Oral Proteins and Peptides Market Size, Share & Industry Analysis, By Drug Class (GLP-1 Peptides, Somatostatin Analogs, PTH Analogs, GLP-2 Peptides, and Others), By Therapeutic Area (Metabolic Disorders, Endocrine Disorders, and Others), By Age Group (Pediatric and Adult), By Formulation (Tablets and Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies & Drug Stores, and, Specialty Pharmacies & Others), and Regional Forecast, 2026-2034

Oral Proteins and Peptides Market Size and Future Outlook

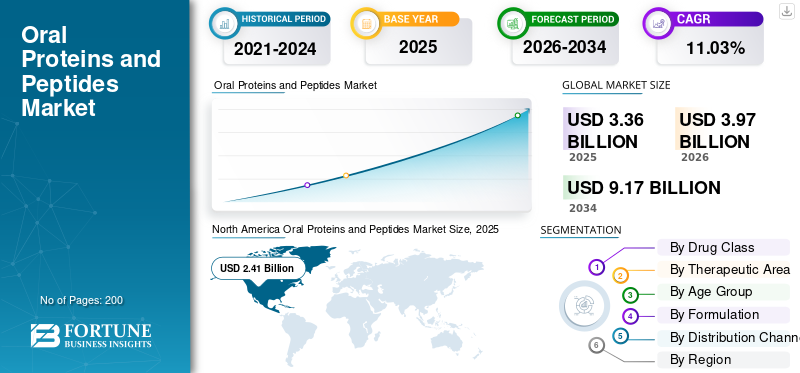

The global oral proteins and peptides market size was valued at USD 3.36 billion in 2025 and is projected to grow from USD 3.97 billion in 2026 to USD 9.17 billion by 2034, exhibiting a CAGR of 11.03% during the forecast period. North America dominated the oral proteins and peptides market with a market share of 71.72% in 2025

The oral protein and peptide therapies which are systemically absorbed aim to provide systemically absorbed peptide and protein medications via oral tablets or capsules to enhance treatment ease, adherence, and earlier initiation of therapy in chronic disease management. The market is growing due to the commercial scaling of oral semaglutide, ongoing physician endorsement of oral peptide treatments for diabetes, the introduction of oral octreotide for acromegaly maintenance, and increased industry funding in oral delivery systems that transform traditionally injectable biologics into oral forms. Expansion is further fueled by the development of next-generation pipelines in oral insulin, oral PTH analogs, and oral GLP-2 and associated peptide initiatives, which are broadening the market beyond its existing approved foundation.

Key players consist of Novo Nordisk, Chiesi Group, EnteraBio Ltd., Oramed Pharmaceuticals Inc., among others. These firms are focusing on oral GLP-1 products, oral somatostatin analog therapy, unique absorption-enhancement and tablet delivery technologies.

Download Free sample to learn more about this report.

Oral Proteins and Peptides MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 3.36 billion

- 2026 Market Size: USD 3.97 billion

- 2034 Forecast Market Size: USD 9.17 billion

- CAGR: 11.03% from 2026–2034

- North America dominated the market with a 71.72% share in 2025.

- GLP-1 peptides held the largest market share in 2025.

- Metabolic disorders accounted for the largest application segment share in 2025.

North American

North America reached USD 2.41 billion in 2025, maintaining its market leadership.

Europe

Europe is projected to expand at a 15.66% CAGR during the forecast period.0

Asia Pacific

Asia Pacific is expected to reach USD 0.46 billion in 2026, driven by rising adoption of metabolic therapies.

U.S.

The market is projected to reach USD 2.62 billion in 2026.

Japan

The market is projected to reach USD 0.12 billion in 2026.

