Patient Registry Software Market Size, Share & Industry Analysis, By Registry Type (Disease Registry, Health Services Registry, Population Registry, and Others), By Functionality (Population Health Management, Medical Research and Clinical Studies, Health Information Exchange, Patient Care Management, and Others), By End User (Hospitals & ASCs, Diagnostics Centers, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Patient Registry Software Market Size and Future Outlook

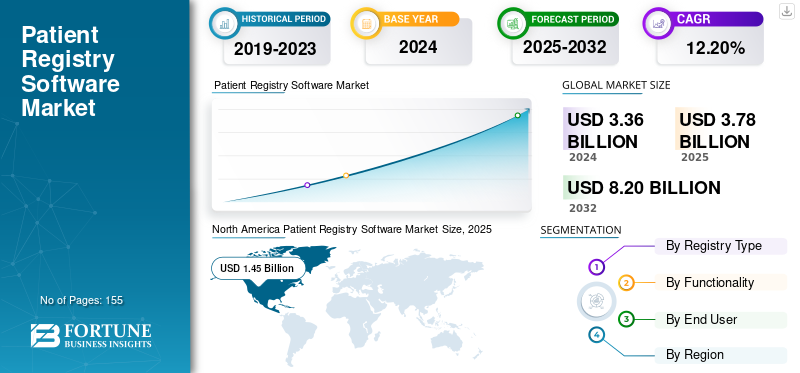

The global patient registry software market size was valued at USD 3.78 billion in 2025. The market is projected to grow from USD 4.23 billion in 2026 to USD 10.15 billion by 2034, exhibiting a CAGR of 11.56% during the forecast period. North America dominated the global patient registry software market with a market share of 42.86% in 2025.

Patient registry solutions support disease registries, product registries, and population health registries by collecting, managing, and analyzing structured patient data for research, public-health surveillance, clinical outcomes tracking, and post-market safety monitoring. It enables healthcare service providers, researchers, and public health agencies to track outcomes over time, generate evidence, and improve clinical care and operational decisions. This market is anticipated to witness strong growth in the near future, owing to the increasing usage of electronic health records, growing focus on real-world evidence (RWE), and increasing prevalence of chronic and rare diseases requiring long-term patient follow-up.

- For instance, according to statistics published by the U.S. Assistant Secretary for Technology Policy in 2021, around 88.0% of the U.S. office-based physicians adopted EHR as of 2021, which is a growth from around 78.4% in 2013.

Furthermore, many key industry players, including IQVIA, Oracle, Veradigm LLC and others, are investing in innovative technologies to maintain their competitive edge.

Download Free sample to learn more about this report.

Patient Registry Software Market Key Takeaways

- 2025 Market Size: USD 3.78 billion

- 2026 Market Size: USD 4.23 billion

- 2034 Forecast Market Size: USD 10.15 billion

- CAGR: 11.56% from 2026–2034

- North America dominated the patient registry software market with a 42.86% share in 2025.

- The population health management segment accounted for a 36.10% market share in 2025.

- Hospitals & ASCs segment is projected to hold a 54.30% market share in 2025.

North America

North America held a 42.86% share in 2025, valued at USD 1.62 billion.

Asia Pacific

Asia Pacific held a market value of USD 0.76 billion in 2025, securing the position of the third-largest regional market.

Europe

Europe accounted for a market value of USD 0.99 billion in 2025 and is projected to grow at a CAGR of 26.19% during the forecast period.

U.S.

The market projected to reach USD 1.69 billion by 2026.

Japan

The market projected to reach USD 0.22 billion by 2026.

Read More

MARKET DYNAMICS

MARKET DRIVERS:

Rising Adoption of Electronic Health Records (EHRs) and Interoperability Initiatives to Drive the Market Growth

The increasing adoption of electronic health records is anticipated to boost the global patient registry software market growth. As more healthcare providers integrate EHRs across departments, registries gain access to large volumes, real-time patient information. Additionally, owing to the mandatory interoperability standards, registry platforms can connect seamlessly with multiple data sources, driving the demand for automated, multi-site registries. This enables providers, researchers, and payers to generate stronger Real-World Evidence (RWE), improving clinical decision-making and population health management.

- For instance, in May 2024, Medical Information Technology, Inc., integrated ambient listening technology into its Expanse EHR solution.

MARKET RESTRAINTS:

Integration Complexity with Legacy EHRs and Variability in Clinical Workflows to Restrict the Market Growth

Legacy EHR integration complexity and variable clinical workflows remain a major restraint limiting the adoption of patient-registry software across the world. Despite the advances in technology, several healthcare providers still rely on legacy Electronic Health Record (EHR) systems with proprietary, non-standard data models and limited interoperability. This results in difficulty in integrating a modern registry platform. Additionally, this also increases the overall cost of integration. As a result, data from legacy EHRs may be fragmented or incompatible, which hampers data exchange and prevents real-time registry updates.

- For instance, according to an article published in February 2025, the extensive use of EHRs is hampered by several challenges associated with their integration.

