Open Banking Market Size, Share & Industry Analysis, By Offering (Account Information, Payment Initiation, Fund Management, Credit & Lending, Fraud Prevention and Risk Management, Compliance and Regulatory Reporting), By Deployment (On-premise, Cloud, and Hybrid), By End User (Banks and Financial Institutions, Individuals, Fintech Companies, E-commerce Companies, Accounting Platforms, and Credit & Lending Companies) and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

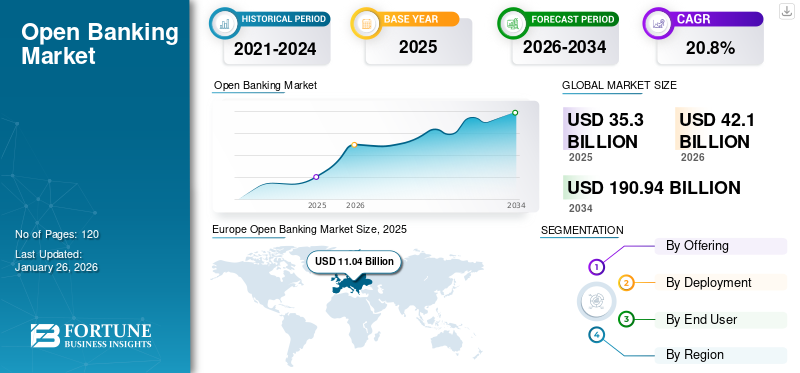

The global open banking market size was valued at USD 35.30 billion in 2025. The market is projected to grow from USD 42.10 billion in 2026 to USD 190.94 billion by 2034, exhibiting a CAGR of 20.8% during the forecast period. Europe dominated the global market with a share of 31.30% in 2025.

Open banking refers to the practice of sharing financial data among financial institutions, banks, and third-party service providers through standardized application programming interfaces APIs. This approach promotes competition and innovation within the banking industry. The adoption of banking services and payments is on the rise in many countries. According to estimates, the value of these banking payment transactions globally is projected to increase by more than 500% between 2023 and 2027, growing from USD 57 billion to USD 330 billion.

Players in the market, including Plaid, TrueLayer, GoCardless, Tink, Yapily, among others, are forming strategic alliances with other industry players, such as fintech companies, technology providers, and regulatory bodies, to accelerate innovation, enhance offerings, and expand their reach.

Download Free sample to learn more about this report.

Open Banking Market MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 35.30 billion

- 2026 Market Size: USD 42.10 billion

- 2034 Forecast Market Size: USD 190.94 billion

- CAGR: 20.8% from 2026–2034

- Europe dominated the open banking market with a 31.30% share in 2025.

- The hybrid segment is projected to dominate the market with a share of 40.94% in 2026.

- The account information (account aggregation) segment is projected to dominate the market with a share of 33.34% in 2026.

North American

The market in North America reached USD 10.13 billion in 2025, representing 28.70% of total market revenue, and is projected to reach USD 12.18 billion in 2026.

Europe

Europe contributed approximately USD 11.04 billion to the global market in 2025, accounting for 31.30% share, and is expected to reach USD 12.75 billion in 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 7.75 billion, representing 22.00% of global demand, and is projected to grow to USD 9.54 billion in 2026.

U.S.

Market expansion is driven by CFPB’s 2024 open banking rules enabling standardized API-based data sharing.

Japan

The Japan market is forecast to attain USD 2.17 billion by 2026

Read More

IMPACT OF GENERATIVE AI

Increasing Demand for Generative AI for Transforming Banking to Boost Market Growth

Generative artificial intelligence has emerged as a transformative technology with the potential to revolutionize global communication and accessibility. The financial service sector has transformed with the adoption of Gen-AI. According to industry experts, the annual revenue is increasing for banks that utilize the technology and is estimated to reach USD 200 to USD 340 billion, equivalent to 9%–15% of operating profits.

Integrating generative AI into open banking offers significant opportunities for transformation and growth in the financial services industry. By utilizing generative AI's capabilities to analyze data, predict outcomes, and create personalized experiences, banks can deliver innovative financial products, streamline regulatory compliance, enhance customer interactions, and improve risk management. This combination provides unprecedented levels of efficiency, personalization, and security, ultimately benefiting both customers and financial ecosystems.

