Polylactic Acid Market Size, Share & Industry Analysis, By Application (Packaging, Textiles, Consumer Goods, Agriculture & Horticulture, and Others), and Regional Forecast, 2026-2034

Polylactic Acid Market Size Overview 2026-2034

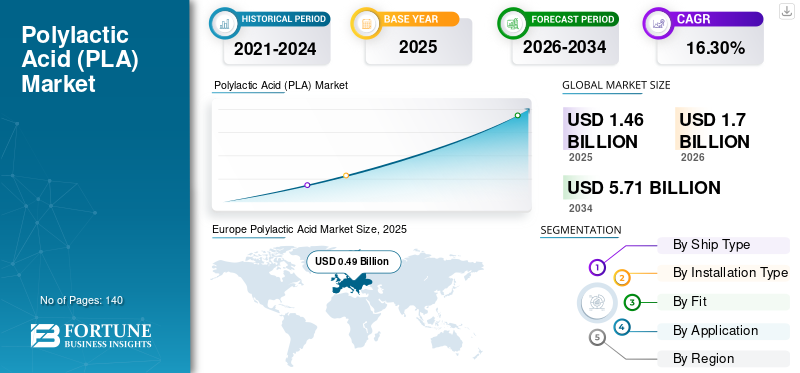

The global polylactic acid (PLA) market size was USD 1.46 billion in 2025 and is projected to grow from USD 1.70 billion in 2026 to USD 5.71 billion in 2034, exhibiting a CAGR of 16.30% during the forecast period. Europe dominated the polylactic acid market with a market share of 39.50% in 2025. Moreover, the PLA market size in the U.S. is projected to grow significantly, reaching an estimated value of USD 545.3 million by 2034. the increasing demand for ready-to-eat food and packaged food offering convenience and nutritional value, along with the change in consumer lifestyle, shall drive the market size in the United States.

Polylactic acid (PLA) material is different from the commonly available form of thermoplastic polymer materials. It is primarily derived from renewable resources such as cornstarch or sugar cane. PLA is relatively cheap and has several beneficial mechanical properties compared to other biodegradable polymers, which has made it a popular material. As of 2019, the production capacity of PLA was approximately 290 thousand tons. PLA is relatively cheap and has several beneficial mechanical properties compared to other biodegradable polymers, which has made it a popular material. As of 2019, the production capacity of PLA was approximately 290 thousand tons. PLA production heavily relies on plant feedstocks such as cassava, potato, corn, and sugar cane.

Other types of feedstock, such as agricultural by-products, cellulosic materials, or greenhouse gases (e.g., carbon dioxide and methane), have been studied and explored. However, the technique is still under development, and agricultural products look likely to remain the primary feedstock for starch blends and PLA for the foreseeable future.

The impact of COVID-19 severely disrupted the polylactic market. Various initiatives have been undertaken to deal with the pandemic such as lockdown measures, the suspension of trading practices, and the closure of multiple factories and workplaces worldwide. However, they had a range of economic consequences. Therefore, the governments in several countries began initiating regulations to get their economies back on track, which is anticipated to help increase product consumption during the forecast period.

Download Free sample to learn more about this report.

Polylactic Acid MARKET KEY TAKEAWAYS

- 2025 Market Size: USD 1.46 billion

- 2026 Market Size: USD 1.70 billion

- 2034 Forecast Market Size: USD 5.71 billion

- CAGR: 16.30% from 2026–2034

- Europe dominated the polylactic acid market with a market share of 39.50% in 2025.

- Packaging segment led the market with a 56.07% share in 2026.

- Consumer goods segment held a smaller but steady niche share in 2023.

North American

North America recorded USD 0.25 billion in 2025 and is projected to reach USD 0.29 billion in 2026, supported by sustainable packaging demand.

Europe

Europe accounted for USD 0.5 billion in 2025 and is projected to reach USD 0.67 billion in 2026, supported by strict plastic regulations and bioplastic R&D.

