Polysilicon Market Size, Share & Industry Analysis, By Application (Solar Photovoltaics and Electronics), and Regional Forecast, 2026-2034

KEY MARKET INSIGHTS

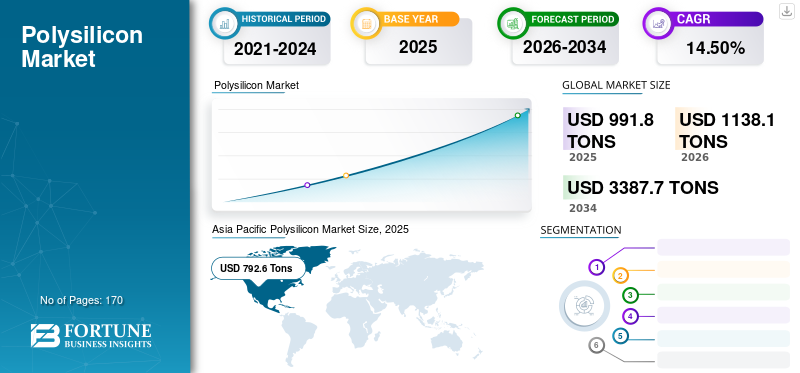

The global polysilicon market size by volume was valued at 991.8 tons in 2025 and is projected to grow from 1,138.10 tons in 2026 to 3,387.70 tons by 2034, exhibiting a CAGR of 14.50% during the forecast period. Asia Pacific dominated the polysilicon market with a market share of 80.30% in 2025. Moreover, the polysilicon market size in the U.S. is projected to grow significantly, reaching an estimated volume of 318.77 tons by 2032, driven by the strong demand from electronics industry for maniufacturing of semicondustors.

Polysilicon or polycrystalline silicon is produced from metallurgical grade silicon. It is an ultra-high pure form of silicon and consists of a number of smaller crystals. This material serves as a crucial material component in the manufacturing of solar cells along with other electronic devices. It is used in the electronics industry and typically contains impurities less than one part per billion. On the other hand, material grades created for solar photovoltaics are comparatively less pure.

The regional lockdown restrictions imposed during the COVID-19 pandemic disrupted supply chains, adversely affecting numerous end-use industries. The shortage of raw material supplies had a significant impact on the semiconductor manufacturing capacity, resulting in a shortage of silicon chips. The solar power market has shown a rising trend during the pandemic, owing to the rising adoption of solar power. However, polysilicon producers were unable to keep up with rising demand, resulting in a significant gap between demand and supply. As a result, prices for this material rose sharply in 2020 for the first time after decreasing constantly in the past few decades.

Download Free sample to learn more about this report.

Polysilicon Market Key Takeaways

- 2025 Market Size: 991.8 tons

- 2026 Market Size: 1,138.10 tons

- 2034 Forecast Market Size: 3,387.70 tons

- CAGR: 14.50% from 2026–2034

- Asia Pacific dominated the market with an 80.30% share in 2025.

- The Solar Photovoltaics segment will account for 80.33% market share in 2026.

- Electronics segment is supported by increasing semiconductor demand across industries.

North America

The market reached 137.7 tons in 2025, driven by growing solar installations and semiconductor demand.

Asia Pacific

The market reached 792.6 tons in 2025, supported by strong solar manufacturing and production capacity.

Europe

The market reached 53.4 tons in 2025, driven by renewable energy targets and expanding solar projects.

U.S.

The US market is projected to reach 149.7 tons by 2026.

Japan

The Japan market is projected to reach 25.4 tons by 2026.

Read More

Polysilicon Market Trends

Growing Digitalization in Emerging Economies to Drive Market Growth

Digitalization presents enormous growth opportunities for emerging economies to boost growth rate and be part of the global economy. Digitalization brings people closer, enables better use of resources, and speeds up development and economic growth. To tap the potential advantages of digitalization, governments and international organizations are encouraging and heavily investing in digitalization. For instance, the Government of India has been running a Digital India program since 2015 with a vision of transforming India into a digitally empowered society and knowledge economy. Digitalization helps with services available to people electronically by improving online infrastructure and increasing internet connectivity or making the country digitally empowered in the field of technology. This has resulted in increased response to digitalization, causing increased demand for consumer electronics, which also caused an increase in demand for electricity. Therefore, rising digitalization provides lucrative opportunities for the market by pushing the demand for electronics grade products.

