Naval Cyber Defense System Market Size, Share & Industry Analysis, By Solutions/Services (Network Security & Secure Communications, Identity, Access Management & Zero Trust, and Others), By Platform (Surface Naval Vessels, Submarines & Undersea Platforms, and Others), By Deployment Mode (On‑Premises, Shore-Based Private Cloud, Hybrid Deployment, and Others), By Security Level (Information Technology (IT) Security, Operational Technology (OT) Security, and Others), By End User (Navies, Defense Ministries, Coast Guards, Naval Shipbuilders, and Others), and Regional Forecast, 2026-2034

Naval Cyber Defense System Market Size and Future Outlook

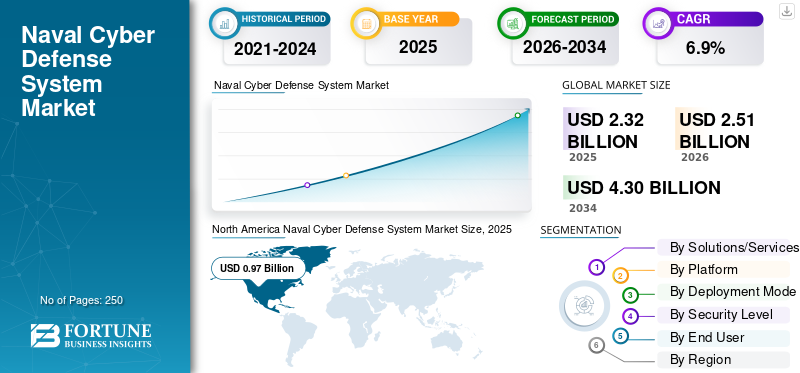

The global naval cyber defense system market size was valued at USD 2.32 billion in 2025. The market is projected to grow from USD 2.51 billion in 2026 to USD 4.30 billion by 2034, exhibiting a CAGR of 6.9% during the forecast period. North America dominated the naval cyber defense system market with a market share of 41.81% in 2025.

Naval cyber defense systems form a critical component of aerospace and defense technologies, providing real-time threat detection, secure communications, and resilient networks for applications in fleet protection, submarine warfare, missile defense integration, and secure naval operations. The global market within aerospace and defense is surging, fueled by escalating geopolitical tensions, rising cyber threats to maritime assets, and next-generation naval missions requiring robust, cyber-hardened C4ISR systems.

Leading industrial players including Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), General Dynamics Mission Systems (U.S.), and L3Harris Technologies (U.S.) are advancing innovations such as AI-driven threat detection systems, zero-trust architectures for shipboard networks, and quantum-resistant encryption systems to enable persistent maritime surveillance, counter-cyber warfare operations, and resilient naval C4ISR constellations in contested digital environments.

Download Free sample to learn more about this report.

Naval Cyber Defense System Market Key Takeaways

- 2025 Market Size: USD 2.32 billion

- 2026 Market Size: USD 2.51 billion

- 2034 Forecast Market Size: USD 4.30 billion

- CAGR: 6.9% from 2026–2034

- North America dominated the market with a 41.81% share in 2025.

- Identity, access management & zero trust segment is projected to grow at a 10.0% CAGR during the forecast period.

- Tactical edge deployment segment is expected to record a 10.3% CAGR over the forecast period.

North America

led the market at USD 0.97 billion in 2025 and is projected to reach USD 1.04 billion in 2026.

Europe

Europe is projected to grow at a 6.7% CAGR during the forecast period.

Asia Pacific

Asia Pacific is expected to be the fastest-growing regional market during the study period.

U.S

The U.S. market was valued at USD 0.89 billion in 2025.

Japan

Japan’s market was valued at USD 0.09 billion in 2025, accounting for 3.8% of global revenue.

Read More

NAVAL CYBER DEFENSE SYSTEM MARKET TRENDS

AI-Driven Threat Detection Emerge as a Defining Market Trend

Naval cyber defense systems increasingly incorporate AI technologies to process vast amounts of sensor and network data in real time. This enables automated identification of anomalies, predictive analytics for potential attacks, and faster decision-making compared to traditional manual methods. The shift supports network-centric naval operations where interconnected platforms demand resilient defenses against sophisticated intrusions. AI facilitates adaptive learning from emerging threats, improving overall system resilience without human intervention delays. The navy is integrating AI into maritime operations to counter escalating cyber threats in modern naval warfare, where adversaries exploit interconnected systems for disruptions.

