Nanosatellite and Microsatellite Market Size, Share & Industry Analysis, By Type (Nanosatellites (1 to 10 kg) and Microsatellites (10 to 100 kg)), By Component (Payload, Telemetry, Tracking, and Command (TT&C), Power System, Propulsion System, Command & Data Handling (C&DH), and Others), By Application (Communication, Earth Observation & Remote Sensing, Scientific Research & Exploration, Defense, Security & Intelligence, and Navigation, and Positioning & Timing), By Orbit (Low Earth Orbit, Medium Earth Orbit, and Highly Elliptical Orbit), By End Use, and Regional Forecast, 2026-2034

Microsatellite and Nanosatellite Market Size

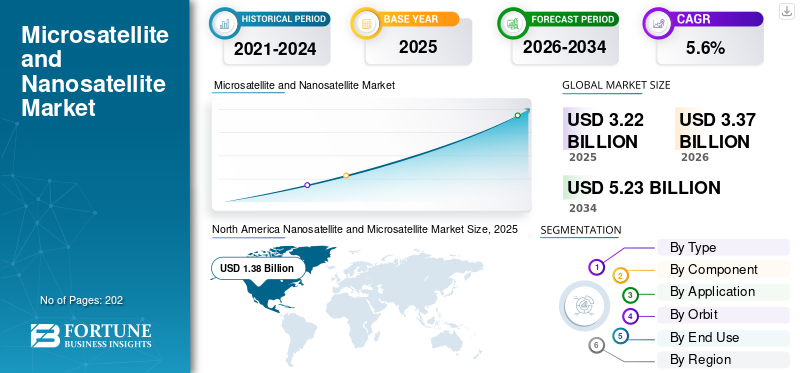

The global nanosatellite and microsatellite market size was valued at USD 3.22 billion in 2025. The market is projected to grow from USD 3.37 billion in 2026 to USD 5.23 billion by 2034, exhibiting a CAGR of 5.6% during the forecast period. North America dominated the global nanosatellite and microsatellite market with a market share of 42.86% in 2025.

A nanosatellite is a satellite with a mass between 1 and 10 kilograms. These satellites are compact and include commonly known satellite formats, such as CubeSats, which are built in standard units. Nanosatellites are cost-effective, have shorter development cycles, and are widely used for communication, commercial, and research purposes in space. Microsatellites are larger in size as compared to nanosatellites, with a mass range typically between 11 and 100 kilograms.

The major players in the market include Planet Labs, Sierra Nevada Corporation, GomSpace, NanoAvionics, Axelspace, Terran Orbital, AAC Clyde Space, and Surrey Satellite Technology. These companies offer a wide range of satellite products such as platforms, payloads, propulsion systems, and integrated services. GomSpace specializes in the design, manufacturing, and operation of nanosatellite and CubeSat solutions. AAC Clyde Space supplies CubeSat and nanosatellite solutions, components, and space-based data services, supporting geospatial intelligence and maritime applications.

Download Free sample to learn more about this report.

Nanosatellite and Microsatellite Market Key Takeaways

- 2025 Market Size: USD 3.22 billion

- 2026 Market Size: USD 3.37 billion

- 2034 Forecast Market Size: USD 5.23 billion

- CAGR: 5.6% from 2026–2034

- North America dominated the nanosatellite and microsatellite market with a 42.86% share in 2025.

- The power system segment is expected to grow at a steady rate of 4.7% over the forecast period.

- The defense, security & intelligence segment is set to grow at the fastest CAGR of 7.0% over the forecast period.

North America

North America held a 42.86% share in 2025, valued at USD 1.38 billion.

Asia Pacific

Asia Pacific is projected to grow significantly due to increasing investments in space technologies and satellite launches.

Europe

Europe is expected to witness steady growth driven by rising defense space budgets and environmental monitoring programs.

U.S.

The U.S. market is projected to witness growth driven by rising military ISR programs and proliferated LEO satellite deployments.

Japan

The Japan market is projected to witness growth supported by increasing investments in communication, navigation, and scientific satellite missions.

