Net Zero Energy Buildings Market Size, Share & Industry Analysis, By Construction Type (New Construction and Retrofit/Renovation), By Building Type (Residential Buildings, Commercial Buildings, and Institutional Buildings), By Solution Type (Building Envelope, Energy Systems, and Renewable Integration & Smart Technologies), and Regional Forecast, 2026-2034

Net Zero Energy Buildings Market Size and Future Outlook

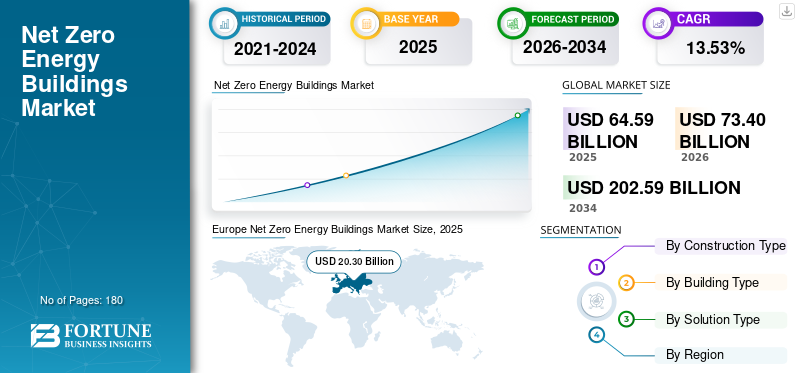

The global net zero energy buildings market size was valued at USD 64.59 billion in 2025. The market is projected to grow from USD 73.40 billion in 2026 to USD 202.59 billion by 2034, exhibiting a CAGR of 13.53% during the forecast period. Europe dominated the net zero energy buildings market with a market share of 31.43% in 2025. Europe dominated the market which is driven by strict energy-efficiency regulations, decarbonization targets, and the EU’s revised Energy Performance of Buildings Directive. Countries such as Germany, France, the U.K., Italy, and the Netherlands are leading adoption as governments and developers focus on reducing building-related energy consumption and carbon emissions. Europe is rapidly moving towards building zero-emission infrastructure which is further supported by renovation programs and renewable energy integration.

In March 2025, UNEP reports that building sector emissions stopped rising for the first time since 2020, per the Global Status Report for Buildings and Construction 2024-2025. Energy intensity dropped nearly 10%, renewables grew 5%, but the sector still accounts for 32% global energy use and 34% CO2 emissions, needing bolder policies.

Net Zero Energy Buildings (NZEBs) are highly efficient structures that produce as much energy on-site as they consume annually for heating, cooling, lighting, and appliances. They utilize passive designs and advanced technology to minimize demand, balancing any remaining needs with on-site generation. Demand is driven by climate change targets, regulatory pressures, and rising occupant demand for sustainable, low-cost operations.

Siemens AG is a prominent leader in the market, driving decarbonization through IoT technologies, smart building solutions, and AI-driven platforms such as Building X. With a pledge to achieve net-zero operations by 2030, Siemens combines on-site renewable energy sources, electrification of heating ventilation, air conditioning, and digital energy management to optimize building performance. The net-zero energy buildings (NZEB) market is highly competitive and rapidly expanding, driven by urbanization and sustainability regulations, with key leaders including Schneider Electric, Johnson Controls, Kingspan Group, and General Electric.

Download Free sample to learn more about this report.

Net Zero Energy Buildings Market Key Takeaways

- 2025 Market Size: USD 64.59 billion

- 2026 Market Size: USD 73.40 billion

- 2034 Forecast Market Size: USD 202.59 billion

- CAGR: 13.53% from 2026–2034

- Europe dominated the net zero energy buildings market with a 31.43% share in 2025.

- The Retrofit/Renovation segment accounted for the largest market share of 55.19% in 2025.

- The Residential Buildings segment accounted for the largest market share of 48.94% in 2025.

North America

North America market valued at USD 18.46 billion in 2025.

Asia Pacific

Asia Pacific market valued at USD 20.30 billion in 2025.

Europe

Europe held 31.43% share in 2025, valued at USD 20.30 billion.

U.S.

Market valued at USD 15.43 billion in 2025.

Japan

Market valued at USD 2.97 billion in 2025.

