Port Construction Market Size, Share & Industry Analysis, By Port Type (Sea Port, Inland Port, and Other Types), By Construction Mode (Old Port Upgrade and New Port Construct), By Terminal Type (Intermodal and Container Terminals, Break Bulk Terminals, Dry Bulk Terminals, and Others), and Regional Forecast, 2026-2034

(Offer valid till 15th Aug 2026)

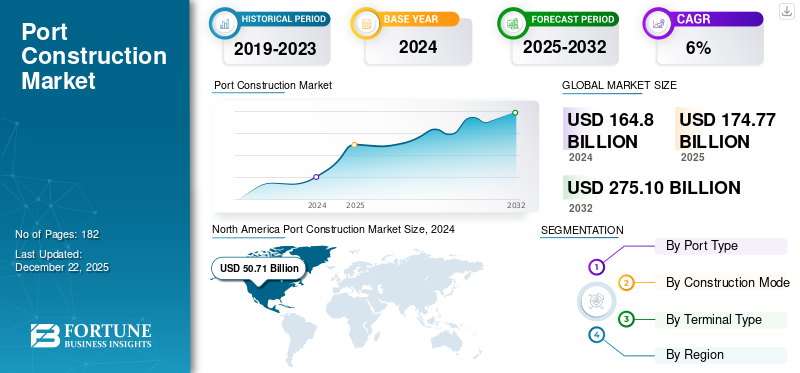

Port Construction Market Size and Future Outlook

The global port construction market size was valued at USD 174.77 billion in 2025 and is projected to grow from USD 185.71 billion in 2026 to USD 311.97 billion by 2034, exhibiting a CAGR of 6.70% during the forecast period. North America dominated the global market with a share of 30.44% in 2025.

The port construction industry focuses on the design, development, and maintenance of port facilities, which are critical for maritime trade and transportation. This sector encompasses a range of activities, including the construction of docks, terminals, cargo handling facilities, and related infrastructure such as roads and rail connections. The market is influenced by global trade trends, increasing shipping volumes, and the need for modernized infrastructure to accommodate larger vessels and efficiently manage cargo flow. As international trade continues to expand, there is a growing emphasis on enhancing port capabilities, driving increased investments in construction projects. Market growth is driven by the rising demand for infrastructure to support energy transition projects and offshore development, including renewable energy installations and liquefied natural gas (LNG) facilities. Additionally, environmental considerations and sustainability are becoming integral to port development, requiring innovative engineering solutions to meet contemporary demands while adapting to future challenges.

Globally, port construction involves constructing structures adjacent to water bodies, including oceans, rivers, ports, and harbors. This encompasses the building of piers, wharves, and seawalls, which are utilized for loading and unloading cargo and passengers from vessels.

The global market is saturated with several global and regional players operating in this industry. Leading companies dominate due to their extensive project experience and strong regional presence. Other companies also leverage market trends. CSCEC is a global leader in construction and engineering services, and its port construction capabilities are robust, spanning terminal expansion, dredging, and maritime infrastructure.

Download Free sample to learn more about this report.

Port Construction Market Key Takeaways

- 2025 Market Size: USD 174.77 billion

- 2026 Market Size: USD 185.71 billion

- 2034 Forecast Market Size: USD 311.97 billion

- CAGR: 6.70% (2026–2034)

- North America dominated the global market with a share of 30.44% in 2025.

- The sea port segment is expected to dominate the market with the largest market share of 64.53% in 2026.

- The old port upgrade segment is projected to dominate the market share of 63.09% in 2026.

North America

The region generated USD 53.2 billion in 2025 and is projected to reach USD 55.95 billion in 2026, supported by port modernization, automation, and rising e-commerce-driven cargo volumes.

Europe

The market was valued at USD 42.83 billion in 2025 and is expected to reach USD 45.69 billion in 2026, driven by investments in port upgrades, intermodal connectivity, and sustainable infrastructure.

Asia Pacific

The region accounted for USD 47.31 billion in 2025 and is projected to reach USD 50.88 billion in 2026, fueled by rapid trade growth, expanding container terminals, and infrastructure investments across major economies.

U.S.

The market is projected to reach USD 36.54 billion in 2026, supported by ongoing investments in port expansion, cargo handling technologies, and digitalized port operations.

Japan

The market is expected to benefit from continued investments in port modernization, automation, and logistics infrastructure to strengthen trade efficiency and support regional maritime connectivity.

