Nano Silica Market Size, Share & Industry Analysis, By Type (P Type, S Type, and Type III), By Application (Concrete, Rubber, Electronics, Healthcare, Coatings, Agriculture, and Others), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

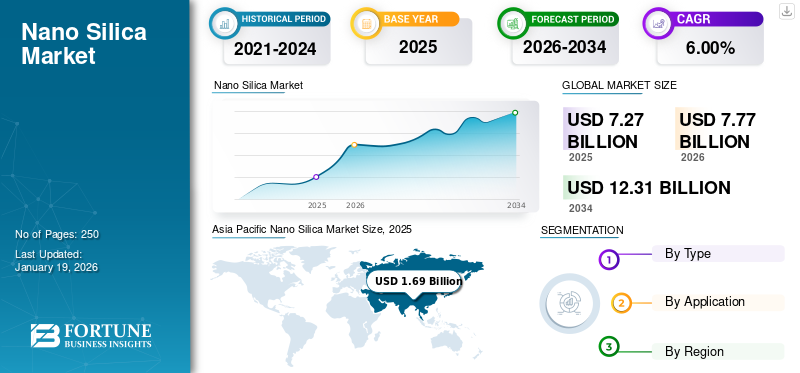

The global nano silica market size was valued at USD 7.27 billion in 2025 and is projected to grow from USD 7.77 billion in 2026 to USD 12.31 billion by 2034 at a CAGR of 6.00% during the forecast period. Asia Pacific dominated the nano silica market with a market share of 23% in 2025.

Nano Silica is an engineered form of silicon dioxide with particle below 100 nanometers. This ultrafine material possesses exceptional properties, including high surface area, remarkable purity, and enhanced reactivity compared to conventional silica. These characteristics make it highly valuable as a performance-enhancing additive across industries, including construction, electronics, healthcare, and coatings, where it significantly improves mechanical strength, thermal stability, and functional properties of host materials.

Evonik Industries AG, Cabot Corporation, Wacker Chemie AG, and Sibelco are key players operating in the market.

Download Free sample to learn more about this report.

Nano Silica Market Trends

Surge in Miniaturization Drives Boom in Semiconductor Industry

As semiconductor manufacturers push toward smaller, more powerful chips, the demand for nano silica surges dramatically. The material's exceptional thermal conductivity and electrical insulation properties enable the production of high-performance microprocessors with reduced energy consumption. Consequently, major electronics companies are investing heavily in nano silica-enhanced components. This trend results in improved device performance, extended battery life, and reduced heat generation, ultimately accelerating adoption across consumer electronics, automotive systems, and communication technologies.

Market Dynamics

Market Drivers

Increase in Sustainable Construction Revolution Propels Market Growth

The urgent global need for resilient, sustainable infrastructure is intensely increasing the demand for high-performance concrete in construction projects. As engineers seek greater strength, durability, and reduced environmental impact, it has emerged as a critical additive that significantly enhances cement properties. This pozzolanic material fills microscopic voids and accelerates hydration reactions, resulting in concrete with superior compressive strength, reduced permeability, and improved resistance to chemical attacks.

Consequently, major infrastructure developers are increasingly specifying nano silica-modified concrete for bridges, tunnels, and skyscrapers, driving substantial market expansion. The resulting performance benefits, including extended structural lifespans, reduced maintenance costs, and lower carbon footprints, continue accelerating adoption rates across developed and emerging construction markets worldwide.

Market Restraints

Production Costs and Regulations Stifle Nano Silica Market Momentum

Escalating production expenses, driven by energy-intensive manufacturing processes and specialized equipment requirements, significantly increase final product costs. Simultaneously, stringent environmental regulations governing nanoparticle production and handling impose substantial compliance burdens on manufacturers. The combined effect limits profit margins and restricts market entry for smaller players. Consequently, many potential end-users opt for conventional alternatives despite its superior properties. Environmental concerns regarding nanoparticle disposal and potential health impacts further dampen market expansion as companies face uncertainty about future regulatory frameworks, ultimately slowing adoption rates across multiple industries.

Market Opportunities

Sustainability and Green Initiatives Unlocks New Horizons for Market Growth

As global sustainability mandates intensify, green technology initiatives create unprecedented opportunities in the market. The material's ability to enhance cement efficiency allows for significant reductions in concrete volume while maintaining structural integrity, directly decreasing carbon emissions in construction projects. This environmental advantage has prompted governments to incentivize adoption through green building certifications and carbon reduction policies.

Consequently, manufacturers are developing eco-friendly production methods, including biomass-derived from agricultural waste. These sustainable innovations open new market segments, particularly in renewable energy infrastructure and green building materials. The resulting expansion into previously untapped applications attracts substantial investment and fosters collaborative research efforts, accelerating global nano silica market growth beyond traditional industrial sectors.