OPEN BANKING MARKET TRENDS

Demand for Open Banking Payment APIs Acts as a Key Market Trend

Payment APIs enable secure and efficient connectivity, data exchange, and functionality between banking systems and external applications. With 87% of consumers using open banking-powered apps, mobile banking usage is on the rise, prompting businesses to develop additional use cases around this type of banking. Banking APIs enhance a bank's appeal, allowing it to meet the evolving demands of existing customers while attracting new ones. These APIs also provide a unique opportunity to increase customer engagement and address customer needs in a secure, agile, and future-proof manner. This shift has opened the door to numerous innovative financial products and services, including budgeting apps, investment platforms, and payment automation.

Open banking APIs enhance bank services and boost customer engagement, and help banks generate digital revenue through new channels. Banks that implement APIs experience a 20% increase in revenue. Therefore, demand for payment APIs is driving the open banking market growth.

Download Free sample to learn more about this report.

MARKET DYNAMICS

Market Drivers

Increasing Consumer Demand for Digital Financial Services to Boost Market Growth

From 2014 to 2021, the percentage of adults making digital payments in low- and middle-income economies doubled, increasing from 26% to 51%. During this period, the proportion of account holders using digital payments rose from approximately 50% to 65%. The availability of mobile phones, even in low-income and rural areas, has facilitated the adoption of services such as mobile banking, digital payments, and credit. Furthermore, the important design of digital services is essential for maximizing the potential of digital finance in promoting global financial inclusion. This consists of considerations including the trade-offs between privately provided infrastructure and government-implemented, access to identification, prioritizing interoperability, and addressing regulatory frameworks and technology compatibility. In 2024, digital banking users exceeded 3.6 billion globally, exceeding earlier projections and marking a 50% jump from 2020's 2.4 billion users.

Therefore, increasing consumer demand for digital financial services boosts market growth.

Market Restraints

Challenges Associated with Data Privacy and Security Concerns Hamper Market Growth

Open banking requires the sharing of sensitive financial information with third-party providers (TPPs), which raises risks related to data breaches, unauthorized access, and identity theft. Many consumers remain hesitant to give consent to share their financial data, especially in regions lacking strong data protection laws. Even with regulatory frameworks such as GDPR or PSD2, inconsistent implementation and weak enforcement destabilize user trust. However, increasing data privacy and security concerns are creating hurdles that may hinder market growth.

Market Opportunities

Increasing Popularity of Embedded Finance to Create Lucrative Opportunities for Market Players

The rise of embedded finance is transforming how financial services are accessed and delivered. This shift moves these services away from traditional banking channels and integrates them into everyday digital experiences. Embedded finance refers to the seamless integration of financial products, including lending, insurance, payments, and banking, into non-financial platforms such as ride-hailing apps, e-commerce websites, and enterprise SaaS tools.

Open banking enables this by providing secure, standardized APIs that allow third-party platforms to access user-permissioned financial data and initiate financial transactions directly. For instance, a small business using an accounting platform could apply for a loan based on real-time financial data aggregated via APIs, or a customer shopping online could pay directly through their bank account without needing to use a credit card or third-party wallet. This model enhances user experience by reducing friction and enabling contextual financial decisions, and opens up new monetization avenues for non-financial companies.

As a result, traditional banks are now partnering with fintech companies and digital platforms to offer banking-as-a-service (BaaS), while fintech is building API-based infrastructure to support this transition. The convergence of open banking and embedded finance is creating a decentralized, customer-centric financial ecosystem that is more comprehensive, responsive, and efficient than conventional models.

Thereby, increasing demand for medical translation is expected to increase the open banking market share.

SEGMENTATION ANALYSIS

By Offering

Account Information Led Market as It Allows to Share of Data Related to Customers' Finance

Based on offering, the market is segmented into account information, payment initiation, fund management, credit & lending, fraud prevention and risk management, and compliance and regulatory reporting.

The account information segment dominated the market in 2024. Account information enables the secure aggregation and sharing of consumer and business financial data such as transaction history, account balances, income, and spending patterns across multiple bank accounts with the user’s consent. This aggregated financial data provides a comprehensive, real-time view of a customer’s financial situation, which is crucial for a wide variety of applications, including personal finance management, credit scoring, budgeting tools, and even financial advisory services. The account information (account aggregation) segment is projected to dominate the market with a share of 33.34% in 2026.

