Pharmaceutical Excipients Market Size, Share & Industry Analysis, By Type (Organic and Inorganic), By Formulation (OSD, Oral Liquids, Parenteral, Topical & Transdermal, Rectal/Vaginal, and Others), By Functionality (Primary Processing & Performance, Stability & Protection, and Others), By Functionality Application (Stabilizers, Taste Masking, Modified-release, Solubility & Bioavailability Enhancement, and Others), By Source (Plant, Animal, Mineral, Synthetic/Petrochemical, and Others), By End User (Pharma & Biopharma Companies, CMOs/CDMOs, and Others), and Regional Forecast, 2026-2034

Pharmaceutical Excipients Market Size and Future Outlook

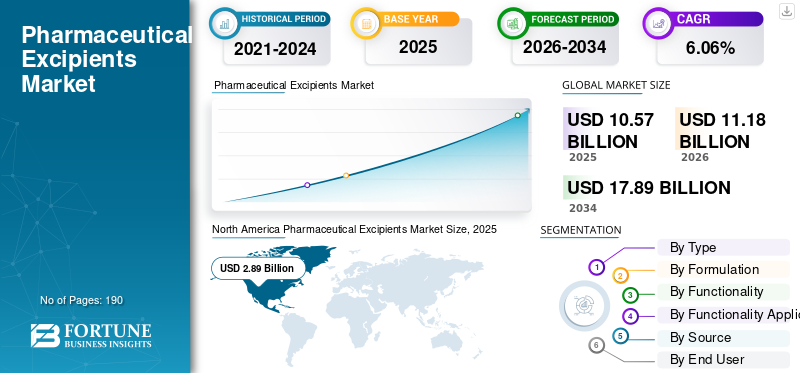

The global pharmaceutical excipients market size was valued at USD 10.57 billion in 2025. The market is projected to grow from USD 11.18 billion in 2026 to USD 17.89 billion by 2034, exhibiting a CAGR of 6.06% during the forecast period. North America dominated the pharmaceutical excipients market with a market share of 27.34% in 2025.

The market is expected to grow steadily over the coming years, driven by rising production of generic drugs, increasing demand for complex drug formulations, and the need to improve drug stability and solubility. As pharmaceutical companies develop more advanced and specialty therapies, the role of excipients becomes more important as these ingredients help medicines perform effectively during manufacturing, storage, and delivery. Additionally, the expansion of biopharmaceuticals and drug-delivery innovation is driving higher demand for functional, high-purity excipients, supporting global market expansion.

Key companies are increasingly focusing on new product launches to capitalize on the market's growth potential and on incorporating capabilities into their excipient solutions.

- For instance, in February 2026, DFE Pharma launched its Continuous Manufacturing (CM) platform to support pharmaceutical companies in formulation development, optimization, and lifecycle management of CM processes. The initiative combined CM-ready excipients, a CM evaluation environment, and multidisciplinary expertise to enable data-driven decisions from early exploration through optimization and long-term CM operations.

Furthermore, leading players such as Roquette Frères, BASF Pharma Solutions, Evonik Industries AG., and Ashland Inc., are focusing on expanding their offerings and strengthening their market positions.

Download Free sample to learn more about this report.

PHARMACEUTICAL EXCIPIENTS MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 10.57 billion

- 2026 Market Size: USD 11.18 billion

- 2034 Forecast Market Size: USD 17.89 billion

- CAGR: 6.06% from 2026–2034

- North America dominated the market with a 27.34% share in 2025.

- The inorganic segment is expected to grow at a CAGR of 6.81% over the forecast period.

- The parenteral segment is projected to grow at a CAGR of 8.43% during the forecast period.

North America

North America led with USD 2.89 billion in 2025, driven by a mature pharmaceutical manufacturing base.

Europe

Europe is projected to reach USD 2.67 billion in 2026, supported by strong R&D and drug production capabilities.

Asia Pacific

Asia Pacific is estimated at USD 3.84 billion in 2026, supported by rising generic drug manufacturing.

U.S.

The market is valued at USD 2.79 billion in 2026, driven by strong demand for high-quality drug formulations.

Japan

The market is estimated at USD 0.87 billion in 2026, supported by advanced pharmaceutical innovation.

Read More

PHARMACEUTICAL EXCIPIENTS MARKET TRENDS

Rising Demand for Multifunctional Excipients in Advanced Drug Formulations is a Significant Market Trend

The global market is witnessing a prominent trend of rising demand for multifunctional excipients in advanced drug formulations. Drug manufacturers are increasingly focusing on improving solubility, stability, taste masking, release control, and manufacturing efficiency simultaneously. As more drugs become complex and more formulations move toward patient-friendly, performance-driven formats, companies prefer excipients that can play multiple roles within a single formulation. This reduces formulation complexity, shortens development timelines, and improves process consistency, which, in turn, supports greater adoption of multifunctional excipients across the market.