Read More

MARKET DYNAMICS

MARKET DRIVERS

Rapid Deployment of Satellite Technologies for Diverse Applications to Drive Market Growth

The world is experiencing the rapid deployment of satellite technologies, which enable faster access to critical data for a wide range of applications. Moreover, there is a rise in space exploration and increased demand for satellite technologies and their data for various sectors such as Earth observation, communication, and tracking & navigation. Various commercial and military organizations are increasingly adopting satellite solutions for diverse use cases such as communication, weather monitoring, border monitoring, and others. The ability to deploy satellite systems rapidly enhances operational efficiency and responsiveness, which is increasingly important in dynamic and evolving markets. Moreover, there is an increase in the development and deployment of nano or microsatellites in space to support applications of a wide range of commercial industries.

- For instance, in January 2025, FOSSA Systems, a Spanish aerospace startup, launched three new nanosatellites aboard SpaceX’s Falcon 9 on the Transporter 12 mission from Vandenberg Air Force Base. These nanosatellites aim to enhance global IoT connectivity by providing satellite roaming capabilities, supporting industries such as energy, logistics, and national security.

MARKET RESTRAINTS

Limited Lifespan and Durability of Small Satellites in Harsh & Adverse Space Environment to Hamper Market Expansion

The restraint that negatively affects the overall market for nanosatellite and microsatellite is the limited lifespan and durability of small satellites in harsh space environments. These satellites are more vulnerable to degradation from radiation, extreme temperatures, and space debris. Due to susceptibility, these types of small satellites can lead to reduced operational life and increased maintenance or replacement expenses. All of these factors are anticipated to create difficulties for the use of such satellites in long-term missions. Therefore, the adoption of small satellites can be hindered by these reasons, which may hamper the growth of the nanosatellite and microsatellite industry.

MARKET OPPORTUNITIES

Expanding Military Adoption of Small Satellites Driven by Rising Defense Budgets Provide Significant Market Opportunities

The surge in defense budgets worldwide is driving the significant adoption of military nanosatellites and microsatellites, which is expected to present a growth opportunity for the market. Governments are increasingly investing in small satellite constellations for enhanced communication, reconnaissance, and real-time surveillance capabilities. The demand for these satellites is increasing to enable the cost-effective and rapid deployment of satellites for tactical military missions. The demand is further propelled by the need for resilient satellite architectures and advanced space-based Intelligence, Surveillance, and Reconnaissance (ISR) solutions.

- For instance, in March 2025, the Australian Defence Force launched the Buccaneer Main Mission nanosatellite to collect high-frequency radio measurements in low Earth orbit, for long-range threat detection and surveillance. This ISR-focused CubeSat supports both defense operations and civilian applications, including border security and maritime monitoring.

NANOSATELLITE AND MICROSATELLITE MARKET TRENDS

Miniaturization of Components Installed in Nano and Microsatellite is a Significant Trend

A significant trend shaping the market is the miniaturization of components, which enables the development of smaller, lighter, and more cost-effective satellites without compromising functionality. Advances in materials and electronics present significant opportunities for the component manufacturers of small satellites to integrate sophisticated and smaller subsystems into compact platforms. Such development supports the adoption of small satellites including nano & microsatellite across commercial, scientific, and defense sectors. Moreover, the component makers are constantly involved in the research and development of compact components to reduce launch costs and improve mission efficiency.

- For instance, in October 2025, September 2025, Dragonfly Aerospace launched the ηDragonfly Bus, a compact satellite platform that miniaturizes microsatellite-level reliability and performance into a smaller, cost-effective nanosatellite bus.

MARKET CHALLENGES

Orbital Congestion and Regulatory Burdens to Challenge Market Growth

The rising congestion in low Earth orbit, resulting from the rapid deployment of satellites, is expected to increase risks related to space debris. Such possibilities of risks can give rise to operational hazards and potential mission failures in space. Moreover, this challenge is further complicated by growing regulatory scrutiny and complex compliance requirements worldwide. All such factors are anticipated to increase the cost and timeline of satellite launches and operations, which may present substantial challenges for the nanosatellite and microsatellite market growth in the future.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

Growing Need for Advanced Optical and SAR capabilities in Defense Programs Drives Microsatellites (10 to 100 kg) Segment Growth

On the basis of type, the market is bifurcated into nanosatellites (1 to 10 kg) and microsatellites (10 to 100 kg).

