Plastic Pipes Market Size, Share & Industry Analysis, By Material (Polyvinyl Chloride (PVC), Polyethylene (PE), Polypropylene (PP), Acrylonitrile Butadiene Styrene (ABS), and Others), By Application (Building & Construction, Agriculture, Oil & Gas, Industrial, and Others), and Regional Forecast, 2026-2034

Plastic Pipes Market Size and Future Outlook

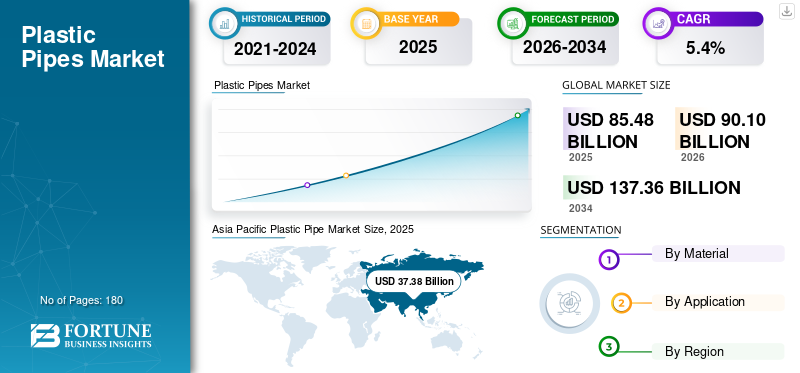

The global plastic pipes market size was valued at USD 85.48 billion in 2025. The market is projected to grow from USD 90.10 billion in 2026 to USD 137.36 billion by 2034, exhibiting a CAGR of 5.4% during the forecast period. Asia Pacific dominated the global plastic pipes market with a market share of 43.72% in 2025.

Plastic fluid pipes are widely used in water supply, wastewater, drainage, irrigation, gas distribution, and industrial transport systems. Demand is closely linked to construction activity, urban growth, and public infrastructure spending. Compared with metal and concrete pipes, plastic pipes offer strong corrosion resistance, a long service life, and easier installation, resulting in lower overall costs. Globally, market demand is driven mainly by the replacement of aging pipeline networks, the gradual expansion of municipal utilities, and ongoing upgrades in agricultural and industrial systems, rather than rapid, capacity-led volume growth, supported by regulatory standards and long-term infrastructure reliability requirements worldwide programs.

The market is dominated by a large group of plastic pipe manufacturers with established extrusion capacity and wide distribution networks. Major players such as JM EAGLE, INC., Aliaxis, GF Industry and Infrastructure Flow Solutions, Wavin Industries Limited, and Finolex Industries Ltd., focus on PVC, HDPE, and PP pipe systems, regulatory compliance, and consistent supply reliability. This results in a moderately consolidated market characterized by steady infrastructure-led demand, high switching costs, and controlled capacity.

Download Free sample to learn more about this report.

PLASTIC PIPES MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 85.48 billion

- 2026 Market Size: USD 90.10 billion

- 2034 Forecast Market Size: USD 137.36 billion

- CAGR: 5.4% from 2026–2034

- Asia Pacific dominated the plastic pipes market with a 43.72% share in 2025.

- The polyethylene (PE) segment accounted for the largest market share in 2025.

- The building & construction segment held the largest share of the market in 2025.

North America

North America accounted for USD 16.67 billion in 2025, driven by ongoing replacement of aging water, sewer, and drainage infrastructure across the region.

Europe

Europe reached USD 19.84 billion in 2025, with demand supported by building renovation projects, wastewater infrastructure upgrades, and pipeline replacement activities.

Asia Pacific

Asia Pacific led the global market with a value of USD 37.38 billion in 2025 and is expected to reach USD 39.63 billion in 2026, supported by strong construction and water infrastructure investments.

U.S.

The market was valued at USD 14.30 billion in 2025, representing approximately 85.8% of North American revenues, supported by construction activity and municipal pipeline replacement projects.

Japan

Demand is driven by water infrastructure modernization, urban utility maintenance, and the adoption of durable piping solutions across residential and municipal applications.

Read More

PLASTIC PIPES MARKET TRENDS

Increasing Focus on Performance and Lifecycle Efficiency Is Shaping the Market

A key trend in the plastic pipes market is the growing focus on performance, durability, and lifecycle cost rather than just initial price. Buyers are increasingly selecting pipes based on pressure strength, long service life, and resistance to corrosion or chemicals. In response, manufacturers are improving material quality, product design, and compliance with stricter standards. This shift is gradually changing product portfolios and competitive positioning, as reliability and long-term performance become more important in purchasing decisions.