Asia Pacific

Asia Pacific generated USD 0.47 billion in 2025 and is expected to reach USD 0.56 billion in 2026, driven by packaging demand and China-led production.

U.S.

Market valued at USD 0.238 billion by 2026, driven by rising demand for ready-to-eat and organic food packaging.

Japan

Market supported by increasing adoption of sustainable packaging materials and food safety regulations.

Read More

Polylactic Acid Market Trends

Decline in Usage of the Fossil Fuels to Drive Demand

Polylactic acid has the potential advantage of reducing reliance on fossil-based emissions. There is a need to reduce reliance on fossil fuels and move towards green carbon to progress towards a circular economy. PLAs provide an environmental advantage over their carbon-based counterparts such as decreased CO2 footprint, reduced fossil resource reliance, and increased use of renewable resources during the manufacturing process. Europe witnessed a growth from USD 0.37 million in 2022 to USD 0.43 million in 2023.

For instance, 0.5 kg CO2 eq/kg is the global warming potential (GWP) of PLA. In contrast with other typical fossil-based polymers such as PS, PET, PP, and PE, this is a ~75 percent drop in carbon footprint.

Download Free sample to learn more about this report.

Polylactic Acid Market Growth Factors

Increasing Demand from Packaging Industry to Drive the Market

For polylactic acid, the packaging is the main application. In 2019, packaging accounted for 59% of biodegradable plastics produced, according to the European Bioplastics. A fraction (0.5 percent) of the overall plastic packaging produced in biodegradable packaging. Almost 500,000 tons of biodegradable plastics are used in flexible packaging. In the consumer packaged goods, supermarkets, and foodservice markets, major multinationals have either made strides or announced plans to ramp up the use of biodegradable plastic significantly. This further drives the need for PLA packaging for fresh fruit, food cutlery, and compostable bags.

In addition, Polylactic acid (PLA) is experiencing a surge in demand within the packaging industry due to its eco-friendly properties. Derived from renewable resources such as corn starch or sugarcane, PLA offers biodegradability and compostability, making it an attractive alternative to traditional petroleum-based plastics. With increasing consumer awareness and regulatory pressures to reduce plastic waste, businesses are turning to PLA for sustainable packaging solutions. Its versatility allows for various applications, including food packaging, disposable cutlery, and bottles. Moreover, advancements in PLA production technologies have improved its performance characteristics, such as heat resistance and barrier properties, further expanding its usage in the packaging industry.

Greenpeace East Asia Magazine in its December 2020 edition mentioned that 164,000 tonnes of biodegradable food & beverage packaging and foodstuffs were processed in 2017. By 2022, this figure is projected to grow by about 10 percent.

PLA bioplastics offer several features that help reduce plastic use while enhancing the use of green plastics. PLA has excellent barrier properties making it very suitable for fresh fruits and vegetable packaging. Moreover, it has high stiffness and strength, which allows for a thin wall part design.

Green packaging provides various benefits such as reduced reliability on fossils fuels, lower utilization of natural resources, increased use of recyclable products, more energy-efficient manufacturing methods, and renewable sources. Recent trends and technological solutions are available in sustainable packaging that includes edible packaging, shrinking carbon footprint, and waste reduction. Furthermore, it is economically appealing to both manufacturers and consumers. Thus, the growing demand for sustainable packaging is anticipated to fuel the demand for the polylactic acid market during the forecast period.

RESTRAINING FACTORS

Concerns over Cost & Agricultural Feedstock to Hamper Market Growth

Compared to traditional plastics, the cost of processing polylactic acid is high. With the falling price of fuel oil, synthetic plastics have become cheaper, leading to a bigger price gap. Several technological hurdles exist to manufacture cheaper biodegradable plastics. Approximately one-third of biodegradable plastics are derived from petrochemicals, and the industry is moving towards feedstock that is bio-based.

The current bio-based feedstock is primarily agricultural products such as maize, cassava, and potato. Using agricultural goods, specifically food crops, on a broad industrial scale could potentially lead to problems such as whether industrial usage competes with the region's food supply.

