Microcars Market Size, Share & Industry Analysis, By Propulsion (Internal Combustion Engine (ICE) Microcars and Electric Microcars), By Seating Capacity (2-Seater Microcars and 3 & 4 Seater Microcars), By Speed Category (Low-Speed Microcars (≤45 km/h), Medium-Speed Microcars (46–70 km/h), and High-Speed Microcars (>70 km/h)), By Application (Personal Urban Mobility and Commercial & Utility Use) and Regional Forecast, 2026-2034

Microcars Market Size and Future Outlook

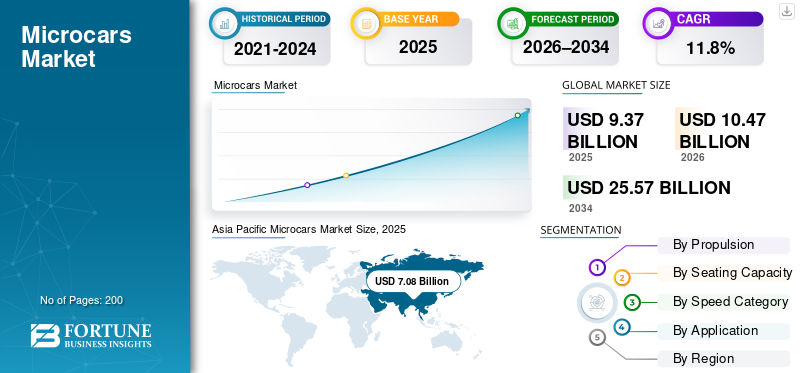

The global microcars market size was valued at USD 9.37 billion in 2025. The market is projected to grow from USD 10.47 billion in 2026 to USD 25.57 billion by 2034, exhibiting a CAGR of 11.8% during the forecast period. Asia Pacific dominated the microcars market with a market share of 75.56% in 2025.

Microcars are ultra-compact, lightweight vehicles designed primarily for urban mobility, typically offering two to four seats, limited power and speed, and optimized for short-distance travel, low emissions, easy parking, and high energy efficiency. The market growth is driven by rapid urbanization, traffic congestion, rising fuel and ownership costs, stricter emission regulations, and growing demand for affordable electric mobility. Expansion of shared mobility, last-mile delivery needs, and supportive city-level policies further accelerate the adoption of microcars. Major players in the global microcars ecosystem, including Stellantis, SAIC-GM-Wuling, Renault Group, Geely, Ligier, Aixam, and Micro Mobility Systems, are focusing on electrification, cost-optimized platforms, localized manufacturing, and expanding microcars into shared mobility and urban delivery applications to strengthen their competitiveness.

Download Free sample to learn more about this report.

MICROCARS MARKET TRENDS

Urban Space Optimization and Compact Mobility Redefine City Transport Trends

Microcars are increasingly positioned as an efficient response to shrinking urban space, congestion, and parking scarcity. Cities worldwide are struggling to expand road infrastructure at the same pace as vehicle ownership, driving demand for ultra-compact vehicles that reduce spatial footprint without eliminating personal mobility. Microcars enable higher parking density, smoother traffic flow on narrow streets, and improved compatibility with historic city centers. Their compact dimensions make them particularly attractive for dense European and Asian cities where parking availability is a critical constraint. As urban planners emphasize space-efficient transport solutions, microcars are becoming integral to city mobility ecosystems alongside public transit and micromobility. In October 2024, Citroen reported cumulative global sales of over 65,000 units of the Ami electric microcar, highlighting strong adoption in congested European cities.

MARKET DYNAMICS

MARKET DRIVERS

Affordability and Low Total Cost of Ownership Sustain Market Growth Drivers

Cost effectiveness remains a powerful force supporting global microcars demand, particularly among first-time buyers, secondary-car households, and budget-conscious urban users. Microcars typically offer significantly lower purchase prices, reduced insurance costs, minimal maintenance requirements, and lower fuel or electricity consumption compared to conventional passenger vehicles. These advantages are particularly pronounced in emerging economies, where income sensitivity is high and personal mobility remains crucial. Electric microcars further strengthen this driver by offering predictable operating costs and reduced exposure to fuel price volatility. As inflation and living costs rise globally, consumers are increasingly prioritizing practical and economical mobility solutions, which microcars are well-positioned to deliver. In December 2024, SAIC-GM-Wuling confirmed that its Hong Guang MINI EV remained among China’s best-selling electric vehicles due to its ultra-low pricing and operating costs. These efforts drive the microcars market growth.