MARKET OPPORTUNITIES:

Integration of AI and Machine Learning Offers Market Growth Opportunities

In recent years, the market for patient registry software has witnessed an increasing integration of artificial intelligence and machine learning technologies. This is due to the growing need for risk stratification, disease prediction, and Real-World Evidence (RWE) through advanced analytics. AI enables pattern recognition, automated data cleansing, and patient-segmentation, in turn reducing timelines, leading to increased efficiency.

- For instance, in May 2024, IQVIA launched an AI-powered Regulatory & Safety Suite on AWS to enhance real-world data analytics, safety monitoring, and patient-registries.

PATIENT REGISTRY SOFTWARE MARKET TRENDS

Shift toward Cloud-based Registry Platforms is a Significant Trend Observed in the Market

The shift toward cloud-based registry platforms has become a prominent trend in the market in recent years. For the past few years, an increasing number of healthcare organizations have been shifting from on-premise infrastructure toward cloud-based platforms. This is driven by the increasing need for flexible access, scalability, lower upfront infrastructure costs, and improved data sharing across sites. Additionally, several advantages offered by cloud-based platforms also supported this trend among end users.

- For instance, in June 2024, Oracle Health announced new cloud-native capabilities on Oracle Cloud Infrastructure (OCI) designed to support population health analytics, care registries, and integrated clinical datasets.

MARKET CHALLENGES:

Data Privacy and Security Concerns Pose a Significant Challenge for the Market

Concerns associated with data security and privacy pose a significant challenge to the market for patient registry software. With the increasing adoption of these technologies in healthcare, highly sensitive health information of individuals is generated on a large scale, making it a prime target for cyberattacks. This elevates the risk of unauthorized access, breaches, or data misuse, in turn slowing down the market growth to a certain extent.

- For instance, in July 2023, HCA Healthcare, the largest health system in the U.S., announced that more than 11 million healthcare records have been affected by cyberattack.

Download Free sample to learn more about this report.

Segmentation Analysis

By Registry Type

Rising Burden of Chronic and Rare Diseases to Propel Disease Registry Segmental Growth

Based on the registry type, the market is divided into disease registry, health services registry, population registry, and others.

To know how our report can help streamline your business, Speak to Analyst

The disease registry segment is expected to account for 46.81% of the market in 2026. The dominance of the segment is attributed to rising burden of chronic and rare diseases, growing need for Real-World Evidence (RWE) studies, and others. Owing to these factors, many key companies are participating in strategic collaborations to launch innovative products and cater to increasing demand.

- For instance, in February 2025, Veradigm launched seven new disease-specific registry datasets to support the next generation of real-world research.

Moreover, the population registry segment is expected to grow at a CAGR of 11.10% during the forecast pe

By Functionality

Shift toward Value-based Care to Drive the Population Health Management Segmental Growth

Based on functionality, the market is segmented into population health management, medical research and clinical studies, health information exchange, patient care management, and others.

In 2026, the population health management segment is projected to lead the market with a 35.93% share. The growth of this segment is driven by a shift toward value-based care, the increasing need to reduce patient readmissions, a large patient population, and the rising integration of AI in population health management. In addition, the rising adoption of PHM by end users also supplemented the market growth. Furthermore, the segment held a 36.1% share in 2025.

- For instance, in April 2024, Kaiser Permanente announced the implementation of the Innovaccer Healthcare AI platform to support its value-based care initiatives.

Additionally, the market for medical research and clinical studies is projected to grow at a CAGR of 11.13% during the study period.

By End User

High Patient Volume to Drive the Hospitals & ASCs Segmental Growth

Based on end user, the market is segmented into hospitals & ASCs, diagnostics centers, specialty clinics, and others.

The hospitals & ASCs segment is poised to account for 54.37% of the market share in 2026. Key factors supporting the dominance of the segment include high patient volume in these settings, increasing integration with EHR systems, and a growing focus on quality benchmarking and accreditation by hospitals. Additionally, collaborations between operating players and these end users further support the segment growth.

- For instance, in July 2025, Medisolv joined the MEDITECH Alliance program with an aim to enable hospitals to improve the total quality of registry submissions, chart abstraction, and others.

In addition, the diagnostic centers segment is projected to grow at a CAGR of 10.36% during the study period.

Patient Registry Software Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Patient Registry Software Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 1.62 Billion, contributing 42.86% to global market revenue, and is projected to grow to USD 1.81 Billion in 2026. The leading position of this region is driven by advanced healthcare IT infrastructure, high RWE adoption, and active registry programs in oncology, rare diseases, and cardiovascular care. Additionally, strategic initiatives by operating players in the region also drive growth further. The U.S. market is projected to reach USD 1.69 billion by 2026.

- For instance, in November 2023, Health Catalyst acquired ERS, a company specializing in cancer registry software and services.

