Point of Care (POC) CT Imaging Systems Market Size, Share & COVID-19 Impact Analysis, By Product Type (Full-sized, Compact), By Application (Hospitals, Ambulatory Surgical Centers, Radiology Centers, and Clinics), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

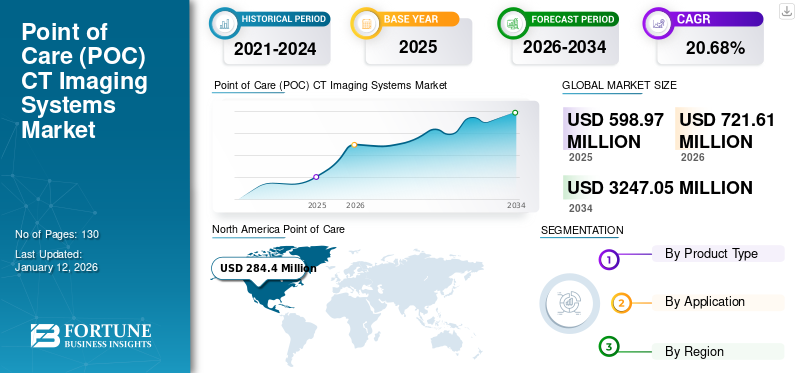

The global point of care (POC) CT imaging systems market size was valued at USD 598.97 million in 2025 and is projected to grow from USD 721.61 million in 2026 to USD 3247.05 million by 2034, exhibiting a CAGR of 20.68% during the forecast period. North America dominated the point of care (POC) CT imaging systems market with a market share of 47.48% in 2025.

The major factors propelling the dynamic growth of this market include the increasing adoption of point of care equipment in outpatient and inpatient healthcare facilities. Additionally, the striking increase in emergency room visits has also aided the growth of the market in recent years. Countries in North America and Europe have significantly aided the point of care CT imaging system market growth owing to the wider acceptance of advanced imaging solutions in these regions.

Disruptions in the Manufacturing on POC CT Imaging Equipment amid COVID-19 to Hamper Growth

There has been a surge in the demand for imaging services across the globe. However, hindrances in production and manufacturing have had a negative impact on the global POC CT market. The key players in the market have delayed the launch of certain products in emerging economies owing to the increasing number of active cases of coronavirus recorded in these countries. For instance, companies such as Siemens have experienced a decrease of 20% in their revenue sales of imaging modalities. On the other hand, the production activities of some of the market players have been affected due to the unavailability of locally-sourced raw materials or parts.

Furthermore, the changing and uncertain geopolitical situation globally, as a result of the outbreak of the coronavirus, has left manufacturers and key players distraught due to the disruptions in the export and import of raw materials and finished goods. This has led the players in the market to re-evaluate the traditional supply and value chains of the market.

Download Free sample to learn more about this report.

Point of Care (POC) CT Imaging Systems Market Overview

Market Size & Forecast:

- 2025 Market Size: USD 598.97 million

- 2026 Market Size: USD 721.61 million

- 2034 Forecast Market Size: USD 3247.05 million

- CAGR: 20.68% from 2026 to 2034

Market Share:

- North America market share was valued at USD 47.48% in 2025, reflecting the region’s early adoption of advanced POC CT imaging technologies and strong healthcare infrastructure.

- The full-sized POC CT imaging systems segment held the largest market share in 2026 due to their wide use in large hospitals and healthcare facilities. However, the compact segment is expected to register significant growth, driven by innovations in portable CT systems.

Key Country Highlights:

- United States: Leading market player focus is on securing FDA approvals and launching innovative POC CT imaging products. The U.S. witnessed increased emergency department visits (139 million in 2018) boosting demand for quick and accurate imaging solutions in critical care and trauma cases. Rising adoption in outpatient and inpatient settings also propels growth. Siemens’ FDA-approved SOMATOM On.site mobile CT scanner is an example of the innovation driving the market.

- Canada: Growth driven by investments in advanced imaging infrastructure and rising preference for outpatient diagnostic services. Healthcare reforms encourage integration of POC imaging to reduce hospital stays.

- Europe: Countries such as Germany, the UK, and France demonstrate strong demand for POC CT imaging, bolstered by government reimbursements for ambulatory surgical centers and advanced outpatient care. The region is characterized by the rapid adoption of innovative AI-powered imaging technologies improving diagnostic efficiency.

- Asia Pacific: The market faced setbacks due to COVID-19, especially disruptions in China—the major OEM supplier—impacting supply chains and manufacturing. However, growing healthcare infrastructure in developing nations and increasing awareness may fuel growth post-pandemic.

- Latin America & Middle East & Africa: These regions exhibit slow growth attributed to lower awareness and limited healthcare infrastructure focused on POC CT imaging systems.

LATEST TRENDS

Download Free sample to learn more about this report.