The microsatellite segment holds the largest share of the market as the governments and commercial operators prefer satellite platforms in the 50–300 kg class. This mass class of satellites is capable of hosting higher-performance optical, multispectral, and SAR payloads, which drives their adoption. Moreover, the rise of defense and earth observation programs in regions such as the Asia Pacific, Europe, and others for securing national imaging capabilities is expected to propel the segment growth.

- For instance, in February 2024, the Greek Ministry of Digital Governance announced a USD 69.17 million Earth observation microsatellite constellation program to provide high-resolution optical, multispectral, and hyperspectral imagery for national users.

The nanosatellite segment is the fastest-growing segment of the market, owing to the rapid popularity of IoT, 5G NB-IoT, and technology-demonstration missions, which prioritize low cost per satellite and rapid iteration cycles. In addition, satellite operators are focusing on deploying large fleets of nanosatellites to extend connectivity to remote assets, collect sensor data, perform rapid data processing, and test new in-orbit technologies. The segment is estimated to record the highest CAGR of 6.2% during the forecast period.

- For instance, in August 2024, Sateliot launched four additional LEO nanosatellites on a SpaceX Transporter-11 mission to expand its 5G NB-IoT constellation.

By Component

Advances in Miniaturized Optical and RF Instruments & Satellite Components Fuel Payload Segment Growth

Based on component, the market is segmented into payload, Telemetry, Tracking, and Command (TT&C), power system, propulsion system, Command & Data Handling (C&DH), and others.

The payload segment acquires the largest nanosatellite and microsatellite market share, driven by a surge in demand for higher-value services from nano/microsatellites. There is a shift toward the use of imaging, RF sensing, and other solutions, which drives the integration of advanced payload according to the requirements. Operators are increasingly aiming to install technologically advanced imagers, miniaturized optical instruments, and compact payloads for a diverse range of applications, including Earth observation, satellite imaging, and others.

- For instance, in April 2024, ESA selected two AI experiments from Thales Alenia Space to fly on the Φsat-2 6U microsatellite, utilizing onboard AI to process Earth-observation imagery in orbit and address environmental challenges worldwide.

The power system segment is expected to grow at a steady rate of 4.7% over the forecast period, due to a surge in demand for advanced and efficient power systems. There is a need for power systems that can smoothly support various components, such as payloads, electric propulsion, and other systems of small satellites. Manufacturers are investing in high-efficiency multi-junction solar cells, deployable solar arrays, and improved Li-ion/solid-state batteries, which further help the segment to grow significantly in the market during the forecast period.

By Application

Rising LEO Broadband Demand and SmallSat Adoption Across Sectors Propel Communication Segment Growth

Based on application, the market is segmented into communication, earth observation & remote sensing, scientific research & exploration, defense, security & intelligence, and navigation, and positioning & timing.

The communication segment held the largest share in the market in 2025, as the Low-Earth-orbit constellations are increasingly used to provide broadband, backhaul, and direct-to-device services, where terrestrial networks are uneconomical or unavailable. Operators are utilizing nanosatellite and microsatellite platforms for narrowband IoT messaging and communication. Therefore, there is an increasing demand for small communication satellite in the commercial and defense sectors, which drives the manufacturing and launch of nano and micro satellites.

- For instance, in December 2024, Airbus Defence and Space was awarded a contract by Eutelsat to build 100 additional small satellites, extending the OneWeb LEO communications constellation and ensuring continuity and enhancement of broadband services for future customers.

The defense, security & intelligence segment is set to grow at the fastest CAGR of 7.0% over the forecast period, owing to the requirement for smallsat constellations for resilient ISR, targeting support, and strategic situational awareness. In addition, the defense sectors of some countries worldwide are investing in domestically built small satellites to secure supply chains and national data security, which in turn stimulates significant market growth.

- For instance, in December 2024, Poland signed a USD 143 million agreement under the MikroGlob program to develop and deploy four reconnaissance microsatellites based on Creotech’s HyperSat platform.

To know how our report can help streamline your business, Speak to Analyst

By Orbit

Low Latency and Lower Launch Costs Drive LEO Segment Growth

Based on orbit, the market is segmented into Low Earth Orbit (LEO), Medium Earth Orbit (MEO), and Highly Elliptical Orbit (HEO).

The Low Earth Orbit (LEO) segment dominates the market, as this orbit is preferred in the nano and micro satellite industry due to its advantages, including low latency, lower launch costs, and easier access for Earth observation and connectivity missions. A large number of the commercial constellations used for communications, IoT, and imaging are being designed with small satellites in LEO, which drives the segment growth.