Polysilicon Market Growth Factors

Rising Demand from Solar Photovoltaics to Drive Market Growth

Climate change is one of the most serious challenges the world is experiencing today, impacting every region on the planet. Extreme weather events such as heat waves, droughts, cyclones, and heavy rains have grown increasingly common in recent years, disrupting businesses and impacting people's lives. According to a 2021 report issued by the United Nations' Intergovernmental Panel on Climate Change (IPCC), the average global temperature has already risen by 1.1 degrees’ Celsius relative to pre-industrial temperatures in the nineteenth century. Scientists estimate that the average global temperature could increase by 1.5 degrees Celsius in the next 20 years, exceeding the 1.5-degree Celsius danger limit set in the Paris Agreement. One of the key actions that can help to avoid the catastrophic impacts of global warming is to reduce greenhouse gas emissions immediately by reducing fossil fuel consumption and transitioning to alternative renewable energy sources such as solar energy.

Leading economies, such as the U.S., China, and the European Union, have already stated their intention to achieve net zero emissions in the subsequent years, with solar power farms playing a key role in their strategy. A significant share of the polycrystalline silicon produced worldwide is consumed by the solar photovoltaic industry to manufacture solar cells and panels. Despite the global economic slowdown caused by the COVID-19 pandemic, demand for solar photovoltaic panels has grown considerably in both the residential and commercial sectors. Several countries around the globe have reported substantial increase in solar power capacities and this trend is likely to continue during the forecast period. For example, China acquired 48.2 Gigawatts of additional solar generating capacity in 2020 as part of a strategy to reduce its dependence on fossil fuels and cut carbon emissions. Rising environmental concerns are anticipated to accelerate adoption of renewable energy sources such as solar power during the forecast period. The solar photovoltaic industry is anticipated to expand significantly during the forecast period owing to the rising adoption of renewable energy sources, which, in turn, will benefit and drive the polysilicon market growth.

Download Free sample to learn more about this report.

Rising Demand for Semiconductors in Various End-use Industries to Fuel the Market Growth

Polysilicon exists in a highly pure form. Being compact, efficient and having low capacitance, it is an excellent material for semiconductors. It is relatively easy to deposit in a large area. There are minimum energy losses during charging and electricity and signal transfer. It provides superior properties, such as high thermal conductivity, large critical fields, and high voltage potential. Polysilicon semiconductor devices offer high power density and switching frequencies and enable transistors to operate at high voltage levels. Due to all these superior properties, these semiconductors are being widely used in different electronic components in several end-use industries, driving market growth.

Progressive development in the Internet of Things, Artificial Intelligence, 5G spectrum and the emergence of Cryptocurrency are some of the key factors anticipated to boost the semiconductor demand in the coming years. This will ultimately result in increased demand for high-purity polysilicon.

RESTRAINING FACTORS

Use of Capital Intensive Manufacturing Process to Restrict Market Growth

The establishment of a manufacturing facility is a capital-intensive enterprise that also requires modern technology and a highly skilled workforce. China presently dominates the market, accounting for around 80% of global production. The pandemic-caused supply chain disruptions resulted in a shortage of silicon chips, impacting all semiconductor electronic-related industries, including the automobile and consumer electronics industries, which rely on semiconductor components. After witnessing the vulnerabilities in supply chains, several countries have recognized the importance of domestic production and its geopolitical implications on their semiconductor-dependent industries.

Countries across the globe have been taking initiatives and investing in developing domestic production facilities to protect their semiconductor-dependent sectors. However, owing to the high capital required to set up manufacturing facilities, investment in these types of ventures is limited to players with deep pockets. The capital-intensive nature of the manufacturing process has been a major bottleneck and is anticipated to restrict market growth. Furthermore, competition from China's low-cost products adds uncertainty to the business, limiting investments and development of manufacturing in other regions.

Polysilicon Market Segmentation Analysis

By Application Analysis

To know how our report can help streamline your business, Speak to Analyst

Rising Adoption of Renewable Energy to Create New Market Opportunities

Based on application, the market is segmented as solar photovoltaics and electronics.

The Solar Photovoltaics segment will account for 80.33% market share in 2026. The solar photovoltaics segment dominated the market due to the wide use of material in the manufacture of solar photovoltaic panels and semiconductors. The growth of this segment is primarily attributed to the growing demand for solar PV systems installation across the world, which, in turn, surges the demand. The solar photovoltaic sector is one of the fastest growing industries worldwide. According to the International Energy Agency (IEA), the industry accounts for almost two-thirds of net energy capacity across the world.

In addition, a solar photovoltaic plant used to power mini grids is a brilliant way to produce electricity available to people who do not have access to power transmission lines, mainly in emerging countries with excellent solar energy resources. Increasing growth of the market due to significant demand from specific end-use sectors, including growth in solar cell installations, increasing investment and incentives for solar photovoltaics installations, and growth in semiconductor sales will drive the development of the market.