- According to the Bureau of Indian Standards (BIS), Government of India, BIS has formulated more than 22,000 Indian Standards, including mandatory standards for plastic pipes used in water supply, drainage, and building applications, supporting the shift toward performance-and quality-driven pipe selection.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Building and Construction Activity Sustains Demand for Plastic Pipes

Plastic pipe demand is largely driven by building and construction activity, particularly in residential and commercial developments. Pipes made from PVC and HDPE are widely used in internal plumbing, drainage, rainwater, and sewage systems due to their durability, corrosion resistance, and ease of installation. Ongoing housing construction, renovation of existing buildings, and compliance with modern building codes continue to support steady demand for plastic pipes, as every new structure and retrofit directly adds to baseline pipe demand rather than discretionary use.

- According to the Ministry of Jal Shakti, Government of India, 15.76 crore rural households have received tap water connections under the Jal Jeevan Mission, supporting large-scale use of plastic pipes in water infrastructure.

MARKET RESTRAINTS

Regulatory Standards and Approval Processes to Limit Market Expansion

Plastic pipe adoption can be constrained by strict regulatory standards, certification requirements, and lengthy approval processes, especially in municipal and public infrastructure projects. Different regions enforce specific material, pressure, and safety standards, which can delay project execution and limit the use of certain plastic pipe types. Compliance costs and extended testing timelines can slow new product adoption, particularly for smaller manufacturers, reducing overall market momentum despite steady underlying demand.

- According to the Press Information Bureau, Government of India, the construction sector in India grew by 9.4% in FY 2024-25, reflecting strong activity but also highlighting how demand can fluctuate with economic conditions and public investment cycles.

MARKET OPPORTUNITIES

Adoption of Advanced Plastic Pipe Systems Creates Strong Growth Opportunities

Growth opportunities in the market are emerging from the increasing use of advanced piping systems in modern buildings. Products such as pressure-rated HDPE pipes, multilayer pipes, and low-noise drainage systems offer better durability, strength, and performance than conventional options. As building standards and customer preferences shift toward higher performance and longer service life, especially in commercial and high-rise construction, demand for value-added plastic pipe solutions is expected to grow beyond basic construction-driven volumes.

- According to the Ministry of Housing and Urban Affairs, Government of India, 1.18 crore houses have been sanctioned under Pradhan Mantri Awas Yojana in December 2024, supporting sustained demand for plastic pipes in residential construction.

MARKET CHALLENGES

Volatility in Polymer Resin Prices Affects Margin Stability for Plastic Pipe Manufacturers

Plastic pipes market growth hinders due to frequent price changes in key raw materials, such as PVC and HDPE resins. These resin prices move in line with crude oil and broader petrochemical market conditions, making cost planning difficult. When demand from construction projects is weak, manufacturers often cannot fully pass along higher input costs to customers, putting pressure on profit margins. This cost uncertainty increases financial risk and highlights the need for efficient sourcing and inventory management.

- According to the Press Information Bureau, Government of India, the government has implemented support measures, such as the Raw Material Assistance (RMA) Scheme, to help manufacturers manage rising, volatile raw material prices, highlighting the persistent cost pressures faced by industrial sectors producers.

Segmentation Analysis

By Material

Polyethylene (PE) Pipes Segment Dominated due to their Extensive Use in Water Supply

Based on material, the market is segmented into Polyvinyl Chloride (PVC), Polyethylene (PE), Polypropylene (PP), Acrylonitrile Butadiene Styrene (ABS), and others.

The polyethylene (PE) segment accounted for the largest plastic pipes market share in 2025. PE pipes lead consumption due to their extensive use in water supply, gas distribution, sewage, and industrial fluid transport applications, where flexibility, high-pressure resistance, and long service life are critical. Demand for PE pipes is functionally driven by utility and infrastructure requirements rather than discretionary use. As infrastructure networks expand and aging pipelines are replaced, PE remains the most structurally important material segment in the market.

The Polyvinyl Chloride (PVC) segment is expected to grow at a CAGR of about 5.2%, driven by continued use in plumbing and drainage systems due to its low cost, durability, and ease of installation in building construction.