- For instance, in September 2024, Evonik announced the start of operations at a new spray-drying facility for EUDRAGIT polymers in Darmstadt to meet increasing demand from pharmaceutical customers for oral drug delivery solutions. This development reflects the growing demand for advanced, multifunctional excipient systems, encouraging manufacturers to expand production capacity and strengthen supply reliability.

MARKET DYNAMICS

MARKET DRIVERS

Rising Generic Drug Production Driving Demand for Pharmaceutical Excipients to Drive Growth

The global market is driven by rising generic drug production. Generic manufacturers require large volumes of excipients such as fillers, binders, disintegrants, coatings, and stabilizers to develop cost-effective and scalable formulations. As patent expiries continue to increase the number of off-patent drugs entering the market, pharmaceutical companies are expanding generic production, which directly raises demand for standard and functional excipients, creating consistent volume demand and broader adoption across generic drug manufacturing. These factors also encourage key players to invest in new product launches.

- For instance, in October 2023, Roquette Frères launched three new excipient grades for moisture protection at CPHI Barcelona, designed to support moisture-sensitive pharmaceutical and nutraceutical ingredients. This development reflected growing demand for generics and formulations, encouraging excipient manufacturers to expand their product portfolios at scale.

MARKET RESTRAINTS

High Quality-Control and Supplier-Qualification Burden to Hamper Market Growth

The global market faces significant constraints due to the high burden of quality control and supplier qualification. Excipients directly affect the safety, stability, and performance of finished drug products. As a result, pharmaceutical manufacturers must conduct detailed supplier audits, document reviews, contamination risk checks, and repeat quality assessments before approving or continuing excipient sourcing. These complex procedures make procurement and formulation development more time-consuming and expensive. These factors can result in slower adoption and increased operating costs, which can restrain faster market expansion.

- For instance, in June 2025, the Radiology Society of North America published an article titled 'Integrating Imaging Tools Helps Radiology AI Deliver Real Value' that highlighted interoperability remains a critical but often overlooked requirement for imaging tools to deliver value, showing that poor system connectivity continues to be a practical barrier in radiology workflow software adoption.

MARKET OPPORTUNITIES

Broader Demand across Oral, Respiratory, Ophthalmic, and Parenteral Dosage Forms to Offer Significant Opportunities

The global market is gaining growth opportunities from broader demand across oral, respiratory, ophthalmic, and parenteral dosage forms. Drug manufacturers are not relying only on conventional tablet formulations. As more therapies are being developed in inhalation, sterile injectable, eye care, and other specialized formats, the need for excipients with specific performance, purity, and safety profiles is increasing. These factors are collectively encouraging excipient companies to diversify their portfolios and support multiple formulation platforms. As a result, suppliers that can serve a wider range of dosage forms are getting stronger opportunities to expand their customer base and increase market penetration.

- For instance, in January 2025, DFE Pharma expanded its Closer to the Formulator (C2F) Center of Excellence in Hyderabad to advance the development of critical respiratory treatments. This development highlights that excipient suppliers are investing in formulation support beyond traditional oral dosage forms, creating new commercial opportunities in specialized drug delivery to expand into higher-value applications.

MARKET CHALLENGES

Strict Regulatory Requirements and Approval Complexity pose a Challenge for Market Growth

The global pharmaceutical excipients market faces challenges from strict regulatory requirements and complex approval processes, as excipients are directly linked to the safety, quality, and performance of finished drug products. As a result, companies must generate extensive safety data, maintain detailed documentation, meet compendial and GMP expectations, and manage region-specific compliance requirements before excipients can be widely adopted in formulations. This makes the introduction of new or advanced excipients slower and more expensive, especially when regulatory pathways are not fully harmonized across markets. Because of this, innovation adoption can be delayed, and product development costs can rise, creating a clear challenge for pharmaceutical excipients market growth.

- For instance, in 2024, a USP policy paper highlighted that novel excipients face significant regulatory, safety, and cost-related barriers and noted that the lack of globally aligned regulatory mechanisms can increase the risk of drug development discontinuation or costly reformulation. Such regulatory uncertainty can discourage faster excipient innovation and wider commercial adoption.

Download Free sample to learn more about this report.

Segmentation Analysis

By Type

High Utilization of Organic Excipients to Lead the Segmental Growth

Based on type, the market is categorized into organic and inorganic.