Read More

NET ZERO ENERGY BUILDINGS MARKET TRENDS

Acceleration of Deep Energy Retrofit Programs are Shaping the Market Trends

Governments and regulatory bodies worldwide are increasingly prioritizing deep energy retrofits as a core strategy to decarbonize the existing building stock, which represents the majority of future emissions. Incentive schemes, tax rebates, and mandatory renovation targets are encouraging building owners to upgrade insulation, HVAC systems, and energy controls to net-zero standards.

- In March 2025, the Government of Canada announced investment of USD 10 million through NRCan's Greener Neighbourhoods Pilot for CityHousing Hamilton's deep energy retrofits on 123 affordable townhouses. Features prefabricated envelopes, rooftop solar, electric heat pumps, and hot water tanks, cutting energy use 61% and emissions 90% while tenants stay housed.

Europe leads this trend through stringent renovation directives, while North America is accelerating through federal and state-level funding programs. This shift is transforming the NZEB market from being predominantly new construction-driven to retrofit-led, creating sustained long-term demand. Additionally, financial institutions are supporting retrofit projects through green financing and ESG-linked investments, further strengthening market growth.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Stringent Government Regulations and Net-Zero Targets is Driving the Market Growth

Government policies and climate commitments are the primary drivers of the NZEB market. Countries worldwide are implementing strict building energy codes, mandating near-zero or net-zero performance for new constructions and major renovations. Initiatives such as the EU Green Deal, U.S. decarbonization policies, and national net-zero targets are compelling stakeholders to adopt energy-efficient building practices.

- In November 2025, The European Commission allocated USD 3.3 billion from EU ETS revenues to 61 net zero technology projects across 19 sectors and 18 countries. These initiatives target energy-intensive industries, renewables, storage, net zero mobility/buildings, cleantech manufacturing, and carbon management, aiming to cut 221 million tons of CO2e in their first decade.

Regulatory enforcement is also increasing, with penalties for non-compliance and incentives for early adoption. These frameworks create a strong policy-driven demand, ensuring long-term net zero energy buildings market growth. As governments tighten emission reduction targets, NZEB adoption is expected to expand across both developed and emerging economies.

MARKET RESTRAINTS

High Initial Cost of Lithium-ion Battery Systems Restraints the Market Growth

One of the primary restraints for NZEB adoption is the high upfront cost associated with advanced materials, technologies, and integrated design processes. High-performance insulation, efficient HVAC systems, renewable energy installations, and smart technologies significantly increase initial project costs compared to conventional buildings. While these investments offer long-term savings, the higher capital requirement can deter developers and property owners, particularly in cost-sensitive markets. Financing challenges further exacerbate this issue, limiting adoption among small and medium-scale projects.

MARKET OPPORTUNITIES

Expansion of Deep Retrofit Market in Existing Buildings is Expected to Create Lucrative Opportunities

The global building stock is predominantly composed of existing structures, with over 70–80% expected to remain in use by 2050, creating a massive opportunity for deep energy retrofits. Governments are increasingly introducing renovation mandates, subsidies, and energy performance requirements to upgrade aging infrastructure to net-zero standards. This presents significant opportunities for solution providers across insulation, HVAC, smart systems, and energy auditing services. Additionally, financial institutions are expanding green financing and energy performance contracting models, reducing upfront cost barriers. As retrofit adoption accelerates, especially in Europe and North America, this segment is expected to become the largest revenue contributor in the NZEB market.

MARKET CHALLENGES

Complex Design and Integration Requirements Creates Challenges for Market Growth

NZEB projects require a highly integrated approach that combines architectural design, engineering, and energy systems. Achieving net-zero performance involves optimizing building orientation, materials, systems, and renewable integration simultaneously. This complexity increases project timelines, costs, and risks. Coordination among multiple stakeholders is essential, making project execution more challenging compared to conventional construction.

Segmentation Analysis

By Construction Type

Retrofit/Renovation is Dominant Due to its Cost-effectiveness

Based on construction type segmentation, the market is classified into new construction and retrofit/renovation.

In 2025, the retrofit/renovation segment has dominated with a share of 55.19%. Further, capturing the largest share due to its cost-effectiveness and ability to upgrade existing structures with energy-efficient technologies such as advanced insulation, solar integrations, and smart HVAC systems. This approach minimizes disruption and reduce carbon emissions.

Meanwhile, new construction has emerged as the fastest-growing segment with a CAGR of 13.84%. It is fueled by rising demand for sustainable designs, stricter building codes, and innovative materials that enable zero-energy performance from the ground up.

By Building Type

Residential Buildings Segment is Dominant Due to Government Incentives for Green Homes

Based on building type segmentation, the market is classified into residential buildings, commercial buildings, and institutional buildings.