Read More

Market Dynamics

Market Drivers

Ongoing Expansion of International Trade Supports Market Growth

The ongoing expansion of global trade acts is a key factor in investments in port construction and infrastructure. As economies become increasingly interconnected, the need for sophisticated and efficient port facilities continues to rise, enabling the seamless transport of goods via sea routes. Port disruptions can result in considerable delays and financial losses, as demonstrated during the COVID-19 pandemic, which revealed the essential requirement for strong port infrastructure. Government policies aimed at advancing port infrastructure play a crucial role in enhancing trade efficiency and economic growth. This is expected to boost the port construction market growth in the coming years.

Strategic improvement in port facilities can help reduce logistical hurdles and lower transportation expenses, making nations with advanced ports more appealing to foreign direct investment. As worldwide trade expands, investing in upgraded port infrastructure becomes more vital to support economic development and facilitate smooth global trade. According to research from NYU Stern, around 80% of international trade is carried out by ships, with nearly 11 billion tons of cargo and goods worth USD 20 trillion passing through ports each year.

- December 2023 - The Maritime Administration declared that the PIDP will keep offering discretionary grants for projects focused on enhancing the safety, efficiency, and reliability of cargo transport within ports. This initiative aids both urban and rural ports. It includes financing for planning and capital initiatives, guaranteeing that port infrastructure can accommodate the expected rise in freight volumes crucial for global trade.

Market Restraints

Significant Upfront Expenditure to Restrain Market Development

The considerable financial commitment required for building and sustaining ports poses a notable obstacle for governments and private investors, especially in regions with constrained budgets. Constructing a contemporary port entails significant expenses, ranging from millions to billions of dollars, based on the size and intricacy of the project. These significant expenses extend beyond the building of docks and terminals to include dredging, breakwaters, and sophisticated cargo handling systems.

The rising expenses of labor and materials make financing efforts more challenging. To address these challenges, long-term financing solutions are essential, particularly through public-private partnerships (PPPs), which help distribute financial risks and obligations. Although there is potential for significant trade and economic benefits, numerous regions find it difficult to obtain the required funding due to competing budgetary priorities and economic limitations. This issue is especially severe for smaller or inland ports that might not have access to federal funding or private investment opportunities. As global trade continues to grow, the need for better port construction is rising. Yet, substantial initial investment costs remain a major obstacle that needs to be tackled to support future development and modernization.

Market Opportunities

Surging Investments by the Government Authorities to Fuel Market Growth

Numerous governments acknowledge the vital role of ports in economic growth and are implementing strategic initiatives to fund port development and improvements. For example, the Indian government has initiated the Sagarmala Programme, aimed at improving port infrastructure and encouraging port-driven economic growth. This initiative encompasses more than 234 projects with a combined investment of approximately USD 35 billion, aimed at upgrading current ports and creating new ones to enhance operational efficiency and capacity. The initiative aims to utilize India's vast coastline and usable waterways to strengthen trade routes and support the manufacturing industry under the 'Make in India' framework.

In the U.S., the Maritime Administration oversees the Port Infrastructure Development Program (PIDP), which provides discretionary grants to enhance port facilities. This initiative backs projects aimed at improving safety, efficiency, and reliability in freight transportation, guaranteeing that ports can handle expected increasing cargo quantities. The PIDP focuses on providing funding for urban and rural ports, with a specific allocation for smaller ports to enhance their capabilities.

- The Indian government has outlined an ambitious National Perspective Plan, proposing an investment of USD 10.51 billion to enhance port development. This strategy intends to improve port facilities and connections, concentrating on upgrading associated infrastructure such as roads and railways. Additionally, the government's policy allowing 100% Foreign Direct Investment (FDI) through the automatic route for port construction and maintenance projects is anticipated to boost further growth in this industry.

- The Irish Government revealed a USD 102 million funding initiative to expand the Port of Cork and improve its facilities to cater to the needs of the expanding offshore renewable energy industry. This investment is part of a wider commitment toward strategic infrastructure development, encompassing substantial financing for transportation services and renewable energy initiatives.

Market Challenges

Lack of Skilled Workforce May Hamper Market Development

The port industry often faces challenges, such as inefficiencies and strikes, primarily due to a lack of skilled workers. With the rise in global trade, the need for effective cargo management and fast turnaround times intensifies, making the availability of skilled workers essential. Moreover, numerous ports face difficulties in attracting and keeping skilled workers, resulting in operational delays and heightened expenses. Labor shortages may lead to increased wait times for ships, decreased efficiency at the docks, and challenges in maintaining shipping timetables, ultimately disrupting the entire supply chain.