Polylactic Acid Market Segmentation Analysis

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Packaging Segment to Lead Market

Based on the application, the market is segmented into packaging, textiles, consumer goods, agriculture & horticulture, and others.

Polylactic acid is widely used in the packaging industry. Companies have raised their appetite for food packaging and single-use plastic and have found biodegradable substitutes for food packaging and single-use cutlery. with a expected share of 56.07% in 2026. Moreover, a move to biodegradable packaging has also been promoted by many e-commerce giants, driving the biodegradable market for online merchandise and food distribution. In China alone, more than 700,000 tons would be added to the demand for biodegradable plastics if online industries met the policy requirement by switching 50 percent of their online delivery packaging and 20 percent of food delivery packaging to biodegradable products.

- The consumer goods segment is expected to hold a 8.9% share in 2023.

Furthermore, by 2025, the January 2020 policy prohibits the use of non-degradable plastics in online delivery. Unless businesses develop ambitious plastic reduction plans and switch from conventional plastics to biodegradable plastics, China's online distribution industry will produce an estimated 5,000 tons of biodegradable plastic waste annually by 2025.

REGIONAL INSIGHTS

Europe Polylactic Acid Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

Europe

In 2025, Europe represented USD 0.5 billion, accounting for 39.50% of the worldwide market, and is projected to grow to USD 0.67 billion in 2026. The region is expected to dominate the market during the forecast period. This is attributable to the stringent government policies on using plastic, increasing R&D supporting the use and development of bioplastic, and consumer spending. Also, the growing agricultural industry is likely to drive the market. The increasing demand for natural ingredients and organic food in the region is supporting the market growth. The UK market is valued at USD 0.055 billion by 2026, while the Germany market is valued at USD 0.155 billion by 2026.

The growing demand for exotic fruits and vegetables has been a major factor driving the market in Europe. Germany is the most consuming country of polylactic acid in the region due to high economic growth and the luxurious lifestyle of consumers preferring fine quality food products. This is expected to boost the demand for good quality packaging applications.

North America

North America recorded a market size of USD 0.25 billion in 2025, capturing 17.20% of the global market share, and is projected to reach USD 0.29 billion in 2026. The increasing demand for ready-to-eat food and packaged food offering convenience and nutritional value, along with the change in consumer lifestyle, shall drive the market in North America. In the U.S., consumers are inclined to consume organic food due to the growing focus on leading a healthy lifestyle. In U.S., the consumer goods segment is estimated to hold a 8.8% market share in 2023. The U.S. market is valued at USD 0.238 billion by 2026.

To know how our report can help streamline your business, Speak to Analyst

Asia Pacific

The Asia Pacific market generated USD 0.47 billion in 2025, representing 32.30% of the global market landscape, and is expected to reach USD 0.56 billion in 2026. In terms of country, China is the key market in Asia Pacific owing to the increasing food demand from the growing population. This demand is being fulfilled by convenience food easily available at a cheaper cost. China is the major producer of packaging materials worldwide, which increases the production and consumption of food packaging in the country. The Japan market is valued at USD 0.074 billion by 2026, the China market is valued at USD 0.222 billion by 2026, and the India market is valued at USD 0.123 billion by 2026.

Latin America

In 2025, Latin America held 8.60% of the global market, reaching a valuation of USD 0.13 billion, and is projected to grow to USD 0.15 billion in 2026. It is predicted that Latin America will show substantial growth by the end of the forecast period. The growth is supported by a rise in the per capita intake of food & beverage packaging in countries such as Brazil, Argentina, and the Caribbean region.

Middle East & Africa

Middle East & Africa accounted for USD 0.04 billion in 2025, representing 2.50% of the global market share, and is projected to reach USD 0.04 billion in 2026. Demand for green packaging in the Middle East & Africa is growing because of the rise in demand for canned goods due to the simplicity of use and longer shelf life. Besides, demand for packaging products will be increased by local brands which supply different types of canned products.