Read More

ORAL PROTEINS AND PEPTIDES MARKET TRENDS

Increasing Preference for Non-Invasive Therapies is a Notable Market Trend

A growing demand for non-invasive therapies is emerging as a distinct trend in the global market, as both patients and physicians exhibit greater interest in treatments that minimize reliance on injections. Oral medications enhance convenience, reduce needle-related reluctance, and can promote earlier treatment commencement in chronic conditions including diabetes and obesity. This trend is particularly significant in long term treatment sectors, where simplified administration can enhance adherence and expand patient acceptance. It is also motivating drug developers to put more resources into oral peptide delivery technologies that can provide injectable-like effectiveness in a tablet form. Consequently, the market is slowly transitioning from merely a formulation innovation narrative to a commercial opportunity driven by patient preferences. This trend is expected to intensify as additional oral peptide products expand from diabetes to obesity and various other chronic conditions. These factors are supporting the overall global oral proteins and peptides market growth.

- For instance, in December 2025, Novo Nordisk received the U.S. FDA approval for Wegovy pill on December 22, 2025, which the company described as the first and only oral GLP-1 for weight loss in adults, followed by broader U.S. availability announced in early 2026.

MARKET DYNAMICS

MARKET DRIVERS

Download Free sample to learn more about this report.

Rising Prevalence of Chronic Diseases is Propelling Market Growth

The growing incidence of chronic diseases significantly influences the global market, as these therapies are primarily designed for long-term conditions including type 2 diabetes, obesity, and endocrine disorders that necessitate ongoing treatment. With the growth of the patient pool, there is a heightened demand for therapies that are simpler to start and maintain over time. Systemically absorbed oral peptide products are drawing interest as they can alleviate the need for injections while effectively addressing significant chronic disease groups. This is particularly significant in diabetes and obesity, where increasing rates are prompting healthcare systems to seek scalable, patient-centered treatment alternatives. Public health data strengthens the trend, indicating that diabetes and obesity are still growing globally and remain significant burdens among noncommunicable diseases. This establishes a more extensive commercial foundation for authorized oral peptide treatments and enhances the long-term potential for pipeline products too. All these factors cumulatively drive the overall market growth.

- For instance, according to the data published by World Health Organization (WHO) in December 2025, around 16% of adults aged 18 years and older across the globe were suffering from obesity in 2022.

MARKET RESTRAINTS

High Costs of Development to Hamper Market Growth

High development costs are a key restraint in the global market as these products require complex formulation work to protect fragile molecules from degradation and improve absorption in the gastrointestinal tract. Compared with conventional oral drugs, developers often need to spend more on specialized excipients, delivery technologies, pharmacokinetic studies, and large clinical programs to prove that oral versions can achieve reliable efficacy. Manufacturing scale-up also adds cost as peptide-based oral formulations need tighter process control and higher technical validation. These factors increase overall development risk and can delay commercialization timelines, especially for pipeline candidates outside the leading GLP-1 category. As a result, smaller developers may face funding pressure, while larger companies become more selective in advancing oral biologic programs. This makes high development cost a meaningful barrier to broader market expansion. This results in limiting the market growth to certain extent.

- For example, in March 2026, Entera Bio stated that the company reported 2025 operating expenses of USD 21.3 million, including USD 11.4 million in research and development expenses, while continuing to advance oral peptide programs such as EB613 and other pipeline assets.

MARKET OPPORTUNITIES

Advancements in Oral Drug Delivery Technologies to Offer Market Growth Opportunities

Innovations in systemically absorbed oral drug delivery systems are generating significant market potential in the global oral proteins and peptides sector by addressing the key obstacles that have traditionally restricted oral biologics, including inadequate stability in the gastrointestinal tract and low absorption rates. Enhanced tablet systems, permeability boosters, and protective delivery methods are broadening the spectrum of peptide and protein medications that can be formulated for oral administration. This is expanding the possibilities beyond diabetes to include bone health, endocrine issues, and various other specialty applications. With advancements in delivery science, businesses can aim at broader patient groups that once relied on injections, enhancing the market's long-term commercial prospects. These advancements also lower development risk for subsequent oral peptide candidates and facilitate lifecycle extension for biologic drug categories. Consequently, advancements in oral delivery are emerging as one of the most significant opportunity for upcoming market growth.