- For instance, in December 2024, Eutelsat selected Airbus to build 100 additional small satellites to extend its OneWeb Low-Earth-orbit constellation, underlining sustained investment in LEO architectures for global broadband connectivity.

The Medium Earth Orbit (MEO) segment is estimated to grow at the fastest rate of 8.5% during the forecast period, driven by the development of government and institutional communication missions that benefit from wider coverage and resilient multi-orbit architectures. MEO small-sat deployments are increasingly being integrated with LEO and GEO assets to provide redundancy, anti-jamming benefits. Thus, the emergence of multi-orbit constellations is driving segment growth during the forecast period.

By End Use

Investments in Small Satellite Fleets for Geospatial and IoT Analytics Expand Commercial Segment Growth

Based on end use, the market is segmented into civil, military, and commercial.

The commercial end-user segment acquires the largest share, as the enterprises, analytics providers, and telecom operators increasingly rely on nanosatellite and microsatellite constellations for data products and connectivity-as-a-service. Moreover, commercial operators are investing in fleets to provide imagery, geospatial analytics, and IoT data across various verticals, including agriculture, infrastructure, maritime, and logistics. Additionally, the rise in the development and launch of small satellite technologies for Earth observation and atmospheric and environmental science applications is expected to drive the demand for nanosatellites and microsatellites.

- For instance, in November 2022, OHB Sweden launched its MATS (Mesospheric Airglow/Aerosol Tomography and Spectroscopy) satellite into a 585 km circular orbit on using Rocket Lab's Electron launch vehicle from New Zealand. The satellite is designed to studying atmospheric waves and their impact on climate,

The military end-user segment is anticipated to grow at a moderate rate of 5.9% during the forecast period, driven by the defense sector’s use of small-sat capabilities for secure communications, ISR, and tactical support. In addition, there is a rise in defense budgets and framework contracts that explicitly target proliferated LEO and maneuverable small satellites for defense missions.

Nanosatellite and Microsatellite Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Nanosatellite and Microsatellite Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the largest market share, valued at USD 1.38 billion in 2025. The nano and micro satellite sector in the region is driven by constant investment in Earth observation, ISR, commercial imaging constellations, and a well-established space industry. There is a presence of major space agencies and a well-developed supply chain of component manufacturers and propulsion startups, which further helps expand the market.

The programs launched in the U.S. by the military sector, such as Proliferated LEO, Tactically Responsive Space (TacRS), and ISR procurement, are encouraging large-scale demand for nanosatellite and microsatellite fleets. Countries in the region, such as the U.S., have major small satellite manufacturers, such as Boeing, Northrop Grumman, Lockheed Martin Corporation, and among others, which drive innovation and product development, propelling the growth of the market in North America.

- For instance, in October 2023, the U.S. Navy's Naval Information Warfare Center Pacific completed the Laser Crosslink Experiment (LaCE), a nanosatellite mission demonstrating advanced optical and radio communication technologies in Low Earth Orbit, to enhance future warfighter capabilities.

Europe

In the European region, the market is expected to grow owing to an increase in defense space budgets in countries such as the U.K., France, Germany, and Italy. There is a shift toward the design and development of small satellite architectures for reconnaissance, space domain awareness, and secure communications. Moreover, the European Union is continuously involved in enhancing environmental intelligence, including climate mapping, agricultural analytics, border monitoring, and disaster response. Additionally, the European space agencies are increasingly investing in the development and small satellite missions to support communication and navigation services.

- For instance, in November 2024, The European Space Agency (ESA) awarded a USD 11.43 million contract to French aerospace firm Hemeria to develop Swing, ESA’s first space weather nanosatellite mission.

Asia Pacific

The growth of the market in the Asia Pacific is expected to grow due to rising government investments in space technology for national security, environmental monitoring, and scientific research. Rapid urbanization and industrialization have increased the demand for advanced communication, Earth observation, and disaster management solutions. Moreover, technological advancements and continuous investment in the launch of small satellites by various countries further push small satellite market growth in the region.

- For instance, in August 2023, China launched its second quantum nano-micro satellite, Jinan 1, aboard a Lijian quick-response rocket from the Gobi Desert to test quantum key distribution in Low Earth Orbit.