Trade Protectionism and Geopolitical Impact

Rising geopolitical tensions have triggered protective trade policies affecting markets. Tariffs on specialty chemicals between major economies force manufacturers to absorb increased costs or relocate production facilities. Consequently, regional supply chains fragment as companies prioritize local sourcing to mitigate risks. Export restrictions on advanced materials further complicate global distribution networks. This geopolitical uncertainty leads to price volatility and supply disruptions, compelling industry players to develop alternative procurement strategies and invest in domestic production capabilities, fundamentally altering the market's competitive landscape.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

P Type Segment Dominated the Market Owing to its Exceptional Purity Levels and Versatility Across Multiple Applications.

Based on type, the market is classified into P Type, S Type, and Type III.

P-type contributed the highest to global nano silica market share due to its exceptional purity levels and versatility across multiple applications. This product type has established a dominant position primarily through its superior performance characteristics in demanding applications. European and North American manufacturers have developed sophisticated production capabilities to maintain quality leadership in this segment. The premium positioning of P-type makes it the preferred choice for applications where performance cannot be compromised, particularly in high-value construction projects and advanced electronics manufacturing.

S-type represents a significant portion of the market, occupying the middle ground in terms of both performance specifications and pricing. This segment has found particular success in pharmaceutical and cosmetic applications where cost-efficiency must be balanced with reliable performance metrics. Asian manufacturers, particularly in China and Japan, have mastered production techniques that optimize the cost-to-performance ratio, making S-Type products especially attractive for mass-market applications. The segment continues to expand as manufacturers improve production efficiencies and broaden application possibilities.

In 2026, the Type III segment is projected to lead the market with a 39.12% share.

By Application

To know how our report can help streamline your business, Speak to Analyst

Concrete Segment to Dominate the Market Owing to High-performance Concrete Demand

Based on application, the market is classified into concrete, rubber, electronics, healthcare, coatings, agriculture, and others.

The concrete industry segment is expected to account for 27.54% of the market in 2026. The material's ability to significantly enhance structural integrity while reducing overall concrete requirements has positioned it essential in modern sustainable construction practices. High-performance concrete containing nano silica has become increasingly specified in infrastructure projects where durability and longevity are paramount concerns. As global urban development accelerates, particularly in emerging economies, this application segment continues to expand despite price sensitivity challenges in some regions.

The rubber industry, particularly for automotive applications, has emerged as a strong and stable market. The material's ability to enhance tire performance while contributing to fuel efficiency represents a compelling value proposition for manufacturers facing stringent environmental regulations. Premium tire brands have widely adopted nano silica formulations to meet consumer demands for longer-lasting, better-performing products. The segment faces challenges from raw material supply fluctuations but maintains growth through continuous innovation in formulation technology.

Nano Silica Market Regional Outlook

By region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and Middle East & Africa.

Asia Pacific

Asia Pacific Nano Silica Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific recorded a market size of USD 1.69 billion in 2025 and is projected to reach USD 1.81 billion in 2026, accounting for a 23% market share in 2025. Chinese manufacturers have rapidly expanded production capacity while steadily improving quality standards, challenging traditional market leaders. The China market is projected to reach USD 0.91 billion by 2026. Japan excels in high-precision applications, particularly in electronics and automotive components. The Japan market is projected to reach USD 0.24 billion by 2026. The massive infrastructure development throughout the region drives substantial demand for concrete applications while rapidly expanding manufacturing sectors create diverse market opportunities. India's emerging pharmaceutical industry increasingly incorporates nano silica into innovative formulations, representing a major growth opportunity. The India market is projected to reach USD 0.23 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

North America

North America contributed 29.00% to the global market in 2025, with a valuation of USD 2.13 billion, and is projected to reach USD 2.28 billion in 2026. North America is a leader in high-value nano silica applications, particularly in advanced electronics, medical technology, and specialty chemicals. The region's innovation ecosystem, anchored by major research universities and corporate R&D centers, continues to develop cutting-edge applications that expand market possibilities. The construction sector in North America has widely adopted nano silica-enhanced concrete for infrastructure renewal projects, while the pharmaceutical industry leverages the material for advanced drug delivery systems. While stringent, regulatory frameworks in the region provide clear pathways for new applications, supporting market growth. Nano Silica demand in the U.S. is driven by its use in construction for stronger concrete, healthcare for drug delivery, electronics for thermal management, and rubber for enhanced durability. The U.S. market is projected to reach USD 1.92 billion by 2026.

