Military Aircraft Market Size, Share & Industry Analysis, By Type (Fixed-Wing, and Rotary-Blade), By Application (Combat, Multirole Aircraft, Military Transport, Maritime Patrol, Tanker, Reconnaissance & Surveillance, and Others), By System (Airframe, Engine, Avionics, Landing Gear System, and Weapon System), and Regional Forecast, 2026-2034

Military Aircraft Market Size and Industry Overview

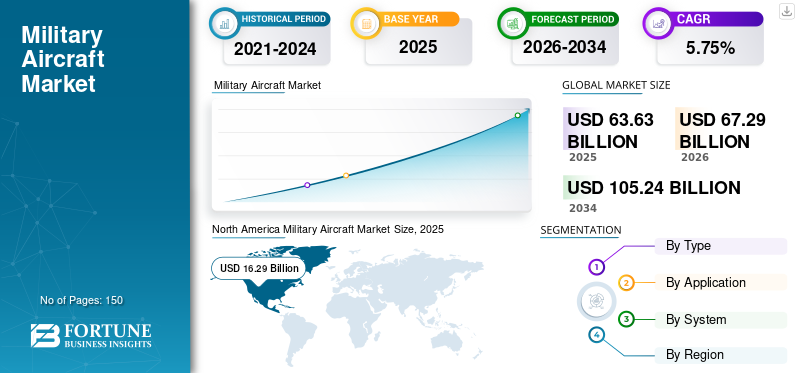

The global military aircraft market size was valued at USD 63.63 billion in 2025. The market is projected to grow from USD 67.29 billion in 2026 to USD 105.24 billion by 2034, exhibiting a CAGR of 5.75% during the forecast period. North America dominated the military aircraft market with a market share of 40.5% in 2025.

A military aircraft involves combat and non-combat aircraft platforms. Combat aircraft are usually developed and procured only by the military forces and are designed to destroy the enemy using their weapons by attacking and reconnaissance & surveillance. The non-combat aircraft are used for transport and training. These aircraft are used by the military, border patrol enforcement, law enforcement, paramilitary forces, and other special security groups. The industry is highly consolidated in terms of suppliers as well as buyers and is highly dependent on government spending.

Evolving threats and growing geopolitical instability are the key factors driving the growth of this market. However, the demand from the military sector has been subject to year-to-year variations owing to the rising strategic considerations. The market in regions such as Asia Pacific and Europe is expected to grow. However, it may be limited in regions such as the Middle East due to budgetary constraints on public spending.

Download Free sample to learn more about this report.

Download Free sample to learn more about this report.

GLOBAL MILITARY AIRCRAFT MARKET KEY TAKEAWAYS

Market Size & Forecast:

- 2025 Market Size: USD 63.63 billion

- 2026 Market Size: USD 67.29 billion

- 2034 Forecast Market Size: USD 105.24 billion

- CAGR: 5.75% from 2026–2034

Market Share:

- North America led the military aircraft market with a 40.5% share in 2025.

- Fixed-wing aircraft dominated the market in 2024, driven by global investments in combat and multirole aircraft such as F-35, Rafale, and Su-35.

- The engine systems segment held the largest market share in 2025 due to rising demand for hybrid and efficient propulsion technologies.

- The avionics segment is expected to grow at the fastest pace owing to advancements in autonomous flight and integrated sensor systems.

Key Country Highlights:

- U.S.: Continued dominance with large-scale F-35 procurement and modernization of F-22 Raptor and B-21 Raider programs.

- India: Developing HAL AMCA fifth-generation stealth fighter; rapid growth in multirole and trainer aircraft orders.

- France & Germany: Collaborating on the Future Combat Air System (FCAS) to replace existing fighter fleets by 2040.

- China: Expanding its J-20 and FC-31 stealth aircraft fleets to compete with U.S. air dominance.

- South Korea: Advancing KF-21 Boramae fighter program; increasing investments in indigenous development.

- Middle East: Regional demand rising, but constrained by economic volatility and budget limitations.

MILITARY AIRCRAFT MARKET TRENDS

Embracing Fifth Generation Technology Aircraft is Supporting the Market Growth

The demand for fifth-generation jet fighters has increased across the globe owing to their characteristics such as high-performance airframes, low-probability-of-intercept radar (LPIR), advanced avionics features, and highly integrated computer systems that can interact with other elements within the battlespace for situation awareness. It would affect the military aircraft market positively.

- North America witnessed a growth from USD 16.02 Billion in 2025 to USD 16.29 Billion in 2026.