MARKET RESTRAINTS

Safety Perception and Regulatory Limitations Restrict Wider Adoption

Safety concerns continue to restrain broader microcar adoption, particularly in markets dominated by high-speed traffic. Many microcars operate under quadricycle or low-speed vehicle regulations, which often require fewer safety features than full passenger cars. Limited crash protection, lower structural rigidity, and reduced top speeds can affect consumer confidence, primarily when used in mixed traffic. Regulatory restrictions on road access further limit usability, confining many microcars to urban or controlled environments. These factors collectively prevent microcars from replacing conventional vehicles for a broader range of driving needs. Addressing safety perception remains critical for unlocking mass-market acceptance beyond niche urban applications. In December 2025, Renault announced the discontinuation of its Mobilize Duo microcar program, citing regulatory complexity and limited scalability as key constraints.

MARKET OPPORTUNITIES

Electrified Last-Mile Logistics Opens New Commercial Opportunities

The rapid expansion of e-commerce and urban delivery services is creating strong opportunities for electric microcars in last-mile logistics. Compact size, low operating cost, and ease of maneuvering make microcars well-suited for dense city delivery routes with frequent stops. Municipal restrictions on emissions and access are further encouraging logistics operators to adopt zero-emission, space-efficient vehicles. Electric microcars can operate in low-emission zones, reduce noise pollution, and lower fleet operating expenses. As urban delivery volumes rise, microcars are increasingly viewed as a viable alternative to larger vans for small-load, high-frequency delivery operations. In June 2024, La Poste Group expanded trials of compact electric vehicles for urban parcel delivery to reduce emissions and congestion in French city centers.

MARKET CHALLENGES

Fragmented Global Regulations Challenge Scalable Market Expansion

A significant challenge facing the global market is the lack of harmonized regulatory frameworks across regions. Vehicle classifications, safety requirements, speed limits, and licensing rules vary significantly between Europe, the Asia Pacific, North America, and other regions. This fragmentation forces manufacturers to develop region-specific models, increasing development costs and limiting economies of scale. A microcar approved under European quadricycle regulations may not be eligible for road use in the U.S. or certain parts of Asia. Regulatory inconsistency complicates global expansion strategies and slows investment decisions, posing a structural challenge to long-term market standardization. In March 2023, the European Commission reaffirmed that L6e and L7e quadricycles remain subject to region-specific approval rules, limiting cross-market vehicle standardization.

Download Free sample to learn more about this report.

Segmentation Analysis

By Propulsion

Cost-Efficient Powertrains Sustain ICE Microcars’ Market Leadership

Based on propulsion, the market is segmented into Internal Combustion Engine (ICE) microcars and electric microcars.

ICE microcars dominate global volumes due to their affordability, established supply chains, ease of refueling, and minimal infrastructure requirements. In emerging and price-sensitive markets, ICE microcars remain the preferred option for personal mobility and small commercial use, particularly where charging infrastructure is limited. Their mechanical simplicity enables low maintenance costs and easier servicing, supporting continued adoption. While electrification is accelerating, ICE microcars retained dominance in 2025, as regulatory flexibility, lower upfront pricing, and wide fuel availability continue to outweigh the benefits of electrification for a large consumer base.

The electric microcars segment is projected to grow at a CAGR of 13.2% over the forecast period.

By Seating Capacity

Multi-Passenger Utility Drives 3 & 4-Seater Microcars Segment Expansion

Based on seating capacity, the market is segmented into 2-seater microcars and 3 & 4-seater microcars.

The 3 & 4-seater microcars segment dominates the market due to its broader usability across families, shared mobility fleets, and small commercial applications. These vehicles strike a balance between compact dimensions and functional passenger capacity, making them suitable as primary urban vehicles rather than niche solutions. Rising demand for flexible, space-efficient alternatives to conventional hatchbacks supports strong adoption. Additionally, higher perceived value and practicality drive stronger purchase intent, particularly in the Asia Pacific and Europe.

2-seater microcars are experiencing steady growth in the microcars market, due to demand from single urban commuters, elderly users, and shared mobility operators who prioritize ultra-compact size, low energy consumption, and minimal operating costs.

The 3 & 4 seater microcars segment is projected to grow at a CAGR of 12.5% over the forecast period.

By Speed Category

Urban Compatibility Positions Medium-Speed Microcars as the Core Market Segment

Based on speed category, the market is segmented into low-speed, medium-speed, and high-speed microcars.

Medium-speed microcars dominate as they offer an optimal balance between regulatory compliance and real-world usability. Capable of operating safely in mixed urban traffic, they address broader commuting needs than low-speed models while remaining more affordable and efficient than high-speed variants. This segment benefits from wider road access, improved safety perception, and suitability for daily commuting. Urban infrastructure compatibility and regulatory acceptance across multiple regions reinforce its leadership.

The high-speed microcars segment is projected to grow at a CAGR of 15.5% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Daily Commuting Needs Anchor Personal Urban Mobility Segment Dominance

Based on application, the market is segmented into personal urban mobility and commercial & utility use.