Europe

Europe accounted for USD 1.94 billion in 2025, representing 27.00% of the global market share, and is projected to reach USD 2.06 billion in 2026. The European market distinguishes itself by focusing strongly on sustainability and environmental performance. Manufacturers in the region have pioneered eco-friendly production methods and circular economy approaches to nano silica. The construction industry leads adoption, particularly in Northern European countries where durability requirements are most demanding. The region's automotive sector extensively utilizes it in high-performance tire formulations to meet strict efficiency standards. European research institutions maintain global leadership in developing novel applications, particularly healthcare and environmental remediation. The UK market is projected to reach USD 0.39 billion by 2026, while the Germany market is projected to reach USD 0.63 billion by 2026.

Latin America

In 2025, the Latin America market stood at USD 0.7 billion, representing 9.60% of global demand, and is projected to grow to USD 0.75 billion in 2026. The Latin American market shows increasing adoption of nano silica technology, primarily led by the construction and agricultural sectors. Brazil's substantial infrastructure investments have created a growing demand for high-performance concrete applications. The region's significant agricultural production has become an early adopter of nano silica-enhanced agrochemicals and soil amendments. Domestic production capacity remains limited, creating dependency on imports and opportunities for strategic investments. The market faces challenges from economic volatility but benefits from increasing awareness of its performance benefits across multiple industries.

Middle East & Africa

The market in Middle East & Africa reached USD 0.81 billion in 2025, representing 11.00% of total market revenue, and is projected to reach USD 0.87 billion in 2026. The Middle East & Africa region demonstrates strong adoption in high-value construction projects, where extreme environmental conditions demand enhanced material performance. Gulf states, in particular, have embraced nano silica-enhanced concrete for prestige projects and critical infrastructure. Africa represents an emerging frontier with growing mining, water treatment, and agricultural applications. The region's limited domestic production capacity presents challenges and opportunities for market development. Government infrastructure initiatives increasingly specify advanced materials, creating steady demand growth despite price sensitivity in many market segments.

Competitive Landscape

Key Industry Players

Rising Demand in High-Tech Application Drives Innovation and Expansion in the Market

Leading players are expanding production capacities to meet demand from electronics, coatings, and tire industries. They’re investing in sustainable and dispersible nano silica technologies, enhancing product performance, and targeting semiconductor, battery, and green applications. Strategic mergers (e.g., Evonik’s Smart Effects) and R&D centers are helping develop customized, high-purity silica grades.

List of Key Nano Silica Companies Profiled in the Report

- Astrra Chemicals (India)

- FUSO CHEMICAL CO., LTD. (Japan)

- nanoComposix (U.S.)

- Bee Chems (India)

- Wacker Chemie AG (Germany)

- Sibelco (Belgium)

- Evonik Industries AG (Germany)

- Cabot Corporation (U.S.)

- R. Grace & Co.-Conn. (U.S.)

- Nanostructured & Amorphous Materials, Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- January 2025: Evonik launched Smart Effects, merging its silica and silane units to drive innovation in green tires, batteries, and carbon capture. The new unit focuses on sustainable solutions across key industries with a global presence.

- October 2024: Evonik is expanding its Charleston, SC site to boost precipitated silica capacity by 50%, driven by demand for fuel-efficient tires. The move supports sustainable silica production and strengthens Evonik’s North American presence.

- June 2024: Evonik began producing ultra-pure colloidal silica in Michigan for semiconductor CMP and opened a Semiconductor Center of Excellent in Pennsylvania, supporting U.S. chip industry growth under the CHIPS Act.

- June 2024: Evonik opened a new plant in Germany to produce AEROSIL E@D fumed silica, which simplifies dispersion in coatings, cuts energy use, and lower carbon dioxide emissions, boosting sustainability and efficiency.

- March 2022: Sibelco has acquired Dutch silica producer Kremer Zande en Grind to expand its silica sand reserves and customer base in Western Europe. Kremer’s sites will continue under its brand, with family staying involved.

REPORT COVERAGE

The report provides a detailed analysis of the market. It focuses on key aspects, such as leading companies, types, compositions used to produce these product types, and product End-use Industry. Besides this, it offers insights into the market and current industry trends and highlights key industry developments. In addition to the factors mentioned above, it encompasses several factors contributing to the market's growth.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) and Volume (Kiloton) |

|

Growth Rate |

CAGR of 6.00% from 2026 to 2034 |

|

Segmentation |

By Type

|

|

By Application

|

|

|

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 7.27 billion in 2025 and is projected to record a valuation of USD 12.31 billion by 2034.

In 2025, the Asia Pacific market value stood at USD 1.69 billion.

Recording a CAGR of 6.00%, the market will exhibit steady growth during the forecast period.

In 2026, concrete is the leading segment in the market by application.

Growing demand from the concrete and rubber industry is a key factor driving the growth of the market.

Asia Pacific dominated the nano silica market with a market share of 23% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us