Lockheed Martin Corporation is working with the U.S. Air Force to upgrade its weapon systems and add new capabilities to its F-22 Raptor which is the only fifth-generation fighter aircraft ready for combat. In 2025, the revolutionary fighter F-35 was used in combat for the first time by the Israeli Air Force and the U.S. Marine Corps. With its stealth, range, and sensor-fusion capabilities, the fifth-generation F-35 is progressively seen as a force multiplier that makes every branch of a nation’s military more integrated and more effective.

India is independently developing a fifth-generation supermaneuverable stealth multirole fighter named HAL Advanced Medium Combat Aircraft (AMCA). It is being designed by the Aeronautical Development Agency (ADA) and will be produced by Hindustan Aeronautics Limited (HAL). As of 2019, the AMCA is in its detailed design phase and the prototype is expected to fly in or before 2025.

Military Aircraft Market Growth FACTORS

The Rising Need To Replacing Aging Fleets Will Fuel Market Growth

Owing to the technical challenges related to structures, propulsion, and other systems, there is a rise in the need for the replacement of conventional military aircraft with technologically advanced military aircraft. A large number of old aircraft fleet constantly requires additional capacity to meet the growing threats and fulfill new mission requirements. The U.S. Air Force will face challenges and issues due to further aging of aircraft over the next 10 years as it is one of the largest operators of old aircraft.

In April 2018, Airbus signed a landmark agreement with Dassault Aviation to jointly develop and produce Europe’s Future Combat Air System (FCAS), which is planned to complement and eventually replace the current generation Rafale and Eurofighter aircraft.

Rising Arms Races Among Economies Have Led To A Surge In Demand For Military Aircraft

Increasing conflicts and cross-border activities around the globe have led countries such as China, India, and South Korea to modernize and strengthen their defense system. Governments of various countries are increasing their defense budgets to expand the air force fleet. The need for up-gradation of aerial firepower from the largest defense spenders is driving the growth of this market. India is estimated to have more than 100 rafales by the year 2025. The rise in the arms race is acting as one of the significant factors behind the military aircraft market growth.

RESTRAINING FACTORS

Adoption of Unmanned Aerial Vehicles To Hinder Growth Of Military Aircraft

Unmanned aerial vehicles (UAVs) are used for reconnaissance and surveillance, target acquisition, and intelligence. They provide battle damage management, delivery and transportation, and combat operations. A rise in the demand for UAVs is majorly driven by the safety of the crew members. Nonetheless, a rise in the adoption of UAVs will hamper the growth of the market.

MILITARY AIRCRAFT MARKET SEGMENTATION ANALYSIS

By Type Analysis

Fixed Wing Segment Dominated the Global Market Due to Significant Deliveries

Based on type, the market is divided into fixed-wing and rotary-blade segments. The fixed-wing segment is estimated to be the largest segment in the market owing to an increase in the defense budgets for combat aircraft and a rise in the demand for the expansion of the Air Force fleet.

The rotary-wing segment is predicted to be the fastest-growing segment. According to the Leonardo Company, 14,000 military helicopters are expected to be built globally over the next 20 years. The demand for military helicopters is higher in Asia, the Middle East and Africa, and Eastern Europe. Thus, the growing deliveries of military helicopters around the globe are driving this market.

By Application Analysis

- The Combat Aircraft segment is expected to hold a 31% share in 2025.

To know how our report can help streamline your business, Speak to Analyst

Multirole Segment To Acquire Dominance In The Global Market

Based on application, the market is classified into combat, multirole aircraft, military transport, maritime patrol, reconnaissance & surveillance, and others (training, tanker, and search & rescue).

The multirole aircraft segment is expected to account for the largest share of the market followed by the military transport segment. Combat aircraft is the most significant segment in terms of the number of deliveries and associated value. The combat aircraft or development projects are accountable for the market growth are the F-35 program, the F/A-18 program, the export of Typhoon and Rafale, and the new Gripen E/F.

U.S. manufacturers dominate the military transport segment and the sale is expected to continue to be stable during the forecast period. The heavy military transport segment is expected to grow where the Airbus A400M heavy transport aircraft conquers an exceptional position.

The multi-role and transport aircraft are further in demand by key defense financiers such as the U.S., the U.K., Russia, and China.

The reconnaissance and surveillance aircraft segment is predicted to be a vital segment of the market followed by the maritime patrol aircraft segment.