- For instance, in April 2026, U.S. Navy announced plans to integrate artificial intelligence into Maritime Operations Centers (MOCs), forming a human-machine team for real-time adversary prediction and commander recommendations. MOCs, central to multi-domain command, now function as active warfighting platforms enhancing information warfare, including cyber defenses, electronic warfare, cryptology, and intelligence

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Escalating Cyber Threats to Naval Assets is Propelling Market Growth

Escalating cyber threats to naval assets are driving naval cyber defense systems market growth as naval operations become increasingly dependent on interconnected digital environments spanning platforms, communications networks, mission systems, and shore-based infrastructure. As cyber risk expands across these interconnected environments, naval organizations are under greater pressure to strengthen the protection of critical systems that support operational continuity, situational awareness, command integrity, and mission readiness.

- For instance, in April 2026, Brazil’s Navy signed a memorandum of understanding with UAE’s EDGE group in São Paulo to bolster cyber defense amid rising digital threats to military systems. The deal focuses on creating a dedicated cyber defense unit, developing tailored monitoring tools for naval networks, and enhancing cybersecurity for ships and operational technology.

MARKET RESTRAINTS

Complex Procurement Processes and Integration Challenges in Legacy Naval Systems to Limit Market Expansion

Lengthy procurement cycles and high integration costs remain a key restraint for the market. Naval cyber modernization does not usually occur in isolated software environments; it must be implemented across mission-critical fleets, shore establishments, tactical networks, and legacy IT-OT architectures that were built over multiple technology generations. This makes adoption slower and more expensive, as cyber upgrades must be validated for security, interoperability, resilience, and operational continuity before wider deployment. Government oversight has repeatedly highlighted that legacy systems create modernization challenges by increasing costs and cybersecurity vulnerabilities and hamper the market growth.

MARKET OPPORTUNITIES

Expanding Zero Trust and IT-OT Security Modernization Across Naval Infrastructure Presents Growth Opportunities for Market

The growing shift toward zero trust architectures and tighter integration between IT and OT environments presents a strong opportunity for the market. Naval organizations are moving beyond perimeter-based national security models and are increasingly prioritizing continuous verification, identity-centric access control, and resilient protection of mission-critical digital assets. This transition is creating demand for more advanced cyber defense solutions across ships, shore establishments, command networks, and connected support infrastructure. As naval systems become more data-driven and operationally interconnected, the need for unified protection across enterprise and operational environments is becoming more urgent.

MARKET CHALLENGES

Complexity of Securing Legacy and Heterogeneous Naval IT-OT Environments as a Key Market Challenge

The complexity of securing legacy and highly heterogeneous naval IT and OT environments remains a major challenge for the market. Naval organizations operate across a mix of aging platforms, modern digital systems, mission networks, industrial control environments, and shore-based infrastructure, many of which were not originally designed with today’s cyber threat landscape in mind. This creates difficulty in building standardized security architectures across fleets, bases, and support systems that must remain continuously available and operationally reliable. As a result, cyber modernization in naval environments often becomes slower, more expensive, and more technically demanding than in conventional enterprise settings.

Segmentation Analysis

By Solutions/Services

Resilient Tactical Networks and Coalition Communications Protection to Drive Strong Network Security & Secure Communication Segment Growth

Based on solutions/services, the market is divided into network security & secure communications, identity, access management & zero trust, security monitoring, detection & response, OT / platform control system security, data protection & encryption, endpoint, device & application security, vulnerability, risk & compliance management, integration & deployment services, managed security services, and others.

The network security & secure communications segment is leading the naval cyber defense system market share and is expected to witness strong growth in the market. As naval operations increasingly rely on resilient, protected, and continuously available communications environments. Modern naval forces operate through interconnected tactical networks, data links, afloat computing environments, and coalition communication architectures that require stronger protection against intrusion, disruption, and data compromise.