To know how our report can help streamline your business, Speak to Analyst

By Application

Building & Construction Segment Led the Market due to their Ease of Installation

By application, the market is segmented into building & construction, agriculture, oil & gas, industrial, and others.

The building & construction segment accounted for the largest share in 2025, as piping systems are essential for plumbing, drainage, sewage, and rainwater management in residential and commercial structures. Plastic pipes are preferred due to their corrosion resistance, ease of installation, and long service life. As building codes increasingly emphasize durability, water efficiency, and lifecycle performance, plastic pipes remain a standard choice in both new construction and renovation projects, creating a stable and regulation-supported demand base beyond short-term construction cycles.

- According to the U.S. Census Bureau, total U.S. construction spending reached USD 2,169.5 billion in August 2025, reflecting the scale of ongoing building and infrastructure activity that supports demand for piping systems, including plastic pipes.

The agriculture segment is expected to grow at a CAGR of 6.6% over the forecast period.

Plastic Pipes Market Regional Outlook

By geography, the market is categorized into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Asia Pacific

Asia Pacific Plastic Pipe Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific held the dominant position in the plastic pipes market in 2025, valued at USD 37.38 billion, and is expected to retain its leading role in 2026, reaching USD 39.63 billion. The region’s leadership is supported by rapid urbanization, large-scale residential construction, and extensive investment in water supply and sanitation infrastructure. Strong demand from building and construction, municipal utilities, agriculture, and industrial applications continues to support high-volume consumption of plastic pipes, particularly in cost-efficient and durable piping systems across developing and mature markets in the region.

China Plastic Pipes Market

Based on Asia Pacific’s strong contribution and China’s large-scale construction and manufacturing base, the China market reached USD 13.66 billion in 2025, accounting for approximately 36.5% of global revenues. Demand is driven by residential and commercial construction, expansion of water supply and drainage networks, and continued urban infrastructure investment. China’s extensive domestic manufacturing capacity further supports high-volume consumption of plastic pipes across municipal, agricultural, and industrial applications.

India Plastic Pipes Market

The India market in 2025 reached around USD 7.32 billion. Growth is supported by expanding residential and commercial construction, rising investment in water supply and sanitation infrastructure, and increased use of the product in agriculture and irrigation, driven by urbanization nationwide.

North America

North America remains a significant regional market for plastic pipes and is expected to reach USD 16.67 billion in 2025. Demand is supported by residential and v q, the ongoing replacement of aging water, sewer, and drainage infrastructure. The region benefits from established manufacturing capacity, well-developed distribution networks, and strict quality standards. However, market growth remains moderate, reflecting high penetration levels and the mature nature of construction and utility markets.

U.S. Plastic Pipes Market

The market in the U.S. in 2025 reached USD 14.30 billion, representing approximately 85.8% of regional revenues. Consumption is driven by residential and commercial construction, the replacement of aging water and sewer pipelines, and ongoing demand from municipal, agricultural, and industrial fluid-handling applications that require durable, reliable piping systems.

Europe

Europe recorded modest growth in the plastic pipes market, reaching a valuation of USD 19.84 billion in 2025. Strict regulatory standards, high energy costs, and mature construction markets characterize the region. Despite these constraints, steady demand from building renovation, water and wastewater infrastructure upgrades, and replacement of aging pipelines continues to support plastic pipe consumption across residential and municipal applications.

Germany Plastic Pipes Market

Germany’s market reached around USD 4.37 billion in 2025, representing approximately 22.0% of regional demand. Consumption is supported by construction activity, building renovations, and ongoing investment in water supply and wastewater infrastructure, all under strict quality and performance standards.

U.K. Plastic Pipes Market

The U.K. market in 2025 stood at USD 2.86 billion, accounting for roughly 14.4% of regional revenues. Consumption is concentrated in residential and commercial construction, water and drainage systems, and the ongoing replacement of aging pipeline infrastructure.

Latin America and the Middle East & Africa

The Latin America and Middle East & Africa regions are expected to witness moderate growth in the market over the forecast period. The Latin America market reached USD 6.54 billion in 2025, supported by infrastructure development, residential construction, and expanding agricultural irrigation networks across key economies. Gradual upgrades also aid demand in water supply and drainage systems. In the Middle East & Africa, growth is driven by urban development, desalination-linked water distribution projects, and oil and gas infrastructure investment. The MEA plastic pipes market reached USD 5.04 billion in 2025, supported by construction expansion projects.