In 2025, the residential buildings segment has dominated with a share of 48.94%, holding the largest net zero energy buildings market share. The growth is driven by growing homeowner awareness of energy cost effectiveness, government incentives for green homes, and advancements in passive solar design, heat pumps, and rooftop renewables. These upgrades promote self-sufficiency and lower utility bills.

Meanwhile, commercial buildings have emerged as the fastest-growing segment with a CAGR of 15.16%. The growth is propelled by corporate sustainability goals, ESG mandates, and innovations such as net-zero offices with integrated microgrids and efficient facades.

To know how our report can help streamline your business, Speak to Analyst

By Solution Type

Comprehensive Energy-Efficient Solutions Drive Dominance of Energy Systems

Based on solution type segmentation, the market is classified into building envelope, energy systems, and renewable integration & smart technologies.

In 2025, the energy systems segment has dominated with share of 38.57%, leading with comprehensive solutions such as high-efficiency HVAC, lighting, and building automation that optimize on-site energy use and generation. These systems form the backbone of zero-energy performance.

Meanwhile, renewable integration & smart technologies have emerged as the fastest-growing segment with CAGR of 28.14%. The growth is driven by AI-driven energy management, IoT sensors, solar-plus-battery storage hybrids, and advanced controls that enable real-time optimization and grid independence.

Net Zero Energy Buildings Market Regional Outlook

By region, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Europe

Europe Net Zero Energy Buildings Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe emerged as a dominating region, with a valuation of USD 20.30 billion by 2025. The region advances through EU directives mandating nearly-zero energy standards, renewable integration such as solar and geothermal, and retrofit incentives. Germany and the Nordic countries lead with passive designs and smart systems, targeting emissions-free urban development.

Germany Net Zero Energy Buildings Market

The German market in 2025 was valued at around USD 4.81 billion. It is projected to reach USD 5.35 billion by 2026, representing approximately 7.44% of the global industry revenues.

Asia Pacific

Asia Pacific held the second largest share in 2025, valued at USD 20.30 billion, and is further set to reach USD 23.91 billion in 2026. Asia Pacific leads the market transformation through rapid urbanization, supportive government policies, and surging construction in China and India. Key drivers include technological advancements in energy-efficient systems, renewable integration, and sustainable materials, alongside corporate sustainability mandates.

Japan and Australia emphasize high-quality standards, while Southeast Asia adopts agile digital solutions. This diverse region balances local manufacturing with global innovation to accelerate low-carbon built environments.

China Net Zero Energy Buildings Market

The China market in 2025 was valued at around USD 7.72 billion, accounting for roughly 11.94% of the global market revenues. China spearheads the market with aggressive government mandates, rapid urbanization, and vast construction pipelines.

India Net Zero Energy Buildings Market

India's market is projected to be one of the largest worldwide, with 2025 revenues recorded at around USD 3.15 billion, representing approximately 4.88% of the global market. India drives the market through rapid urbanization, ambitious sustainability goals, and government incentives promoting energy-efficient designs. Key drivers include rooftop solar adoption, passive cooling techniques, and retrofitting existing structures with advanced insulation and smart controls. Supported by green building councils and private developers, the sector advances low-carbon housing, offices, and smart city projects.

Japan Net Zero Energy Buildings Market

The Japan market in 2025 was valued at around USD 2.97 billion, accounting for approximately 4.61% of global revenues.

North America

The North America market was valued at USD 18.46 billion in 2025, North America contributes to the market through stringent energy codes, widespread renewable adoption such as solar and wind, and strong incentives for retrofits. The U.S. and Canada drive growth with advanced building envelopes, smart technologies, and corporate sustainability goals, focusing on residential upgrades and commercial hubs for energy independence and reduce carbon emissions.

U.S. Net Zero Energy Buildings Market

With North America's strong contribution and the U.S. dominance in the region, the U.S. market was valued at around USD 15.43 billion in 2025, accounting for roughly 23.88% of the global market. The U.S. market thrives on federal incentives, state mandates such as California's zero-energy codes, and widespread solar adoption. Advanced retrofits, smart grids, and energy efficient building dominate residential and commercial sectors, driven by sustainability goals and rising energy costs.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market is set to reach a valuation of USD 3.38 billion in 2026.

Latin America advances Net Zero Energy Buildings via Brazil and Mexico's green initiatives, solar integration, and efficiency retrofits. Urban growth spurs passive designs and renewable adoption, supported by regional councils targeting low-carbon infrastructure.