- For instance, in March 2026, Entera Bio announced that it has submitted a streamlined Phase 3 protocol to the FDA for EB613 (oral PTH (1-34), teriparatide) in postmenopausal women with osteoporosis.

MARKET CHALLENGES

Low Bioavailability of Oral Proteins to Pose a Prominent Challenge to Market Growth

The low bioavailability of oral proteins that are systemically absorbed continues to be a significant obstacle in the global market, as these molecules are readily degraded in the gastrointestinal system and typically have difficulty crossing the intestinal barrier. Consequently, firms need to employ intricate absorption enhancers, protective layers, or tailored delivery systems merely to attain significant systemic exposure. This complicates dose optimization and raises variability in clinical outcomes compared to injectable products. It also increases development risk; as even potential peptide candidates might not provide reliable blood levels in broader patient groups. The challenge is particularly significant in chronic conditions including diabetes and obesity, where consistent long-term exposure is essential for commercial viability. Consequently, low bioavailability remains a barrier to the transformation of research-stage concepts into approved oral products. All the factors cumulatively affect the market growth.

Segmentation Analysis

By Drug Class

Increase in Commercial Adoption of Oral GLP-1 Therapies Enabled GLP-1 Peptides Segment’s Dominance

In terms of drug class, the market is divided into GLP-1 peptides, somatostatin analogs, PTH analogs, GLP-2 peptides, and others.

The GLP-1 peptides segment captured the largest global oral proteins and peptides market share. The segment’s leadership is mainly supported by its use in large-volume chronic metabolic conditions, especially type 2 diabetes, where long-term therapy demand is high. Moreover, GLP-1 peptides have a much stronger approved-product base and broader physician acceptance. The segment also benefits from better commercial visibility, wider geographic reach, and stronger patient preference for oral treatment over injectable alternatives.

- For instance, in Novo Nordisk’s Annual Report 2025, published in February 2026, the company reported that Rybelsus sales reached USD 3,407.4 million in 2025. Such strong sales performance clearly shows that oral GLP-1 therapies continue to account for the largest share of the market.

The PTH analogs segment is anticipated to rise with a CAGR of 40.24% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Therapeutic Area

Reduced Dependence on Injections Led to Metabolic Disorders Segmental Dominance

On the basis of therapeutic area, the market is divided into endocrine disorders, metabolic disorders, and others.

The metabolic disorders segment accounted for the largest global market share in 2025. The segment’s growth can be attributed to the presence of the largest approved oral systemically absorbed peptide therapy used in routine clinical practice. Additionally, oral peptide therapies are gaining stronger acceptance in metabolic care as they reduce dependence on injections and fit better into daily treatment routines.

For instance, in November 2025, Novo Nordisk announced that the U.S. FDA approved oral semaglutide (Rybelsus) to reduce cardiovascular risk in adults with type 2 diabetes who are at high risk, further expanding its role in metabolic disease management.

The others segment is anticipated to rise with a CAGR of 58.64% over the forecast period.

By Age Group

High Usage of Oral Peptide Therapies in Adult Patients Supported Segment’s Leading Position

In terms of age group, the market is divided into pediatric and adult.

The adult segment captured the highest share of the global market in 2025. The currently approved oral systemic peptide products in this market are mainly targeted toward adult patient populations. The segment’s dominance is supported by the high burden of chronic diseases such as type 2 diabetes, obesity, and acromegaly in adults, where long-term treatment demand is much higher than in pediatric populations. For instance, MYCAPSSA and Rybelsus both are approved for adult patients.

The pediatric segment is anticipated to rise with a CAGR of 51.18% over the forecast period.

By Formulation

Strong Commercial Presence of Semaglutide Tablets Supported Tablets Segmental Dominance

On the basis of formulation, the market is divided into tablets and others.