Personal urban mobility dominates as microcars are primarily adopted for daily commuting, short trips, and secondary household transportation. Their compact size, ease of parking, and low operating costs align well with individual urban lifestyles. Congestion concerns, limited parking availability, and rising ownership costs of conventional cars are factors that reinforce growth. While fleet applications are expanding rapidly, personal ownership remains the largest demand base, driven by consistent and repeat usage patterns in densely populated cities.

The commercial & utility use segment is projected to grow at a CAGR of 15.4% over the forecast period.

MICROCARS MARKET REGIONAL OUTLOOK

By geography, the market is categorized into Europe, North America, Asia Pacific, and the rest of the world.

Asia Pacific

Asia Pacific Microcars Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific dominated with the largest microcars market share due to high urban density, cost sensitivity, and large-scale adoption of compact electric vehicles. China leads with mass-market micro EVs, while Japan and India contribute through structured urban mobility solutions and regulatory-backed vehicle categories. Growth is fueled by affordability, electrification, and suitability for urban areas with high congestion. Microcars are increasingly used for personal commuting, shared mobility, and small commercial operations. Strong local manufacturing ecosystems and supply chain advantages further support rapid scaling. Asia Pacific remains the fastest-growing region in both volume and value terms.

China Microcars Market

China is the global growth engine for microcars valued at USD 5.92 billion in 2025, driven by widespread adoption of low-cost electric micro vehicles for urban commuting. Strong manufacturing scale, affordability, supportive local policies, and dense city environments enable China to dominate global microcar volumes.

Japan Microcars Market

Japan’s market benefits from ultra-compact mobility concepts tailored for short-distance travel and aging populations. Government-backed frameworks, strong OEM participation, and high urban density support steady growth, particularly for electric microcars designed for use in neighborhoods and city centers. Japan is expected to grow with a CAGR of 20% during the forecast period.

India Microcars Market

India’s market is emerging with a growth rate of 16.5%, driven by affordability needs, urban congestion, and formal recognition of quadricycle categories. Growth is supported by small commercial use, last-mile mobility, and gradual electrification, though infrastructure and safety perception remain moderating factors.

North America

North America represents a niche but steadily expanding market, driven primarily by urban utility use, gated communities, campuses, and fleet operations. Growth is supported by rising interest in low-speed electric vehicles for controlled environments, sustainability-focused municipal fleets, and cost-efficient mobility solutions. While consumer adoption remains limited due to safety concerns and speed restrictions on roads, commercial and institutional demand is strengthening. Regulatory acceptance of low-speed vehicles and incentives for electrification contribute to a gradual expansion of the market. Mexico adds incremental volume through affordable urban mobility and small commercial applications, while overall growth remains slower than in other regions due to infrastructure and cultural preferences.

U.S. Microcars Market

The U.S. market is driven by low-speed electric vehicles used on campuses, in retirement communities, at industrial sites, and in delivery fleets. Growth valued at USD 0.31 billion is supported by electrification, fleet economics, and sustainability mandates. However, widespread personal adoption remains constrained by safety concerns and highway-oriented infrastructure.

Europe

Europe is a mature and structurally well-defined market, supported by formal quadricycle regulations, dense urban environments, and strong environmental policies. City-level emission restrictions, congestion mitigation strategies, and long-standing consumer acceptance of micro mobility drive growth. France, Italy, and Germany anchor demand, while electrification accelerates the replacement of legacy ICE quadricycles. The region benefits from established OEMs, diverse product offerings, and supportive regulatory frameworks. As urban access rules tighten, microcars increasingly serve as practical alternatives to conventional cars for short-distance travel, sustaining stable growth across both personal and shared mobility applications.

U.K. Microcars Market

The U.K. market remains a niche market valued at USD 0.17 billion, but stable one, supported by urban congestion challenges and the growing demand for low-speed vehicle usage in controlled environments. Adoption is limited compared to continental Europe, and interest is gradually increasing in electric quadricycles for city commuting and short-distance personal mobility.

Germany Microcars Market

Germany’s market is driven by urban sustainability goals and demand for compact mobility in densely populated cities. While safety concerns limit large-scale adoption, interest in electric quadricycles is on the rise, driven by environmental awareness, pilot urban mobility programs, and the expansion of electric vehicle ecosystems.

Rest of the World

The rest of the world market, including Latin America, the Middle East, and Africa, exhibits growing interest in microcars for urban mobility and utility applications. Rising fuel costs, dense urban centers, and demand for low-cost transportation drive growth. Adoption is primarily fleet- and utility-led, with electric microcars gaining traction where charging access is available. However, infrastructure limitations and regulatory inconsistency slow widespread penetration. Despite these constraints, the region presents long-term growth potential as affordable electric mobility solutions become more accessible.

