Petroleum Sorbent Pads Market Size, Share & Industry Analysis, By Material Type (Polypropylene (PP), Natural Fiber, and Synthetic Blended), By Structure (Single-Layer, Multi-Layer (Laminated), and Perforated), By End User (Oil & Gas, Marine & Shipping, Manufacturing & Heavy Industry, Chemical & Petrochemical, and Others), and Regional Forecast, 2026-2034

Petroleum Sorbent Pads Market Size and Future Outlook

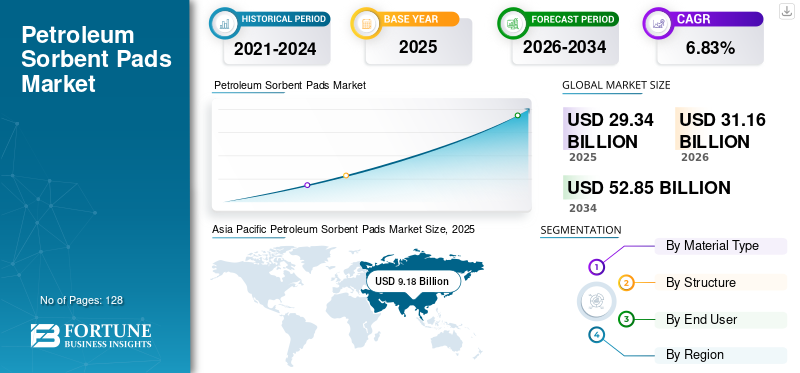

The global petroleum sorbent pads market size was valued at USD 29.34 billion in 2025. The market is projected to grow from USD 31.16 billion in 2026 to USD 52.85 billion by 2034, exhibiting a CAGR of 6.83% during the forecast period. Asia Pacific dominated the petroleum sorbent pads market with a market share of 31.28% in 2025.

Rising global oil throughput is a primary factor driving market share. The petroleum supply reached ~101.9 million b/d in 2023, creating a constant risk of spills across storage, transfer, and transportation points. High dependence on seaborne logistics further accelerates demand: 76% of oil volumes (≈77.5 million b/d) move via maritime routes, while oil tankers accounted for 29% of global shipping deadweight in 2022, necessitating routine spill-response materials at ports and terminals. Onshore expansion adds momentum, with U.S. crude production exceeding 13.3 million b/d in December 2023, increasing spill-control inventories at wells, pipelines, and depots. Regulatory enforcement also drives recurring consumption; the U.S. EPA’s updated SPCC requirements (2026) mandate spill-prevention preparedness for facilities storing over 1,320 gallons of oil.

- For instance, in a full-year 2024 assessment, petroleum sorbent pads demonstrated strong industrial reliance: approximately 74% of industrial facilities handling fuels or lubricants maintained sorbent pads in mandatory spill kits, reflecting their routine use for compliance and operational safety rather than just emergencies. Additionally, over 61% of demand came from routine maintenance activities, underscoring consistent consumption beyond accidental spill response. These pads can absorb hydrocarbons while repelling water, with many products achieving 12–25× their own weight in oil absorption depending on pad design.

Some of the leading companies operating in the petroleum sorbent pads industry include 3M, Sorbent Products Company (SPC), New Pig Corporation, and others. 3M is a prominent supplier of petroleum sorbent pads, leveraging its expertise in advanced nonwoven materials and industrial safety solutions. The company offers oil-only sorbent pads designed to absorb hydrocarbons while repelling water, making them suitable for marine, industrial, and onshore oil-handling environments. 3M’s sorbent pads are widely used for routine maintenance, leak management, and spill preparedness across refineries, manufacturing plants, warehouses, and transportation facilities, supported by its strong global distribution network. Oil-Dri Corporation specializes in mineral-based absorbent products that deliver efficient solutions for spill control, filtration, and purification across industrial and consumer markets.

Download Free sample to learn more about this report.

PETROLEUM SORBENT PADS MARKET TRENDS

Rising Focus on Sustainability and Product Performance are Key Market Trends

Recent industry developments show a heightened focus on sustainability and product performance enhancements. Manufacturers are increasingly innovating eco-friendly and high-efficiency pads made from advanced polymers and biodegradable materials to reduce environmental impact and meet tightening regional regulations. In North America and Europe, lightweight, high-capacity synthetic sorbents are gaining traction for their ease of deployment and improved absorbency. At the same time, Asia Pacific’s rapid industrialization is fueling broader adoption across the logistics and manufacturing sectors. New product designs emphasize durability, enhanced absorbency, and ease of handling to serve routine maintenance and preventive applications better.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Hydrocarbon Handling and Stricter Spill-Response Readiness to Drive Market Growth

Recent demand for petroleum sorbent pads is driven by expansion in hydrocarbon handling and heightened spill-response preparedness across oil & gas, marine, and industrial sectors as infrastructure and transport activity increase, raising baseline leakage risk. Frequent small leaks and maintenance requirements in refineries, pipelines, and chemical plants necessitate reliable absorbents. Tightening environmental and safety enforcement, such as EPA SPCC and global equivalents, compels facilities to stock and deploy pads to avoid fines and reputational damage while meeting ESG targets.