- For instance, in February 2025, Airbus Defence and Space, together with Naval Group, received the RIFAN stage 3 contract from the French Defence Procurement Agency to upgrade and maintain the French Navy’s IP communications network, with a maximum contract value of USD 564.4 million.

Identity, access management & zero trust segment is anticipated to rise with a steady long term growth with a CAGR of 10.0% over the forecast period.

By Platform

Integrated Shipboard Digital Infrastructure Modernization for Cyber-Resilient Operations to Drive Surface Naval Vessels Segment Growth

By platform, the market is segmented into surface naval vessels, submarines & undersea platforms, aircraft carriers & large-deck vessels, unmanned surface & underwater systems, naval shore establishments, and dockyards, bases & port infrastructure.

The surface naval vessels segment dominates the market and is projected to grow steadily as these platforms remain the most widely deployed and operationally central assets across naval fleets. Surface vessels increasingly depend on integrated shipboard networks, mission applications, communications systems, and platform-level digital infrastructure, making cybersecurity a more critical requirement across both combat and support roles. The increase in tactical network and afloat-network modernization programs for cyber-resilient networking, and operational availability drives the segment growth during the forecast period.

- For instance, in December 2024, Thales delivered the first serial production system of mine countermeasure drones to the French Navy under the Franco-British MMCM programme, marking a major milestone in autonomous and cyber-secured naval mine warfare capability.

The unmanned surface & underwater systems segment is projected to be fastest growing segment with a CAGR of 10.6% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Deployment Mode

Locally Governed Cybersecurity Architectures for Contested Maritime Connectivity to Support On-Premises Segment Dominance

By deployment mode, the market is segmented into on‑premises, shore-based private cloud, hybrid deployment, and tactical edge deployment.

The on-premises segment is projected to hold largest naval cyber defense system market share owing to need for require locally controlled, mission-assured, and tightly governed cybersecurity architectures in naval environments. Shipboard systems, tactical networks, secure facilities, and sensitive command environments often operate with strict latency, availability, sovereignty, and resilience requirements that make fully remote or cloud-dependent models less practical as a standalone approach. In naval settings, on-premises deployments also remain important for securing operational continuity in environments where connectivity may be constrained, disrupted, or deliberately contested.

- For instance, in November 2024, L3Harris Technologies received a U.S. Navy IDIQ contract worth up to USD 999 million for MIDS JTRS terminals, supporting secure and resilient Link 16 communications across U.S. and coalition platforms, including maritime systems.

Tactical edge deployment segment is projected to be grow with fastest CAGR of 10.3% over the forecast period.

By Security Level

Enterprise Network and Data Protection Priorities for Naval Force Readiness to Accelerate Information Technology (IT) Security Segment Growth

Based on security level, the market is segmented into information technology (IT) security, operational technology (OT) security, and integrated IT-OT cyber defense.

The Information Technology (IT) security segment is expected to hold largest share in the market as naval organizations continue to strengthen the protection of enterprise networks, data environments, user access layers, and mission-support systems that underpin day-to-day operations and force readines. Moreover, increasing need for prioritizing defense of enterprise IT, data, and network is expected to propel the market growth.

Integrated IT-OT cyber defense segment is expected to grow with a fastest CAGR of 8.4% over the forecast period.

By End User

Data-Driven Fleet and Infrastructure Cyber Defense Imperatives to Propel Navies Segment Growth

On basis of end user, the market is segmented into navies, defense ministries, coast guards, naval shipbuilders, and defense system integrators.

The navies segment is expected to remain a primary dominant segment in the market as naval forces remain the primary operators of interconnected warfighting platforms, fleet networks, shore establishments, and mission-support infrastructure. As naval operations become more data-driven and digitally coordinated, cyber defense is becoming an essential requirement for protecting communications, mission execution, asset readiness, and operational continuity across maritime environments.

- For instance, in October 2024, The U.S. Navy’s Flank Speed service announced that it had achieved all 91 Department of Defense target zero-trust activities and 60 of 61 advanced activities, establishing a new benchmark for zero-trust implementation across the Department of Defense.