COMPETITIVE LANDSCAPE

Key Industry Players

Lightweight Vehicle Platforms, Electrification, and Strategic Partnerships Shape Microcars Market Competitiveness

The global microcars market trends are shaped by the specialization of compact vehicles, electrification, and region-specific regulatory frameworks, with competition driven by affordability, urban suitability, and manufacturing efficiency. Leading players, including Stellantis, SAIC-GM-Wuling, Geely, Renault Group, Ligier, Aixam, and Micro Mobility Systems, compete through lightweight vehicle architectures, cost-optimized platforms, and the increasing electrification of microcar portfolios. Manufacturers focus on modular designs, localized production, and simplified component ecosystems to control costs while meeting safety and emission norms. Competitive differentiation is strengthened through battery integration, extended urban driving range, and digital connectivity features tailored to city use. Strategic partnerships with battery suppliers, electronics providers, and mobility service operators support faster product development and market access. Companies are also expanding microcar applications into shared mobility and last-mile delivery, while leveraging government incentives and city-level policies to reinforce adoption in dense urban environments worldwide. In June 2023, Fiat officially launched the fully electric Topolino microcar, targeting affordable urban mobility in European cities and reinforcing Stellantis’ strategy to scale cost-efficient electric microcars across dense metropolitan markets.

LIST OF KEY MICROCARS COMPANIES PROFILED

- Stellantis N.V. (Netherlands)

- Renault Group (France)

- Smart Automobile Co., Ltd. (China)

- Toyota Motor Corporation (Japan)

- SAIC-GM-Wuling Automobile Co., Ltd. (China)

- Geely Automobile Holdings Ltd. (China)

- Chery Automobile Co., Ltd. (China)

- BAIC Group (China)

- Bajaj Auto Ltd. (India)

- Ligier Group (France)

- Aixam Mega S.A.S. (France)

- Mahindra & Mahindra Ltd. (India)

- suzuki motor corporation (Japan)

- Honda Motor Co Ltd. (Japan)

- Micro Mobility Systems AG (Switzerland)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Bolt launched its “Little Bolt” microcar ride-hailing category pilot in Nuremberg, Germany, focusing on compact electric vehicles for inner-city mobility. The initiative aims to offer affordable, urban-friendly transportation alternatives to traditional taxis and ride-hailing services, highlighting the role of microcars in sustainable city travel.

- December 2025: Fiat confirmed plans to introduce the tiny electric Topolino to the U.S. in 2026, following its showcase during Miami Art Week. The announcement signals increasing interest in microcars/quadricycles beyond Europe and highlights a strategy to test demand for ultra-compact urban EVs under low-speed or neighborhood-use conditions.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 11.8% from 2026 to 2034 |

|

Unit |

Value (USD Billion), & Volume (Thousand Units) |

|

Segmentation |

By Propulsion, By Seating Capacity, By Speed Category, By Application, and By Region. |

|

By Propulsion |

· Internal Combustion Engine (ICE) Microcars · Electric Microcars |

|

By Seating Capacity |

· 2-Seater Microcars · 3 & 4 Seater Microcars |

|

By Speed Category |

· Low-Speed Microcars (≤45 km/h) · Medium-Speed Microcars (46–70 km/h) · High-Speed Microcars (>70 km/h) |

|

By Application |

· Personal Urban Mobility · Commercial & Utility Use |

|

By Geography |

· North America (By Propulsion, By Seating Capacity, By Speed Category, By Application, and By Country) o U.S. (By Propulsion) o Canada (By Propulsion) o Mexico (By Propulsion) · Europe (By Propulsion, By Seating Capacity, By Speed Category, By Application, and By Country) o Germany (By Propulsion) o U.K. (By Propulsion) o France (By Propulsion) o Rest of Europe (By Propulsion) · Asia Pacific (By Propulsion, By Seating Capacity, By Speed Category, By Application, and By Country) o China (By Propulsion) o Japan (By Propulsion) o India (By Propulsion) o South Korea (By Propulsion) o Rest of Asia Pacific (By Propulsion) · Rest of the World (By Propulsion, By Seating Capacity, By Speed Category, and By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 9.37 billion in 2025 and is projected to reach USD 25.57 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 7.08 billion.

The microcars market demand is expected to grow at a CAGR of 11.8% during the forecast period of 2026-2034.

By application, the personal urban mobility segment led the market.

Affordability and low total cost of ownership are the key factors driving the market.

Key market players include Stellantis, SAIC-GM-Wuling, Renault Group, BAIC, and Geely.

Asia Pacific accounted for the largest share of the market in 2025.

North America, Europe, Asia Pacific, and the rest of the world.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us