Port Construction Market Trends

Integration of Advanced Technologies in Construction Activities is a Latest Market Trend

The incorporation of cutting-edge technologies such as automation, artificial intelligence (AI), and the Internet of Things (IoT) is transforming port operations, enhancing both efficiency and sustainability. As ports transform into "smart ports" equipped with advanced digital systems, they gain greater operational visibility and greatly decrease vessel turnaround times. For example, AI-powered systems enhance vessel management by examining extensive datasets in real time to forecast demand, improve workflows, and prevent minor bottlenecks from developing into significant problems. Additionally, automation technologies are transforming cargo handling operations.

Automated cranes and robotic systems are being utilized more frequently to load and unload containers with little human involvement, lowering labor expenses, minimizing human errors, and accelerating operations. The IoT is essential for linking different devices in the port ecosystem, enabling real-time tracking of equipment and cargo flows. This interconnectivity promotes improved decision-making and resource allocation, resulting in increased operational efficiency.

Download Free sample to learn more about this report.

Segmentation Analysis

By Port Type

Sea Port Holds the Largest Market Share Due to Rise in Maritime Commerce Activities

On the basis of port type, the market is segmented into sea port, inland port, other types.

The sea port segment is expected to dominate the market with the largest market share of 64.53% in 2026. Sea ports serve as vital entry points for global commerce, managing a substantial amount of freight and playing a crucial role in worldwide supply networks. The growth of maritime commerce and the larger dimensions of container vessels require ongoing investment in port infrastructure, such as deepening waterways, enlarging terminals, and improving operational effectiveness.

The Inland port segment market is estimated to experience the highest compound annual growth rate during the forecast period. Inland Ports are undergoing swift expansion as advancements in logistics and supply chain management drive their progress. Inland ports are becoming more crucial for enabling the transfer of goods from seaports to inland locations.

To know how our report can help streamline your business, Speak to Analyst

By Construction Mode

Old Port Upgrade Segment Takes the Lead Due to Aging Infrastructure

By construction mode, the market is divided into old port upgrade and new port construct.

The old port upgrade segment is projected to dominates the market share of 63.09% in 2026 and is expected to register the highest CAGR during the forecast period. The segment holds the leading market share, as numerous existing ports undergo major renovations and expansions to support larger ships, boost operational effectiveness, and improve cargo handling abilities. This trend is influenced by various elements, such as an aging infrastructure as numerous ports globally need modernization to satisfy current shipping requirements. Regulatory compliance enhancements are often necessary to align with environmental norms and safety regulations. Technological progress is also a driving factor due to the incorporation of cutting-edge logistics and cargo management technologies that require infrastructure improvements. The segment is set to capture 66% of the market share in 2025.

The new port construct segment market held a significant share in the market in 2024. The sector is expanding, especially in areas undergoing swift economic growth or where current port capacity is inadequate. Factors driving this expansion involve the increase in global trade, with new ports being built to accommodate growing trade volumes, particularly in developing markets. The segment is anticipated to grow with a considerable CAGR of 8.20% during the forecast period (2026-2034).

By Terminal Type

Rising International Trade Activities is Supporting the Intermodal and Container Terminals Segment Growth

Based on terminal type, the market has included intermodal and container terminals, break bulk terminals, dry bulk terminals, and others.

Intermodal and container terminals represent the leading sector in the market. This dominance is mainly attributed to the growing volume of international trade and the emergence of container shipping, which requires effective handling and storage options. The segment is foreseen to grow with a market share of 46.49% in 2026.

The global market for container terminal operations is expected to increase as international trade grows, fueled by technological innovations such as automation and digitalization. The incorporation of intelligent technologies in these terminals improves operational efficiency, making them essential to contemporary supply chains.

Break bulk terminals are witnessing considerable expansion as worldwide trade trends evolve, and there is a growing need for specialized management of non-containerized goods. The growth of sectors such as construction and manufacturing, which depend on break bulk cargo, is prompting investments in this area. Moreover, the demand for improved logistics abilities to handle various cargo types adds to the growth of break bulk terminals.

The dry bulk terminals segment is poised to grow with a substantial CAGR of 7.70% during the forecast period (2026-2034).

Port Construction Market Regional Outlook

Based on geography, the market is studied across North America, Asia Pacific, Europe, and the Rest of the World.