The tablets segment captured the highest share of the global market in 2025. Tablet formulations are preferred as they are more convenient for daily use, easier for patients to carry and take, and better suited for long-term treatment in chronic diseases including diabetes. Additionally, tablets also have stronger physician familiarity and broader acceptance in routine prescribing. The segment’s leadership is further supported by the fact that the only U.S. FDA-approved oral GLP-1 medicine which is systemically absorbed is marketed as semaglutide tablets.

- For instance, in March 2025, OPKO Health and Entera Bio announced a collaboration to advance the first oral dual agonist GLP-1/glucagon peptide as a once-daily tablet treatment for obesity, metabolic, and fibrotic disorders.

The others segment is anticipated to rise with a CAGR of 9.79% over the forecast period.

By Distribution Channel

Wide Availability Through Retail Pharmacy & Drug Stores Networks Supported Segment’s Leading Position

Based on distribution channel, the market is segmented into hospital pharmacies, retail pharmacies & drug stores, and specialty pharmacies & others.

In 2025, the retail pharmacies & drug stores segment held the leading position in the global market. The segment’s dominance is supported by the fact that oral peptide therapies are taken as regular prescription medicines, which makes retail pharmacies a more convenient access point for patients than hospital-based channels. Retail outlets also support repeat refills, better geographic reach, and easier access for adults managing long-term diseases such as diabetes and obesity. Furthermore, the segment is set to hold 71.5% share in 2026.

- For instance, in January 2026, Novo Nordisk announced that Wegovy pill was broadly available through more than 70,000 U.S. pharmacies, including CVS and Costco.

In addition, hospital pharmacies are projected to witness CAGR of 15.88% during the forecast period.

Oral Proteins and Peptides Market Regional Outlook

By geography, the market is divided into North America, Asia Pacific, Latin America, Europe, and the Middle East & Africa.

North America

North America Oral Proteins and Peptides Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America market reached USD 2.52 billion in 2024 and led the global market. In 2025, the region continued to hold its leading position, with USD 2.41 billion. North America’s growth is driven by early commercialization of approved oral peptide products, strong prescription access, expanding clinical trial landscape, and rapid expansion of oral GLP-1 use in diabetes and obesity.

U.S. Oral Proteins and Peptides Market

The U.S. market dominated the North American market and can be analytically approximated at around USD 2.62 billion in 2026, accounting for roughly 66.0 % of global market.

Europe

Europe’s market size is anticipated to grow at 15.66% CAGR during the forecast period. Europe is growing due to expanding use of oral semaglutide in diabetes management, broader regulatory support, and rising acceptance of systemically absorbed oral peptide therapies in cardiometabolic care. Europe also has good reimbursement structures in major countries and a strong osteoporosis opportunity for future pipeline products.

U.K. Oral Proteins and Peptides Market

The U.K. market is estimated at around USD 0.13 billion in 2026, representing roughly 3.3% of global revenues.

Germany Oral Proteins and Peptides Market

Germany’s market size is projected to reach approximately USD 0.17 billion in 2026, equivalent to around 4.3% of global sales.

Asia Pacific

Asia Pacific’s market is expected to reach a valuation of USD 0.46 billion by 2026, making it the third largest region in the global industry. Large diabetes population, improving diagnosis and treatment rates, and increasing access to innovative metabolic therapies in Japan, China, and India are some of the prominent factors driving the regional market growth.

Japan Oral Proteins and Peptides Market

The Japan market is estimated at around USD 0.12 billion in 2026, accounting for roughly 3.1% of global revenues.

China Oral Proteins and Peptides Market

China’s market is projected to reach revenues of around USD 0.10 million in 2026, representing roughly 2.5% of global sales.

India Oral Proteins and Peptides Market

The India market is estimated at around USD 0.06 billion in 2026, accounting for roughly 1.6% of global revenues.

Latin America and Middle East & Africa

The Middle East & Africa, and Latin America are expected to experience slower growth throughout the forecast period. The market in Latin America is projected to attain a valuation of USD 0.05 billion by 2026. Prominent factors such as rising diabetes and obesity burden, improving urban pharmacy access, and gradual expansion of branded oral metabolic therapies into private and specialty care channels are propelling the market growth in these regions.