The coast guards segment is projected to emerge as the fastest-growing at a CAGR of 7.4% over the forecast period.

Naval Cyber Defense System Market Regional Outlook

By geography, the market is segmented into North America, Europe, Asia Pacific, Middle East, and rest of the world.

North America

North America Naval Cyber Defense System Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America dominated the naval cyber defense system market in 2025 with a valuation of USD 0.97 billion, growing to USD 1.04 billion in 2026. The growth is driven by its large defense procurement base, mature naval digital infrastructure, and early adoption of zero trust, secure cloud, and cyber-resilient fleet networking architectures. Demand is supported by sustained investment in protecting naval enterprise systems, tactical networks, shore establishments, and distributed maritime operations against increasingly complex cyber threats.

- For instance, in October 2024, the U.S. Navy’s Program Executive Office Digital and Enterprise Services announced that Flank Speed had achieved full compliance with all 91 Department of Defense target zero-trust activities and 60 of 61 advanced activities, three years ahead of the FY2027 deadline, while supporting more than 560,000 users worldwide.

U.S. Naval Cyber Defense System Market

Based on North America’s strong contribution and the U.S. dominance within the region, the U.S. market was valued at around USD 0.89 billion in 2025. The U.S. is expected to witness growth within the market owing to its dominant naval spending position, active cyber modernization programs, and large installed base of fleet, port, dockyard, and shore-network infrastructure. Growth is driven by the need to harden tactical and enterprise networks, expand secure access architectures, improve cyber resilience across afloat and ashore environments, and modernize legacy digital systems that support mission readiness.

- For instance, in March 2024, the Department of Defense’s FY2025 Information Technology and Cyberspace Activities budget overview showed the Department of the Navy at USD 1,825.1 million in cyberspace activities, within a total FY2025 DoD cyberspace activities request of USD 14,453.2 million.

Europe

Europe is projected to record a growth rate of 6.7% during 2026 to 2034 and witness a steady growth in the market due to rising defense investment, stronger maritime deterrence requirements, and increasing emphasis on cyber resilience across fleets, shore establishments, and defense support infrastructure. Demand is being supported by the region’s push to strengthen naval readiness, protect digital and operational systems, and improve the resilience of military networks and maritime command environments in a more contested security setting.

U.K. Naval Cyber Defense System Market

The U.K. market was valued at around USD 0.45 billion in 2025, representing roughly 5.6% of global revenues.

Germany Naval Cyber Defense System Market

Germany’s market reached approximately USD 0.10 billion in 2025, equivalent to around 5.4% of global sales.

Asia Pacific

Asia Pacific is projected to be the fastest-growing region in the market due to the rising defense investment, stronger maritime deterrence requirements, and increasing emphasis on cyber resilience across fleets, shore establishments, and defense support infrastructure. Demand is being supported by the region’s push to strengthen naval readiness, protect digital and operational systems, and improve the resilience of military networks and maritime command environments in a more contested security setting.

- For instance, in October 2024, the Australian Defence Force said Exercise Cyber Sentinels brought together Cyber Command teams and Five Eyes counterparts to defend networks against high-fidelity simulated threats and strengthen military cyber resilience and training.

Japan Naval Cyber Defense System Market

The Japanese market was valued at around USD 0.09 billion in 2025, accounting for roughly 3.8% of global revenues.

China Naval Cyber Defense System Market

China’s market is projected to be one of the largest globally, with 2025 revenues valued at around USD 0.22 billion, representing roughly 9.3% of global sales.

India Naval Cyber Defense System Market

The Indian market was valued at around USD 0.11 billion in 2025, accounting for roughly 4.6% of global revenues.

Middle East

The Middle East region is expected to witness solid growth in the market due to rising defense digitalization, growing emphasis on protecting critical maritime infrastructure, and stronger focus on cyber resilience across naval operations, shore establishments, and strategic coastal assets. Demand is being supported by the region’s need to secure communications networks, mission-support systems, and operational technology environments linked to ports, bases, and maritime security operation.