The payment initiation segment is estimated to grow with the highest CAGR during the forecast period, as it allows merchants and service providers to bypass card networks and interchange fees by initiating direct bank-to-bank transfers. This factor reduces transaction costs, especially for high-volume or recurring payments.

By Deployment

Cloud Segment Commanded Market Due to Its Scalability and Flexibility

By deployment, the market is further segmented into on-premise, cloud, and hybrid.

The cloud segment dominated the market in 2024, as it offers scalability and flexibility, allowing financial institutions to quickly deploy, update, and expand services without the heavy upfront investment and long lead times associated with traditional on-premise infrastructure.

The hybrid segment is expected to grow with the highest CAGR during the forecast period. Financial institutions face growing pressure to innovate quickly and meet regulatory requirements while protecting sensitive customer data and maintaining operational resilience. Hybrid models allow banks to keep critical, sensitive data and core banking functions on secure private clouds or their own data centers, addressing concerns around data privacy, compliance, and latency. The hybrid segment is projected to dominate the market with a share of 40.94% in 2026.

By End User

To know how our report can help streamline your business, Speak to Analyst

Adoption of Open Banking by Banks and Financial Institutions to Enhance Customer Experience to Drive Segmental Growth

By end user, the market is further segmented into banks and financial institutions, individuals, fintech companies, e-commerce companies, accounting platforms, and credit & lending companies.

In 2024, banks and financial institutions dominated the market. By collaborating with fintech companies and other third-party providers, they enhance customer experience and increase their revenue streams. Currently, banks are undergoing a significant transformation driven by customer preferences and technological advancements. Open banking serves as a crucial drive for them to shift away from traditional banking practices, allowing them to explore new opportunities, generate additional revenue, and build a loyal customer base. The banks and financial institutions segment is expected to lead the market, contributing 31.88% globally in 2026.

Fintech companies are expected to grow with the highest CAGR during the forecast period. Open banking provides fintechs with real-time access to customer accounts, transactions, and balance data from multiple banks, and also, APIs also allow fintechs to build and launch products faster without needing direct partnerships with each bank.

OPEN BANKING MARKET REGIONAL OUTLOOK

The market is regionally studied across North America, South America, Europe, the Middle East & Africa, and Asia Pacific, and each region is further studied across countries.

Europe

Europe Open Banking Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe contributed approximately USD 11.04 billion to the global market in 2025, accounting for 31.30% share, and is expected to reach USD 12.75 billion in 2026. Open banking in Europe was initiated under PSD2, and it is evolving from a regulatory requirement into a data-driven marketplace. It is becoming a key driver of a new era in financial innovation. In 2024, there were around 64 million open banking users in the EU. Europe represents 46% of the global API offerings, highlighting the region's essential role in facilitating it through technology and innovation.

In the U.K., the market is projected to experience significant growth during the forecast period. The value of bank transactions in the U.K. is expected to increase by 500% between 2023 and 2027, reaching approximately USD 82 billion. According to a Mastercard survey conducted in 2024, around 70% of U.K. consumers currently connect their financial accounts directly to tools that assist them in managing various financial tasks. However, only 22% of consumers are familiar with the term "open banking." The survey also highlights that the top three use cases for open banking in the U.K. are sending or paying money (72%), paying bills (66%), and utilizing banking services (66%). The UK market is expected to reach USD 3.01 billion by 2026, while the Germany market is anticipated to account for USD 2.69 billion by 2026.

Asia Pacific

In 2025, the Asia Pacific market stood at USD 7.75 billion, representing 22.00% of global demand, and is projected to grow to USD 9.54 billion in 2026. The Asia Pacific region is expected to grow with the highest CAGR during the forecast period. Governments across Asia Pacific are actively promoting this type of banking through regulatory mandates or voluntary frameworks, creating a foundation for secure and standardized data sharing. The Japan market is forecast to attain USD 2.17 billion by 2026, the China market is poised to reach USD 2.77 billion by 2026, and the India market is set to achieve USD 1.46 billion by 2026. For instance,

- In Singapore, the Monetary Authority of Singapore launched API Exchange in 2024 and promotes a pro-innovation approach with strong guidelines for data sharing.

- In India, the government has launched the Account Aggregator Framework in 2021, which helps users to control and share financial data across regulated entities.