The reconnaissance and surveillance segment is discovering a growing market in emerging countries such as India. The demand for training aircraft has risen due to the increasing demand for skilled pilots from different aerial forces around the world.

By System Analysis

Higher Adoption of VNS devices by Specialty Clinics to Enable Dominance of the Segment

Based on the system, the market is segmented into the airframe, engine, avionics, landing gear system, and weapon system. The engine segment is anticipated to dominate the market owing to the rising research and development activities by key players. Engine manufacturers are conducting R&D activities for designing hybrid engines. The rise in fuel prices will also create demand for hybrid propulsion systems.

The avionics segment is anticipated to showcase significant growth in the market owing to the rising demand for autonomous applications in the military aircraft segment. The demand for real-time data exchange and complexity in the development of military aircraft avionics is set to propel the growth of this market during the forecast period.

REGIONAL MILITARY AIRCRAFT MARKET ANALYSIS

North America Military Aircraft Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America

The findings based on our research methodology indicate North America to dominate the market during the forecast period. Over 50% of the global demand for military aircraft both manned and unmanned is predicted to come from the United States.

Europe

Europe with the predominance of demand for transport and combat aircraft is expected to exhibit substantial growth in the market. Defense budgets in Europe are expected to grow owing to the heightened security risks and geopolitical tensions.

Asia-Pacific

Owing to the rise in the arms race, the defense budgets and modernization plans in Asia-Pacific are expected to rise at a robust pace. India increased its defense budget by 9.31% in the year 2019-20, to modernize the armed forces and strengthen their position for better managing of foreign affairs strain. The region is leading the market for new orders with India alone accounting for over 40% of the military helicopter orders from the region.

KEY INDUSTRY PLAYERS

Long-Term Government Contracts to Make Boeing and Lockheed Martin at a Leading Position In the Market

The military aircraft is dominated by large and medium-sized American and European companies such as the Boeing Company, Lockheed Martin Corporation, and Airbus S.A.S. The competitive factors among these major players are affordability, technical and management capability, the ability to develop and implement complex integrated system architectures, and the ability to provide solutions to the customers.

List of Top Military Aircraft Companies:

- Airbus S.A.S. (Netherlands)

- The Boeing Company (the U.S.)

- Dassault Aviation SA (France)

- Lockheed Martin Corporation (the U.S.)

- Saab AB (Sweden)

- Embraer S.A. (Brazil)

- GE Aviation (the U.S.)

- Hindustan Aeronautics Limited (India)

- Bell Textron Inc. (the U.S.)

- Sukhoi Corporation (Russia)

- Korea Aerospace Industries (KAI) (S. Korea)

- Chengdu Aircraft Industry Group (CAIG) (China)

KEY INDUSTRY DEVELOPMENTS:

- April 2019 – The Boeing Company was awarded a contract worth USD 14.3 billion by the U.S. Department of Defence (DOD) for the support and upgrade of B-1B Lancer and B-52 Stratofortress aircraft in service with the U.S. Air Force. The flexible acquirement and sustainment contract is anticipated to improve the survivability, lethality, supportability, and responsiveness of the B-1 and B-52 bombers. The program includes radar modernization, communication systems upgrades, and B-52 Software Block (BSB) upgrades for new weapon integration.

- October 2019 – Lockheed Martin Corporation was granted a contract worth USD 35 billion by the U.S. Department of Defence for the delivery of 478 F-35 aircraft. It is the largest contract to date for the fighter program. This contract will achieve an average 12.7% cost reduction across all three variants of F-35 aircraft. Lockheed Martin Corporation’s fifth-generation F-35 aircraft comes in three variants, the F-35A for the U.S. Air Force, F-35B for the U.S. Marine Corps, and F-35C for the U.S. Navy.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

The military aircraft market report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides this, the report offers insights into the market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the market over recent years.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD billion) |

|

Segmentation |

By Type

|

|

By Application

|

|

|

By System

|

|

|

By Geography

|

Frequently Asked Questions

Fortune Business Insights says that the global military aircraft market size was USD 63.63 billion in 2025 and is projected to reach USD 105.24 billion by 2034.

Growing at a CAGR of 5.75%, the market will exhibit steady growth in the forecast period (2026-2034).

Fixed-wing multirole aircraft segment is expected to be the leading segment in this market during the forecast period.

The Boeing Company, Lockheed Martin Corporation, and Airbus S.A.S are the leading players in the global market.

North America dominated the market share in 2025 .

- 2021-2034

- 2025

- 2021-2024

- 150

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us