Europe

Europe is expected to experience notable growth in the coming years. During the forecast period, the Europe market accounted for USD .99 Billion in 2025, representing 26.19% of the global industry, and is expected to reach USD 1.09 Billion in 2026. The growth in the region is attributed to the strong public-health registry initiatives, emphasis on data privacy and standards, and growing RWE use in regulatory submissions. Backed by these factors, the UK market is projected to reach USD 0.21 billion by 2026, and the Germany market is projected to reach USD 0.25 billion by 2026, and France USD 0.17 billion in 2025.

Asia Pacific

Asia Pacific recorded a market size of USD 0.76 Billion in 2025, capturing 20.11% of the global market share, and is projected to reach USD 0.87 Billion in 2026 and secured the position of the third-largest region in the market. In the region, the Japan market is projected to reach USD 0.22 billion by 2026, the China market is projected to reach USD 0.29 billion by 2026, and the India market is projected to reach USD 0.11 billion by 2026. The growth in the Asia Pacific region is driven by rapidly developing healthcare infrastructure in India and China, coupled with the increasing penetration of advanced products in the region.

Latin America

Latin America accounted for USD 0.16 Billion in 2025, representing 4.23% of the global market share, and is projected to reach USD 0.18 Billion in 2026. The increasing adoption of advanced technologies in healthcare management is expected to drive market growth in these regions further.

Middle East & Africa

In the Middle East & Africa, the GCC captured a value of USD 0.06 billion in 2025. The Middle East & Africa market generated USD 0.25 Billion in 2025, representing 6.61% of the global market landscape, and is expected to reach USD 0.28 Billion in 2026.

COMPETITIVE LANDSCAPE

Key Industry Players:

Strategic Acquisitions and Collaborations by Key Players to Strengthen their Market Presence

The market for patient registry software reflects a moderately consolidated structure, comprising prominent players such as Oracle, IQVIA, Veradigm, Medical Information Technology, Inc., among others. The dominance of these companies can be attributed to factors such as strong investments in new product launches, extensive product portfolios, strategic acquisitions, and robust interoperability capabilities.

- For instance, in February 2024, Veradigm LLC acquired ScienceIO, a healthcare-AI company, for approximately USD 140 million.

Other notable players in the global market include interActive Systems Berlin, RAYLYTIC Software GmbH, Access Healthcare, ScienceSoft USA Corporation, and others. These companies focus on new product launches, collaborations, and partnerships to increase their global market presence.

LIST OF KEY PATIENT REGISTRY SOFTWARE COMPANIES PROFILED:

- Oracle (U.S.)

- IQVIA (U.S.)

- interActive Systems Berlin (Germany)

- RAYLYTIC Software GmbH (Germany)

- Veradigm LLC (U.S.)

- Access Healthcare (U.S.)

- ScienceSoft USA Corporation. (U.S.)

- Medical Information Technology, Inc. (U.S.)

- Halemind Inc. (U.S.)

- NXGN Management, LLC. (U.S.)

- BizData Pty Ltd (Australia)

KEY INDUSTRY DEVELOPMENTS:

- October 2025: Oracle introduced new cloud networking capabilities for any workload. This development will enable Oracle's patient registry and healthcare data management solutions to utilize the enhanced Oracle Cloud Infrastructure (OCI) capabilities.

- August 2025: American College of Cardiology launched the new CONNECT-HCM Registry to enhance insights into Hypertrophic Cardiomyopathy (HCM).

- February 2025: MEDITECH collaborated with key technology companies to showcase interoperability, including Google Cloud, Microsoft, Commure, and DrFirst, at HIMSS25.

- February 2024: Persistent Systems, a digital solution provider in India, introduced an innovative, generative AI-powered PHM solution in partnership with Microsoft.

- April 2023: Verantos introduced Pragmatic Registry product and new registry for severe asthma patients. The Pragmatic Registry is a disease specific product and uses real world data from various sources.

REPORT COVERAGE

The market analysis provides a detailed study of the market size and forecast for all the market segments included in the report. The report also provides insights into market dynamics and trends expected to drive the market during the forecast period. The market report for patient registry software also comprises key aspects, such as an overview of technological advancements, product launches, insights on strategic partnerships, mergers and acquisitions, and key industry developments by top regions. The market forecast also provides a detailed competitive landscape, including market share and profiles of major industry players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 11.56% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation |

By Registry Type

By Functionality

By End User

By Geography

|

Frequently Asked Questions

Fortune Business Insights states that the global market value stood at USD 3.78 billion in 2025 and is projected to reach USD 10.15 billion by 2034.

In 2025, the market value stood at USD 1.62 billion.

The market is expected to exhibit a CAGR of 11.56% during the forecast period of 2026-2034.

The disease registry segment led the market in terms of registry type in 2026.

Rising adoption of Electronic Health Records (EHRs) is one of the key factors driving the market.

Oracle, IQVIA, Veradigm, and Medical Information Technology, Inc., are among the major players in the global market.

North America dominated the global patient registry software market with a market share of 42.86% in 2025.

- 2021-2034

- 2025

- 2021-2024

- 155

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us