Powered Surgical Instruments Market Size, Share & Industry Analysis, By Product (Handpieces {Drills, Saws, Reamers, Shavers/Burs, Wire/Pin Drivers, and Others}, Power & Control Units {Electric Consoles, Pneumatic Regulators, and Battery Packs & Chargers}, Powered Stapling Systems, and Consumables & Accessories), By Application (Orthopedic Surgery, Neurosurgery, ENT Surgery, Cardiothoracic Surgery, Oral & Maxillofacial, and Others), By End-user (Hospitals & ASCs, Specialty Clinics, and Others), and Regional Forecast, 2026-2034

Powered Surgical Instruments Market Size and Future Outlook

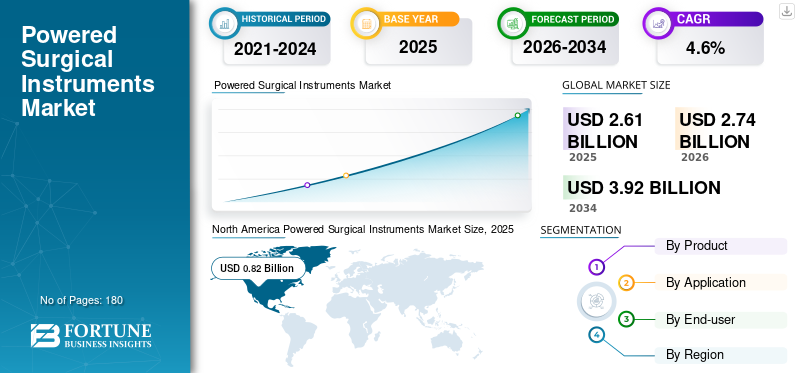

The global powered surgical instruments market size was valued at USD 2.61 billion in 2025. The market is projected to grow from USD 2.74 billion in 2026 to USD 3.92 billion by 2034, exhibiting a CAGR of 4.6% during the forecast period. North America dominated the global powered surgical instruments market with a market share of 31.42% in 2025.

Powered surgical instruments are advanced medical tools powered by electricity, batteries, compressed air, or ultrasound to help surgeons cut, drill, shape, or remove bone and tissue with precision during surgeries. These tools enables faster and more accurate surgical procedures compared to manual tools, while minimizing damage to the body. The growth of the market is supported by rising demand for minimally invasive surgeries, where these tools enable smaller incisions, quicker recovery, and better outcomes, fueling their adoption.

Furthermore, Medtronic, Stryker, and Johnson & Johnson Services, Inc. held the highest market share due to their significant product offerings and focus on strategic decisions to expand their business.

Download Free sample to learn more about this report.

Powered Surgical Instruments Market KEY TAKEAWAYS

- 2025 Market Size: USD 2.61 billion

- 2026 Market Size: 2.74 billion

- 2034 Forecast Market Size: USD 3.92 billion

- CAGR: 4.6% from 2026–2034

- North America dominated the market with a 31.42% share in 2025.

- Hospitals & ASCs segment is projected to hold a 67.2% share in 2026.

- Orthopedic surgery segment is projected to hold a 33.3% share in 2026.

North America

North America USD 0.82 billion in 2025. Strong presence of key players in the U.S. and Canada and rising number of ASCs increasing surgical volumes and instrument demand.

Europe

Europe USD 0.71 billion in 2026. Well-established healthcare infrastructure supporting higher surgical volumes and demand for powered surgical instruments.

Asia Pacific

Asia Pacific USD 0.67 billion in 2026. Large patient pool for orthopedic and cardiovascular disorders driving surgical demand for powered surgical instruments.

U.S.

U.S. USD 0.79 billion in 2026. Increasing adoption of ASCs and strong surgical ecosystem driving demand for powered surgical instruments.

Japan

Japan USD 0.23 billion in 2026. Advanced healthcare system and rising demand for surgical procedures supporting market growth.