The organic chemicals holding the largest pharmaceutical excipients market share stems from its widespread use as pharmaceutical excipients in tablets, capsules, liquids, and advanced drug delivery systems. Excipients such as cellulose derivatives, povidones, copovidones, cyclodextrins, and other organic solubilizers are used repeatedly for binding, coating, controlled release, and bioavailability enhancement. These materials can serve multiple formulation needs across a broad range of dosage forms. This broad applicability, higher formulation dependence, and strategic initiatives by key companies are expected to keep organic chemicals as the leading segment.

- For instance, in October 2024, Colorcon partnered with LOTTE Fine Chemical to launch the AnyCoat hypromellose product family, covering polymers for immediate, controlled, and enteric-release applications.

The inorganic segment is expected to grow at a CAGR of 6.81% over the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Formulation

Cost Efficiency and Wide Usage of Oral Solid Dosage Leads to its Dominance

Based on formulation, the market is segmented into oral solid dosage, oral liquids, parenteral, topical & transdermal, pulmonary & nasal, ophthalmic & otic, rectal/vaginal, and others.

In 2025, the oral solid dosage segment dominated the market as tablets and capsules remain the most widely used and most cost-efficient pharmaceutical dosage forms worldwide. These formats require large and recurring volumes of excipients for filling, binding, disintegration, coating, flow improvement, and release control. Also, they are easier to manufacture, transport, store, and scale up for commercial use, leading drug manufacturers to rely heavily on them. This directly keeps the excipient demand highest in the OSD segment. Key companies are focusing on expanding their manufacturing facilities to strengthen their market positions.

- For instance, in September 2024, Evonik began operations at a new spray-drying facility for pharmaceutical oral excipients in Darmstadt to meet increasing demand for oral drug-delivery solutions. Such capacity expansion reflects the large and sustained demand coming from oral solid formulations.

The parenteral segment is projected to grow at a CAGR of 8.43% during the global pharmaceutical excipients market forecast period.

By Functionality

Primary Processing and Performance Functionality Leads Due to Increasing Adoption for a Core Application

Based on functionality, the market is classified into primary processing & performance roles, stability & protection roles, patient experience & adherence roles, device-compatibility roles, and others.

In 2025, primary processing and performance roles led the market, as pharmaceutical formulations require core excipient functions such as filling, binding, flow support, lubrication, compression support, and disintegration before any advanced features are added. These functions are essential at the beginning of formulation design and remain necessary through commercial manufacturing. As they are foundational applications, their usage spans a much larger number of products than more specialized roles. This makes primary processing and performance functions the largest segment of functionality.

- For instance, in February 2026, DFE Pharma launched its Continuous Manufacturing platform to support formulation development using CM-ready excipients designed for stable processing, simplified system design, and robust lifecycle performance. This supports the dominance of primary processing and performance roles by highlighting manufacturers' continued investment in excipients that improve processing consistency and manufacturing efficiency at scale.

The device-compatibility roles segment is projected to grow at a CAGR of 8.88% during the study period.

By Functionality Application

Immediate-Release & Content Uniformity Dominates Due to its Uniform API Distribution

Based on functionality application, the market is sub-segmented into stabilizers, taste masking, modified-release, solubility & bioavailability enhancement, immediate-release & content uniformity enablement, injectability & parenteral compatibility, preservation & microbial control, and other functionality applications.

The immediate-release & content uniformity enablement accounted for the largest pharmaceutical excipients market share and also holds a large share of pharmaceutical products. These products depend heavily on excipients that ensure uniform API distribution, reliable blending, compressibility, and consistent release during routine high-volume manufacturing. Since immediate-release products are used across a broad range of therapy areas and generic portfolios, the excipient demand linked to this application remains larger than that for more specialized uses such as modified release or injectability support, positioning them in a leading position. Key companies also strategize for innovative product launches to capitalize on growth.

- For instance, in October 2022, Roquette launched PEARLITOL 200 GT and PEARLITOL CR-H for direct compression, highlighting improved flowability, processability, and high-speed tableting performance. Such innovation supports the leadership of immediate-release and content uniformity enablement to improve blend consistency and tablet manufacturability.

The solubility & bioavailability enhancement sub-segment is projected to grow at a CAGR of 7.57% during the study period.

By Source

High Availability of Plant-Based Excipients Fuel Segment Growth

Based on source, the market is fragmented into plant-derived, animal-derived, mineral-derived, synthetic/petrochemical-derived, and others.