REGIONAL INSIGHTS

Asia Pacific Polysilicon Market Size, 2025 (Tons)

To get more information on the regional analysis of this market, Download Free sample

Asia Pacific

In 2025, Asia Pacific generated USD 792.6 Tons, contributing 80.30% to global market revenue, and is projected to grow to USD 914.1 Tons in 2026. China dominated the global market in terms of manufacturing and export due to its well-established silicon sector and the availability of low-cost labor and coal. In 2020, China acquired 48.2 Gigawatts of additional solar power capacity, as part of a strategy to reduce reliance on fossil fuels and lower its carbon emissions. Polycrystalline silicon manufacturers, most of them based in China, are struggling to meet the increased demand from the photovoltaic industry. Prices for the material have risen by 40% due to a supply shortage and are expected to remain high for the next few years, although new manufacturing facilities are under development, it will take time to catch up with rising demand. High costs have impacted the solar industry, forcing manufacturers to reduce their photovoltaic module manufacturing capacity. Other countries in the region have begun to invest in domestic production facilities to safeguard their expanding photovoltaic and electronic sectors against potential shortages. For example, the Indian public sector companies such as NTPC and BHEL have announced intentions to construct a polycrystalline silicon production facility with a capacity of roughly 10 Gigawatts to reduce their dependence on China. The solar photovoltaic industry is anticipated to expand as several countries in the region are likely to adopt renewable sources such as solar energy to meet their energy needs. Polycrystalline silicon is a key component in the manufacture of solar photovoltaic modules and is expected to witness a surge in demand, driving the market expansion in the South East Asia Pacific region. The Japan market is projected to reach 25.4 tons by 2026, the China market is projected to reach 793.4 tons by 2026, and the India market is projected to reach 12.6 tons by 2026.

To know how our report can help streamline your business, Speak to Analyst

North America

The North America region captured 13.70% of the global market in 2025, generating USD 137.7 Tons in revenue, and is projected to reach USD 156.4 Tons in 2026. The North America polysilicon market share is anticipated to expand attributed to the rising demand from the solar photovoltaic industry. Residential and business solar installations in the U.S. have increased significantly in recent years as a result of rising affordability, government incentives, and commitment to reduce carbon emissions. According to a study published by the Solar Energy Industries Association and Wood Mackenzie, despite the economic slowdown caused by COVID-19, the U.S. solar industry installed a record 19.2 Gigawatts of new capacity in 2020, a 43% increase over the previous year. The study also projects that solar installations will quadruple compared to current levels by 2030. The solar power industry in the region is anticipated to expand during the forecast period, which will benefit and drive the expansion of the market. The US market is projected to reach 149.7 tons by 2026.

Europe

Europe maintained a strong presence in the global market, reaching USD 53.4 Tons in 2025, accounting for 5.20% share, and is expected to reach USD 58.7 Tons in 2026. The European Commission has established legally binding targets to reduce net carbon emissions by 55% by 2030 compared to 1990 levels and to eliminate them entirely by 2050. One of the European Union's initiatives to achieve these goals is to expand the use of renewable energy, with the aim of increasing the percentage of renewable energy to 40% of total consumption by 2030. According to a report published by SolarPower Europe, the region's solar industry expanded by 11% in 2020, providing an extra 18.7 Gigawatts of energy generation capacity through solar photovoltaic modules. Recent volatility in polycrystalline silicon prices and allegations of forced labor and human rights violations in Chinese production facilities are anticipated to cause a short-term delay in solar installation projects in Europe. However, the European Union is expected to take essential actions in the long run such as developing domestic production facilities to strengthen its solar power industry. Rising demand from the region's solar industry and the EU's strong commitment to the transition to renewable energy are anticipated to drive market expansion. The UK market is projected to reach 6.5 tons by 2026, while the Germany market is projected to reach 16 tons by 2026.

Rest of the World

Rest of the World recorded a market size of USD 8.1 Tons in 2025, capturing 0.8% of the global market share, and is projected to reach 8.9 Tons in 2026.

Government initiatives to encourage green energy and the high availability of land are likely to boost the growth of utility-scale solar farms in countries such as Brazil and Mexico during the forecast period, driving market expansion. Many oil-producing countries, including Saudi Arabia, Iran, Iraq, and Kuwait, have previously stated their ambition to diversify their energy portfolio by incorporating renewable energy sources such as solar power. Several massive solar projects in the pipeline, all of which are likely to benefit and expand the market in the Middle East & Africa.