Latin America

The market growth in Latin America is supported by the need for affordable observation assets for agriculture analytics, forestry management, natural-resource monitoring, Countries such as Brazil, Argentina and Chile are adopting nanosatellite and microsatellite solutions for such applications.

Middle East & Africa

In addition, in the Middle East and Africa, the industry growth is supported by government initiatives in reconnaissance, border surveillance, oil infrastructure monitoring, and environmental assessment across the Gulf states and parts of North Africa. The rise in partnerships for the development and deployment of small satellites further accelerates the market growth during the forecast period.

- For instance, in November 2025, Kongsberg NanoAvionics announced expansion operations in the UAE by opening a new branch dedicated to satellite integration and testing, in partnership with Dubai’s Mohammed Bin Rashid Space Centre (MBRSC). This collaboration includes the development of five 12U CubeSats.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation, Production Scale, and Long-Term Constellation Contracts Drive Market Leadership of Key Players

The competitive landscape of the market is shaped by key space satellite manufacturers such as Surrey Satellite Technology Ltd. (U.K.), GomSpace (Denmark), AAC Clyde Space (Sweden), and Kongsberg NanoAvionics (Lithuania), among others. These key players face competition from one another in the industry, with a focus on technology, production efficiency, and constellation-operations expertise. Moreover, these players are trying to stand out in the market by integrating advanced bus architectures and miniaturized payload systems that support higher power, on-orbit autonomy, and rapid tasking.

In addition, the companies are pursuing strategic alliances with defense agencies, commercial imaging operators, connectivity providers, and national space programs to secure long-term constellation contracts. Furthermore, the players are also involved in investment in propulsion miniaturization and design of compact components to upgrade their product offerings.

LIST OF KEY NANOSATELLITE AND MICROSATELLITE COMPANIES PROFILED:

- GOMspace Group A/S (Denmark)

- Surrey Satellite Technology Ltd. (U.K.)

- Kongsberg NanoAvionics UAB (Lithuania)

- Axelspace Corporation (Japan)

- AAC Clyde Space AB (Sweden)

- OHB System AG (Germany)

- Terran Orbital Corporation (U.S.)

- Sierra Nevada Corporation (U.S.)

- Spire Global, Inc. (U.S.)

- Astrocast SA (Switzerland)

- Planet Labs (U.S.)

KEY INDUSTRY DEVELOPMENTS

- August 2025: Infinite Orbits signed a framework agreement with the French Ministry of Defence to deliver a microsatellite named PALADIN for GEO (Geostationary Earth Orbit) surveillance, set to be launched in 2027 under the Action and Resilience in Space (ARES) program.

- July 2025: SFL Missions Inc. was awarded a contract by the Norwegian Space Agency to rapidly develop and deploy the AISSat-4 nanosatellite on its proven SPARTAN 6U platform.

- April 2025: Inovor Technologies Pty Ltd developed and built the nanosatellite bus for the Buccaneer Main Mission nanosat (1–10 kg class) launched from the U.S. in Low-Earth Orbit for the Royal Australian Air Force / Defence Science & Technology collaboration.

- March 2025: Kongsberg NanoAvionics launched its first microsatellite, Arvaker 1 N3X from Vandenberg Space Force Base aboard a SpaceX Transporter-13 rideshare.

- March 2024: GomSpace secured a USD 3.77 million contract with a new customer in Singapore for the joint design and delivery of two micro satellites by 2026, marking its third micro satellite contract in 2024.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 5.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, By Component, By Application, By Orbit, By End User, and Region |

| By Type |

|

| By Component |

|

| By Application |

|

| By Orbit |

|

| By End Use |

|

| By Geography |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 3.22 billion in 2025 and is projected to reach USD 5.23 billion by 2034.

In 2025, the market value stood at USD 1.38 billion.

The market is growing at a CAGR of 5.6% during the forecast period of 2026-2034.

The communication segment led the market by application in 2025.

The rapid deployment of satellite technologies for diverse applications is a key factor driving the market.

GOMspace Group A/S (Denmark), NanoAvionics (Lithuania), Axelspace Corporation (Japan), and others are some of the prominent players in the market.

North America dominated the market in 2025 with the largest share.

- 2021-2034

- 2025

- 2021-2024

- 202

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us