Plant-derived excipients are estimated to dominate the market, as many of the most commonly used excipients in oral formulations are derived from plants. Formulators widely accept these materials because they offer strong functionality, broad regulatory familiarity, and suitability across tablets, capsules, and other patient-friendly dosage forms. In addition, growing industry interest in naturally sourced and widely established materials continues to support their use in both conventional and advanced formulations. This is expected to keep plant-derived excipients ahead of other source categories.

- For instance, in February 2025, Roquette launched a new high-performance pharmaceutical coatings platform, designed to meet growing demand in prescription pharmaceutical, nutraceutical, and OTC markets. The development supports the dominance of plant-derived excipients and continues to drive innovation in botanical-source excipient systems.

The mineral-derived segment is projected to grow at a CAGR of 6.89% during the study period.

By End User

Pharmaceutical & Biopharmaceutical Companies are Leading End Users Due to their Large Patient Volumes

Based on end user, the market is sub-divided into pharmaceutical & biopharmaceutical companies, CMOs/CDMOs, research & academic institutes, and others.

The pharmaceutical and biopharmaceutical companies are estimated to dominate as they are the primary developers, owners, and large-scale manufacturers of finished drug products. These companies continuously consume excipients across formulation development, scale-up, regulatory filings, commercial production, and lifecycle management. They also have broader product pipelines and higher procurement volumes than academic institutes or smaller outsourced users. As they represent the largest and most consistent demand base for excipient suppliers, they are expected to remain the leading end-user segment.

- For instance, in June 2025, BASF opened a new GMP Solution Center in Michigan to support pharmaceutical and biopharmaceutical customers with excipients, bioprocessing ingredients, customized chemistries, and high-quality manufacturing support. Such investments reflect excipient suppliers' prioritization of pharmaceutical and biopharmaceutical companies as their largest commercial customer base, reinforcing this segment's dominance.

The CMOs/CDMOS segment is projected to grow at a CAGR of 8.31% over the study period.

Pharmaceutical Excipients Market Regional Outlook

By geography, the market is categorized into Europe, North America, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Pharmaceutical Excipients Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America held the dominant share in 2024 at USD 2.75 billion and maintained its leading position in 2025 with USD 2.89 billion. The regional market is growing as it has a large and mature pharmaceutical manufacturing base, strong regulatory oversight, and continued demand for high-quality drug production across oral solids, sterile products, and biologics. This increases the use of functional and high-purity excipients that support formulation performance, stability, and GMP-compliant manufacturing.

U.S. Pharmaceutical Excipients Market

Given North America's substantial contribution and the U.S. dominance in the region, the U.S. market is estimated at around USD 2.79 billion in 2026, accounting for roughly 25.01% of the global market.

Europe

Europe is projected to grow at 5.02% over the coming years, the second-highest among all regions, and reach a valuation of USD 2.67 billion by 2026. The market is growing in Europe because the region remains a major manufacturing hub for innovative medicines and related ingredients, supported by a strong research-based pharmaceutical industry. Since the region continues to invest in pharmaceutical production and supply security, demand for reliable, performance-driven excipients remains strong across multiple dosage forms.

U.K. Pharmaceutical Excipients Market

The U.K. is estimated at around USD 0.51 billion in 2026, representing roughly 4.57% of the global market.

Germany Pharmaceutical Excipients Market

Germany's market will reach approximately USD 0.61 billion in 2026, equivalent to around 5.48% of the global market.

Asia Pacific

In 2026, Asia Pacific is estimated to reach USD 3.84 billion secure third position in the market as emerging economies such as India are expanding pharmaceutical production, generic drug manufacturing, and exports rapidly. As production volumes rise and formulation capabilities improve, excipient demand also increases because these materials are essential for scale-up, cost efficiency, and finished-dose performance.

Japan Pharmaceutical Excipients Market

Japan is estimated to achieve USD 0.87 billion in 2026, which accounts for approximately 7.82% of the global market.

China Pharmaceutical Excipients Market

China's market is projected to be one of the largest worldwide, with 2026 revenues projected to reach USD 1.26 billion, representing approximately 11.26% of global sales.

India Pharmaceutical Excipients Market

India pharmaceutical excipients market in 2026 is estimated at around USD 0.51 billion, accounting for roughly 4.54% of global revenue.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa are expected to witness moderate growth in this market space during the forecast period. Latin America is set to reach a valuation of USD 0.90 billion in 2026. The market is growing in Latin America as Brazil and Mexico strengthen local pharmaceutical production and reduce dependence on imports through industrial and policy support. In the Middle East & Africa, the GCC is set to reach USD 0.35 billion in 2026.