Read More

POWERED SURGICAL INSTRUMENTS MARKET TRENDS

Shift Toward Battery-Powered and Cordless Systems to Emerge as a Key Trend

Currently, there has been an increasing adoption of battery-powered and cordless surgical instruments, which improve mobility in the operating room, reduce cable clutter, and enhance surgeon comfort. Moreover, battery technology improvements allow for longer operating times and faster recharging. Also, several companies are focusing on ergonomic design and lightweight handpieces to enhance the overall operating scenario.

- For instance, Arthrex, Inc. launched Synergy Power, a battery-powered orthopedic system featuring an ergonomic sagittal saw and a dual-trigger rotary drill for procedures in arthroplasty, sports, trauma, and the distal extremities.

Download Free sample to learn more about this report.

MARKET DYNAMICS

MARKET DRIVERS

Rising Volume of Key Surgeries to Fuel the Market Expansion

In recent years, there has been an increasing number of orthopedic and trauma surgeries worldwide, driven by joint degeneration, fractures, spinal disorders, and sports injuries. This is driving the need for precise bone cutting and drilling, which powered instruments handle efficiently. Such a scenario is anticipated to drive the global powered surgical instruments market growth during the forecast period.

- For instance, in October 2022, the Centers for Advanced Orthopedics mentioned that around 800,000 knee replacements are conducted annually in the U.S.

MARKET RESTRAINTS

High Cost of Devices and Maintenance to Restrict Market Growth

Powered surgical systems require expensive handpieces, batteries, and consoles, and also require regular servicing. Smaller hospitals and clinics, especially in low- and middle-income countries, often struggle with such constraints.

As a result, these facilities prefer manual instruments, limiting the adoption of powered surgical instruments, which is anticipated to hinder the market growth over the forecast period.

MARKET OPPORTUNITIES

Growth of Minimally Invasive and Outpatient Surgeries to Create Significant Growth Opportunities

In recent years, the growing demand for minimally invasive procedures has heightened the need for compact, efficient, and high-speed instruments that enable surgeons to work through smaller incisions. Moreover, an increasing number of outpatient departments are creating significant demand for portable, battery-powered systems, which are expected to offer key players significant opportunities for innovation.

- For instance, in December 2021, DePuy Synthes, part of Johnson & Johnson Services, Inc., launched the UNIUM System, a next-generation power tools platform optimized for trauma procedures.

MARKET CHALLENGES

Device Reliability and Sterilization Issues to Challenge Market Expansion

Powered surgical tools operate under high mechanical stress and must function consistently during long procedures. Any malfunction is expected to delay surgery and increase patient risk.

Moreover, complex instrument designs make cleaning and sterilization more difficult, which is why hospitals are required to follow reprocessing protocols strictly to avoid infection risks. Such a scenario is anticipated to challenge the market expansion.

Segmentation Analysis

By Product

Primary Usage of Handpieces in Drilling and Reaming to Boost Segment’s Growth

Based on product, the market is segmented into handpieces, power & control units, powered stapling systems, and consumables & accessories. Furthermore, the handpieces segment is further sub-segmented into drills, saws, reamers, shavers/burs, wire/pin drivers, and others. On the other hand, the power & control units are sub-divided into electric consoles, pneumatic regulators, and battery packs & chargers.

The handpieces segment accounted for the largest global powered surgical instruments market share in 2025, as they are the primary interface between the surgeon and the device, used across multiple procedures such as drilling, sawing, and reaming. As a result, companies are continuously upgrading their handpiece products, which is anticipated to drive the segment’s growth.

Additionally, the power & control units segment is projected to grow at a 5.0% CAGR during the forecast period.

To know how our report can help streamline your business, Speak to Analyst

By Application

Increasing Number of Key Orthopedic Procedures to Fuel the Segment’s Growth

By application, the market is segmented into orthopedic surgery, neurosurgery, ENT surgery, cardiothoracic surgery, oral & maxillofacial, and others.