In addition, industrial diversification into automotive, manufacturing, and logistics elevates operational spill risk and mandates on-site containment tools. Material innovations that improve absorption capacity and lower disposal impact further encourage adoption in routine safety protocols rather than solely emergency use.

MARKET RESTRAINTS

Post-Use Disposal Challenges to Hamper Market Growth

Despite rising utilization, petroleum sorbent pads face notable constraints that can limit adoption and increase lifecycle costs. One significant restraint is post-use disposal challenges: once saturated, pads become hazardous waste and require controlled handling, incineration, or specialized treatment to prevent secondary environmental contamination, which raises operational costs and complexity, especially in environmentally sensitive regions. Technical limitations also persist as specific pads are less effective with very heavy crudes or mixed contaminants, driving users to supplement with alternative cleanup tools, which dilutes investment in pads alone. These factors collectively restrain broader, cost-efficient deployment driven by stringent environmental regulations.

MARKET OPPORTUNITIES

Advanced Product Innovation and Performance Differentiation to Present Excellent Market Opportunities

An emerging opportunity for the petroleum sorbent pads industry lies in advanced product innovation and performance differentiation, as manufacturers focus on developing pads with higher absorbency, enhanced durability, and tailored use cases (e.g., marine-grade or heavy-industrial pads) to meet evolving operational needs and stricter environmental standards.

Also, the expansion into new application sectors, such as automotive maintenance, construction sites, and renewable energy installations, creates demand beyond traditional oil & gas and marine spill response. Further, the emerging regional growth in South America, Asia Pacific, and Africa, driven by expanding industrial and hydrocarbon handling infrastructure, presents new markets for the deployment of petroleum sorbent pads in routine containment and environmental protection efforts.

MARKET CHALLENGES

Operational and Environmental Factors Present Significant Challenges for Market Growth

Although petroleum sorbent pads are widely used for spill control, they face significant operational and environmental challenges that hamper broader efficiency and sustainability. One core issue is the environmental and disposal burden of synthetic pad materials, such as polypropylene; once oil-saturated, these pads become hazardous waste, requiring costly, regulated disposal methods such as incineration or specialized treatment, particularly in regions with stringent waste laws, thereby raising end-user expenses and logistical complexity.

Segmentation Analysis

By Material Type

Polypropylene (PP) Dominated Market Owing to Its High Oil Absorbency, Hydrophobicity, and Cost-Effectiveness

Based on material type, the market is classified into polypropylene (PP), natural fiber, and synthetic blended.

In 2025, polypropylene (PP) dominated the market share. Polypropylene (PP) has material properties that align closely with operational spill-control needs. PP is inherently hydrophobic and oleophilic, allowing it to selectively absorb hydrocarbons while repelling water, critical in marine, offshore, and rain-exposed industrial settings. The polymer’s nonwoven structure enables high capillary action and retention, supporting rapid uptake of light to medium petroleum products without dripping. PP also offers strong chemical resistance and thermal stability (melting point 160–170 °C), maintaining integrity when exposed to fuels, lubricants, and solvents.

The synthetic blended segment is experiencing the highest growth and is expected to grow at a CAGR of 8.00% during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Structure

Multi-Layer (Laminated) Dominated Market as It has Higher Absorbency, Strength, and Controlled Fluid Retention

On the basis of the structure, the market is classified into single-layer, multi-layer (laminated), and perforated.

In 2025, the multi-layer (laminated) segment dominated the global market. Multi-layer (laminated) petroleum sorbent pads are dominant as they deliver superior performance under demanding spill-control and maintenance conditions. The layered construction, typically combining high-loft meltblown polypropylene with spunbond outer layers, significantly increases absorbency capacity while maintaining structural strength during saturation. This design allows pads to retain oil without tearing, dripping, or deforming, even when fully loaded, which is critical in high-traffic industrial sites and marine environments.

The perforated segment is expected to grow at a CAGR of 7.98% in the coming years.

By End User

Manufacturing & Heavy Industry Dominated Market Due to High Leak Frequency and Equipment Density

On the basis of end user, the market is classified into oil & gas, marine & shipping, manufacturing & heavy industry, chemical & petrochemical, and others.