North America

The market in North America reached USD 10.13 billion in 2025, representing 28.70% of total market revenue, and is projected to reach USD 12.18 billion in 2026. North America is expected to show significant market growth during the forecast period. Major North American banks such as JPMorgan Chase, Wells Fargo, Bank of America, RBC, and TD Bank are no longer resisting open banking. Instead, they are transitioning into platform-based models, offering open APIs to fintechs and third-party developers through secure developer portals. This shift enables banks to expand distribution channels, partner with digital innovators, and improve customer experience without building every feature in-house.

The U.S. is estimated to witness high growth among countries in the region. Open banking adoption in the U.S. is gaining strong momentum, particularly following the Consumer Financial Protection Bureau’s (CFPB) finalization of rules in October 2024 under Section 1033 of the Dodd-Frank Act. These rules mandate standardized, secure API-based data sharing between financial institutions and third-party providers, aiming to replace legacy screen-scraping practices. The U.S. market is estimated at USD 9.92 billion by 2026.

Middle East & Africa

Middle East & Africa maintained a strong presence in the global market, reaching USD 3.96 billion in 2025, accounting for 11.20% share, and is expected to reach USD 4.77 billion in 2026. The Middle East & Africa region is expected to experience steady growth during the forecast period. The financial landscape in the Middle East is evolving due to this type of banking and new regulatory frameworks that enhance competition, promote financial inclusion, and empower consumers to have greater control and transparency over their financial choices.

South America

The South America market generated USD 2.42 billion in 2025, representing 6.90% of the global market landscape, and is expected to reach USD 2.86 billion in 2026. South America is likely to register steady growth during the forecast period. The South American fintech landscape is growing rapidly, with Brazil alone expanding at approximately 300% from 2017, and the number of fintech institutions increased from 244 in 2017 to 771 in 2020. Therefore, the demand for banking APIs is increasing.

Competitive Landscape

Key Market Players

Market Players Implement Merger & Acquisition Strategies to Expand Their Presence

Key players in the market are adopting various business strategies to enhance their market presence and capitalize on emerging opportunities. Players are collaborating with fintechs, startups, tech providers, and aggregators to accelerate time to market and improve product offerings. Players are expanding to new regions or markets, where there are more banking regulations or demand.

List of Key Open Banking Companies Profiled

- Plaid (U.S.)

- TrueLayer (U.K.)

- Tink AB (Sweden)

- Token (U.K.)

- Yapily (U.K.)

- Salt Edge (U.K.)

- Finastra (U.K.)

- MX Technologies (S.)

- Volt (K.)

- Worldline (France)

- Finicity (S.)

- Bud (U.K.)

- Brite Payments (Sweden)

KEY INDUSTRY DEVELOPMENTS

- June 2025 – Experian collaborated with Plaid to enhance credit access with real-time cash flow insights.

- May 2025 – Backbase formed a partnership with Salt Edge to enhance the adoption of open banking. This collaboration will assist banks in meeting compliance requirements seamlessly while creating new revenue opportunities.

- April 2025 – Yapily partnered with Allica Bank to introduce a new top-up service built on Yapily’s Open Banking infrastructure, providing customers an easier and faster way to deposit funds into their savings accounts.

- October 2024 – Axway acquired Sopra Banking Software to enhance the open banking solution.

- February 2024 – Adyen collaborated with Yapily to improve merchant onboarding and strengthen account verification.

REPORT COVERAGE

The market research report provides a detailed market analysis. It focuses on key points, such as leading companies, offerings, and applications. Besides this, the report offers an understanding of the latest market trends and highlights key industry developments. In addition to the above-mentioned factors, the report contains several factors that have contributed to the growth of the market in recent years.

Request for Customization to gain extensive market insights.

REPORT SCOPE & SEGMENTATION

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 20.80% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

By Offering

By Deployment

By End User

By Region

|

|

Companies Profiled in the Report |

|

Frequently Asked Questions

The market is projected to reach USD 190.94 billion by 2034.

In 2025, the market was valued at USD 35.30 billion.

The market is projected to grow at a CAGR of 20.80% during the forecast period.

The account information segment led the market in terms of market share.

Increasing consumer demand for digital financial services is expected to boost market growth.

TrueLayer, Plaid, Token, Salt Edge, and Yapily are the top players in the market.

Europe dominated the market with a share of 31.3% in 2025.

By end user, the fintech companies segment is expected to grow with the highest CAGR during the forecast period.

- 2021-2034

- 2025

- 2021-2024

- 120

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us