Incorporation of Artificial Intelligence to Improve Efficiency of Diagnosis to Fuel the Market

The point of care CT imaging market potential is getting enhanced as a result of the advancements in artificial intelligence (AI) in healthcare, leading to improved efficiency of radiologists and subsequent diagnosis of disease indications. These have been attributed to the increased focus on patient satisfaction. For example, in July 2019, Siemens received CE approvals for their AI-Rad Companion Chest CT intelligence software. Such innovations are a key trend witnessed among leading players in the healthcare industry.

DRIVING FACTORS

Increasing Emergency Case Visits in Healthcare Facilities to Aid Market Growth

POC CT systems have proved to be crucial in the emergency department of healthcare facilities owing to an increased need for higher efficiency and accuracy in the detection of critical illnesses and in the treatment of complex injuries. According to the Center for Disease Control and Prevention (CDC), there were around 139.0 million emergency department visits in the U.S in 2018, out of which 2.0 million were admitted to critical care units. Healthcare management has progressed speedily owing to the advancements in new-age medical technologies. Health records, diagnoses, and treatments have all been made easier and more convenient in clinics, hospitals, and other outpatient centers. Modern medical technologies have become the cornerstone for breakthroughs in the diagnosis and treatment of diseases. The emergency department (ED) serves as the first line of aid in any health crisis or trauma situations.

The rising number of trauma cases in hospital emergency rooms is estimated to bolster the demand for POC CT imaging equipment. For instance, unintentional traumatic injuries are the fourth leading cause of death in the US, surpassed only by heart disease, cancer, and lower respiratory diseases.

Drift towards Outpatient Services to Propel Market Growth

Worldwide, there is an increasing preference for outpatient services owing to the lower cost of care. Additionally, the development of new advanced treatment methods and technological innovations in medical imaging equipment combined with active government initiatives has caused this drift from inpatient services to outpatient care. The rising demand for outpatient care is estimated to drive the point of care CT imaging systems market in the coming years. For example, the demand for outpatient care in the UK grew at a higher rate than the population of the country. According to the Royal College of Physicians, outpatient appointments accounted for around 85% of the hospital visits in the UK in 2018.

RESTRAINING FACTORS

Limited Availability of Trained Radiographers to Constrain the Market

Trained and skilled radiographers are crucial for performing CT scans and handling other imaging equipment. However, the increasing shortage of radiographers in developed and developing nations poses a challenge for the growth of the market in the coming years.

In countries such as the UK and the US, there is currently a massive shortage of trained radiographers, making it difficult for healthcare facilities to cope up with the increasing demand for imaging services. For instance, the American Society of Radiologic Technologists (ASRT) stated that the radiographer vacancy rate increased to 8.5% in 2019 from the previous survey that recorded a vacancy of 4.3% in 2017. The same trend was witnessed in the UAE, where, in 2016, there were less than 300 radiologists in the Emirate of Abu Dhabi. According to the estimates by the Department of Health, Abu Dhabi (2016), there would be an additional 410 full-time radiology workforce requirement by the end of 2025.

SEGMENTATION

By Product Type Analysis

To know how our report can help streamline your business, Speak to Analyst

Full-sized POC CT Imaging Systems Segment Held Highest Market Share in 2024

On the basis of product type, the market is bifurcated into full-sized and compact. The full-sized product type segment led the market accounting for 80.52% market share in 2026. Full-sized CT imaging systems are widely adopted in larger healthcare facilities such as public and private hospitals.

However, the compact segment is expected to grow at a notable CAGR during the forecast period due to the increasing number of market players engaged in the development of advanced portable CT imaging equipment. Also, recent product launches of compact CT imaging systems are expected to drive the segment’s growth in the upcoming years. In July 2017, for instance, Samsung NeuroLogica, the healthcare subsidiary of Samsung Electronics, launched a portable full-body computed tomography imaging system.

By Application Analysis

Hospitals Segment Dominated the Market in 2024

The point of care CT imaging systems market by application is categorized into hospitals, ambulatory surgical centers, radiology centers, and clinics. The hospital segment dominated the market accounting for 58.68% market share in 2026. Improving public healthcare infrastructure in developing countries is the predominant driving factor for this segment. For instance, in 2019, Shaikh Shakhbout Medical City was inaugurated in Abu Dhabi. The medical facility started accepting outpatients in the ENT, neurology, ophthalmology, cardiology, and gastrointestinal clinics.

REGIONAL INSIGHTS

North America

North America Point of Care (POC) CT Imaging Systems Market Size, 2025 (USD Million)

To get more information on the regional analysis of this market, Download Free sample

North America contributed 47.48% to the global market in 2025, with a valuation of USD 284.4 million, and is projected to reach USD 346.79 million in 2026. Increased preference of key players to introduce products in the developed countries of North America is a key factor driving the growth of the market in the region. These players are focused on securing approvals from the U.S Food and Drug Administration (FDA) to expand their customer base in other regions. For instance, in October 2020, Siemens received FDA approval for the SOMATOM On.site point of care computed tomography system. The U.S. market is projected to reach USD 321.08 million by 2026.