In 2025, the manufacturing & heavy industry segment held the largest market share. Manufacturing and heavy industry dominate petroleum sorbent pad usage due to the continuous presence of oils, lubricants, hydraulic fluids, and fuels across production lines and machinery. These facilities operate dense equipment layouts, presses, compressors, gearboxes, and conveyor systems that generate frequent minor leaks, drips, and overflows rather than isolated large spills, driving steady sorbent consumption.

The oil & gas segment is expected to grow at a CAGR of 7.12% over the forecast period.

Petroleum Sorbent Pads Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Petroleum Sorbent Pads Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific was valued at USD 9.18 billion in 2025 and ranked as the largest region in the market. In the region, India and China were valued at USD 1.85 billion and USD 3.26 billion, respectively, in 2025.

Asia Pacific is rapidly scaling up the use of petroleum sorbent pads due to industrial expansion and rising oil-handling activities. In 2023 alone, over 16 million sorbent pads were deployed across the region, with China and India accounting for more than 12.5 million units used in refineries, industrial parks, and chemical corridors. Japan added roughly 1.2 million pads in automated warehouses and marine ports, while South Korea and Vietnam consumed 630,000 units for offshore containment.

Japan Petroleum Sorbent Pads Market

The Japan market in 2025 was valued at USD 1.02 billion, accounting for roughly 3.47% of global petroleum sorbent pads revenues. Japan’s petroleum sorbent pad demand is supported by strict industrial safety norms and marine spill preparedness, with over 1 million units deployed annually (2023–2024) across ports, refineries, and high-automation manufacturing facilities.

China Petroleum Sorbent Pads Market

China’s market is projected to be significant globally, with 2025 revenues valued at USD 3.26 billion, representing roughly 11.11% of the global petroleum sorbent pads market.

India Petroleum Sorbent Pads Market

The India market in 2025 was valued at USD 1.85 billion, accounting for roughly 6.31% of global revenues.

North America

North America held the second-highest share in 2025, at USD 9.12 billion, and is also expected to account for a significant share in 2026, at USD 9.53 billion.

North America dominates petroleum sorbent pad demand largely due to its well-developed oil & gas infrastructure, extensive industrial base, and stringent regulatory environment. In 2024, North America accounted for the largest regional share of global sorbent pad consumption, with over 22 million units used, including more than 18.7 million in the U.S. alone, driven by heavy industrial and energy activity in states such as Texas, Louisiana, and North Dakota. These pads are widely used to meet EPA and OSHA spill-response and workplace-safety requirements, including Spill Prevention, Control, and Countermeasure (SPCC) obligations that mandate proactive containment measures for facilities that handle petroleum.

U.S. Petroleum Sorbent Pads Market

Given North America’s strong contribution and the U.S. dominance in the region, the U.S. market was valued at around USD 8.13 billion in 2025, accounting for roughly 27.72% of the global market.

Europe

Europe is projected to record a growth rate of 6.02% in the coming years, which is the highest among all regions, and was valued at USD 7.29 billion in 2025. Europe’s petroleum sorbent pad consumption is propelled by strong industrial activity and tight environmental regulations targeting chemical and oil spills, especially in Germany, France, the U.K., and Italy, where heavy manufacturing and automotive sectors drive usage. Oil-only and hazmat absorbents are increasingly stocked in facilities to meet EU spill-containment directives and workplace safety standards, while bio-based and lightweight absorbents saw a notable uptake in 2023–24 as companies pursue eco-compliance alongside spill readiness.

Germany Petroleum Sorbent Pads Market

The German market in 2025 was valued at USD 1.87 billion and is estimated at around USD 1.98 billion in 2026, representing roughly 6.37% of global petroleum sorbent pads revenues.

Latin America

Latin America is expected to witness moderate growth in this market space during the forecast period. The Latin America market was valued at USD 1.26 billion in 2025. In Latin America, petroleum sorbent pad usage is growing alongside expanding oil exploration and industrial activity, particularly in Brazil, Mexico, and Argentina, where onshore and offshore hydrocarbon operations are increasing routine spill-control needs. The region accounted for roughly 8% of global spill absorbent pad consumption in 2023, reflecting rising awareness among industrial operators of the need for rapid, efficient oil spill response.

Brazil Petroleum Sorbent Pads Market

Brazil's market was valued at USD 0.58 billion in 2025, representing roughly 1.99% of the market.

Middle East & Africa

The Middle East & Africa are expected to witness significant growth in this market space during the forecast period. The Middle East & Africa market was valued at USD 2.49 billion in 2025.