The orthopedic surgery segment accounted for the largest market share in 2025. Over the past few years, there has been an increasing number of joint replacements, trauma fixation, and spine surgeries, which has been driving the use of drills, saws, and reamers. Moreover, the segment is estimated to hold a 33.3% share in 2026.

- For instance, in June 2025, PMG Hospital stated that over 200,000 knee replacement procedures are performed annually in India.

Additionally, the cardiothoracic surgery segment is anticipated to grow at a CAGR of 4.2% over the forecast period.

By End-user

Rising Number of Hospitals Globally is Pushing the Dominance of Hospitals & ASCs Segment

On the basis of end-user, the market is segmented into hospitals & ASCs, specialty clinics, and others.

In 2025, hospitals & ASCs dominated the market as end users. These facilities handle complex orthopedic, trauma, and neurosurgical procedures that require reliable powered instruments. ASCs, in particular, are driving demand for compact and battery-powered systems. As a result, growing number of hospitals & ASCs are projected to fuel the segment’s growth. Furthermore, the segment is set to hold a 67.2% share in 2026.

- For instance, according to the American Hospital Association (AHA) Fast Facts on Hospitals, the US had 6,093 hospitals in total as of early 2025.

In addition, the specialty clinics segment is projected to grow at a 4.9% CAGR over the forecast period.

Powered Surgical Instruments Market Regional Outlook

Based on geography, the market is classified into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

North America

North America Powered Surgical Instruments Market Size, 2025 (USD Billion)

To get more information on the regional analysis of this market, Download Free sample

North America accounted for the largest share of revenues in 2024, valued at USD 0.78 billion, and reached USD 0.82 billion by 2025. The growth is attributed to the strong presence of key players in the U.S. and Canada and to increasing number of ASCs, which are supporting the number of surgeries performed, thereby driving demand for powered surgical instruments.

- For instance, according to the data from the Ambulatory Surgery Center Association in March 2025, there are over 6,500 Medicare-certified ASCs in the U.S.

U.S. Powered Surgical Instruments Market

In 2026, the U.S. is projected to reach USD 0.79 billion, accounting for approximately 28.9% of the global market.

Europe

Europe is projected to record a 4.1% growth rate during the projection period, the second-highest globally, reaching USD 0.71 billion by 2026. The growth is attributed to the well-established healthcare infrastructure, which is favoring surgical volume and driving demand for powered surgical instruments.

U.K Powered Surgical Instruments Market

The U.K. market is expected to reach USD 0.09 billion by 2026, accounting for roughly 3.3% of global revenues.

Germany Powered Surgical Instruments Market

Germany's market is projected to reach USD 0.19 billion by 2026, accounting for approximately 6.8% of global revenue.

Asia Pacific

By 2026, the Asia Pacific's market is expected to reach USD 0.67 billion, ranking third globally. The growth is attributed to the large patient pool for orthopedic and cardiovascular disorders, which often require surgery and are expected to drive demand for powered surgical instruments.

Japan Powered Surgical Instruments Market

Japan is forecasted to generate USD 0.23 billion in revenue by 2026, capturing nearly 8.4% of the global market.

China Powered Surgical Instruments Market

China’s market is expected to reach approximately USD 0.24 billion by 2026, representing nearly 8.7% of global revenues.

India Powered Surgical Instruments Market

India’s market is expected to reach approximately USD 0.09 billion by 2026, accounting for around 3.1% of global market revenue.

Latin America and Middle East & Africa

Both Latin America and the Middle East & Africa are expected to showcase moderate growth, with Latin America market predicted to reach USD 0.41 billion by 2026. The growth of these regions is attributed to increasing healthcare expenditure and government initiatives to develop the infrastructure supporting the adoption of such instruments.

GCC Powered Surgical Instruments Market

By 2026, the GCC market is estimated to reach approximately USD 0.04 billion, representing around 1.4% of global revenues.