Saudi Arabia Naval Cyber Defense System Market

The Saudi Arabia market was valued at around USD 0.06 billion in 2025, accounting for roughly 2.6% of global revenues

Rest of the World

The rest of the world is expected to witness moderate but sustained growth in the market due to the gradual strengthening of maritime-security capabilities across Latin America and Africa. Demand is being supported by the need to improve cyber resilience across naval shore infrastructure, port environments, maritime communications, and defense support systems as countries expand digital connectivity within their security architectures.

Latin America Naval Cyber Defense System Market

The Latin America market was valued at around USD 0.04 billion in 2025, accounting for roughly 1.9% of global revenues.

COMPETITIVE LANDSCAPE

KEY INDUSTRY PLAYERS

Zero Trust Expansion, Open-Architecture Integration, and Cyber-Resilient Fleet Networking Drive Market Leadership

The global naval cyber defense systems market is characterized by close coordination among navies, defense ministries, tactical-network integrators, major defense primes, and enterprise cyber providers delivering secure communications, identity-centric access control, cyber-resilient afloat networks, shore-based digital infrastructure, and integrated protection across IT and OT environments. Market leadership is increasingly being shaped by players that can support zero-trust implementation, secure cloud-enabled naval collaboration, fleet-wide network hardening, and modular cyber upgrades across ships, bases, dockyards, and unmanned maritime systems.

LIST OF KEY NAVAL CYBER DEFENSE SYSTEM COMPANIES PROFILED IN REPORT

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman Corporation (U.S.)

- General Dynamics Mission Systems (U.S.)

- L3Harris Technologies (U.S.)

- CACI International (U.S.)

- BAE Systems plc (U.K.)

- Thales Group (France)

- Leonardo S.p.A. (Italy)

- Saab AB (Sweden)

- Kongsberg Defence & Aerospace (Norway)

KEY INDUSTRY DEVELOPMENTS

- March 2026: CACI was awarded a five-year task order worth up to USD 85 million to provide engineering and technical support for U.S. Navy ships, submarines, and other naval vehicles at NSWC Carderock, with the scope including support for cybersecurity and protection of critical naval system.

- February 2026: Data Link Solutions, a joint venture of BAE Systems and Collins Aerospace (RTX), received a U.S. Navy production contract worth USD 248 million to deliver MIDS JTRS terminals, expanding jam-resistant Link 16 connectivity and secure tactical communication systems for U.S. and allied forces.

- October 2025: Lockheed Martin announced the delivery and certification of Ship Self Defense System Baseline 12, Capability Package 4 (CP4) for the U.S. Navy, strengthening fleet defense against advanced missile and cyber threats.

- March 2025: The U.S. Navy’s PEO Digital formally designated Flank Speed and Hyperion as Department of the Navy Enterprise IT Services for messaging and collaboration, marking a significant step in standardizing secure digital operations across the Navy and Marine Corps.

- March 2025: Thales was awarded a contract through ST Engineering to provide the Republic of Singapore Navy with the Pathmaster mine countermeasures system, which the company described as cyber-secured and AI-powered, for deployment on an unmanned surface vehicle.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the naval cyber defense system market segmentation included in the report. It includes details on the market dynamics, market trends, and regional analysis expected to drive the market during the forecast period. The market report includes porter s five forces analysis which illustrates the potency of buyers’ suppliers in the market. The market forecast offers information on the technological advancements, new product launches, key trends, major industry developments, and details on partnerships, mergers & acquisitions. The market analysis also encompasses detailed competitive landscape with information on the market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.9% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Solutions/Services, By Platform, By Deployment Mode, By Security Level, By End User, and By Region |

| By Solutions/Services |

|

| By Platform |

|

| By Deployment Mode |

|

| By Security Level |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 2.32 billion in 2025 and is projected to reach USD 4.30 billion by 2034.

In 2025, the North America’s market value stood at USD 0.97 billion.

The market is expected to exhibit a CAGR of 6.9% during the forecast period of 2026-2034.

By platform, the surface naval vessels segment is expected to lead the market.

Escalating cyber threats to naval assets driving market expansion.

Lockheed Martin Corporation (U.S.), Northrop Grumman Corporation (U.S.), General Dynamics Mission Systems (U.S.), and L3Harris Technologies (U.S.), are top players in the market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 250

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us