The Middle East & Africa’s petroleum sorbent pad demand is driven by extensive oil production and export infrastructure, with the region accounting for approximately 12% of global pad consumption in 2024. Saudi Arabia petroleum sorbent pads are high-absorbency solutions designed to quickly soak up oil and fuel spills in industrial, marine, and energy applications.

GCC Petroleum Sorbent Pads Market

The GCC market was valued at USD 1.27 billion in 2025, representing roughly 4.32% of the global market.

COMPETITIVE LANDSCAPE

Key Industry Players

Vendors Are Actively Expanding Their Market Share Via Partnerships, Business Expansion, And Technological Advancements

The global petroleum sorbent pads market is highly consolidated, with prominent players including 3M, Sorbent Products Company (SPC), New Pig Corporation, Oil-Dri Corporation, and others. Companies operating in the petroleum sorbent pads market are adopting targeted growth strategies focused on strengthening their product portfolios, technical capabilities, expanding manufacturing presence, and other areas.

- For instance, in full-year 2024, more than 9,200 oil spill incidents were recorded globally, many on offshore platforms and industrial storage sites, highlighting the critical need for rapid containment tools such as petroleum sorbent pads. This elevated spill frequency reinforced their application across emergency response and routine maintenance, especially in oil-handling zones.

Other key players in the global market include Chemtex, Darcy Spillcare Manufacture Ltd., Fentex Ltd., Meltblown Technologies Inc., ENPAC LLC, and others. These companies are expected to prioritize new product launches and collaborations to increase their global market share during the forecast period.

LIST OF KEY PETROLEUM SORBENT PAD COMPANIES PROFILED:

- 3M (U.S.)

- Sorbent Products Company (SPC) (U.S.)

- New Pig Corporation (U.S.)

- Oil-Dri Corporation (U.S.)

- Brady Corporation (U.S.)

- Chemtex (India)

- Darcy Spillcare Manufacture Ltd. (U.K.)

- Fentex Ltd. (U.K.)

- Meltblown Technologies Inc. (U.S.)

- ENPAC LLC (U.S.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: A spill containment training guide highlighted the critical role of oil-only petroleum sorbent pads in safety kits for facilities prone to hydrocarbon leaks. The guide stressed that oil-specific pads outperform universal products in rejecting water while absorbing petroleum, especially in marine and rainy environments. Industrial safety managers were urged to review pad inventories ahead of seasonal weather events.

- November 2025: Petroleum sorbent pads saw increased industrial adoption as global oil and gas activities expanded, driving facilities to enhance spill response capabilities. Operators in the marine, transportation, and heavy manufacturing sectors reported increased integration of high-capacity pads to manage routine leaks and accidental drips, reflecting a growing emphasis on environmental protection and workplace safety compliance. This trend continues as infrastructure usage intensifies.

- February 2025: Safety forums emphasized portable petroleum sorbent pads as frontline tools for rapid cleanup of small to medium hydrocarbon spills at refineries and distribution terminals. Users reported that quick deployment significantly reduced spill spread and minimized downtime, particularly when pads were pre-staged near high-risk equipment. This operational insight boosted routine pad stocking alongside standard PPE.

- June 2024: Coastal cleanup crews increasingly used floating oil absorbent pads to skim petroleum from water surfaces after localized tanker leaks. The lightweight pads repelled water while capturing hydrocarbons, helping crews contain contaminants quickly and protect sensitive shorelines. Emergency teams praised their efficiency compared to booms alone.

- November 2023: Reports from maritime authorities showed a rise in on-deck use of petroleum sorbent pads aboard tankers and offshore platforms following a series of minor hydrocarbon leaks. The pads served as quick-response tools, absorbing oil before it reached seawater, and were credited with mitigating environmental impact in multiple regional incidents.

REPORT COVERAGE

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.83% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Material Type, Structure, End User, and Region |

| By Material Type |

|

| By Structure |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 29.34 billion in 2025 and is projected to reach USD 52.85 billion by 2034.

In 2025, the market value in North America stood at USD 9.12 billion.

The market is expected to grow at a CAGR of 6.83% over the forecast period of 2026-2034.

The polypropylene (PP) segment led the market by material type.

The key factors driving the market include rising oil handling activities, stricter spill-control regulations, and increased emphasis on workplace and environmental safety.

3M, Sorbent Products Company (SPC), New Pig Corporation, and others are prominent players in the market.

Asia Pacific dominated the market in 2025.

Major factors favoring the adoption include higher spill-preparedness requirements, frequent equipment leaks, and a preference for fast, easy-to-deploy oil-only cleanup solutions.

- 2021-2034

- 2025

- 2021-2024

- 128

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us