COMPETITIVE LANDSCAPE

Key Industry Players

Strong Brand Reputation and Diversified Portfolios to Strengthen the Market Positions of Key Players

In 2025, Medtronic, Stryker, and Johnson & Johnson Services, Inc. held the majority of the global powered surgical instruments market share. This share is attributed to their broad portfolios and strong brand reputation, which is enhancing their competitive positions.

Moreover, other prominent players are implementing strategic initiatives, such as collaborations and partnerships, as well as geographic expansions, to enhance their market share in the coming years.

LIST OF KEY POWERED SURGICAL INSTRUMENTS MARKET COMPANIES PROFILED

- Medtronic (Switzerland)

- Stryker (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- CONMED Corporation (U.S.)

- Zimmer Biomet (U.S.)

- Braun SE (Germany)

- Smith+Nephew (U.K.)

- adeor medical AG (Germany)

- MicroAire (U.S.)

- De Soutter Medical (U.K.)

KEY INDUSTRY DEVELOPMENTS

- December 2025: Medtronic secured FDA clearance for its Hugo Robotic-Assisted Surgery (RAS) system in urologic procedures, including prostatectomy, nephrectomy, and cystectomy, representing about 230,000 annual U.S. surgeries.

- December 2025: Apyx Medical Corporation received FDA 510(k) clearance for its AYON Body Contouring System, the first all-in-one aesthetic surgical platform integrating Renuvion helium plasma technology.

- October 2025: Medtronic launched two advanced electrosurgical devices in India, the Valleylab FT10 Electrosurgical Generator and Valleylab FT10 Vessel Sealing Generator, featuring TissueFect sensing technology for automatic energy adjustment based on tissue type.

- March 2025: Olympus Corporation launched its first AI-powered surgical planning tool, developed in partnership with Ziosoft, integrating imaging analytics and machine learning for pre-op 3D modeling in thoracic, liver, and urologic procedures.

- March 2025: Smith+Nephew showcased advanced orthopedic reconstruction technologies at AAOS 2025, including the CORI Surgical System with CORIOGRAPH pre-op planning for personalized robotics in knee/hip procedures and the CORI Digital Tensioner for precise gap balancing.

- June 2024: Zimmer Biomet has partnered with THINK Surgical to introduce the TMINI, a compact handheld robotic system designed for total knee arthroplasty procedures.

- June 2023: GE HealthCare and DePuy Synthes announced a U.S. distribution partnership to pair GE's OEC 3D Imaging System with DePuy's product portfolio, enhancing precision imaging for complex spine surgeries in acute and outpatient settings.

REPORT COVERAGE

The powered surgical instruments market report delivers in-depth analysis across all market segments, covering drivers, trends, opportunities, restraints, and challenges influencing the landscape. It also offers key insights on technological advancements, key surgical procedure volumes, industry developments, market share analysis, and detailed company profiles.

Request for Customization to gain extensive market insights.

Report Scope & Segmentation

| ATTRIBUTE | DETAILS |

| Study Period | 2021-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2021-2024 |

| Growth Rate | CAGR of 4.6% from 2026-2034 |

| Unit | Value (USD Billion) |

| Segmentation | By Product, Application, End-user, and Region |

| By Product |

|

| By Application |

|

| By End-user |

|

| By Region |

|

Frequently Asked Questions

Fortune Business Insights says that the global market value stood at USD 2.61 billion in 2025 and is projected to reach USD 3.92 billion by 2034.

In 2025, the market value stood at USD 0.82 billion.

The market is expected to grow at a CAGR of 4.6% over the forecast period.

The handpieces segment led the market, by product.

The key factor driving the market is the rising volume of key surgical procedures.

Medtronic, Stryker, and Johnson & Johnson Services, Inc. are among the prominent players in the market.

North America dominated the market in 2025.

- 2021-2034

- 2025

- 2021-2024

- 180

Get 30-60 hrs Free Customization

Expand Regional and Country Coverage, Segments Analysis, Company Profiles, Competitive Benchmarking, and End-user Insights.

-

US +1 833 909 2966 ( Toll Free )

-

Get In Touch With Us