KEY INDUSTRY PLAYERS

Strategic Planning Adopted by Companies to Strengthen their Market Positions

The market is fragmented owing to the presence of several key players at a global and regional level. Some major players are putting perpetual efforts to offer quality and advanced products by adopting novel technologies in manufacturing. In addition to this, several key players are adopting strategies such as mergers and acquisitions, developing and modifying infrastructure, expanding their manufacturing facilities across cities, and investing in R&D facilities. These companies are also looking for opportunities to integrate vertically across the value chain.

For example, NatureWorks LLC manufactures its Ingeo PLA bioplastics from dextrose, a sugar extracted from maize starch cultivated for many industrial and practical applications.

List of Top Polylactic Acid Companies:

- NatureWorks (Minnetonka, Minnesota, United States)

- Total Corbion PLA (Gorinchem, Netherlands)

- BASF SE (Ludwigshafen, Germany)

- Sulzer (Winterthur, Switzerland)

- COFCO Biochemical

- FUTERRO S.A.

- Zhejiang Hisun Biomaterials Co., Ltd

- Nantong Jiuding Biological Engineering

- Chongqing Bofei Biochemical Products, Ltd.

- UNITIKA LTD.

KEY INDUSTRY DEVELOPMENTS:

- April 2023 – NatureWorks LLC and Jabil Inc. collaborated to provide a novel powder based on Ingeo PLA that can be used for selective laser sintering 3D printing platforms. This is a cost-effective option, compared to the incumbent PA-12.

- October 2019 – Evonik announced the launch of the world’s first bioresorbable portfolio of polylactide-polyethylene glycol (PLA-PEG) copolymers for use in implantable medical device applications.

- November 2020 – Total Corbion PLA released its whitepaper outlining its position on the preferred end-of-life options for PLA bioplastics. The whitepaper further explains the significance of PLA products and applications that can contribute to the circular economy.

REPORT COVERAGE

The global polylactic acid market research report provides a detailed analysis of the market and focuses on crucial aspects such as leading companies, products, and applications. The market includes insights into market trends and highlights vital industry developments. In addition to the factors mentioned above, the report encompasses various factors that have contributed to the growth of the market over recent years. It includes historical data & forecasts revenue growth at global, regional, and country levels, and analyzes the industry's latest market dynamics and opportunities.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Unit |

Value (USD Billion) and Volume (Tons) |

|

Growth Rate |

16.30% CAGR from 2026 to 2034 |

|

Segmentation |

By Application

|

|

By Geography

|

Frequently Asked Questions

According to Fortune Business Insights, the global polylactic acid (PLA) market size was valued at USD 1.70 Billion in 2026 and is projected to grow to USD 5.71 Billion by 2034.

Yes, polylactic acid is considered environmentally friendly. It is biodegradable, compostable, and made from renewable resources like corn starch and sugarcane. It also has a 75% lower carbon footprint compared to traditional fossil-based plastics such as PET and PP.

Registering a CAGR of 16.30%, the market will exhibit steady growth over the forecast period (2026-2034).

Europe dominated the polylactic acid market in 2025 with a value of USD 0.49 Billion, driven by strict environmental regulations, increasing bioplastic R&D, and consumer demand for sustainable packaging.

Key growth drivers include the rising demand for sustainable packaging, increasing consumer awareness, government regulations on plastic use, and technological advances in polylactic acid processing that enhance performance and cost-efficiency.

Challenges include the high production cost compared to conventional plastics, limited composting infrastructure, and concerns over agricultural feedstock use, which may compete with the global food supply.

Key companies include NatureWorks LLC, Total Corbion PLA, BASF SE, Sulzer, FUTERRO S.A., and Zhejiang Hisun Biomaterials. These players are investing in R&D, expanding production capacity, and forming strategic partnerships to strengthen their market positions.

The polylactic acid market has a promising future due to the global push for sustainable materials, government bans on single-use plastics, and the adoption of green packaging across industries. Growth is expected to be strong across North America, Europe, and Asia-Pacific, with innovation driving new applications in medical, automotive, and electronics sectors.

- 2021-2034

- 2025

- 2021-2024

- 140

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us