South Africa Pharmaceutical Excipients Market

The South African market is projected to reach approximately USD 0.09 billion in 2026, accounting for roughly 0.78% of global revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations by Key Players to Propel Market Progress

The global pharmaceutical excipients market is highly consolidated, with companies such as Roquette Frères, BASF Pharma Solutions, Evonik Industries AG, Ashland Inc., Croda Pharma, MEGGLE Excipients, Shin-Etsu Chemical Co., Ltd. holding significant market share. Strategic partnerships, new product launches, technological advancements, and increased investments in the sector drive these companies' market share.

- For instance, in October 2025, Shin-Etsu collaborated with Biogrund as its new distribution partner for pharmaceutical excipients in Spain. The collaboration focused on the dietary supplement sector in Europe and has now expanded to include the Spanish pharmaceutical market.

Other notable players in the global market include SPI Pharma, Inc., JRS Pharma GmbH & Co. KG, and Colorcon Limited. These companies are expected to prioritize technological advancements, strategic collaborations, and new product launches to strengthen their positions during the forecast period.

LIST OF KEY PHARMACEUTICAL EXCIPIENTS COMPANIES PROFILED

- Roquette Frères (France)

- BASF Pharma Solutions (Germany)

- Evonik Industries AG (Germany)

- Ashland Inc. (U.S.)

- Croda Pharma (U.S.)

- MEGGLE Excipients (Germany)

- SPI Pharma, Inc. (U.S.)

- JRS Pharma GmbH & Co. KG (Germany)

- Shin-Etsu Chemical Co., Ltd. (Japan)

- Colorcon Limited (U.K.)

KEY INDUSTRY DEVELOPMENTS

- November 2025: Clariant completed its facility expansion at Daya Bay, China. This strategic investment marked a significant milestone in the company's Asia growth strategy, enhancing its manufacturing capacity, supply resilience, and product portfolio for pharmaceutical excipients and specialty chemicals.

- October 2025: Global pharma major Lupin Limited (Lupin) announced the launch of a strategic partnership program aimed at expanding the reach of PrecisionSphere – the long-acting injectable (LAI) platform developed by its subsidiary, Nanomi B.V. (Nanomi). Precision Sphere demonstrates efficacy and safety in drug delivery and is ready for commercial use following recent U.S. FDA approval of the first product developed with this platform.

- October 2025: Asahi Kasei Corporation launched two new specialty grades in its Sonanos Next-Generation Excipients portfolio. These products are manufactured in compliance with Good Manufacturing Practice (GMP). Sonanos are excipients designed to improve the formulation of injectable drugs.

- September 2025: Evonik collaborated with Ethris, a clinical-stage biotechnology company pioneering next-generation RNA therapeutics and vaccines, to develop and market a novel lipid nanoparticle (LNP) platform for nucleic acid delivery.

- June 2025: BASF SE inaugurated its new Good Manufacturing Practice (GMP) Solution Center in Wyandotte, Michigan. The development underscored the company's commitment to providing innovative solutions in the biopharma and pharmaceutical ingredients industries, including the reliable supply of bioprocessing ingredients and excipients for biopharma applications as well as small molecules.

REPORT COVERAGE

The global market analysis includes a comprehensive study of market size and forecast across all the market segments covered in the report. It contains details on the market dynamics and trends expected to drive the global market over the forecast period. It provides information on key aspects, including product innovation, formulation advancements, and the growing use of functional excipients across pharmaceutical applications. Additionally, it details partnerships, expansions, mergers & acquisitions, and other important industry developments. The global market research report also provides a detailed competitive landscape, including global market share and profiles of major operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 6.06% from 2026 to 2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Type, Formulation, Functionality, Functionality Application, Source, End User, and Region |

| By Type |

|

| By Formulation |

|

| By Functionality |

|

| By Functionality Application |

|

| By Source |

|

| By End User |

|

| By Region |

|

Frequently Asked Questions

According to Fortune Business Insights, the global market value stood at USD 10.57 billion in 2025 and is projected to reach USD 17.89 billion by 2034.

In 2025, North America’s market value stood at USD 2.89 billion.

The market is expected to grow at a CAGR of 6.06% over the forecast period of 2026-2034.

The organic segment is expected to lead the market.

Rising generic drug production is driving the need for efficient excipients and market growth.

Roquette Frères, BASF Pharma Solutions, Koninklijke Philips N.V., Ashland Inc., and Croda Pharma are the major market players in the global market.

North America dominated the market in 2025 in terms of share.

- 2021-2034

- 2025

- 2021-2024

- 190

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us