Europe

Europe accounted for USD 224.03 million in 2025, representing 37.40% of the global market share, and is projected to reach USD 268.63 million in 2026. Similarly, Europe is highly receptive towards advanced therapy options for untreatable diseases. There is an increase in the demand for outpatient services in countries such as Germany, France, and the UK. The recent medical reimbursements to ambulatory surgical centers are one of the predominant reasons for the growth of the regional market. The UK market is projected to reach USD 39.82 million by 2026, while the Germany market is projected to reach USD 84.92 million by 2026.

Asia Pacific

The Asia Pacific market was valued at USD 68.35 million in 2025, capturing 11.41% of global revenue, and is estimated to reach USD 81.04 million in 2026. The COVID-19 pandemic that originated from China is estimated to create a shift in the global geopolitical situation, impacting market growth in the region. Furthermore, the OEMs in China that supply parts for the manufacturing of POC CT equipment have faced significant disruptions in the manufacturing and supply chains owing to the pandemic. These developments are expected to have adverse impacts on the global market. The Japan market is projected to reach USD 35.24 million by 2026, the China market is projected to reach USD 8.86 million by 2026, and the India market is projected to reach USD 6.27 million by 2026.

Latin America and the Middle East & Africa

Latin America and the Middle East & Africa POC CT imaging systems market is estimated to grow at a slow rate in the coming years. This is attributed to the lower awareness regarding point of care imaging systems in these regions. The market in Middle East & Africa reached USD 7.54 million in 2025, representing 1.26% of total market revenue, and is projected to reach USD 8.35 million in 2026. In 2025, the Latin America market stood at USD 14.65 million, representing 2.45% of global demand, and is projected to grow to USD 16.8 million in 2026.

KEY INDUSTRY PLAYERS

Small Number of Companies to Dominate Market Competition

The market is consolidated with a few players such as Xoran Technologies, Carestream Health, Genoray Co, and Samsung NeuroLogica, among others, dominating its competitive landscape. Other leading players include SCANCO Medical, Curve Beam, Planmed Oy, and KaVo Kerr, among others. Merger & acquisition activities, launch of new products, and participation in radiology and imaging conferences are some of the key trends followed by the major market players to capture a larger customer base globally.

LIST OF KEY PLAYERS PROFILED:

- Carestream Health (U.S)

- Planmed Oy (Finland)

- Samsung NeuroLogica (U.S)

- SCANCO Medical (Switzerland)

- CurveBeam (U.S)

- KaVo Kerr (U.S)

- Genoray Co (South Korea)

- Xoran Technologies (U.S)

KEY INDUSTRY DEVELOPMENTS:

- March 2021 – NeuroLogica Corp. announced that they have started the commercial sale of SmartMSU with OmniTom Elite CT scanner. This device advances the technology available for stroke imaging on an ambulance and the OmniTom Elite multi-slice computer tomography gives high resolution image quality.

- May 2021- SCHILLER India, announced that they have installed OmniTom, a portable head and neck CT scanner in All India of Medical Sciences, Patna (India). This device is the first ever OmniTom to be installed in Asia. The device is a point of care 16-slice CT scanner with 360 degree movement

- August 2020: Philips completed the acquisition of Carestream Health’s Healthcare Information Systems business in 26 of the 38 countries Carestream operates in. Carestream HCIS’s cloud-enabled enterprise imaging platform will expand Philips’ current enterprise diagnostic informatics solutions portfolio.

- August 2020: Siemens Healthineers announced the FDA approval of SOMATOM On.site mobile head computed tomography scanner for critically ill patients admitted in intensive care units.

REPORT COVERAGE

The point of care CT imaging systems market research report provides a detailed analysis of the market and focuses on key aspects such as leading companies, product types, and leading applications of the product. Besides this, the report offers insights into market trends and highlights key industry developments. In addition to the aforementioned factors, the report encompasses several factors that have contributed to the growth of the advanced market over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD million) |

|

Segmentation |

By Product Type

|

|

By Application

|

|

|

By Geography

|

Frequently Asked Questions

According to Fortune Business Insights, the global point of care (POC) CT imaging systems market was valued at USD 598.97 million in 2025 and is projected to reach USD 3247.05 million by 2034.

The market is driven by rising emergency department visits, growing adoption of outpatient care, technological advancements like portable and AI-powered CT systems, and an increasing preference for faster, on-site diagnostic imaging.

The market will exhibit a stunning growth of 20.68% in the forecast period (2026-2034).

The full-sized CT imaging systems segment currently holds the largest market share, mainly due to high usage in hospitals. However, compact and portable CT systems are expected to grow rapidly in the coming years.

Key trends include the integration of artificial intelligence (AI) to improve diagnostic accuracy, development of mobile CT scanners for use in ambulances and ICUs, and a shift toward outpatient and decentralized care.

Xoran Technologies, Carestream Health, Genoray, and Samsung NeuroLogica are the major players in the global market.

North America dominated the market in terms of share in 2026.

Outpatient care is a significant growth driver due to cost efficiency, faster patient turnover, and the availability of portable imaging systems. This shift is especially strong in the UK and North America where outpatient appointments make up the majority of hospital visits.

- 2021-2034

- 2025

- 2021-2024

- 130

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us