North America

North America Port Construction Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

In 2025, North America generated USD 53.2 billion, contributing 30.44% to global market revenue, and is projected to grow to USD 55.95 billion in 2026, due to its vast network of major ports that enable considerable regional and international commerce. The swift expansion of e-commerce has resulted in a rise in the need for effective port facilities that can manage larger freight capacities. This trend requires capital to enlarge container ports and enhance cargo handling technologies. Government projects and partnerships with the private sector are essential for enhancing port infrastructure developments. These collaborations provide financial support for significant expansions and modernization initiatives, improving the overall capacity and efficiency of ports. The incorporation of cutting-edge technologies in port operations, including automation and digitalization, is further propelling modernization efforts enhancing ports' competitiveness internationally. The U.S. market is set to gain USD 36.54 billion in 2026.

For instance, the Maritime Administration (MARAD) of the U.S. Department of Transportation has announced plans to allocate nearly USD 580 million from the Bipartisan Infrastructure Law for the enhancement of 31 port improvement projects across 15 states and one U.S. territory.

Europe

The Europe market accounted for USD 42.83 billion in 2025, representing 24.51% of the global industry, and is expected to reach USD 45.69 billion in 2026, with Western Europe at the forefront of market size and investment opportunities. The emphasis on enhancing current ports while constructing new ones demonstrates the region's dedication to preserving its competitive advantage in international trade logistics. The U.K. market is projected to reach a market value of USD 11.02 billion in 2026. As intermodal connectivity gains importance, both container and inland terminals are predicted to play a vital role in shaping the future of European ports. Moreover, as global trade dynamics evolve, Europe's ports are positioning themselves as strategic hubs, leveraging their geographic advantages while striving to meet the challenges of climate change and increasing competition from emerging markets. This multifaceted approach strengthens Europe's trade networks and supports economic growth and sustainable development. Germany is expected to hold USD 5.66 billion in 2026, while France is poised to be valued at USD 7.47 billion in 2025.

Asia Pacific

Asia Pacific recorded a market size of USD 47.31 billion in 2025, capturing 27.07% of the global market share, and is projected to reach USD 50.88 billion in 2026. The region is set for major developments in port building, fueled by strong economic expansion and rising global trade. As one of the fastest-expanding regions worldwide, nations such as China, India, and Vietnam are leading the way by making significant investments to upgrade current infrastructure and build new facilities. A key trend in the region is the rapid growth of intermodal and container terminals, which lead the market due to their essential role in promoting global trade. Moreover, the expansion of e-commerce is compelling ports to implement advanced technologies and automation to enhance efficiency.

For instance, China has unveiled a comprehensive plan to boost economic growth in its western provinces, centering on the development of key logistical infrastructure. This initiative encompasses the construction of strategically located ports, airports, and other connectivity hubs in major cities such as Chengdu, Chongqing, and Xi'an. This move seeks to seamlessly integrate various transportation modes, including rail, air, river, and sea routes, enhancing the provinces' connectivity to global markets. The Indonesia market is projected to reach USD 10.09 billion by 2026, the Philippines market is projected to reach USD 8.31 billion by 2026, and the Malaysia market is projected to reach USD 6.28 billion by 2026.

Rest of the World

The Rest of the World market was valued at USD 31.42 billion in 2025, capturing 18.00% of global revenue, and is estimated to reach USD 33.19 billion in 2026. The rest of the world, comprising South America, the Middle East & Africa, held a decent share of the market in 2024. The port infrastructure industry is experiencing significant changes due to rising international trade and the pressing demand for updated infrastructure. As economies in the region acknowledge the strategic role of ports in enhancing trade, significant investments are being allocated to improve current facilities and build new ones. Emerging markets in South America, the Middle East & Africa are also developing their port infrastructure to connect with global supply chains more effectively. The market is characterized by a vibrant landscape, where both mature and emerging economies are emphasizing port development as an essential element of their economic growth plans. This trend highlights the essential importance of ports in worldwide logistics systems, setting the industry up for sustained expansion in the future.

Competitive Landscape

Key Market Players

Key Players in the Market Emphasize Expanding into New Geography to Gain a Competitive Advantage

The global port construction market is fragmented, with many established and emerging players operating in the market. Major players have established their presence in major countries and are focusing on expanding their business in emerging countries. Top 5 key market players in the market include China State Construction Engineering Corporation Ltd., Grupo ACS, Hyundai Engineering and Construction Co. Ltd, DEME Group, and VINCI Construction. Other significant players in the market include Ningbo Zhoushan Port Company Ltd.