GCC Oral Proteins and Peptides Market

The GCC market is projected to reach approximately USD 0.01 billion by 2026, representing about 0.3% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Robust Commercial Leadership and Pipeline Partnerships of Key Companies Strengthened their Market Position

The global oral proteins and peptides market features a highly concentrated competitive landscape. Prominent players such as Novo Nordisk, Chiesi Group, and EnteraBio Ltd., hold an important position in the market due to their commercial presence, pipeline depth, and platform-based development strategies. Novo Nordisk has established strong leadership through oral semaglutide, while other companies are focusing on expanding future market access through oral insulin, oral PTH analogs, oral GLP-2, and other peptide candidates.

- For instance, in February 2026, OPKO Health and Entera Bio expanded their partnership to advance a first-in-class oral long-acting PTH tablet for hypoparathyroidism, while also progressing oral oxyntomodulin programs for metabolic and fibrotic disorders.

Additional key contributors include Oramed Pharmaceuticals Inc., and Rani Therapeutics Holdings, Inc., and others. These companies are emphasizing collaborations, technology partnerships, and late-stage clinical development to strengthen their long-term competitive standing.

LIST OF KEY ORAL PROTEINS AND PEPTIDES COMPANIES PROFILED IN REPORT

- Novo Nordisk (Denmark)

- Chiesi Group (Italy)

- EnteraBio Ltd. (Israel)

- Oramed (U.S.)

- Protagonist Therapeutics Inc. (U.S.)

- Biocon (India)

- Rani Therapeutics (U.S.)

KEY INDUSTRY DEVELOPMENTS

- September 2025: EnteraBio reported positive PK data for its first-in-class oral GLP-2 tablet at the 2025 ESPEN Congress.

- June 2025: Protagonist nominated PN-477 as an oral and injectable peptide development candidate for obesity, adding another obesity-focused oral peptide program to the competitive pipeline

- February 2025: Rani Therapeutics released new preclinical semaglutide data showing successful oral delivery of semaglutide via the RaniPill capsule.

- November 2024: Protagonist reported positive Phase 3 ICONIC topline results for icotrokinra. Icotrokinra (JNJ-2113) is a first-in-class investigational targeted oral peptide that selectively blocks the IL-23 receptor.

- June 2024: Rani Therapeutics partnered with ProGen to develop RT-114, an oral obesity treatment.

REPORT COVERAGE

The global oral proteins and peptides market analysis encompasses an extensive examination of the market size and projections for all market segments featured in the report. It provides information on the market dynamics and trends that are anticipated to propel the market during the forecast period. It offers insights into crucial elements, such as innovations in products, the regulatory landscape, pipeline analysis, and the introduction of new products. Furthermore, it outlines collaborations, mergers & acquisitions, along with significant advancements in the industry within the market. The global market outlook report additionally offers a comprehensive competitive landscape with details on market share and profiles of major active participants.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.03% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Drug Class, Therapeutic Area, Age Group, Formulation, Distribution Channel, and Region |

| By Drug Class |

|

| By Therapeutic Area |

|

| By Age Group |

|

| By Formulation |

|

| By Distribution Channel |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 3.36 billion in 2025 and is projected to reach USD 9.17 billion by 2034.

In 2025, the North Americas market value stood at USD 2.41 billion.

The market is expected to exhibit a CAGR of 11.03% during the forecast period of 2026-2034.

By drug class, the GLP-1 peptides segment is expected to lead the market.

Increasing prevalence of chronic diseases and growing demand for patient-friendly therapeutics are primarily driving market expansion.

Novo Nordisk, Chiesi Group, and EnteraBio Ltd. are some of the prominent players in the global market.

North America held the largest market share in 2025.

- 2021-2034

- 2025

- 2021-2024

- 200

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us