodies, and other strategic initiatives.

LIST OF KEY MICRO-PUMPS COMPANIES PROFILED

- Medtronic plc. (Ireland)

- Insulet Corporation (U.S.)

- Tandem Diabetes Care (U.S.)

- Debiotech SA (Switzerland)

- Sensile Medical (Switzerland)

- Ypsomed AG (Switzerland)

- SOOIL Development (South Korea)

- Medela AG (Switzerland)

- TTP Ventus (U.K.)

- Micropump Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- May 2023: Medtronic announced its plan to acquire EOFlow Co., Ltd to consolidate its market position in the wearable insulin patch market.

- December 2022: Tandem Diabetes Care announced the acquisition of AMF Medical with an aim to strengthen its share in the insulin delivery market.

- September 2022: The Lee Company announced the acquisition of TTP Ventus Limited from TTP Group in order to consolidate its presence in the micro-pump and pump modules market.

- November 2020: MilliporeSigma and Dolomite Microfluidics announced a strategic partnership to manufacture controlled drug delivery technologies.

- May 2020: KNF announced the launch of its new and compact high-performance pumps.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 8% from 2026-2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Product Type, Application, End User, and Region |

|

By Product Type |

· Mechanical Micro-pumps o Piezoelectric Micro-pumps o Peristaltic Micro-pumps o Others · Non-Mechanical Micro-pumps |

|

By Application |

· Drug Delivery · Dialysis and Renal Care Devices · Diagnostics & Analytical Devices · Others |

|

By End User |

· Hospitals & Specialty Clinics · Biotechnology & Pharmaceutical Companies · Others |

|

By Geography |

· North America (By Product Type, Application, End User, and Country) o U.S. § By Product Type o Canada § By Product Type · Europe (By Product Type, Application, End User, and Country/Sub-region) o Germany § By Product Type o U.K. § By Product Type o France § By Product Type o Spain § By Product Type o Italy § By Product Type o Scandinavia § By Product Type o Rest of Europe § By Product Type · Asia Pacific (By Product Type, Application, End User, and Country/Sub-region) o China § By Product Type o Japan § By Product Type o India § By Product Type o Australia § By Product Type o Southeast Asia § By Product Type o Rest of Asia Pacific § By Product Type · Latin America (By Product Type, Application, End User, and Country/Sub-region) o Brazil § By Product Type o Mexico § By Product Type o Rest of Latin America § By Product Type · Middle East & Africa (By Product Type, Application, End User, and Country/Sub-region) o GCC § By Product Type o South Africa § By Product Type o Rest of the Middle East & Africa § By Product Type |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.03 billion in 2025 and is projected to reach USD 6.06 billion by 2034.

In 2025, the market value stood at USD 3.03 billion.

The market is expected to exhibit a CAGR of 8% during the forecast period of 2026-2034.

The mechanical pump segment led the market by product type.

The key factors driving the market are the rising adoption of wearable drug delivery devices and the installed base of dialysis machines.

Medtronic plc, Insulet Corporation, Tandem Diabetes Care, Debiotech SA, and Sensile Medical are some of the prominent players in the market.

North America dominated the market in 2026.

- 2021-2034

- 2025

- 2021-2024

- 205

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us