GCC Plastic Pipes Market

The GCC plastic pipes market accounted for around USD 2.50 billion in 2025, representing approximately 49.6% of regional revenues. Demand is driven by construction activity, water and sanitation infrastructure projects, and ongoing urban and industrial development across major GCC economies.

COMPETITIVE LANDSCAPE

Key Industry Players

High Capital Intensity and Strategic Asset Management Shape Competition in the Market

The plastic pipes market is relatively consolidated and capital-intensive, as large-scale extrusion operations, material certification requirements, and established distribution networks create significant barriers to entry. These factors limit new participation and concentrate supply among a group of regional and global plastic pipe manufacturers with established production scale and technical expertise.

Key players, such as JM EAGLE, INC., Aliaxis, GF Industry and Infrastructure Flow Solutions, Wavin Industries Limited, and Finolex Industries Ltd., focus primarily on optimizing manufacturing efficiency, expanding product portfolios, and strengthening distribution reach rather than pursuing aggressive capacity expansion. Recent activities across these companies highlight a strategic emphasis on operational efficiency, regulatory compliance, and value-added pipe solutions to support long-term market positioning.

LIST OF KEY PLASTIC PIPES COMPANIES PROFILED

- JM EAGLE, INC. (U.S.)

- CHINA LESSO (China)

- Aliaxis (Belgium)

- Prince Pipes and Fittings Ltd. (India)

- Amiblu Holding GmbH (Austria)

- GF Industry and Infrastructure Flow Solutions (Switzerland)

- Wavin Industries Limited (Netherlands)

- REHAU (Germany)

- Finolex Industries Ltd (India)

- Chevron Phillips Chemical Company LLC. (U.S.)

KEY INDUSTRY DEVELOPMENTS

- November 2023: Georg Fischer AG completed the acquisition of Uponor Corporation, integrating Uponor’s plastic piping systems into its GF Piping Systems division to create a global leader in sustainable water and flow plastic solutions.

- June 2023: Aliaxis SA completed the acquisition of the manufacturing division of Valencia Pipe Company in the U.S., expanding its presence in North America and strengthening its plastic pipe production and distribution footprint.

- August 2024: Australian pressure pipe manufacturer into the Amiblu Group to expand its presence in the Asia-Pacific region and strengthen its portfolio of large-diameter pipe systems for water supply and wastewater infrastructure applications.

- August 2020: Prince Pipes and Fittings Ltd. partnered with Lubrizol Advanced Materials to launch the CPVC piping solution in India, enhancing its CPVC plastic plumbing pipe portfolio for residential and commercial building applications.

REPORT COVERAGE

The global market analysis provides an in-depth study of market size & forecast by all the market segments included in the report. It includes details on the market dynamics and market trends expected to drive the market in the forecast period. It offers information on technological advancements, new product launches, key industry developments, and partnerships, mergers & acquisitions. The market research report also encompasses a detailed competitive landscape, including market share and profiles of key operating players.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 5.4% from 2026 to 2034 |

|

Unit |

Value (USD Billion) Volume (Kiloton) |

|

Segmentation |

By Material, Application, and Region |

|

By Material |

|

|

By Application |

|

|

By Geography |

North America (By Material, Application, and Country) o U.S. (By Application) o Canada (By Application) Europe (By Material, Application, and Country) o Germany (By Application) o U.K. (By Application) o France (By Application) o Italy (By Application) o Spain (By Application) o Rest of Europe (By Application) Asia Pacific (By Material, Application, and Country) o China (By Application) o India (By Application) o Japan (By Application) o South Korea (By Application) o Rest of Asia Pacific (By Application) Latin America (By Material, Application, and Country) o Brazil (By Application) o Mexico (By Application) o Rest of Latin America (By Application) Middle East & Africa (By Material, Application, and Country) o GCC (By Application) o South Africa (By Application) o Rest of the Middle East & Africa (By Application) |

Frequently Asked Questions

Fortune Business Insights says that the global market size was valued at USD 85.48 billion in 2025 and is projected to reach USD 137.36 billion by 2034.

Recording a CAGR of 5.4%, the market is slated to exhibit steady growth during the forecast period (2026-2034).

By application, the building & construction segment led in 2025.

Asia Pacific held the highest market share in 2025.

Sustained building and infrastructure construction activity is the key factor driving market growth.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us