Brazil Net Zero Energy Buildings Market

Brazil's market reached approximately USD 1.31 billion in 2025, accounting for a very minor share of the global market.

Middle East & Africa

The Middle East & Africa accounts for market share of 3.19% in 2025 and expected to witness significant growth in this market space during the forecast period. The Middle East and Africa market reached a valuation of USD 2.06 billion in 2025.

GCC Net Zero Energy Buildings Market

The GCC market reached approximately USD 1.15 billion by 2025, accounting for around 1.78% of the global market. The Middle East & Africa advance Net Zero Energy Buildings through UAE and Saudi Vision initiatives, solar dominance, and efficiency retrofits. South Africa leads with green standards, emphasizing passive cooling and renewables for sustainable urban and commercial development.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors Actively Expanding Market Share through Technological Advancements to Gain a Competitive Edge

The global net zero energy buildings industry is considered moderately consolidated, featuring a mix of major global players and numerous regional market players. While top-tier companies such as Siemens AG, Johnson Controls International plc, Schneider Electric SE, and Honeywell International Inc., among others, are some of the prominent players in the market. For instance, in March 2024, Mahindra Group and Johnson Controls launched the Net Zero Buildings Initiative to decarbonize India's commercial, residential, and public buildings. The free toolkit provides best practices, energy consumption, conservation measures, regulations, incentives, and training workshops. Such developments are expected to fuel market growth during the forecast period.

LIST OF KEY NET ZERO ENERGY BUILDINGS COMPANIES PROFILED

- Siemens AG (Germany)

- Johnson Controls International plc (Ireland)

- Schneider Electric SE (France)

- Honeywell International Inc. (U.S.)

- ABB Ltd. (Switzerland)

- Daikin Industries Ltd. (Japan)

- Carrier Global Corporation (U.S.)

- Trane Technologies plc (Ireland)

- Saint-Gobain (France)

- Kingspan Group plc (Ireland)

- Rockwool International A/S (Denmark)

- Bosch Thermotechnology (Germany)

- Mitsubishi Electric Corporation (Japan)

- Panasonic Corporation (Japan)

- Lennox International Inc. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Tata Steel and constructsteel unveiled a pioneering steel-based Zero Energy Building in Bhubaneswar using Light-Gauge Steel Frame technology. Completed in 3.5 months, it achieves net-zero energy via insulation, solar panels, BIPV, natural ventilation, and water optimization for sustainable construction.

- March 2025: GIZ unveiled West Africa's first Nearly Zero Energy Building at Ghana's Energy Commission in Accra. Funded by Germany, this sustainable facility uses solar PV for 88% energy needs, efficient cooling, local materials, and shading to minimize carbon footprint while serving as an Energy Academy.

- June 2024: CREDAI signed an MoU with AEEE to promote net-zero buildings in India via knowledge exchange, capacity building, and Solar Decathlon India (SDI) challenge. Focuses on energy usage and efficiency, climate resilience, and sustainable construction, targeting real estate net zero by 2050.

- March 2024: Mahindra Group and Johnson Controls launched a Net Zero Buildings Initiative to decarbonize India's commercial, residential, and public buildings. The free toolkit offers best practices, assessments, conservation measures, regulations, incentives, and training via workshops starting March 2024.

- April 2022: Mahindra Lifespace Developers launched India's first net zero energy residential project, Mahindra Eden in Bengaluru, IGBC-certified. Features climate-responsive design strategies, on-site renewables, water/waste efficiency, and nature-positive amenities, pledging all net zero buildings from 2030.

REPORT COVERAGE

The global net zero energy buildings market analysis provides an in-depth study of the market size & forecast by all the market segments included in the report. It contains details on the market dynamics and industry trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market report also encompasses a detailed competitive landscape, including market share and profiles of key players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 13.53% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Construction Type, Building Type, Solution Type, and Region |

| By Construction Type |

|

| By Building Type |

|

| By Solution Type |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 64.59 billion in 2025 and is projected to reach USD 202.59 billion by 2034.

In 2025, the market value stood at USD 20.30 billion.

The market is expected to exhibit a CAGR of 13.53% during the forecast period.

The residential buildings led the building type segment.

The stringent government regulations and net-zero targets is driving the market.

Siemens AG, Johnson Controls International plc, Schneider Electric SE, and Honeywell International Inc. are some of the prominent players in the market.

Europe dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us