List of Key Port Construction Companies Profiled-

- China State Construction Engineering Corporation Ltd. (China)

- Grupo ACS (Spain)

- Hyundai Engineering and Construction Co. Ltd (South Korea)

- DEME Group (Belgium)

- VINCI Construction (France)

- Ningbo Zhoushan Port Company Ltd. (China)

- CK Hutchison Holding Ltd. (Hong Kong)

- Hindustan Construction Company Ltd. (India)

- Van Oord (Netherlands)

- Adani Group (India)

Key Industry Developments

- November 2024 - DEME received a contract for building an offshore wind terminal in the Port of Cuxhaven. This project aimed to strengthen Cuxhaven's status as a vital industrial center for offshore wind energy by enabling the management of heavy loads required for offshore wind farm parts.

- November 2024- Belgium-based DEME secured a contract to build a new offshore wind terminal at the Port of Cuxhaven in Germany. Collaborating with partners Depenbrock and TAGU, DEME would oversee the dredging and land reclamation efforts, with an anticipated reclamation volume exceeding 3 million cubic meters.

- October 2024 - Congo Terminal announced plans for the development of a new container terminal named Congo Terminal 'Môle Est,' which is set to become operational by 2027. The project is part of the company's expansion strategy and would feature 750 meters of quays with a depth of 17 meters, encompassing 26 hectares of quayside area. Additionally, it would be equipped with 16 fully electric gantry cranes, comprising 4 Ship-to-Shore (STS) cranes and 12 Rubber-Tyred Gantry (RTG) cranes.

- September 2024 - Ningbo Zhoushan Port announced plans to increase its container handling capacity by 2 million TEU with a new USD 922 million container terminal. Construction is scheduled to start in October 2025, with completion and commissioning expected by December 2027. The terminal would include two berths designed to accommodate ultra-large containerships, preparing the port for future shipping needs.

- April 2024 - In April 2024, Hyundai E&C gained a contract to build a 1,400-meter breakwater at Jinhae New Port located in Busan. The goal of this project is to integrate advanced construction technologies, employing Building Information Modeling (BIM) for effective risk management while incorporating robotics and AI-driven technology services to improve productivity and quality in the construction process.

Investment Analysis and Opportunities

Rise in International Trade Fuels Market Opportunity

- As global trade continues to rise, countries are investing heavily in building and upgrading their ports to accommodate the growing volume of cargo. This includes the development of new terminals, containerization facilities, and the expansion of existing infrastructure to handle larger vessels and increased cargo volumes.

- For instance, In September 2024, CMA CGM, the world's third-largest shipping group, announced a USD 1.1 billion investment to acquire a 48% stake in Brazilian port terminal operator Santos Brasil. This strategic move aims to enhance CMA CGM's presence in the logistics sector and is expected to lead to a complete takeover valued at over USD 2 billion. The acquisition includes assets such as South America's largest container terminal in the port of Santos.

- In March 2023, COSCO Shipping acquired a 20% stake in the Antwerp Gateway terminal in Belgium. As one of Europe’s largest ports, this investment positions COSCO to bolster its logistics and container operations in a key geopolitical location, improving distribution channels within Europe and expanding its influence in global shipping networks.

Report Coverage

The global port construction market report analyzes the market in-depth and highlights crucial aspects such as prominent companies, market segmentation, competitive landscape, train type, propulsion type, electrification type, and technology adoption. Besides this, the market research report provides insights into the market trends and highlights significant industry developments. In addition to the aspects mentioned earlier, the report encompasses several factors contributing to the market growth over recent years.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

|

ATTRIBUTE |

DETAILS |

|

Study Period |

2021-2034 |

|

Base Year |

2025 |

|

Estimated Year |

2026 |

|

Forecast Period |

2026-2034 |

|

Historical Period |

2021-2024 |

|

Growth Rate |

CAGR of 6.7% from 2026 to 2034 |

|

Unit |

Value (USD Billion) |

|

Segmentation |

Port Type

Construction Mode

Terminal Type

By Region

|

Frequently Asked Questions

Fortune Business Insights says that the market was valued at USD 185.71 billion in 2026 and is anticipated to reach USD 311.97 billion by 2034.

The market will exhibit a CAGR of 6.7% over the forecast period (2026-2034).

By construction mode, the old port upgrade segment dominates the market.

The crucial factors driving the market are the expanding international trade and globalization.

The top players in the market include China State Construction Engineering Corporation Ltd., Grupo ACS, VINCI Construction, Hyundai Engineering and Construction Co. Ltd, and DEME Group.

North America dominated the global market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 182

-

(Offer valid till 15th Aug 2026)

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

Related Reports

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us