List of Key Companies in Polysilicon Market

Strategic Planning Adopted by Companies to Strengthen their Market Share

A few major polysilicon players primarily dominate the market. The existing players have developed proprietary products and they maintain a competitive edge over other players owing to their unique product offerings. Furthermore, the companies are continuously conducting R&D activities to develop better solutions to match the changing needs of the electronic industry.

The major companies operating in this market include Wacker Chemie AG, Xinte Energy Co., Ltd., OCI Company Limited, Hemlock Semiconductor Corporation, and REC Silicon ASA, among other players. Plant expansions and development of new manufacturing facilities characterize the global market. Several other companies, such as Daqo New Energy Corp., GCL Technology Holdings Co., Ltd., Mitsubishi Materials Corporation, Qatar Solar Technologies, Tokuyama Corporation, are among other active participants in the market.

LIST OF KEY COMPANIES PROFILED:

- Daqo New Energy Corp. (China)

- GCL Technology Holdings Co., Ltd. (China)

- Hemlock Semiconductor Corporation (U.S.)

- Mitsubishi Materials Corporation (Japan)

- OCI Company Limited (South Korea)

- Qatar Solar Technologies (Qatar)

- REC Silicon ASA (Norway)

- Tokuyama Corporation (Japan)

- Wacker Chemie AG (Germany)

- Xinte Energy Co., Ltd. (China)

KEY INDUSTRY DEVELOPMENTS:

- August 2022: REC Silicon announced that it has entered into a Memorandum of Understanding with Mississippi Silicon, committing the companies to negotiate a raw material supply agreement and help establish a low-carbon and fully traceable U.S.-based solar supply chain. The move will help the company support the development of an end-to-end U.S. solar supply chain from raw silicon to polysilicon and, finally, fully assembled modules.

- April 2022: OCI signed a memorandum of understanding to supply polysilicon to South Korean solar manufacturer Hanwha Solutions. The supply contract has a value of approximately USD 1.2 billion.

- February 2021: GCL Technology Holdings Limited finalized deals with Tianjin Zhonghuan Semiconductor and LONGi Green Energy Technology. As a part of the deal, GCL will supply its polysilicon to both Chinese companies on a long-term basis.

REPORT COVERAGE

The research report provides qualitative and quantitative insights on the market share, size, growth rate, and trend analysis by different segments. Along with this, the research report provides an elaborative analysis of the market dynamics and competitive landscape. Various key insights presented in this market analysis report are PORTER’s five forces, recent industry developments, regulatory scenarios, and key industry trends. The report also highlights the competitive landscape between key players operating in this market.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 14.50% from 2026 to 2034 |

|

Unit |

Volume (Tons) |

|

Segmentation |

By Application

|

|

By Region

|

Frequently Asked Questions

According to Fortune Business Insights, the global polysilicon market size by volume was 991.8 tons in 2025 and is projected to grow from 1,138.10 tons in 2026 to 3,387.70 tons by 2034, exhibiting a CAGR of 14.5% during the forecast period.

The market is driven by rising demand from solar photovoltaic (PV) systems, increased adoption of renewable energy, and growing use of semiconductors in electronics, electric vehicles, and communication technologies like 5G and AI.

Registering a CAGR of 14.50%, the market will exhibit steady growth during the forecast period (2026-2034).

Asia Pacific dominates the global polysilicon market, accounting for 80.30% of the total volume in 2025. China leads the region due to its strong manufacturing infrastructure, low-cost labor, and high demand for solar power installations.

Polysilicon is primarily used in solar photovoltaic panels and semiconductors. Solar-grade polysilicon powers solar energy systems, while electronics-grade polysilicon is used in microchips, transistors, and integrated circuits.

Rapid digitalization in emerging economies is increasing demand for consumer electronics and internet infrastructure, which in turn boosts the demand for high-purity polysilicon used in semiconductor devices.

The market faces challenges such as capital-intensive manufacturing, supply chain disruptions, and geopolitical dependency on China for over 80% of global polysilicon production, limiting diversification and investment in other regions.

Yes, the solar sector is a major driver of polysilicon demand. Countries transitioning to net-zero emissions are investing heavily in solar energy, and polysilicon is a critical raw material for solar cell and panel production.

Key players include Daqo New Energy (China), Wacker Chemie AG (Germany), OCI Company (South Korea), Hemlock Semiconductor (U.S.), and REC Silicon (Norway). These companies focus on capacity expansion, R&D, and strategic partnerships to strengthen their market presence.

- 2021-2034

- 2025

- 2021-2024

- 170

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us